Several months after going public with his plan for really large increases in capital requirements for locally-incorporated banks, and apparently feeling under a bit of pressure, the Governor of the Reserve Bank selected some foreign academics – anyone local, he claimed, had been bought and paid for – to each write a report on aspects of the multi-year bank capital review. I wrote here about the appointments, the terms of references the three selected people were working to, and what we might reasonably expect from them.

Their role was tightly-drawn, wasn’t primarily focused on the current (most contentious consultation), and they were only supposed to talk to anyone outside the Bank with the advance approval of the Reserve Bank. Their focus was supposed to be on the Bank’s documents, not on (for example) the submissions the Bank had received in response. And while there was talk of looking at the New Zealand specific context, none of the invited academics had any particular knowledge or, or background in, New Zealand.

This is what I wrote about what we might expect

I’m not impugning the integrity of the independent experts. But they have been chosen by the Governor, having regard to their backgrounds, dispositions, and past research – a different group, with different backgrounds etc, would reach different conclusions – and the Governor is well-known for not encouraging or welcoming debate, challenge or dissent. Quite probably the experts, each working individually, will identify a few things the Bank could have done better, but it will all be very abstract, ungrounded in the specifics of New Zealand, and the value of their reports is seriously undermined in advanced because of who made the appointment, and the point in the process where the appointment was made. This is the sort of panel that, at very least, should have been appointed a year ago. Better still, it would not have been appointed by the Governor.

The three reports were released a few weeks ago and the visitors pretty much delivered for the Bank – as, no doubt, having carefully selected them, the Bank was pretty sure they would. There were, as I suggested, a few apt suggestions and questions but very little sustained engagement with the deeper issues, with the New Zealand context, or with the process. The experts appear to have been let out to talk to a few (commercial bank) people outside the Reserve Bank but – as per their terms of reference – there is no sign of systematic engagement with the range of expert submissions or submitters. One declared himself comfortable that the Bank had answers to all the points raised by submitters, which may have been comforting for him but – and this report was written months ago – not so much for New Zealanders who’ve had no engagement from the Bank.

A Bank summary of the three report is here. The Bank has claimed full-throated endorsement from the experts they selected. Personally, I was a bit surprised how limited the reports were: offering more support (from people already strongly disposed to think more capital “a good thing”) than illumination.

I’m going to step through the reports one by one but I’m only going to talk about their comments on the current consultation on the minimum level of bank capital (for some – and reasonably enough given the terms of reference – that makes up only a fairly small portion of the report).

The first of three was by James Cummings, now of Macquarie University and formerly a researcher at APRA. His report was quite long, but there wasn’t much insight offered relevant to the current consultation. There is a lot of reportage. For example, he simply channels – without examining – the Reserve Bank’s claim about the greater vulnerability of New Zealand. And despite being (a) Australian, and (b) previously from APRA he offers no thoughts on how robust the case might be for minimum core capital ratios here being material higher than those in Australia. Then again, neither has the Reserve Bank. There is no discussion about the trans-Tasman nature of the big four banks and the possible implications for the design of a sensible capital regime. He mentions the Bank’s stress tests but – again simply, and briefly, channelling the Bank – to downplay them.

Cummings makes what appears to be a reasonable point that the Bank may have over-estimated the cost of equity in the Australasian banking sector (I presume that is one of the points the Bank will be having a look at). But that is really about all the value he adds on the current consultation. He is clearly highly sympathetic to the idea of the Australian banks listing their New Zealand subsidiaries locally and reducing their 100 per cent ownership of the subsidiaries. That will have been music to the ears of Messrs Orr and Bascand – Orr in particular appears to have been pursuing that outcome as some sort of “New Zealand nationalist” goal, quite unrelated to his statutory mandate. Cummings is correct that issuing equity locally could get round the fact that the imputation regime, although operating domestically in both New Zealand and Australia, doesn’t operate trans-Tasman. But he doesn’t engage at all with the likely costs to selling down ownership and local listing (if they were non-existent, for example, the tax argument might already have led to partial local floats of the subsidiaries). Those costs might well include a less strong ability to rely on the parent in the event of a crisis. You’ll recall that really serious crises are supposed to be the focus of the capital review.

The second report is by David Miles of Imperial College, London (who spent a term on the Bank of England’s Monetary Policy Committee). Miles has published some past research (unsurprisingly, given his selection) pretty sympathetic to higher capital ratios. His (shorter) report is almost entirely focused on the current consultation.

He appears keen to be supportive of the Bank, and he begins his report by pushing back against the claim – made by various critics – that the Governor’s 1 in 200 year risk appetite stake in the ground was really just plucked out of the air. And yet the Bank itself released a paper – dated a mere six weeks before the release of the Bank’s proposals – written by one of their internal experts, which adds the 1 in 200 year risk appetite possibility (ie a 0.5 per cent annual probability of crisis) almost as an afterthought.

Presumably the Governor latched onto 1 in 200 and they were off. Much of the subsequent supporting analysis and modelling was only done, and released, after the Governor had already nailed his colours to the mast and published his radical plans.

Miles is actually somewhat sceptical about several of the assumptions the Bank has made in its modelling, and Ian Harrison – expert submitter on the modelling etc who neither Miles nor the others show any sign of having engaged with – plausibly argues that Miles show signs of not fully understanding the modelling framework and thus being less critical than he should be. One of the parameters (R, around correlations) was based on a particularly shoddy piece of “analysis” – Miles, being more diplomatic, observes simply “but this evidence is quite weak and not a firm basis to be confident that a higher value of R [than used conventionally] is justified.”.

By background, Miles is a macroeconomist and you might therefore have supposed that he would something insightful to offer around the scale (in GDP terms) of the sort of severe crisis the Governor’s plans are designed to avoid. The Bank uses quite a high number – 63 per cent of GDP – in turn based on remarkably little analysis (several sentences in this paper). Miles reckons this is quite possibly a “serious underestimate” and “seems optimistic”. His argument for this appear to rest on nothing more (you can check – page 14 of his paper) than a thought experiment in which he posits the possibility that the entire extent to which UK GDP now is below the pre-2008 trend is a) all due to a financial crisis, and (b) permanent then the cost of crisis might be 330 per cent of GDP. As indeed it might, but Miles provides no discussion for why we should interpret even UK GDP that way, no mechanism for how these huge effects (more costly than World War Two?) might arise, no distinction between GDP lost because of poor lending and borrowing in the boom (costs which crystallise later) and those actually related to the banking crisis itself, and no engagement with (for example) comparisons between the output paths of countries which had financial crises with those that did not. I’ve argued – it was in my submission – that something more like 10-20 per cent of GDP might well be more reasonable.

You might also have supposed that the macroeconomist among the experts might also thought about discount rates. As we typically have the highest real long-term interest rates among advanced countries, the appropriate long-term discount rate here should also be higher (making taking insurance against even a costly future crisis rather less valuable than it might be in some other countries). Even the Reserve Bank noted that point (even if it changed nothing in their analysis) but not the Bank’s macroeconomic expert adviser.

Miles’s offering is pretty abstract and doesn’t engage with the specifics of New Zealand (or the trans-Tasman nature of our large banks) much at all (although he does note the difficulty the Governor’s proposal may pose for our capital-constrained local banks). Given his background, that isn’t really surprising – and is more a reflection on the Bank than on him.

But a couple of his concluding remarks are worth highlighting. He is quite dismissive of the issue that I and others have raised as to whether there is a robust case for setting New Zealand core capital requirements so much higher than those in Australia or than in most other advanced countries. There is, in his view, no information value whatever in such judgements by other authorities, when set against a “careful” Reserve Bank of New Zealand analysis. That analysis really should pose questions not for New Zealand citizens etc but for other countries, who perhaps just haven’t done enough of the Bank’s sort of analysis. He makes a fair point that we don’t want the same speed limits on all roads – it depends on the risk – but offers not a scintilla of reason to suppose that macroeconomic risks, and exposure to severe shocks, is more severe in New Zealand than elsewhere.

And then there is his final, distinctly two-handed, defence of the Bank’s stance. As far as I’ve seen, his final – perhaps delicately worded – swipe at the New Zealand regime has had no coverage. Here is what he has to say.

The RBNZ has adopted a principle of being conservative as regards bank capital to offset possible risks from its light-handed approach to supervision. That is a choice and one partly based on the view that having very large resources devoted to intrusive oversight of banks is not the most efficient road to go down. That is a conclusion that engineers and safety experts often apply when dealing with the design of structures. There is a choice between building bridges many times stronger than you expect them to need to be OR you having large teams of inspectors who pay frequent visits to examine all bridges and monitor flows of traffic over them. It is clear that nearly all countries follow the first strategy.

That may be a useful guide for bank supervision.

[UPDATE: Rereading this years later, I think I misinterpreted Miles on this point.]

Ouch. On the Reserve Bank’s own numbers, the Governor’s capital proposals involve an annual loss of GDP of $750 million. You could buy a really large (by New Zealand standards) number of new bank supervisors and regulators for even a 10th of that amount. I’m sceptical there even is much of that sort of trade-off in New Zealand, at least for the big 4 banks, given that they are, in effect, subject to APRA’s own more hands-on supervision. But 30 more supervisors might be cheap compared to the costs and distortions of the Governor’s current proposal – even allowing for the old maxim, about the devil making work for idle hands.

It was striking that neither Miles nor Cummings devoted any space at all to the sectoral and distributional effects of what the Governor is proposing – and thus did not point out that the Bank’s consultation papers have not done so either. Thus, no mention of the fact that the rules would apply to locally-incorporated banks, but not to (a) other banks, (b) non-banks, whether deposit-takers or otherwise, or (c) to market-based funding mechanisms (eg securitisations or bond finance directly). Or, thus, that the burden of the policy will fall very unevenly – those with easy access to alternative sources of finance will face no material impact at all, and those without could be hit quite severely (whether in terms of cost, credit standards, or competition among credit providers).

The third of the experts, Ross Levine, a US academic – with no particular background in policymaking or bank regulation, but with an impressive publications record across a range of areas – does touch on alternative sources of finance. Indeed, it is one of the main themes of what is really an essay on incentives, risk-taking and so. It is quite a thoughtful essay – with some suggestions of issues the Bank might have discussed but didn’t – but it isn’t really clear what bearing it has on the merits of the Governor’s proposals or the quality of the analysis and argumentation supporting them.

Levine’s deep conviction is that banks are heavily subsidised, prone to recklessness, and that anything that reins them in, reducing their relative importance, is prima facie a good thing. Those aren’t his exact words, but a paraphrase they seem to capture his view pretty well. Well, fine, but some evidence would be nice, perhaps especially when you are dealing with (a) a pretty vanilla banking system, (b) in a country largely free of a track record of serious systemic financial crises, and (c) where the country’s vanilla banking system is owned by banks based in, supervised in, another country with a similarly strong track record of financial stability. Remarkably, despite the focus on issues around incentives, Levine does not discuss at all how his thinking about the issues facing New Zealand might be affected by the fact that the big 4 banks are themselves owned by other (foreign) banks, subject to group capital requirements. He suggests the Bank should assess some of these issues – and it is a fair enough criticism that it hasn’t – but offers no perspectives of his own. If the New Zealand subs remain wholly owned by the parents, for example, it is unlikely that any New Zealand capital requirement policies will affect the incentives on managers of the New Zealand operations, who operate largely as part of wider banking groups.

Because Levine is keen on a reduced reliance on banks, he thinks the Reserve Bank should have put more weight on how non-banks might respond. He is keen that they should do so but it isn’t clear if he is aware that (a) the last (small) financial crisis in New Zealand was among non-banks or (b) that non-banks are subject to a lighter (materially so if the Orr proposal proceeds) regulatory regime than banks. Nor, it seems, has he given much thought to the implications of potential bank lenders not covered by the proposed new requirements.

His conviction is that banks are heavily subsidised and thus that capital requirements are generally too low. But he shows no sign of having engaged with, for example, indications regarding the sort of capital ratios found to work (for shareholders and creditors) in financial intermediaries where there is no credible prospect of a government bailout. I touched on this in a post earlier in the year: as yet, we have no deposit insurance, and yet TSB, Heartland, and SBS each operate with actual risk-weighted total capital ratios of around 14 per cent. while the Governor wants to insist on 16 per cent minimum core capital ratios for the big 4 banks. But I guess that sort of perspective would muddy the rhetorical story.

Levine doesn’t get into at all the issues around the actual economic cost of crises, the marginal reductions in those costs from the last few percentage points of capital requirements, discount rates or the myriad of other relevant angles. In fairness, he claims not to be taking a strong view on whether what the Governor is proposing is too high or too low, but his priors pervade his paper – priors the Bank knew very well when they hired him.

The reviewers reports are generally pretty positive on the Reserve Bank analytical staff involved in the technical aspects of this project. That is good, but not particularly surprising or new. The issues here are more about senior management – the Governor in particular – and reluctance to engage more broadly or on a wide range of angles and perspectives. The Governor has recently been attempting to deflect criticism of him by suggesting it is all about his staff – “you are all beating up on my wonderful staff” – when no one is criticising them much if at all. Staff have to deliver for senior management, and the Bank’s technical staff seem to have done the best they could to provide support for the Governor’s whims and priors. It is the Governor and senior management colleagues who refuse to engage, refuse to look wider, and fail to provide any sort of robust defence of a proposal to impose much higher core capital requirements here than in most other places and, in particular than in Australia.

As I said at the start, for handpicked reviewers, chosen at a time when the Governor had already put his stake in the ground, the reports were much what one should have expected. The Bank seems to have taken the reports as reassuring support – but that is why they hired these particular people, known for particular predispositions – but I suggest you don’t. Many of the bigger picture questions simply haven’t been engaged with, adequately or at all.

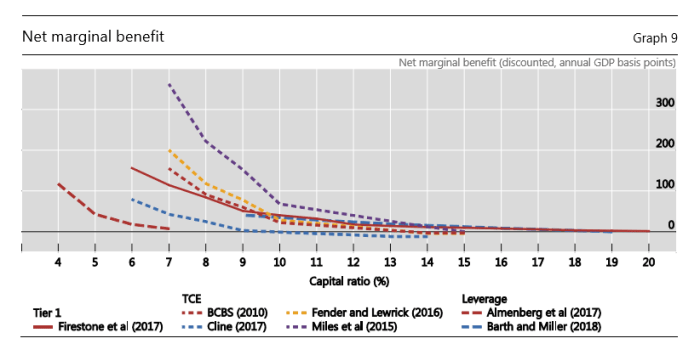

And, somewhat to my surprise, I didn’t see any mention at all of the paper that came out three months ago, from a working group of major central banks, looking at issues around appropriate minimum capital requirements, working within the academic framework these reviewers are comfortable with. I discussed that paper here and highlighted this chart and these issues

On my reading, this is the bottom line chart in the BCBS paper.

They report the net marginal economic benefit (slightly lower GDP each year, offset against savings from a less serious crisis decades hence) from higher bank capital ratios, drawn from a series of studies. On these models there were really big gains in lifting capital ratios, up to around to around 9-10 per cent. If there are gains at all – and they don’t report margins of error around these estimates – they are looking extremely small beyond about 13 per cent. Perhaps that doesn’t sound too far from the 16 per cent number the Reserve Bank is proposing for the big banks but (among other limitations, many made inevitable by data limitations):

- this modelling is done on actual capital ratios, not regulatory minima (a 16 per cent minimum ratio is likely to see banks aim for something between 17 and 18 per cent actual ratio), and

- none of this modelling takes account of differences in accounting and regulatory treatment across countries: conventional wisdom, (backed by estimates done by PWC) suggest that effective capital ratios in New Zealand (and Australia) would be far higher if things were measured the same way they were done in various other advanced countries, and

- none of it takes account of the regulatory floor in how risk-weighted assets are calculated. As the Bank is quite open about, a significant part of what is proposing is that in calculating risk-weighted assets, the big banks will have a floor of 90 per cent of what the standardised rules would generate (the more normal floor is, as I understand it, about 72 per cent). A 17.5 per cent headline actual capital ratio would, on RB proposed rules, be akin to something like 20 per cent in the sort of framework the BCBS authors are looking at.

Nothing in this paper suggests any reason for confidence that effective capital ratios of, say, 20 per cent of risk-weighted assets would be generating net economic benefits, even on the (overly pessimistic) macro assumptions the authors are using. But that is what the Reserve Bank claims to believe. The onus, surely, is on them to show us, and to engage on their assumptions and analysis – in open dialogue – well before decisions are made.

There were other problems in this paper – for example, to my reading of the experiences of other countries they use too-high estimates of the cost of crises – but those will do to be going on with. Neither the Bank nor their independent reviewers have engaged with the challenges this paper – not by some lone academic or iconoclast, but from within the hallowed halls of central bankers and supervisors – poses to the Governor’s plans.

Cumming is not any longer at MC he is a Lecturer at University of Sydney.

LikeLike