A post on the Annual Report of the Reserve Bank’s Board has become something of an annual event here (here was last year’s). The Bank’s Board is charged by statute with holding to account the Governor (and now the MPC) on behalf of the public and the Minister of Finance. Almost throughout their history, they’ve almost entirely abdicated that responsibility, acting as if their prime responsibility is to support and provide cover for the Governor. Of course, they are compromised because they play a key role (unelected and unaccountable as they themselves are) in appointing this key policymaker, and so – with no other real role – it is perhaps little wonder that they been duchessed. It doesn’t help that the Governor himself sits on the Board, a Bank staffer acts as secretary, and the Board has no independent resources or (for example) analytical support. They aren’t paid very much and all seem to have pretty much settled for the easy life and whatever mild prestige seems to attach to the Reserve Bank Board. It wasn’t always the approach of the current chair – when he wasn’t chair – but since getting to the top of the greasy pole a few years ago, he is now much the same as his predecessors.

It is a deeply flawed model, and by now pretty much everyone seems to recognise it. The Minister of Finance has made an “in-principle” decision, as part of the Reserve Bank Act review, to turn the Board into a conventional decisionmaking body, but there is quite a way to run until any such decision becomes law, and in the meantime in this year’s Annual Report the Board has chosen to do us a public service by reminding us just how willingly useless they are in the monitoring and accountability role.

But before getting into the substance of the Board’s report, there are a couple of snippets worth noting from Bank management (ie the Governor’s) own report and supporting press release.

I’ve already drawn attention on Twitter to this startling claim from Monday’s press release (so he can’t even blame publication lags).

The New Zealand economy has proved resilient through a period of weakening global growth and heightened global uncertainty according to the Reserve Bank’s Annual Report 2018-19 released today.

Not much better than pure spin, but no doubt welcome in the Beehive.

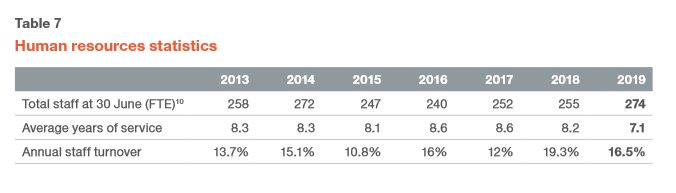

Then there was this table

Another year of really high staff turnover, if a little lower than the previous year. Rarely a particular positive commentary on the way an organisation of this sort is being run, and all of the 2019 year was on Adrian Orr’s watch (and the people I happen to know who’ve left over the past year were typically very able).

And this quote

We’re committed to promoting a diverse, inclusive and forward-thinking economic and financial system for all New Zealand.

As one reader notes, a backward-thinking economic and financial system might be one that learns from history and experience, rather than pursuing ideological agendas. Most financial institutions that have failed badly thought they were being innovative, forward-thinking etc.

But my real objection here is that it simply not the role of the Reserve Bank to promote, shape, champion, any particular type of economy or financial system, whether for “all New Zealand” or otherwise. The Reserve Bank is a statutory body, given access to scarce taxpayer resources to pursue specific statutory responsibilities. Those are largely about monetary policy and financial system soundness. The trendy mantra of the left (“diversity and inclusion”) is simply none of the Reserve Bank’s business when it comes to any organisation than its own. Nor is the shape of the “ecnomic and financial system”. No doubt the Governor has personal ideological and political agendas, perhaps suppported by many of his political and big business mates. But it is not his job. He has no authority to spend our money to promote his agendas. It really should be Public Management 101. But no doubt it suits the Minister of Finance to have an ideological ally championing Labour/Greens type causes at public expense.

What of the Board’s Annual Report? The usual process criticisms can be logged. The report is buried in the middle of Bank management’s report, and there is no press release from the Board chair, or even mention of the independent Board Annual Report in the Governor’s press release. Which really rather gives the game away.

When I first started writing these posts, the Board’s report was very short. It has grown again this year, and is now eight pages of text (pages 6-13 here). Last year I gave the Board’s report a moderately favourable rating (“bare pass”) but no matter how many more words they churn out, this year in substance they seem to have reverted to form. I guess last year it was easy: the old Governor (and the unlawful acting Governor) had just gone, and the new man had been in office for only three months. The mildly useful comments related to what had gone before Orr, and those responsible had already left.

Just a few specific points that caught my eye in this year’s report.

As I noted, the Minister of Finance has made an in-principle decision to change the role of the Board

Together with the Governors, we supported the proposal to adopt a governance model for the Bank that will provide more standard powers and clearer responsibilities for the Board. Directors have begun to consider the corporate governance processes, including Board meeting agendas, risk appetite statements, agreed cycles for strategic planning and formal management delegations that will be required as these in-principle decisions are implemented.

That seems a little surprising given that (a) it is only an in-principle decision, (b) an election is only a year away and it would be surprising if any serious changes were legislated in this government’s term (given the various consultation documents still to come) and (c) the second terms of both the chair and deputy chair expire in four months from now, and (d) one might reasonably imagine a government might want different types of people on a decision-making Board than on the sort of Board we notionally have at present. Surely there would be plenty of time to do all this process stuff when, say, a bill is before Parliament? Most probably though, this is the sort of stuff the Board members might be good at (corporate board processes), unlike the role they are actually currently charged with.

Then there was monetary policy, until March the primary statutory function of the Bank. You’d get no idea from the Board’s report that core inflation has been running below the target midpoint (focal point in successive agreements) for eight years, or that the Bank had again been misjudging policy and inflation pressures. The other worrying note about monetary policy was this

With the external members of the MPC now having the primary responsibility to undertake external scrutiny of the research and formulation of monetary policy,

But they simply don’t have that role. The external members of the MPC aren’t supposed to be external reviewers, but full participants in the process of formulating and communicating monetary policy. And isn’t it extraordinary that the Board would claim to look to external MPC members when the Board itself, in agreement with the Minister, disqualified for consideration of membership of the MPC anyone who actually had any research interests – past, present, or future – in monetary policy or macroeconomics.

That was a truly weird decision in the first place, for which they and Grant Robertson should be held accountable, but then to try to suggest that having excluded research-qualifed people from the MPC, the actual appointees were responsible for providing external scrutiny of research……well, it is like some topsy-turvy Alice-in-Wonderland world.

What of some of the other things they write about?

Last year, the Board was so bold as to note that bank conduct issues were really more a matter for the FMA. But the Governor has them properly corralled again this year

We believe it is appropriate for the Bank to be concerned about inappropriate cultures and behaviours in regulated institutions. Poor conduct affecting customers can be symptomatic of governance problems and can adversely affect confidence in the New Zealand financial system.

Do note those “can”s: the way is opened to a great deal of regulatory over-reach there. If the chief executive is having marital problems it probably won’t be great for the bank either, but we don’t want the Reserve Bank undertaking fishing expeditions in those areas either.

Of CBL, last year they defended the Bank’s handling of the affair. This year they were back, still only slightly abashed, and still claiming it was nothing to do with the Bank that shareholders weren’t informed (in fact, the Bank barred directors from telling shareholders). They are there with management all the way – which might even be appropriate in a decisionmaking Board, but this Board is supposed to stand at arms-length.

There were the almost comical bits

We have supported the development of the Bank’s Te Ao Mäori strategy, including through the integration of tikanga Mäori into our own meetings.

Never mind any serious scrutiny – including of the questionable and expensive Maori strategy (tree gods anyone?) itself – but we’ll do something Maori in our meetings.

And the one area they could be seen as somewhat critical relates to a IT project that appears to have gone wrong, but which had already been scrapped by management

The trade valuation system has been unsuccessful and has been terminated. We were kept fully informed about the problems with the development of this system and supported the move to avoid compounding the problems by further investment. The lessons learned from the ex post project review, including the need for deeper due diligence at the outset, stronger stage-gating of the project, and appropriate resourcing of the procurement and contract management function, have already been reflected in Bank procurement and project management processes.

Which is fine, no doubt, but there is no sign of the Board having added any value.

What of the highly-controversial bank capital proposals that the Governor rushed out late last year, and then spent months having to backfill material in support, still not having provided any sort of serious cost-benefit assessment for what he is proposing? Here is what the Board had to say.

The Bank’s proposal to increase capital requirements for registered banks has attracted considerable public comment and created greater awareness of the importance of the quality of capital and capital ratios for financial stability. We have closely followed public commentary on the proposals and directors have been open to hearing the views of senior executives, chairs and board members of the banks operating in New Zealand.

Seems quite telling that to the extent the Board is interested in any other perspectives than the Governor’s it is only that of banks. Public interest anyone?

They go on

In our oversight of the transition from consultative process to final decisions and the completion of the Bank’s cost/benefit evaluation, we are mindful of the Minister’s expectation that we test the Bank’s thinking on regulatory proposals and be satisfied that the Bank has reasonably considered and addressed alternative perspectives.

Isn’t that nice. No sense that they might themselves have a statutory obligation to hold the Governor to account, no sense that a cost-benefit analysis is useful at the start of consultation, not after the single prosecutor-judge-jury has already made his final decision.

If you were being charitable one might read a subtext of some unease, but it is as if they are embarrassed to be uneasy, when in fact it is supposed to be their job.

What of the Governor’s great enthusiam for all things green and climate changey?

The Bank’s work programme on climate change is also of national importance. The programme follows increasing global interest in the implications of climate change for financial stability and the risks associated with asset stranding, uninsurable assets and economic shocks resulting from catastrophic loss from climate events and the sectoral impacts of emission-reduction strategies. It is important that the Bank provides leadership in understanding the implications of climate change for different sectors of the economy as well as the financial system.

Give me strength. Not once do they attempt to ground of this in the statutes the Bank operates under. They don’t even try to pretend that it is related to the specific statutory responsibilities the Bank has. No, they declaim that this “work programme” – of which we’ve seen very little – is somehow (but how?) of “national importance”. Not just that, it is – they tell us – “important for the Bank to provide leadership in understanding the implications of climate change for different sectors of the economy”. You’d think we didn’t have a Treasury or a Ministry for the Environment, and that heroically the Governor was swooping in to save the day. Instead, he is again using public resources for personal ideological/political agendas – they might even be popular, at least in his left-wing circles, but they simply aren’t his job. The Act(s) tell him what is. The Board clearly doesn’t care, either in his thrall or intimidated by the Governor.

The Board – no doubt guided by management – make much about external communications but don’t even pause to note that now, 18 months in to the Governor’s term we’ve not had a single speech from the Governor on financial stability issues (where he remains sole legal decisionmaker) and – finally last week – a single short, really rather bad and lightweight, speech on monetary policy. In his own statement, the Governor talks of how

all initiatives this year have been propelling us forward to be a Great Team, Best Central Bank.

And yet strangely, this goal isn’t even mentioned by the Board – supposedly holding him to account – let alone how such a dreadful track record of speeches (where the Governor could readily be benchmarked against overseas peers) measures up to it.

One of the themes of the Annual Report – Bank and Board – is that the Bank just doesn’t have enough money. I used to, perhaps still am, mildly sympathetic to that view but they really don’t make the case when

- so much of what they do isn’t done well (see bank capital as just one example, or CBL, or that recent speech, or….),

- and when there is no sign that new and costly whims are rigorously evaluated, no sign that whims and interests are sacrificed in favour of doing core business better.

If you think the word “interests” is some jaundiced invention of mine, you’d be wrong. Here is the Board (emphasis added)

The interests of the Bank, and its public engagement, have broadened in appropriate ways. But it is clear that in order for the Bank to meet public expectations, to continue to meet the highest standards of monetary policy formulation, to increase its regulatory/supervisory capability and to be more externally engaged in both traditional and new policy interests, additional resources will be required in the future.

Government agencies aren’t supposed to be funded for the whims of senior managers, the “new policy interests” of Governors, but for the statutory duties Parliament has set ouf for the institution. As regards the Reserve Bank, those are really pretty clear. They don’t include playing the tree god (from memory that Maori strategy was costing about $1m), let alone some self-interested role of national importance as champion of centre-left climate change rhetoric.

The Governor ended his own statement in the Annual Report this way

I would like to thank our Minister, Hon Grant Robertson, and our Board for their unwavering support during the year.

And there, in a sentence, is surely the problem. The Governor works for, and is accountable to, the Minister and the Board (and the public). Their job is to pose hard questions, demand excellent performance, and generally be just a little annoying – that is what serious scrutiny feels like. Both seem to have been AWOL on the Governor’s biggest rash initiative of the year – the bank capital proposals. Both seem to see deference to the Bank, rather than accountability from it, as their role. In that sense, neither adds any value.