Mervyn King was successively chief economist, Deputy Governor and Governor of the Bank of England over 20+ years. Now in private life, with all the honours the UK can bestow (as Lord King, and a Knight of the Garter). he periodically offers his thoughts – lucidly, rigorously, and respectfully (a model, in that regard, for any central bank Governor) – on various economic policy issues. There was. for example, his book The End of Alchemy a few years ago (which I wrote about here). There is a new book, with another respected UK economist John Kay, due out early next year.

Over the weekend, at the IMF/World Bank Annual Meetings, King delivered the prestigious Per Jacobsson Lecture in Washington DC (video rather than lecture text). His lecture has had quite a lot of media coverage (for example here), with an emphasis on the idea that we are “sleepwalking towards a new crisis” and with various ideas and emphases for reform.

There are things to agree with and to disagree with in the lecture. He is clearly right to be expressing concern about the likely economic and political consequences of any new severe downturn, with little conventional monetary policy capacity at the disposal of the authorities. If/when such a downturn happens it is going to be very difficult to navigate successfully. That message needs to uttered loudly and often, to alert the public and (perhaps) galvanise some policymakers.

Where I’m rather more sceptical is around Lord King’s expressed enthusiasm for the idea that the disappointing growth performance over the last decade or so is primarily a problem of a shortfall of demand. Of course, it is likely that there is a demand (and monetary policy) element to the story – in most places, inflation has undershot targets and as central banks (and markets) have been repeatedly surprised by the fall in market interest rates, they’ve had a bias to hold policy rates higher than they probably should have been.

But King’s story is a much more radical one than that.

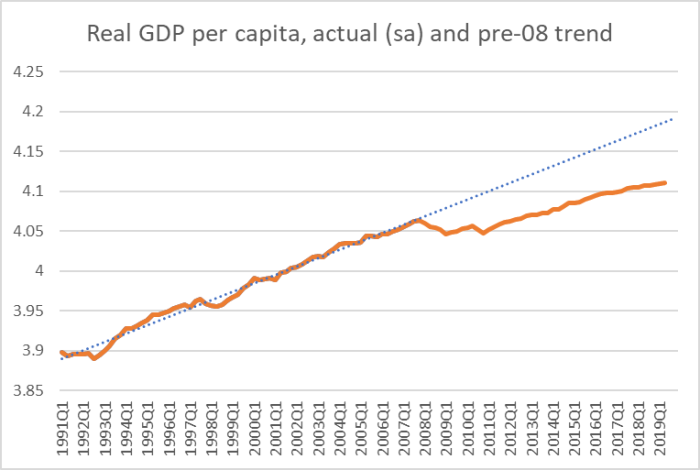

One of the ways he set up his story was by analogy with the last great period of macroeconomic disappointment, the Great Depression. He notes that in most advanced countries now real per capita GDP is well below the level implied by the trend in the decades running up to 2008. Here is a New Zealand version of the sort of chart he has in mind.

And then he moves on to assert (a) that similar charts could have been produced in the mid-late 1930s, extrapolating trend growth in real per capita GDP for the 20th century up to the Depression and yet (b) by 1950 actuals had returned to the pre-Depression trend. So, he argues, we should not jump too readily to the conclusion that what we are seeing now is fundamental, grounded in supply-side problems. It might simply be an insufficiency of demand and with the right policies we too might find ourselves, 20 years on from the 2008/09 recession, back on the long-term trend line.

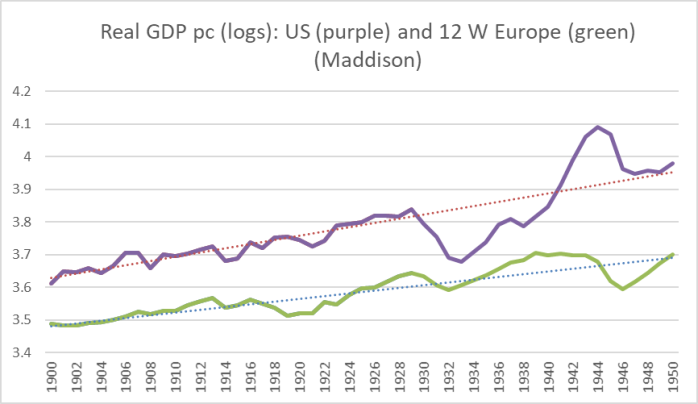

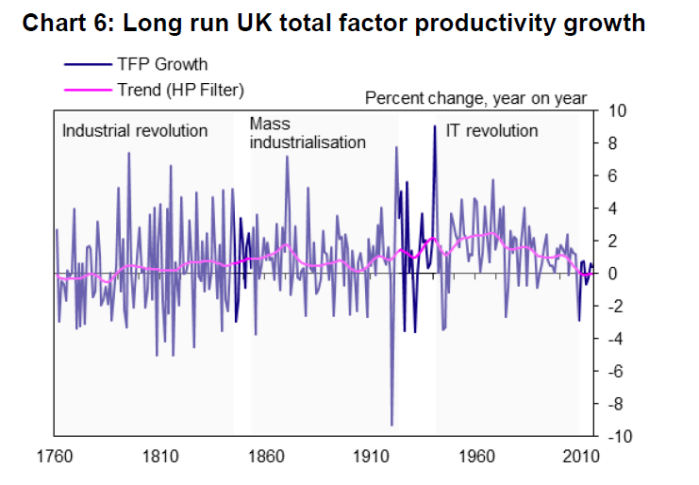

King’s story of the 1930s holds very well for the United States, where (for example) the unemployment rate was savagely high throughout the 1930s (a notable contrast to the situation today). I’ll illustrate that in a moment. But it isn’t a story that generalised even then. Here, for example, is UK real GDP per capita for the first half of the 20th century.

The first few decades of the 20th century hadn’t been great for the UK, but then the UK experience of the Great Depression was fairly mild and by 1937/38 the economy was running above the pre-Depression trend (and remained so all the way through to 1950).

Rather than illustrates dozens of different countries, in this chart I’ve shown the situation for the US and for Maddison’s grouping of 12 larger Western European countries.

You can see King’s point very starkly for the US, but for the Western Europe grouping it isn’t there at all – the picture is more like that for the UK (above). (For what it is worth, New Zealand was also above the trend line by 1937/38 – a overheating economy running towards a fresh crisis – and Australia was a bit below its pre-Depression trend line.)

So the general story just doesn’t seem to stack up very well at all. There were significant demand (and monetary issues) associated with the Great Depression, but mostly they were dealt with within a few years. The US was the glaring outlier – a country that then managed to have another pretty severe downturn in 1937/38 as a result of its own demand (mis)management choices.

As is now widely recognised, global productivity growth has slowed very substantially. Here is one illustration, using the OECD’s multi-factor productivity data for 23 OECD countries (the “older” OECD countries – none of the former eastern bloc OECD members are yet included). I’ve calculated rolling 10 year average growth rates for each country and then taken the median of those growth rates.

Being a median measure, you can tell that almost half these advanced countries had (typically slightly) negative annual average MFP growth over the last decade. In the decade to 2007 (say) only two did.

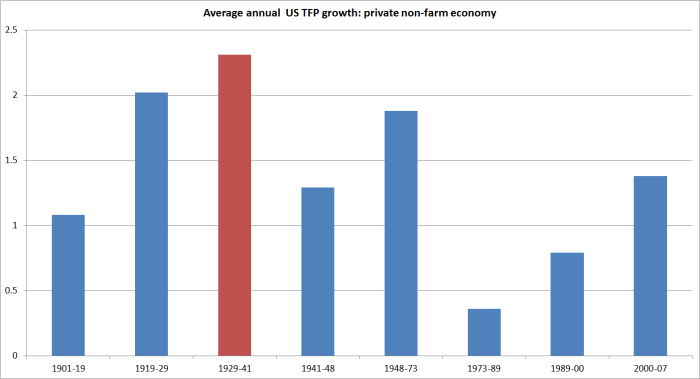

By contrast, here are leading economic historian Alexander Field’s estimates for multi/total factor productivity in the US in decades past.

The period when overall economic activity lagged behind trend so badly, which pretty much everyone agrees was largely down to demand shortfalls, was also the period of very strong underlying TFP growth.

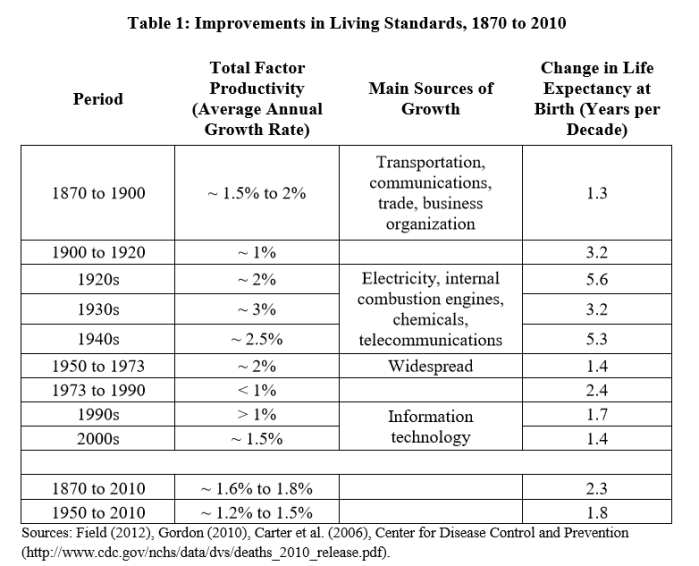

In a similar vein, here is table from a 2013 CBO report on TFP growth in historical perspective (which also draws on Field).

Historical estimates get reworked, and I’ve seen some revisions to some of these numbers. But they don’t change the story of strong underlying TFP growth in the 1930s – all it took was enough demand to translate those new possibilities into higher per capita GDP (back to the longer-term trend line in the charts above).

What about other countries? Here is chart from a speech given a couple of years back by the Bank of England’s chief economist

It is harder to read, but there is no sign of any slump in TFP growth in the 1930s there either (then again, as illustrated above, demand didn’t look to lag badly for long at all in the UK).

There is a story, that King also tried to tell, that somehow the incipient productivity gains now simply can’t be realised – let alone translated into higher GDP per capita – because the demand isn’t there and because of heightened policy and trade uncertainty. But that doesn’t ring true either. After all, equity markets have been strong, real borrowing costs have been low (unlike the 1930s), and – if anything – the IMF is worrying about corporate sector overborrowing and vulnerabilities associated with it. That borrowing might not have been funding much new investment, but business credit conditions haven’t exactly been very tight for years now.

And as for uncertainty, yes we all now that the general policy and trade policy indexes are quite high at present, but (a) trade policy uncertainty has really only become a big issue since the start of 2017 and the economic underperformance was well in place before then, and (b) consider the 1930s…..the demise of the Gold Standard, ongoing sovereign debt defaults (including the US and the UK), Smoot-Hawley and all the associatred/subsequent trade protection, the rise of Hitler, Japan’s invasion of China, the growing fear of war. I’d have thought all those made for much greater uncertainty than we see today, but even if you read things differently, it was hardly a decade that made for a stable and certain political or business climate. And yet…..consider the realised TFP growth, consider (outside the US) the return to pre-1929 real GDP per capita pathways, contrast it with what we’ve seen in the last decade, and you should doubt that the 1930s provides much useful insight on our current situation.

I don’t have a compelling story for why the productivity slowdown has been so stark and sustaine among countries at or near the frontier. But a demand-based story doesn’t yet seem very credible, and if such a case is to be made it is going to need to rest in argumentation, theory and evidence, based on something other than parallels with the 1930s.

(And, of course, whatever the frontier story none of it should be of much relevance to New Zealand, starting from average productivity levels so far behind those of the frontier economies.)

I would have thought the rise of the healthcare sector and the hospitality sector would be a compelling enough story? Listened to RNZ 101.4 today of a what is likely a systemic failure of our rest home and health care facilities in terms of enough trained people and equipment to cope with aging illnesses and increasing obese patients who require lifting equipment and increased numbers of personnel. A sick old lady was left to rot with open sores filled with maggots in a rest home facility and staff were too busy and no one noticed.

LikeLike

With Immigration blocking access to more than 700 arrivals on holiday Visas at the airport this year no wonder our healthcare sector is suffering from a shortage. Clearly these are young people are on holiday and looking for work.

I myself arrived on a holiday Visa first, found a job and stayed on. It is rather hard to apply for work from outside the country and for prospective employers to even take notice or for employment agents to treat you as a serious prospect.

LikeLike

If you are a working on a holiday visa how do you get an IRD number? I can imagine many fruit pickers having no problem but care homes?

For many Europeans it is fairly easy to get a working holiday visa (as did some of my own family) – it is then rather random as to how much work they actually do – my neice only did unpaid woofing.

LikeLike

Once you have a job offer in hand you can apply for a work Visa and a IRD number. Tax residency is not the same as permanent residency.

LikeLiked by 1 person

Have you any idea how long it now takes to get any INZ staff member to look at any visa application? Not time to process but simply time to be assigned to a case officer. Last I heard it was 9 months unless you have a job offer from the govt.

LikeLike

No idea how long it takes these days but 30 years ago NZ was practically dishing out work permits with a rubber stamp on your passport. Fast and an immediate turnaround.

There was a long queue however when they started giving amnesty permanent residency to any foreigner in the country, no questions asked.

LikeLike

I’m struggling to understand why the avalanche of regulation and welfare makes lost productivity and economic progress surprising.

LikeLiked by 1 person

Across the OECD there is little sign of increased welfarism in the last decade or two (it was really a story several decades back). Same goes for size of govt (tax/GDP etc). I accept that there is a growing amount of increasingly complex regulation – here and abroad – but whether that burden has become more intense (relative to the past) at a pace that can really explain such a sharp collapse in productivity growth is rather more of an open question.

From a NZ perspective, and switching back to labour productivity, the former eastern bloc EU countries have much the same burden of regulation as their western peers, and it hasn’t stopped them recording rapid catch-up productivity growth in the last 15-20 years. NZ, by contrast, has drifted a bit further behind.

LikeLike

I think the constraints in building and land use have certainly intensified in the past two decades. Multigenerational welfarism has compounded into declining educational achievement, unstable families and increasing drug abuse. I don’t know if these have been mirrored in the Eastern EU block but I suspect not to the same extent.

LikeLike

Fair pont re building. One could also cite AML laws.

But just needs to be cautious in too readily explaining such a deep and broadranging (across so many countries) slowdown in productivity growth of a sort there is little hint of in the couple of hundred years since the Industrial Revolution (a period when all sorts of things have been hypothesised to lead to major troubles). Have a look at that US chart in the post – you can run the chart all the way from the mid 19th C to 10 years ago and things always reverted to trend (not true everywhere else, so not a general proposition) but still a sobering reminder of all the things that didn’t throw the US off course.

LikeLike

Is it time for the Productivity Commission to report on its own productivity and effectiveness?

LikeLiked by 1 person

With 57 Volcanos and we are trying to put our largest city in an dormant but still potentially volcanic field that could blow up anytime. I think you would have a really tough job to try and fix geographical constraints.

LikeLike

Strange that the Commission reports (Fig 9) a growth breakdown by sector for 1996-2018 but not a comparable one for the lagging last decade:

Click to access Productivity-by-the-Numbers-2019.pdf

You would think the discontinuity since 2008 warranted proper investigation.

LikeLike

The main avalanche in social welfare is our $400 million a year in Treaty of Waitangi racist social welfare payments. Meng Foon our racist race relationship commissioner is calling for resignation of Andrew Hollis incoming Tauranga Councillor for making statements that the Treaty of Waitangi is out of date.

The only racist is Meng Foon who should himself resign.

LikeLike

As a first class passenger on the Waitangi gravy train, Mr Foon has a preeminent view of its entitlements..

LikeLike

Not an economist so the following may seem silly … One of the government actions (here and abroad) to arrest the Great Depression was the State purchase of public works (roads, bridges, pine forests and so on). This was ‘demand’ and an ability to pay, that formed the catalyst for jobs and business endeavour. WW2 and subsequent peace-time rebuilding had a similar effect. From the time of Reaganomics, Thatcherism and our subsequent Rogernomics (bring up the rear like Dopey) governments have stepped back from significant State programmes, privatising State enterprises, and leaving it to the private sector the take the initiative. Yes I know the State has commissioned a public hospital here, or a school there, but what was previously seen as the purview of the State (Insurance, banking, telephony, and other commercial activities) the State has stepped back from. The State economic demand instrument has significantly reduced over the last 30 years, and private enterprise has only picked up what was profitable to their business interests (as you would expect). There were calls during the early stages of the Cash Crisis in the US as elsewhere for the State to commission public works – replacing infrastructure (bridges was one) but instead the US got cash-for-clunkers to help the auto industry, and quantitative easing. I wonder if this reduction in State demand is a factor in Lord King’s thinking … just asking.

LikeLike

Note that during the Great Depression govt capital works were often severely cut back (happened in NZ). Monetary policy – notably breaking the link to gold and, in effect, devaluing currencies – is generally regarded as having played a crucial role in the recovery.

LikeLike

Seems a bit contradictory to state we are “sleepwalking towards a new crisis” and then point out all the uncertainty that exists as if people aren’t awake to the issues. Not many talked about a pending financial crisis pre the GFC but the threat gets plenty of headline space these days (e.g. IMF meeting / GFSR). The cycle can roll on longer – especially given the low growth / low productivity / low interest rate combination? (even if the causes are not fully understood)

LikeLike

Given that the last 2 if not 3 recessions were engineered by the RBNZ, it is more a case of “If it is not broken and you do not know what you are doing then don’t try and fix it.”

LikeLike

I think there is a difference between policy uncertainty (eg tariffs, Brexit or whatever) and the potential accumulation of financial risks (IMF emphasising the corp sector) which could, on King’s argument, tip us into a new crisis

LikeLike

The “Long run UK TFP growth” chart is interesting. Assuming prior to 1760 it is fairly flat into the recorded past maybe we are just returning to normal. The industrial revolution took decades before it impacted the majority of the population with the 1860 peak coinciding with completion of a UK rail network. Dramatic changes such as telegraph and telephone may explain continuing growth to 1910 and then buses, trucks and eventually cars changed Britain from the twenties to the fifties. What I find most interesting is the dramatic plateau from the 40’s to the 60’s and the continued but lower growth rate to the end of the century. One thing it cannot be is the IT revolution; that only became significant in the early 1970’s onwards (I was there) and the common use of the PC was from the late-1980s.

My explanation for the increased productivity of labour while technology improved no faster than in the past would be to examine the labour. Prior to 1920 paid labour was almost entirely male and it comprised all males. When women did enter the workforce it was disproportionately the educated women and they did so when they were at their age of highest productivity. Meanwhile the male workforce changed with some of the deadwood going on to benefits. So from the end of WW2 to about 2000 the quality of labour improved on average. Since then the rate of longterm unemployment has plateaued. Now all women work whether educated or not. Our massive increase in tertiary education is robbing society of 3 or 4 years of our most productive workers. It makes sense that the decline in the quality of our workforce cancels our current technological developments.

LikeLike

Labour productivity increased as our factories automated. Since we replaced our industrial sector with farming and services, productivity has been achieved by adding cows. Since we are at peak cows with currently 10 million cows and it is unlikely we will ever have the industrial sector we once had, we will see declining and worsening productivity as we shut down our energy sector and replace that with tourists and Air BnB.

LikeLike

You forget the potential slowdown in tourism as air travel becomes demonised for its carbon intensity which could have a significant influence unless our tourism sector becomes for the wealthiest and so its productivity increases. Catering to the hoi polloi generates “wealth” through volume

LikeLike

Are tourism and AirBnB earnings excluded from the ‘total aggregate output’ and the labour used in both from the ‘total aggregate output’ used to estimate TFP?

My comment relates to the graph of UK TFP growth. In the UK milk production is insignificant and probably didn’t alter dramatically over the last 70 years.

Your interest in the dairy industry may well explain why NZ is falling behind the UK and France – a totally anecdotal comment based on the recent months holiday I spent in Europe. Certainly two decades ago I didn’t have the same feeling for a wealth difference between NZ and the UK; a visit to the two main supermarkets in Farnborough certainly gave me a strong impression that we are falling behind.

LikeLike

Remember that these are per-unit-deployed measures, so even if (say) tertiary education were adding no economywide value, TFP measures shouldn’t be affected by all those students having a few years out.

The decades to the 70s certainly look exceptional but i’d be more sceptical (yet) that such lower productivity growth as recorded in the last few years is the new long-term normal. Perhaps, but of course only time will tell.

LikeLike

My point is from the age of 18 to 22 we are at our most energetic and productive and from 60 to 65 our least. That may be debated in our modern society but would not be self evident in less developed societies. Both education and medicine have changed the age profile of our workforce increasing the median age and therefore moving it from the dynamism of youth to lethargy of old age. Admittedly it is not much of an argument whereas I think there is something to be made of productivity and the introduction of women into the workforce.

The UK had its peak TFP growth in the decades predating the IT revolution during precisely the decades the UK industry collapsed with export markets lost to Germany and Japan and the loss of empire and UK factories crippled by trade union activities. If with all the benefits of hindsight we cannot explain why then we have little chance of sorting out NZ’s current lack of productivity.

LikeLike

Re the UK story, you would need a proper multi-country comparative analysis. Productivity growth across the advanced world was pretty strong in those post-war decades.

LikeLike