I spent yesterday afternoon at a couple of policy-focused seminars in Wellington.

The first of them – “Tax on Tuesdays: Time to Even it Up” – was hosted by Victoria University’s Institute for Governance and Policy Studies, in conjunction with (if I heard correctly) the PSA and something called the Tax Justice Network Aotearoa NZ. So the orientation was fairly left-wing, and explicitly focused more on fairness than, say, efficiency or prosperity. But there were some interesting speakers, even if they didn’t have much time each so couldn’t dot all the i’s, cross all the t’s etc.

The first was Andrea Black, former Treasury/IRD official, former independent expert adviser to the recent Tax Working Group, tax blogger (and occasional commenter here), who focused on taxation of capital income. After repeating her support for a capital gains tax, her distinctive argument was for an increase in the company tax rate to match the maximum personal income tax rate. The main arguments appeared to be that (a) the most assured way of being able to tax the incomes of rich people in New Zealand was to tax companies (since in closely-held companies much of profits are distributed by way of loans – not taxable in the hands of recipients – rather than as dividends), and (b) the old argument about cleanness, minimising avoidance etc in having the company tax rate, the trust rate, and the maximum personal tax rate aligned (there being plenty of evidence that people will do what they can to defer tax by being paid through companies etc where possible).

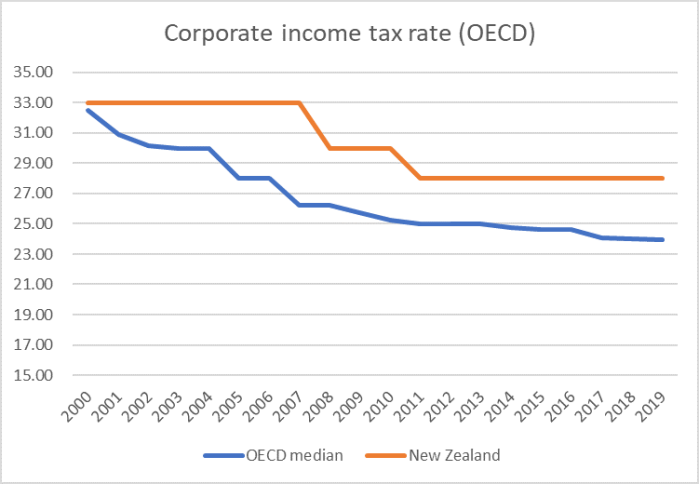

I wasn’t really persuaded. With dividend imputation, the company tax rate in New Zealand bears much more heavily on foreign investors (none of whom needs to be here) than it does on domestic shareholders. In a country with low rates of business investment and now relatively low rates of foreign investment, it seems cavalier to be calling for increases in company tax rates which the global trend is clearly downwards (at 33 per cent the company tax rate would be the second highest in the OECD). In defence of her position, Andrea invoked some old IRD analysis that company tax cuts haven’t made much difference to investment – IRD has a strong institutional bias towards a simple tax system and little real focus on productivity, economic performance or anything of the sort – while noting that “if you did care about foreign investors” – there were various technical tweaks (I didn’t catch them, but perhaps thin capital rules?) that could be adjusted to compensate them at least in part.

As if to forestall a question, Andrea alluded to this chart I’ve used several times – a version of which appeared in the TWG’s own background document last year.

Prima facie, it didn’t as though – by international standards – we were undertaxing business income.

Now, of course, there are some well-recognised caveats to this data. First, it doesn’t take account of dividend imputation in New Zealand (and Australia, but not elsewhere), and the TWG suggested there were some issues around consistency of treatment of government-owned businesses. On the other hand, in many countries lots of stocks are owned by long-term savings vehicles with much less onerous tax provisions than their peers in New Zealand would have, and our tax system (mercifully) has fewer deductions and “holes” in it. In yesterday’s presentation Andrea suggested that in many other countries various classes of business income that would be incorporated – and thus captured in the chart – here wouldn’t be treated the same way in other countries.

All that said, if anyone is seriously suggesting that the chart of OECD data is substantially misleading about the New Zealand position – say that in truth we might be in the lower half of the chart on an apples-for-apples comparison, the onus is probably on them to demonstrate that more specifically. The OECD data itself suggests we have taxed businesses quite heavily going back 50 years, to (for example) well before imputation was ever on the scene (chart in this post). Perhaps it is just coincidence – and I’m certainly not suggesting it is the only factor – that business investment as a share of GDP has been low by OECD standards throughout almost all that period.

The second speaker was inequality researcher Max Rashbrooke. His focus was on taxing wealth. He doesn’t like the idea of a land tax (partly because land is held more widely than most assets, partly because Maori land would have to be “omitted for justice”) or the risk-free rate of return deemed income method that has been proposed by various groups (including the McLeod tax report, and TOP) because he doesn’t believe it is right or politically feasible to include the family home. His argument was for a wealth tax, levied at (say) 1 per cent per annum on net wealth, but applying only to those with net wealth in excess of (say) $1 million. This was sold as something of a moneypot, with revenue estimates of $6 billion a year.

Based on what he told us yesterday, the ideas didn’t seem to have been advanced in much detail yet, including the question of how one might get annual valuations of unlisted companies. I asked about what proportion of his estimated $6 billion of revenue would come from ordinary middle-aged and elderly Auckland homeowners (given his unease about taxing the family home), but he didn’t know. Personally, I couldn’t help thinking that a better approach would be to fix the urban land market at source – kill off the regulatorily-induced artifical land values, and (a) the cause of justice and fairness more generally would be served, and (b) there would be nothing like $6 billion per annum of revenue on offer.

The third speaker was someone called Michael Fletcher, of IGPS, who was apparently an advisor to the Welfare Working Group. He was mostly talking about the welfare system – in lots of detail, but with a view of the place of the welfare system that was so different to my own that I’m not going to spend much time here on what he said. There was the odd striking statistic, notably his suggestion that perhaps 100000 people may be entitled to the Accomodation Supplement but not getting it (and he highlighted how easy the Australian comparable entitlement is to access, if you are entitled to it, relative to New Zealand), but I was left unchanged in my view that so much could be done for the better, for those at the bottom, if only the urban land market were freed-up. Rents, after all, should have dropped very substantially in real terms over the last decade – in a functioning market that would be an expected corollary of steep falls in long-term real interest rates – and haven’t because central and local government rig the system against renters and new purchasers of dwellings.

For myself, on tax I remain tantalised by the idea of a progressive consumption tax. In the abstract, it gets around all the debates on capital gains taxes, realisations (or not), company taxes, gift or inheritance taxes or whatever, and has the appealing the feature of taxing people on what they consume not on what they produce. Of course, no country runs such a system – which does have formidable practical issues. And if one wants to align company and personal rates – which has some appeal (although the Nordic model questions that), better to lower the personal income tax rates by 5 percentage points (max rate to 28 per cent) and add a Social Security Tax of 5 percentage points on labour income up to a certain threshold. New Zealand and Australia are, as I understand it, the only OECD countries not to adopt some such model (we do it on a very small scale with ACC).

From Victoria University, it was up the street to The Treasury where Alan Bollard was billed as speaking on

“New Zealand as a Leaky Economy: Are We Responding to Changes in Globalisation?”

As Alan is a smart guy, has been one of the “great and the good” of the New Zealand establishment for decades – chief executive of one body after another for more than 30 years – even as New Zealand’s economic performance has continued to languish, and has recently finished a stint as Executive Director of the APEC Secretariat, it should have been interesting and stimulating. It wasn’t.

Here was the summary that drew me along

For the last few decades New Zealand’s general policy approach has been to pursue economic openness (with some protections), in order to get the benefit of international growth drivers. Some of the political and economic developments around globalisation today are challenging that traditional approach.

Traditionally we think of external economic balance as the current account. Dr Bollard’s approach would go much wider, exploring our patterns of merchandise trade flows, services trade, short term capital movements, outward direct investment, labour movements, economic migration, data movements, business mobility and other less tangible flows (e.g. intellectual property, human capital) across borders.

Much of the debate centres on our inflows. This seminar turns the spotlight on outflows. It questions whether we are leaking value internationally: losing talent, falling off the value chain, undervaluing services, losing businesses (including their ideas and their taxes) to overseas interests. Questions abound: do we really leak value, do we have any alternatives, and what might “sticky policies” look like?

But there just wasn’t very much there.

He talked under various headings.

On goods market trade, what he had to say seemed to boil down to the fact that distance really matters for New Zealand and that two-thirds of our exports are still commodities, noting the failure of the Fonterra value-added dream. We draw on tangible and inflexible resources (natural resources) whereas places like Hong Kong or Singapore (or, one could add, major European or North American cities) don’t.

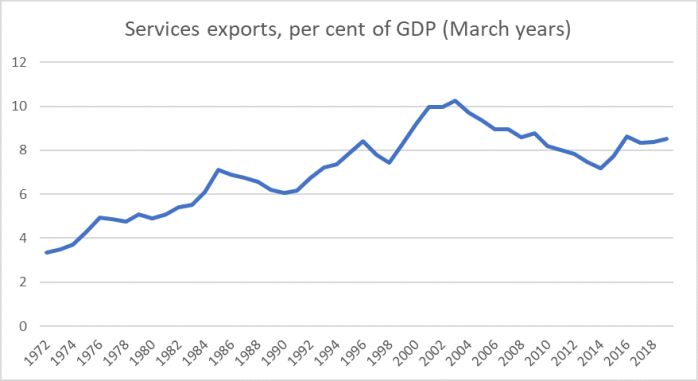

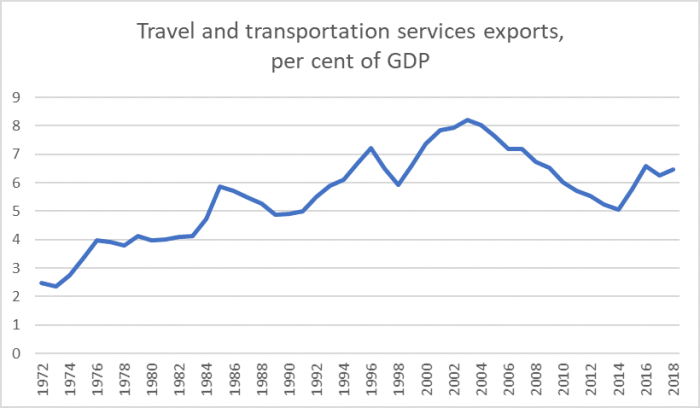

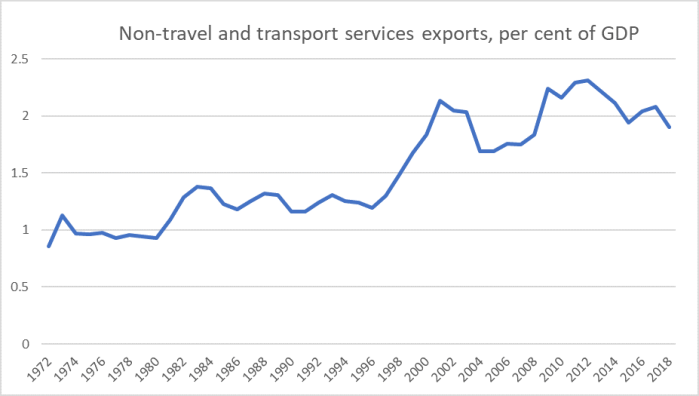

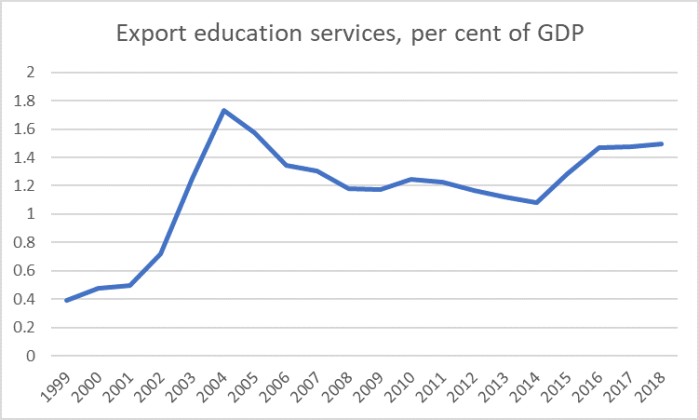

On services trade, there also wasn’t much there. He noted that New Zealand had long been a net services importer, but beyond noting – rather misleadingly – that tourism and export education had been doing well, there wasn’t much beyond noting various global trends and technologies.

On international capital markets, there also wasn’t much. As he noted, we typically have current account deficits, have modest savings rates, and have a banking system mainly run by Australian banks. The claim that markets internationally are “increasingly globalised” seemed odd, both against the backdrop of smaller global imbalances than were apparent last decade, and the rising tide of restrictions in various places on foreign investment (whether US restrictions on China, or New Zealand restrictions on purchases of houses or farm land – both of which he noted).

Of the market in labour, there was (surprisingly) little or no mention of immigration policy, but quite a focus on the outward flow of New Zealanders (and the high skill levels of many New Zealanders). His assertion is that “talent is increasingly mobile”, and yet across the board for New Zealand that also looks not really true – it is harder for New Zealanders now to go to Australia than it was and, as a result, that net outflows of NZ citizens) are much smaller (share of population) than they were several decades ago, even as the productivity and income gaps have widened further.

In discussing the market for corporate control, Alan listed various facts and factoids, including the suggestion that one of the biggest assets now owned by foreign companies was “our data”, and the notion that New Zealand ideas leaked abroad (but then, as he had noted earlier, this is hardly new – Glaxo having been founded in the 19th century New Zealand).

And then as he got to the end and turned to policy, he could only conclude that there were – in his view – ‘no easy answers’, including noting that we were constrained by various international agreements (he didn’t tell us what interventions he’d propose if we weren’t). There was favourable mention of the student loans policy that bears more heavily on people if they leave than if they stay, repetition of an old (misleading) line that houses have become international financial assets, and really not much more. And there was the old question of who do we make New Zealand policy for: New Zealand or New Zealanders, and who counts as New Zealanders in this context, but few or no attempts at answers. The fact that New Zealanders would be crewing many of the America’s Cup yachts of other countries, and that some New Zealanders would be playing for other countries’ RWC teams was mentioned, but not in a way that left me any close to sensing that he was doing more than lamenting New Zealand’s continuing economic decline – without, in the hallowed halls of Treasury, being so upfront as to mention it – which sees able New Zealanders looking abroad for better returns to their talent (as able people from many middle income and poor countries do – see African or Latin American players in European soccer leagues).

To his credit, Alan took a lot of questions. In many cases, the questioners seemed to be attempting to get Alan to endorse their preferred line of argument or policy option. Actually, that included his wife – Jenny Morel – who suggested that Alan was underplaying the success of our high-tech firms (citing the repeatedly spun and highly misleading TIN report), to which Alan returned to his theme that such companies can and do leave very quickly, and noting again the loss of able people (explicitly highlighting that the two Bollard children are now living and working abroad, apparently permanently).

A Treasury official asked Alan about the real exchange rate, noting that many conventional analyses (and, perhaps, unconventional ones like my own) stress the role of a persistently overvalued real exchange rate. Alan was pretty dismissive of the issue, suggesting if there was an issue it was nothing more than cyclical.

Perhaps, but when the gap between productivity and income levels in New Zealand and the rest of advanced world has kept widening for decades, and yet the real exchange rate has been high and rising this century and the foreign trade shares (imports and exports) have been falling, it looks like an issue that might repay rather more attention. In my experience, Alan always tended to treat the real exchange rate as a financial variable, whereas is generally better seen as a real phenomenon, the outcome of various domestic pressures and imbalances (the price of non-tradables – driven by domestic forces – relative to the global price of tradables).

Alan Bollard wasn’t purporting to offer some fully-developed story of New Zealand’s economic decline, so I won’t fault him for not doing so, but it ended up as a rather strange talk. The subtext was of the failures – and yet those declining trade shares were never mentioned, nor (for that matter) the productivity story – and there was the mixed pride and regret of older parents whose children have joined, perhaps permanently, the diaspora. It was as if he knew there were problems, perhaps even rather serious ones, but wasn’t able or willing to think hard, or talk openly, about causes and what aspects New Zealand authorities could so something about. That’s a shame.