As we wait to learn where the government has setttled on the idea of a capital gains tax, Radio New Zealand had an interview this morning in which their presenter Guyon Espiner talked to a business lobby group opponent (John Milford of the Wellington Chamber of Commerce) of a capital gains tax. I’m someone who is, at best, sceptical of the merits (and potential revenue gains) of a CGT, but it wasn’t the most effective case made against such a tax.

But what really prompted me to pay attention was when Milford argued that business was already quite highly taxed. The interviewer responded along the lines of “oh, come on, the company tax rate of 28 per cent isn’t high at all”, and Milford simply let it pass and moved off to a claim that regulatory burdens and other costs were high.

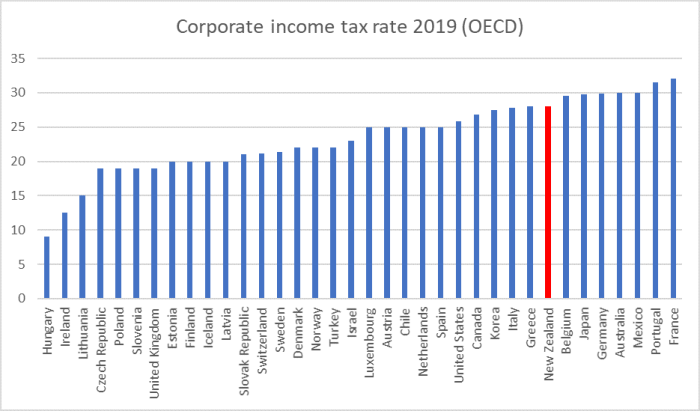

We should not lose sight of the fact that we have one of the highest statutory company tax rates of any OECD country. Here are the OECD’s own numbers for 2019 (incorporating all levels of government – some countries, including the US, have state level company taxes as well as national ones).

As almost everyone knows, headline corporate tax rates can mask a multitude of exemptions and deductions. So here is the data on the tax collected on the “income, profits, and capital gains” of corporates, expressed as a share of GDP. Data on actual tax collections takes time to compile, so these data are for 2017.

In this particular year, we took the second highest share of GDP in corporate tax revenue. That rank bobs around a bit from year to year (in the year the Tax Working Group used in their discussion document, we ranked number 1) and it appears to matter a bit whether countries collect taxes from central government entities or not (we do), but no one seriously questions that however one looks at things, New Zealand is one of the handful of countries collecting the highest tax (share of GDP) from corporates.

The picture is further complicated by the fact that New Zealand (and Australia, but almost no one else) runs a dividend imputation scheme, such that for domestic resident shareholders (only), corporate tax is really a withholding tax, and tax paid at the corporate level is credited against the shareholder’s personal tax liability. In most other countries there is a double taxation issue (profits and dividends are taxed with no offsetting credits), and partly as a result dividend payout rates tend to be lower. (This, incidentally, is one reason why there is a stronger case for a CGT in other countries than there is in New Zealand or Australia.)

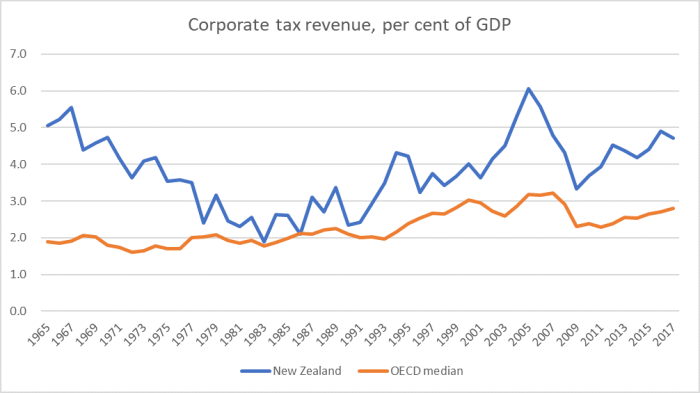

Incidentally, here is how corporate tax revenue (same measure as in the previous chart) in New Zealand compares with that of the median OECD country over 50+ years.

If anything, the gap appears to have been widening over the last 25 years or so.

It is worth remembering here that New Zealand is not, by OECD, standards a highly taxed country. Over that entire 50 year period we’ve been around the median OECD country for total tax revenue as a share of GDP (currently just a bit below). We also have relatively low levels of capital in our production processes (recall low rates of business investment, relative to population growth, over many decades), and yet we raise among the largest share of GDP from companies of any OECD country.

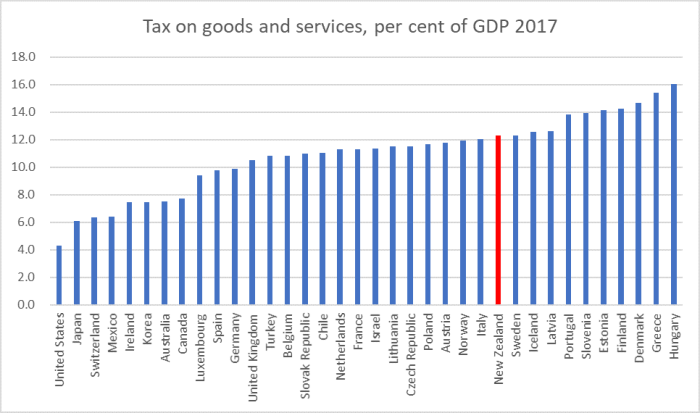

We also get quite a lot of revenue from taxes on good and services (mostly GST here).

We are also a bit above the median OECD country in the share of GDP taken in property taxes (mostly local authority rates, levied on property).

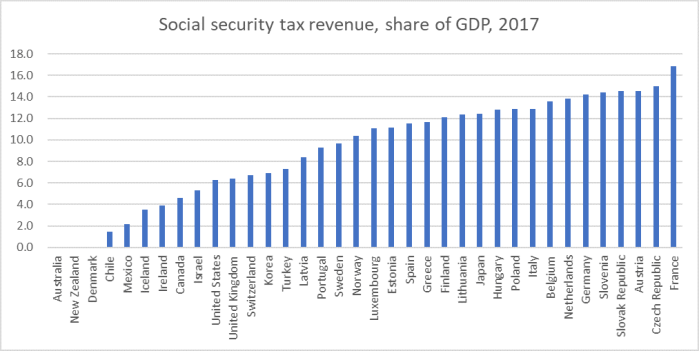

And, by contrast, the area where New Zealand collects hardly any tax revenue at all, as a share of GDP.

I can’t highlight the New Zealand bar. There isn’t one. On this definition, we collect nothing (on other definitions one might include ACC levies, but their equivalent is presumably also excluded in the calculations for other countries).

Most advanced countries fund a significant chunk of their welfare systems (unemployment, disability, age pension) with explicit social security taxes, typically levied only on labour earnings (although some are directly paid by employees, and some directly by employers). Of course, as the chart indicates there is a wide range in practices, but we (and Australia) are at one extreme, and partly in consequence we are the two OECD countries taking the largest share of total tax revenue in corporate taxes.

Does all this have much bearing on the case for a CGT? Personally, I don’t think so. A decent CGT – that didn’t tax pure inflation and allowed proper loss-offsetting – would be expected to raise very little revenue over time. If there is an argument for a CGT it is mostly in some conception of “fairness”, which needs to be weighed up against problems such as lock-in, and of the consequent biasing of asset holdings towards big institutional entities and away from individuals.

But don’t try to use as an argument for a CGT that business activity in New Zealand is lightly taxed. It isn’t. In absolute terms, business tax revenue as a share of GDP is currently well above the average for the last 50 years. In international comparative terms, we tax business activity more heavily than almost OECD country – and perhaps it isn’t entirely coincidental that we sometimes anguish about why we don’t have more business activity.

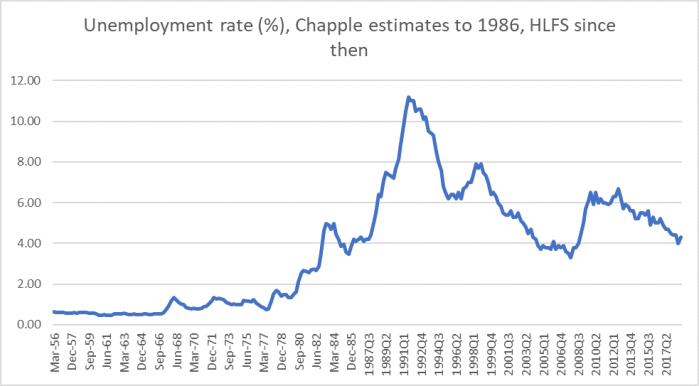

I listened to more of Morning Report than usual this morning (kneading hot cross bun dough as I did) and had the misfortune to hear Business New Zealand chief executive commenting on government proposals to crackdown on the “exploitation” of migrant workers. I haven’t looked into the details, so have no view on the substantive merits of the specific proposals (sympathetic as I am to the cause generally). But people shouldn’t be able to advance their cause with straight-out lies. Kirk Hope claimed that what the government was proposing was quite inappropriate in part because we currently have “record low” unemployment. Perhaps his memory is short, but Business NZ used to have an economist who could have briefed him. In the absence of that person, here are the data

Perhaps you might want to discount the first 20 years (although it was a real phenonenon), but current unemployment rates haven’t even reached the lows we managed for several years prior to the last recession. And these days older workers (aged over 65) are a much larger share of the labour force, and naturally tend to have a materially lower unemployment rate (in other words, what might have been unsustainably low 15 years ago, is probably rather more sustainable now).

Andrew Coleman argues that this forms the justification for a social security tax, in order to split out the tax burdens on labour and capital. Do you agree with him?

LikeLike

Yes, I think there is a good case for either a social security tax (ie cut general income tax rates, including company tax rate) and put on a social security tax, which would shift the (direct) burden of tax from capital to labour. In tax incidence terms, much of our high capital taxes are probably borne by labour anyway (lower than otherwise investment and wages).

Alternatively I have argued previously for a Nordic tax system, which explicitly distinguishes between income tax rates on labour income and those on capital income, setting the latter much lower (reflecting the greater tax-elasticity of investment, esp in any particular country). We all have to eat (and thus work, over the course of our lives), but no one has to invest in expanding a business. We are generally worse off when less of the latter happens.

To be clear, I don’t think our capital income taxation approach is the dominant part of the story for our long-term productivity underperformance, but it interacts with and exacerbates that other self-imposed disadvantages (high, by international stds, real interest rates and a persistently high real exchange rate).

LikeLike

Singapore has a corporate tax rate of 18% but does have a Employer super contribution rate of 15% compared to our miserly 3%.

LikeLike

The idea that No Zealand is an “advanced country” is really laughable; the twin facts that No Zealand is most definitely NOT advanced, and as time goes by, largely thanks to immigration levels that make those in Brexitland and Trumpland look positively tame, not really a country, are becoming more apparent by the day 🙂

LikeLike

I”m not unsympathetic to the argument, but among OECD member countries we are still earning higher incomes, and are more productive, than 10-15 other countries.

But we are no France, Belgium, Netherlands, Denmark, Germany, Austria, Sweden, Norway, Ireland, Switzerland or the US.

LikeLike

With a persistent yellow vest violence, and now church burning seems a regular occurrence, France is not exactly on my list nor is the US after my recent Xmas holidays. Clearly cities like Los Angeles with it’s streets of filthy homeless encampments indicates poverty rather than wealth.

LikeLike

Met a US visitor to Auckland and the first thing she says to me is that she loves that Auckland has a great smell. I can understand that comment after LA where the stench of human excrement, alcohol vomit and smoked weed was everywhere.

LikeLike

I hope you sent a copy of the note to RNZ. The liberals there wont mention it but they won’t have an excuse to make such ignorant, silly statements next time.

LikeLike

I didn’t explicitly, altho I think I’m read in the right circles. Sadly, these points just have to be made over and over again, but even the TWG discussion document highlighted some of these statistics (in their case approvingly).

LikeLike

Reblogged this on The Inquiring Mind and commented:

Excellent post

LikeLike

“”government proposals to crackdown on the ‘exploitation’ of migrant workers””. I’m delighted to hear it.

Admittedly my preference is for reduced quantity, higher quality immigration that would leave NZ similar to the country I chose to become a citizen of. But if the NZ establishment remains keen on rapid growth via a high rate of immigration with large numbers of relatively low paid immigrants then it must try to eradicate the widespread rorts and corruption that have been identified many times in our system. The reasons being:-

1. Exploitation is wrong

2. It handicaps honest business

3. It affects our international reputation.

So I wrote a letter in january to our minister suggesting that without parliamentary discussion he could mmediately increase the costs of visas to cover the costs of increasing his labour inspectorate (last reported as under 30). This week I had a reply from Mr Lees-Galloway that says new fees took effect last November.

The current fees are:-

Visa Cost Increase

Skilled Migrant Category $2,710 9.72%

Partner of a New Zealander Resident Visa $1,480 18.40%

Essential Skills Work Visa (online) $495 66.11%

Fee Paying Student Visa (online) $275 10.00%

I was hoping for something like the skilled visa I had in PNG that cost roughly the annual wage of two teachers and had to be renewed every three years. That would be roughly equivalent to $100,000 or $35,000 per year. Spending that kind of money would reduce exploitation dramatically and increase govt revenue.

LikeLike

I looked up Work Visa fees in PNG and the fee is only PGK1,000. Visa extensions cost PGK2,000. I think you are rather exaggerating the costs?

LikeLike

In my day (20 years ago) the PNG employer had to obtain a permit to employ a foreigner and it applied to the position not the person – that was the big expense and it applied even if the foreigner never arrived. My employer localised most jobs (from 40 foreign accountants to one for example) but kept the option open to bring in foreigners if the rare qualified native employee chose to move on or failed to perform. The large cost of employing foreigners made them develop a very strong training department and they sent most senior native employees for overseas courses.

My point remains: give the employer a big financial incentive to employ locals over foreigners.

LikeLike

The employment rate, as of December 2018, was higher than it’s been at any point since 1986. At 67.7%, it’s almost 2 points higher than the mid-2000s peak of 65.9%.

Expect that Kirk was using shorthand for tightness of overall labour markets.

LikeLike

Perhaps that was what he meant……….but the unemployment rate (or underemployment rights) is a more typical measure of labour market imbalances, being designed specifically for that purpose.

Had he simply asserted that labour markets are tight, I’d no doubt have let it pass, it was the specific claim that bothered me (and there is no evidence – in survey data, or wage behaviour, or inflation – that labour markets are as tight now as they were over say 2005 to 2007

LikeLiked by 2 people

Never forget that residential property renting (i.e. being a residential landlord) is, in NZ, a small business.

LikeLike

The tax rate usually is 33% on the rental profit which many investors preferring direct ownership or the use of the Look Through companies. That is a significant tax on a small business.

LikeLike

Our high unemployment rate for the last 30 years looks like using the unemployed as a buffer stock against inflation (NAIRU/Phillips Curve rationale). Prior to that it looks like we used an employed buffer stock. Does the data show a relationship between our unemployed buffer stock policy and productivity? I submit it might as having 140,000 NZers unemployed and 280,000 underemployed must be costing billions as a wasted real resource.

LikeLike

Productivity with working days as a denominator ignores the unemployed.

LikeLike

Elon Musk, Tesla factories are utopian robotic factories which delivers the highest productivity but can’t make a profit. Apple Iphones uses third party mega factories of cheap human labour in China and makes a massive profit. It is also perceived as high productivity because it does not count the third party china human labour component not resident in the US.

LikeLike

Hi Michael now that I have a bit more time I’d like to look at this some more, in particular how the numbers pan out once imputation is accounted for.

One thing though is the use of the term ‘corporate’. In NZ anyway this tends to imply a big company rather than any company which is what the NZ data is.

When you get to smaller companies TWG info showed climbing loans from companies to their shareholders, climbing imputation balances and a problem with dividend avoidance. All which says that small company shareholders are paying the company tax rate on personal income that should be taxed much higher.

But I am not sure if NZ has proportionately more smaller companies than other countries. I do know it is much easier to incorporate a company here than in other countries.

None of which is to say that your points are wrong – my inclination though is that the story is more nuanced than it may first appear.

LikeLike

Thanks Andrea. Interested in any future posts you do in this area (and that snippet about small companies was particularly interesting).

LikeLiked by 1 person