When you worked for an organisation for 30+ years you really do try to look for the best in it. Perhaps it is just me, but I tend towards optimism (notwithstanding Cassandra) and so have had trouble appropriately calibrating my expectations of the Reserve Bank. They keep surprising me on the downside. It isn’t so much the specific policy choices themselves (reasonable people might differ) as the too-often threadbare cases they mount in support of interventions which have taken the fancy of successive Governors, or causes Governors (especially the current one) have used their official bully-pulpit to champion.

I had another example yesterday when I opened a (very belated) response from the Bank to an Official Information Act request I’d lodged a couple of months ago.

You’ll recall that last December the Governor launched a consultative document in which he proposed to massively increase the amount of capital banks have to hold to conduct their current level of business. There had been no prior socialisation of this work, testing the analysis in expert fora etc. Just a (very far-reaching) proposal. A month or so later, in response to various OIA requests, they finally released some of the relevant background papers (one of which they had only written after the consultative document was released). (In fact, four months into the consultation there was another big new supporting document released last week, although those who’ve looked at it closely say it doesn’t really shed any fresh light on the issues.)

By February, the Bank’s Monetary Policy Statement was due. To their credit, the Bank devoted a box (Box E), a couple of pages in length, to the proposal, under the heading “Monetary policy implications of higher bank capital requirements” (pages 35 and 36).

They make a number of claims in the box. They correctly note the need to distinguish between the transition and the long-run (itself something of a concession, since there was no discussion of the transition at all in the consultative document itself).

Of interest rate effects they note

All other things unchanged, bank funding costs would rise as a result of their higher capital requirements, because the cost of equity (in terms of investors’ required rate of return) is usually higher than debt. This could lead banks to increase lending rates, lower deposit rates, and/or tighten credit standards in order to retain their expected return on equity.

However, in reality, the impact on the lending and deposit rates will be affected by a range of offsetting forces.

The extent that banks will be able to pass on their potentially higher funding costs – in the form of higher lending rates and lower deposit rates – will be constrained by:

• competition from both within the banking sector and alternative

sources of funding (for example, capital markets); and

• other interest rates in the economy being broadly unchanged, or

lower, as risk premia in New Zealand decline.

Hard to argue with most of that (I would make an exception for the second bullet).

They went on to elaborate that particular point (a little)

The increased stability of the banking system should reduce the risk premium associated with investing in New Zealand. This results in a reduction in the expected frequency and severity of economic disruption associated with systemic financial crises.

Summing up

In the long run, bank lending rates are likely to be slightly higher. How much higher depends on a range of factors, such as how much the cost of equity and debt for banks declines, the degree to which risk premia in New Zealand fall, and how competitive pressures affect banks’ ability to pass on costs to customers in the form of higher lending rates or lower deposit rates. The Bank expects that the spread of banks’ lending rates to the rates at which they borrow will settle in the range of around 20 to 40 basis points higher as a result of the proposed changes, although the exact effect is uncertain.

And then there is a further claim

Higher bank capital requirements could also improve the government’s fiscal position. A higher share of bank equity funding would likely increase tax revenue from the banking sector since debt funding is tax-deductible while equity funding is not. The value of any perceived implicit public guarantee of the banking system would also be reduced as the system becomes safer, improving the government’s credit profile.

And there was a final interesting observation

If implemented, changes to bank capital requirements are likely to affect economic conditions through a number of channels.

At his press conference that day, the Governor was also quizzed extensively about the capital proposals. In the course of that press conference the Governor told the assembled media that the proposed capital requirements would be “well within the range of norms” seen in other countries.

All of which was interesting, but supported (on the day) by no further analysis. And so I lodged an official information act request

I am writing to request copies of any analysis undertaken by or for the Bank in support of Box E in today’s Monetary Policy Statement, including (but not limited to) the numerical estimate of the impact on the banks’ lending margins.

I am also requesting any material/analysis used to support the Governor’s claim (at the press conference) that the proposed capital requirements will be “well within the range of norms” seen in other countries. I would note that there was no such supporting material in the Bank’s consultative document.

And finally on Monday, having had the request extended for a month to allow for, as they put it, “ongoing consultations” I had my answer.

I have tended all along to assume that the Bank would have done extensive and detailed analysis, and would have been keen to get that analysis out into the public domain to, as they would see it, strengthen the case for the proposals they clearly believe to be in the public interest.

But the evidence is increasingly against that presumption. The response from the Bank is here. There was only six pages of it. There is, apparently, one (possibly substantive) paper

Paper 1.6: What might higher bank capital requirements mean for monetary policy?

But they simply refuse to release any of that, on principle.

The second document is a single page exercise in arithmetic, described as

Table: Stylised example of the pricing impact of different required returns on equity

I did not check every calculation but I have no reason to doubt the numbers are what they say they are. It is the sort of exercise a new graduate should have been able to churn out in a couple of hours. It appears to be the source of the suggestion that bank lending margins might widen by 20 to 40 basis points. But – being a stylised example in a simple table – there is no discussion or analysis about whether the scenarios are the correct ones, no engagement with estimates other analysts have come up with, no discussion of (for example) whether for the wholly-owned Australian banks (which dominate the market) group earnings variability etc might not be a relevant metric (shareholders in ANZ Banking Group probably do not great care whether the profits – mean and variance – come from the New Zealand operations, the Australian operations, or anywhere else in the world). Just nothing.

There is no discussion or analysis of those (entirely reasonable) points in the MPS about the extent of competition from entities not subject to the capital requirements, possibilities of disintermediation and so on. Nothing.

There was also, apparently, nothing to support the claim made by the Bank that overall New Zealand interest rates would fall if the capital proposals were adopted, and nothing to support (or quantify) the suggestion that the capital proposals might be fiscally positive (recall that in his speech a few weeks later, Geoff Bascand suggested that the proposals would permanently reduce the level of GDP by up to 0.3 per cent, which would surely also have some fiscal consequences).

And that was that on the material in the two page box: one page of arithmetic. Breathtaking really.

The rest of the release was devoted to material to support the Governor’s claim that the Bank’s proposed capital requirements would be, in the words of the Governor, ‘”well within the range of norms” in other advanced countries.

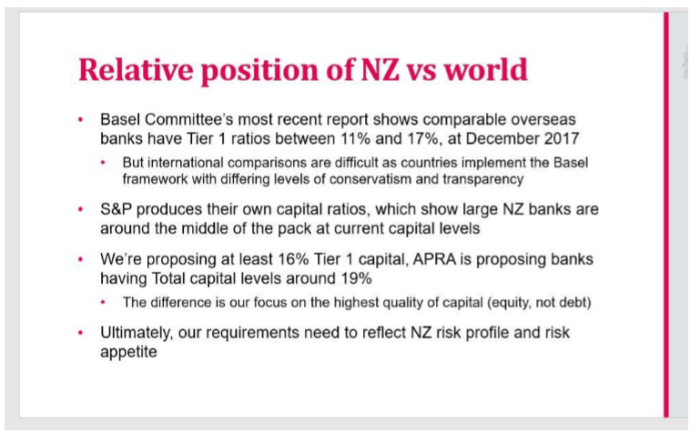

One piece they released was this slide they had used in a presentation to the Minister of Finance on the day the Governor made his public comments.

The comparisons with Australia – surely the most relevant? – are simply asserted, with no supporting evidence or analysis (nothing that, for example, recognises that the Reserve Bank is proposing to pull up the floor (on the weights used in calculating risk-weighted assets in the first place) much further than Australia has done). Nor do they acknowledge to the Minister that the sorts of capital they propose to rule out not only does the job in the event of a bank failure (and bank failures of trans-Tasman banks are inevitably going to be handled in a trans-Tasman way), but is much less expensive than what they are proposing to require.

In any case, this slide is not analysis, and we do not gain any insight from being told that the Governor told the Minister the same as he told the journalists. In reality, it seems to be enough for the Bank to say it is “hard to do” the comparisons, so do not expect us to do them.

You will have noticed a couple of other comparisons on the slide. They are covered a bit more extensively in a document described as

Media resource: international comparisons of bank capital ratios, 12 December 2018

That was the day before the consultative document was released. Presumably some people have had this document for months, and yet the Bank took two months to release it under an OIA.

Among the shonkiest bits of the document is a comparison (using World Bank data) of the unweighted 2017 ratio of total capital to total assets. Of the seven other countries they choose to cite, New Zealand conveniently would sit almost bang on the median But so what? First, these proposals are to markedly increase the amount of capital banks in New Zealand have to hold: in fact on the numbers the Bank uses in that stylised table (see above) total capital to total asset after these changes were implemented would be above those of any of the seven other countries the Bank sought to compare us with. And second, and perhaps more importantly, the reason why capital frameworks focus on risk-weighted assets is that not all assets have similar risk characteristics: the balance sheets of New Zealand banks, for example, look very different to those of US banks.

But I suspect the Bank itself doesn’t really regard that data as relevant. They seem to put most weight on the S&P framework, and some on the BIS comparisons. I dealt with both of those at some length in my post on Geoff Bascand’s February speech. Of the BIS comparisons I noted then

All else equal, a 16 per cent capital ratio calculated on Reserve Bank rules could easily be equivalent to something like 19 per cent in many other countries’ systems. And not even the 95th percentile of G-SIB banks will – according to the BCBS table – have a Tier 1 capital ratio of 19 per cent.

But here is the rather plaintive tone of the Bank’s comments in the 12 December document, finally released now.

“We acknowledge that there is a genuine interest…..which cannot easily be met”. Give us strength. Well, give us a rigorous and robust official agency, because on this sort of evidence we certainly don’t have one at present.

Here is some of what I wrote about the S&P numbers in February

The rating agency S&P engages in its own attempt to calculate risk-weighted capital ratios for a large number of banks, using its own risk-weighting framework. But a great deal depends on the “economic country risk score” the S&P analysts assign. And they take a dim view of New Zealand, assigning us a score of 4 (on a 10 point scale). Here is what that means for housing risk weights

And there are similarly large differences for the corporate risk weights.

As I said, S&P gives New Zealand a 4. But Sweden, Norway, Belgium, Switzerland, and Canada all get a 2. You might think there are such large systematic economic risk differences between New Zealand and those countries, but I doubt the Bank really does, and I certainly doubt. I wrote about this a few years ago where I noted

The S&P model appears to put quite a lot of weight on New Zealand’s relatively high negative NIIP position. But I think they are largely wrong on that score too. First, the NIIP/GDP ratio has been fluctuating around a stable average for 25 years now. That is very different from the explosive run-up in international debt in countries such as Spain and Greece prior to 2008/09. But also the debt is largely taken on by the government (issuing New Zealand dollar bonds) and the banks. No one seriously questions the strength of the government’s balance sheet, or servicing capacity, even after years of deficits. And the ability of banks to borrow abroad largely depends on the quality of their assets and the size of their capital buffers. If asset quality really is much poorer than most have recognised, rollover risk could become a real problem, but it isn’t really an independent source of vulnerability.

Score us as a 3 or even a 2 and suddenly the Deputy Governor’s chart will have the implied capital ratios for New Zealand banks a lot higher.

The Bank knows all this, but despite attempting to rely on these numbers they make no effort to highlight the limitations (and there are others with the S&P methodology).

As I noted in that earlier post

There aren’t easy right or wrong answers to some of these issues, but the uncertainties just highlight how much better it would have been if the Reserve Bank had engaged in an open consultative process at a working technical level, before pinning their colours to the mast with ambitious far-reaching proposals.

(Incidentally, I see that I also made this point in February.

As another marker of what is wrong with the process, the Deputy Governor told us yesterday that the Bank will be releasing an Analytical Note on the Bank’s estimates of the costs of their proposals: it will, we were told, be out in a “couple of weeks”, by when two-thirds of the (extended) consultative period will have passed.

That Analytical Note still hasn’t been published.)

In truth, despite the Governor airily declaiming that his proposals are nothing to worry about, and comfortably within the range of international requirements, so far they have produced no evidence or analysis that could lead reasonable observers to share his confidence. That simply isn’t good enough.

There is no sign, for example, that the Bank has ever seriously engaged with APRA and in a mutual process sought to robustly assess how each regulator’s proposals would apply to the same portfolio of assets. If the two agencies both agreed on the results, I’d probably be persuaded (not necessarily that we need such high ratios, but on the relative demandingness of the two sets of rules themselves). Similarly, they have made no effort to sit down with the regulators in the countries with the (apparently) most demanding capital rules (Sweden?) and look at how their rules and those the Reserve Bank are proposing might work out (in terms of required capital) for the same portfolio of assets. It might not be easy to do, but….that is what we fund the Reserve Bank and pay Reserve Bank staff for. There are huge amounts of money involved here (my former colleague Ian Harrison called it The 30 billion dollar whim and, on a quite different approach I suggested that the Bank’s own guesstimates of the real economic costs could easily capitalise to $15 billion).

With no sign that the New Zealand financial system is imperilled – recall that the Bank itself tells us every six months that it is strong and stable – there is no obvious a priori case for much higher capital requirements: any such case needs to be made rigorously, in detail, with lots of careful scrutiny. In other words, in ways quite unlike how the current ambitious proposal has been done. It may have been the outcome of a meandering multi-year process (on lots of things other than the minimum ratio), but in the end it looks a lot like the fruit of a gubernatorial whim, without even the decency of constructing a robust ex post rationalisation that would withstand serious scrutiny.

That simply isn’t how policy in a serious country should be made. And the frightening thing about the New Zealand system is that if the initial proposal was one man’s whim, the same one man is the final decision maker: prosecutor, judge and jury in his own case, with no subsequent rights of appeal. There is no decisionmaking board, no separation of management from final decisionmakers, no powers for the Minister of Finance to have any say. Just one unelected man pursuing a whim.

(If you still happened to think that policy advice in New Zealand was that of a serious country – actual whether you do or don’t – don’t miss checking out Eric Crampton’s post yesterday on a new adventure and enthusiasm for The Treasury. As a flavour

Imagine surprising Aotearoa with a strain of compassion so delightful that it re-wires our collective consciousness!

Don’t miss clicking through to the feelings game. You too might want to spend $113.85 on a set of feelings cards, devised by a business set up by a former Treasury staffer who

She saw an opportunity for her and other people within the Ministries to more deeply, creatively and energetically serve New Zealanders by bringing more of their hearts to work and being able to more empathetically connect with colleagues, staff and service end users.

Spare us. As one of New Zealand most eminent economists, now resident in Canada, put it “if I were dead, I’d be rolling in my grave” )