There seem to have been more than a few people on the left pretty deeply disillusioned with the Prime Minister after she walked away from the possibility of a capital gains tax, not just now (when the parliamentary votes for it probably couldn’t be found) but at any future time while she is Labour leader. Some parallels are drawn with John Key ruling out doing anything about raising the age for New Zealand Superannuation while he was leader – an important difference perhaps being that Key had never evinced any enthusiasm for such a policy, only to recant, let alone been the leader who put the issue back on the table. Perhaps something closer was Key’s refusal to use whatever “political capital” he had to do anything much useful around economic reform. But, again, despite occasional encouraging rhetoric while in Opposition, no one ever really thought Key was someone who would rock the boat, or was that bothered about doing useful longer-term stuff, as opposed to holding office and managing events as they arose). Some, perhaps, thought Ardern was different.

But in the wake of the Prime Minister’s abandonment of the possibility of a CGT – and whatever (quite diverse apparently) hopes people pinned to that quite slender reed – there is the growing question of what, if anything, the government might actually do. It is, after all, in their phraseology, supposed to be the year of delivery.

In his Political Roundup column yesterday, Bryce Edwards posed the question as “What will Labour do about inequality now?”. There is a lot of talk about different possible tax reforms – I might even come back and look at a couple in later post – and some reference to the forthcoming “wellbeing budget” (which can surely only disappoint, given the self-imposed fiscal constraints). But there was nothing about the option most directly under government control which would probably make the biggest tangible difference to the most people, with clear efficiency gains not losses, and with the possibility of a considerable degree of across-Parliament support: fixing the housing and urban land market at source.

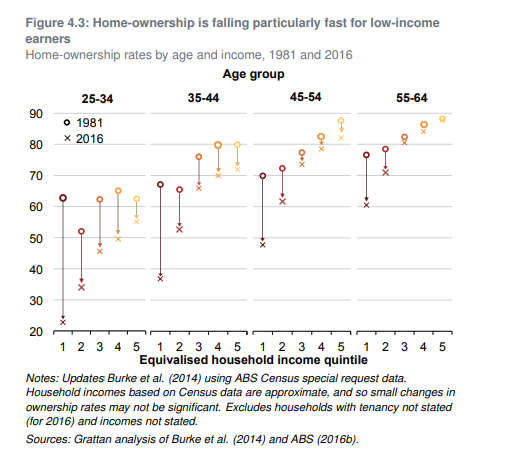

As a reminder of the symptoms of the problem, I ran this chart in my post earlier in the week. It is Australian data, but the picture seems unlikely to be much different in New Zealand.

The young and the poor (especially the young poor, and probably especially the Maori and Pacific young poor) are increasingly squeezed out of the possibility of home ownership, for decades or at all. There is no good economic or social case for tolerating this systematic penalisation of the more marginal groups in our society.

But there are obstacles to reform, including the economic interests of those who could suffer quite seriously – through no real fault of their own – if the situation was fixed.

Some elements of the government – well, really only one, the Minister of Housing – talks a good talk. In a recent speech he talked up the prospect of reforms that the “flood the market” with development opportunities and thus lower, presumably quite considerably (when you use a strong word like “flood”), urban land prices. It warmed the hearts of many (mostly rather geeky) readers, including me. And yet I’m very sceptical that it will come to much. As I noted in a post shortly after the speech

And yet, I remain sceptical. Perhaps Phil Twyford’s heart is really in this.

But is the Prime Minister’s? Even though housing was a significant campaign issue, even though she has been in office for 18 months now, we’ve never heard her putting her authority behind fixing the housing disaster at source, let alone substantially lowering house prices.

And is the Green Party on board? Quintessentially the party of well-paid inner-city urban liberals, are they really on board with bigger (physical footprint) cities, or with encouraging intense competition among landowners for their land to be developed next. Some of them seem to believe that it would somehow be morally virtuous – and “solve” the affordability issues – if people lived instead in today’s equivalent of shoeboxes.

The approach of the Wellington City Council – led by one of Labour’s rising figures – just reinforced my doubts.

There are various practical issues to be worked through in any serious reform effort. But one consideration that always seems to play on the minds of politicians (understandably enough I guess) is that lower house prices means lower house prices: in other words, people who currently own a house will find their asset worth a lot less than it was. For those of us without a mortgage on our primary residence or with only a modest remaining mortgage, such a fall wouldn’t matter at all. Our natural position is to own one house, and we intend to own one house (perhaps a different one) well into our dotage. The label (the estimated value) attached to that property doesn’t really matter. And for our kids hoping to enter the market in the next decade or two it is pure gain.

But it, understandably, feels quite different if you are one of the growing number of people who have taken out a very large mortgage (perhaps 80 per cent or more LVR) to get into a house. If someone talks of halving house prices, that can sound pretty threatening. As a result, very few politicians ever do (I recall Metiria Turei doing it, but only once, and……). Banks have the legal right to call in their loan if the value of the collateral (the house) drops below the outstanding value of the loan, and although they probably wouldn’t do so in normal times – when the labour market was okay – it leaves people feeling quite vulnerable, and also quite trapped (hard to move cities if selling would immediately crystallise a large loss).

When house prices first shoot up there aren’t many people affected that way. The longer they stay high – five or six years now of the latest surge up – the more people have taken out mortgages based on the high house and land prices. Most of the owner-occupiers among them aren’t business operators or “speculators”, just people at a stage of life where they want to settle and to be secure in a place of their own. And they – and their parents – vote.

Of course, there is a whole other class of people who would lose from house and land prices coming down. But mostly they are a less sympathetic group. There are the “landbankers” – people who responded to government-created incentives – to sit on potentially developable and let the artificial scarcity push up the price of their asset. That’s a business operation, and in business you win some and you lose some. Risk is at the heart of business, and that means the possibility of real and substantial losses. And there are those in the residential rental business, many of them (especially recent entrants) quite highly leveraged. Halve the price of city properties – and that is what re-establishing sensible price/income multiples would imply – and many of those owners would be either wiped out, or see their real wealth (real purchasing power for things other than houses) very dramatically reduced. But, again, it is a business, and business implies the possibility of gains and losses (one reason I was always at best ambivalent about a CGT was that no real world CGT really treated gains and losses symmetrically).

Of course, these business owners vote too, and will lobby intensively. But (a) there are fewer of them than mortgaged owner-occupiers,(let alone unmortgaged renters, hoping to be mortgaged owner occupiers) and (b) they just don’t command the same public sympathy (and rightly so) – we might sympathise with any business owner whose operation falls in hard times, but we know that is the nature of business.

Back when Jacinda Ardern first became leader of the Labour Party I did a post on what a radical reform package, that might really make a difference to our economic woes (housing and productivity), might look like. Buried in that post was a suggestion for a partial compensation scheme for mortgaged owner-occupiers that might help smooth the way towards overdue structural reform. I noted then the desirability of getting house prices down a long way.

No one will much care about rental property owners who might lose in this transition – they bought a business, took a risk, and it didn’t pay off. That is what happens when regulated industries are reformed and freed up. It isn’t credible – and arguably isn’t fair – that existing owner-occupiers (especially those who just happened to buy in the last five years) should bear all the losses. Compensation isn’t ideal but even the libertarians at the New Zealand Initiative recognise that sometimes it can be the path to enabling vital reforms to occur. So promise a scheme in which, say, owner-occupiers selling within 10 years of purchase at less than, say, 75 per cent of what they paid for a house, could claim half of any additional losses back from the government (up to a maximum of say $100000). It would be expensive but (a) the costs would spread over multiple years, and (b) who wants to pretend that the current disastrous housing market isn’t costly in all sorts of fiscal (accommodation supplements) and non-fiscal ways.

If I recall rightly, I came up with the rough suggested parameters as I was typing, but a couple of years on it still looks like the sort of thing that might be worth considering, perhaps with a larger cap on the maximum payout and a restriction to a first (owner-occupied) home. The expected cost will have escalated since 2017, because we have had another couple of years of people taking our large mortgages on properties with values inflated by government-controlled regulation in the face of trend increases in demand), but so has the number of people unable to do what they would otherwise “naturally” do; purchase a first house in their mid to late 20s.

This is a sketch outline of a scheme, and like all such government schemes would need lots of detail to limit abuses. But what are some of the features of the scheme:

- you only get to lodge a claim if you sell your house (someone who is going to stay in the same house for 50 years doesn’t need any explicit compensation, even if they are left with a heavier servicing burden than might otherwise have been possible if they’d waited to buy). Of course, some people will choose to sell and buy somewhere different just to crystallise the right to make a claim, but selling a house – a genuine arms-length transaction – and moving isn’t cheap.

- the nominal price has to have fallen more than 25 per cent to be able to make a claim at all. For the last few years LVR restrictions have meant that most owner-occupiers have been borrowing only 80 per cent of less at purchase, and there will have been some principal repayments since then. Relatively few people would be in a negative equity position if their house price fell by 25 per cent, and even fewer would be facing immediate pressure from their lender. Owning an asset has to mean some exposure to reasonable swings in price.

- beyond a 25 per cent fall, you could claim back up to half of subsequent losses from the government. Thus, if you had bought an $800000 first house and the price halved, you would be eligible to claim $100000 back from the government (half of the difference between $800000 and $400000. On reflection, and with such a large deductible (the owner takes the first 25 per cent loss) it might be more appropriate for a compensation scheme to cover 75 per cent of subsequent losses (in this example $150000).

- any such scheme should have a maximum payout capped. There is no obvious justice in paying out large amounts to a couple who happened to buy a $4 million house which then halved in price (there was a similar issue when the government bailed out AMI).

I don’t have a good sense of how large the cost might be (but it would be in the billions, spread over at least a decade). Unfortunately, I’m not one of those who believes that fixing the housing market would produce significant productivity gains for New Zealand – so it isn’t by any means a free economic lunch – but the sheer injustice of what successive central and local governments have done to our young and poor cries out for action, and sometimes it is worth offering compensation to help pave the way for the sort of thoroughgoing reform that is desperately needed.

Fixing the housing/land market at source would be a huge step to improving the economic and social wellbeing of so many. Compensating some of the more sympathetic of the losers from such a reform – most of whom won’t be in an overly strong financial position themselves – shouldn’t offend too many canons of justice. In an ideal world, one might seek to finance such a scheme from those who benefited greatly from the previous (well, current) rigged market – but that would be hard to do. In the real world, we are fortunate that the government has fiscal surpluses and very low net debt (especially including the politically managed money pools in NZSF).

I’m not optimistic the government (Prime Minister) really has much interest in addressing the housing/land problems at source. But if she is ever is tempted to take seriously Phil Twyford’s rhetoric, a compensation scheme of some sort might be an option to consider, to help dull the inevitable opposition in some quarters (some purely from business interests who would have misjudged, but some from people who through little fault of their own became trapped by these longrunning government policy distortions, that generated the scandal of the New Zealand housing market).