BusinessNZ describes itself as “New Zealand’s largest business advocacy body”. Its chief executive, the lobbyist Kirk Hope, seems to have easy access to the op-ed pages of the Dominion-Post newspaper, and I’ve critiqued a couple of his columns (here and here) earlier in the year.

Hope – and presumably BusinessNZ – is a big fan of high levels of non-citizen immigration to New Zealand. Business groups have been for decades – as far as I can tell, through all the decades of New Zealand’s relative economic decline. We’ve had some of the highest controlled immigration flows of any country, and one of the worst relative economic performances. However large the inflow it is never seems to be enough for the Manufacturers’ Federation (in decades past) or BusinessNZ now. I have in front of me, the memoirs of Fred Turnovsky, twice head of the Manufacturer’s Federation and one of the “great and the good” of an earlier generation, where he records a lecture he gave at Waikato University in 1971 calling for a doubling in the officially proposed immigration target.

Earlier this week, following the government’s migration policy changes, BusinessNZ had a press release out – under the heading Migration rules a sign of progress – which seemed to welcome the changes. I was quite surprised, but on closer inspection it wasn’t the small drop in the residence approvals programme target they were welcoming, or the cutback in the family quota (mostly non-working older parents), but simply the increase in the points requirement.

“Increasing the points required by skilled migrants to gain residence from 140 to 160 will help sharpen the annual intake towards higher skilled people.”

But, of course, increasing the points requirement isn’t an independent policy adjustment, it is just the logical corollary of a likely increase in demand for residence (mostly because of the large inflow of foreign students in recent years), while the availability of skilled migrant places hasn’t changed. When demand changes the “price” needs to adjust.

And thus far I agree with Hope. If we are going to allow in lots of “skilled” migrants, the more skilled they are, the better. Of course, it is always hard for officials to detect skills, which makes it too easy to fall back on paper qualifications.

In an op-ed earlier in the year, Hope made the case for high levels of immigration to New Zealand on the grounds that we needed lots of immigrants to pay for our superannuation.

Restricting immigration as proposed would harm the economy.

With a birth rate just above replacement level, an ageing population and baby boomers retiring, we need immigrants to sustain the economy and pay for our superannuation, just as in decades past.

In response I noted

And on the NZS side of things, if there are affordability challenges with the current system, we have it in our own hands to modify the system to make it more readily affordable. We could raise the age of eligibility – National knows it needs to happen, even if the Prime Minister has pledged not to, and Labour campaigned for a higher age at the last election. Other countries have made these sorts of changes. We could also age-index NZS eligibility. We could modify the entitlements of those who haven’t spent most of their working lives in New Zealand. And there are other options I don’t support, but which would also ease the fiscal pressures, such as income and asset testing, or linking NZS increases to prices rather than wages. And we can keep the way open for more older people to stay in the labour force for longer – on that count, we already have one of the least distortionary old age pensions systems anywhere. We are quite capable of managing the pressures ourselves.

Large scale immigration might make a small difference to NZS affordability, but it is an awfully big intervention for a really quite small difference. As it is, New Zealand’s birth rate is around replacement, unlike many European and Asian countries, so the ageing population issues are in any case less pressing here than in most places.

In the end, the best way to support the various social spending commitments society wants to make is to foster a highly productive economy. We’ve kept on failing to do that, and while immigration policy almost certainly isn’t the whole story, there is no evidence whatever that high rates of immigration have improved the position.

Strangely, the affordability of NZS seemed then to be his main argument for large-scale immigration.

But I suspect that was just an attempt to try to frame the issue in a more generally acceptable way. In fact, business lobby groups in New Zealand tend to make the case for high levels of immigration largely in terms of keeping the cost of labour down. Of course, they don’t put it in quite those words. Instead, the constant refrain is “skill shortages” is mostly just another way of saying “I can’t get enough workers at the wage I want to pay”. Markets have ways of taking care of looming shortages, or surpluses: the price adjusts. We don’t hear of shortages of foreign exchange – the price adjusts. The availability of tomatoes varies with the seasons and storms, but almost always any consumer can buy as many tomatoes as he or she wants, at a price which adjusts (up and down) quite frequently.

When it comes to people, and labour markets, these mechanisms don’t work instantaneously. But markets take care of structural shifts in the demand for labour, if they are allowed to work. A commenter argued earlier this week that we need lots of immigration to provide the workers to care for a growing elderly population. No. Immigration is certainly one option – look at the staggering number of aged-care nurses we’ve granted visas to in the last decade – but so are changes in relative prices. If the demand for labour in that sector increases, then over time relative wages in that sector will tend to rise. In turn, that will draw more New Zealanders to the sector, and will also reward investing in some more labour-saving technologies. The same goes for almost any sector. The wages changes might be small, if labour moves easily into the new in-demand sector, or large, if there is some reluctance of people to move into those roles. But that is how the labour market would deal with shifts in the patterns of labour demand, if allowed to do so.

But to return to BusinessNZ. Kirk Hope has another op-ed in the Dominion-Post this morning. It is a useful piece because it is so explicit about his – and his organization’s (?) -views. Here is what he has to say:

One in four people in New Zealand is foreign-born, and many New Zealanders routinely leave to live in other countries.

This is what New Zealand is like – it’s ‘migration central’, awash with people coming and going, and it has always been this way.

This is simply quite historically misleading. Large short-term migration is a new phenomenon – we saw nothing like it in earlier decades. And while it is no doubt true that “many New Zealanders routinely leave to live in other countries” – I’ve done it three times – the net outflow (the loss of almost a million New Zealanders) dates from when the growing gap between living standards in New Zealand and those in other advanced countries (especially Australia) started to become more apparent. In successful countries, not many people leave for long. Compare the net outflow of Norwegians from Norway with the net outflow of New Zealanders from New Zealand and you’ll see what I mean.

Business has long asked for more immigration…

You can’t get clearer than that. We have probably the second largest controlled immigration programme in the advanced world (behind that other economic laggard, Israel), a residence programme three times the size (per capita) of that in the United States, large and growing numbers of short-term work visas, and still it just isn’t enough for business.

He elaborates

….as in more access to more skilled migrants to do the jobs that New Zealanders aren’t available for.

But as even Hope recognizes, in this and his earlier article, New Zealand hasn’t done very well at attracting really skilled migrants in recent decades. Which shouldn’t really surprise anyone; after all, New Zealand is an awfully long way from anywhere (ie home and family), and simply doesn’t offer as good material living standards as many other advanced countries (including such migration recipient countries as Australia and Canada) do. We haven’t been doing well at getting the best people to date, so why should expect to do better if we aim for even more migrants?

And Hope never once refers to the OECD data, cited by Steven Joyce and MBIE, suggesting that New Zealand workers’ skill levels are already among the very highest in the OECD (and the average immigrant had, on those measures, slightly lower skills than the average native). Perhaps he doesn’t believe the numbers, but if so perhaps he could lay out his specific concerns with the data. As I noted in my earlier post on that OECD data

Importing people doesn’t look as though it has been a means of raising skill levels here, or in most other countries. In general that shouldn’t be surprising – successful countries solve their own problems, and when they succeed they might share their bounty with newcomers. But a different sort of people is very rarely the answer to serious economic challenges.

But to revert to Hope

the points system will be able to deliver higher skills, but not necessarily the specific skills in most demand.

It might not answer the specific need for more engineers, construction managers, quantity surveyors, technologists, technicians and ICT workers – the actual skills needed today.

Fortunately, there is work underway to achieve more weighting in the points system to achieve specific skills such as these.

This is a sort of line he has run before and I commented then.

it is curious to see the leader of a business group reckon that he knows what skills and what industries will be the ones that will prosper in a future, more successful, New Zealand. And it is puzzling to see so little faith placed in the workings of the labour market, or the skills and capabilities of New Zealand. It is redolent of some sort of 1960s indicative planning mentality – the sort of line of argument I have previously criticized MBIE for.

BusinessNZ tell us they believe in markets, private enterprise etc etc, but in fact they seem to want to shape our long-term migration policy around the ability of people like them – and MBIE bureacrats – to work out quite what skills “the economy” needs right now. Even though, in granting residence to a 25 year old, we are bringing in someone who might have 40 year plus of working life in New Zealand. No one knows, or can know, what specific skills will be needed over that sort of horizon. If we are going to bring in long-term migrants, with an economic focus, lets attract able, energetic, skilled people, with a realistic chance of adapting well to New Zealand, and not try central planning beyond that.

Hope goes on

Business will be hoping this work comes to fruition soon.

Without it, we face the danger of a breakdown in the political consensus around migration policy

If we are not able to import migrants with the specific skills needed, there will be little support for bringing in many migrants without them.

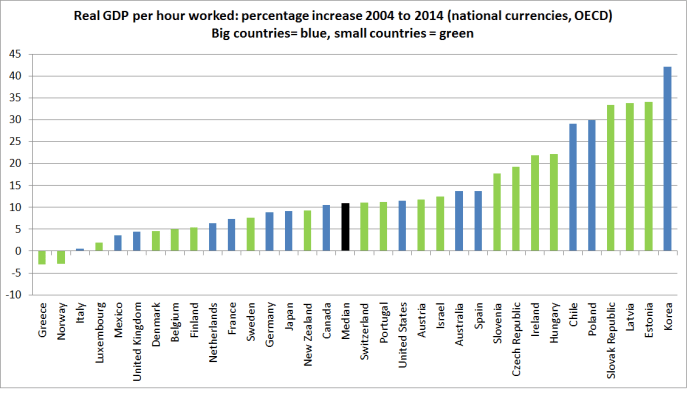

To the second sentence, I can only add “I hope so”. There is just no evidence – from BusinessNZ, from the NZ Initiative, from MBIE, from Treasury, from National or Labour ministers – that the strong elite consensus in favour of high levels of non-citizen immigration has done anything, at all, to benefit the economic performance of the New Zealand economy as a whole. Perhaps it might produce such benefits in some times, some locations. But our focus in on contemporary New Zealand – this specific location. Of course, the economy is bigger – there are lots more people – but there is no evidence, at all, that GDP per capita, or GDP per hour worked for New Zealanders are better as a result. And that really should be the test, and especially in programme that is avowedly focused on the claimed economic benefits of the programme. There is no more reason to simply assume that putting an extra million people in New Zealand – roughly what our immigration policy has done in the last 25 years – would make any more sense than putting an extra million people in Wales, Scotland, Tasmania or Nebraska, if local territorial authorities in those places had control of their own immigration policy.

And what of that final sentence? For all I know, it might be descriptively accurate, but actually I suspect there is little support now for “bringing in many migrants without them [skills]”. Why would we, refugees aside? There might be a case for attracting some really highly-skilled immigrants (not tied to specific current vacancies), but why would we want to bring in people with very limited skills. At best, doing so could only drag down the relative returns to relatively lowly-skilled (absolutely or relatively) New Zealanders. At worst, it could drag down our overall economic performance.

Hope goes on

These generalisations are not true. The fabric of New Zealand life, rather than being destroyed by immigration, is largely the result of ongoing immigration and is colourful, interesting and diverse as a result.

My focus in on the economic dimensions of the issue, but as a reminder – and with no suggestion of causation – living standards in New Zealand (relative to those in other countries) were probably at their best in the 1950s, a period of a great deal of cultural homogeneity in New Zealand. Large scale immigration – particularly from different cultures than the native population – changes societies, and there are likely to be both pros and cons from those changes. If a country has meaning – other than just a physical location – it must involve something around shared identity and values. If the economic gains from large scale immigration are slim or non-existent ( as I argue in the New Zealand case), one might want to examine more closely the other implications of large scale immigration – whether that is about environmental pressures, or the declining relative place of Maori (the original native population). But consciously or not, business lobby groups and their advocates tend to see little role for the nation state.

Having made his arguments about immigration, Hope attempts a pivot. Never having succeeded in showing that there are widespread economic gains from our immigration programme – let alone an even larger one – he turns paternalistic. The problem apparently isn’t large scale immigration, it is the low level of skills of many New Zealanders.

For this group, upskilling is their most pressing need.

This is why the education system needs our focus as debate on immigration continues.

There needs to be more help for unskilled adults to get upskilled in basic areas of literacy, numeracy, communication and computing.

I’m not going to dispute that skills matter, or that the education system (or some families) could do better in equipping people for life and work.

But fundamentally this is a distraction.

The data show that New Zealanders on average have a fairly high level of skills. Not everyone of course – here, or in any of those other countries. And, in any case, much of the education system isn’t about adding skills, but about signaling and ranking. We don’t have a high unemployment rate by international standards, or a low labour force participation rate (and here I agree entirely with BusinessNZ and the NZ Initiative that immigration does not raise local unemployment, or take jobs from natives). So focus on skills and the best possible design of the tertiary education system all you like, but it really is a different issue from the appropriate immigration policy for New Zealand.

Towards the end of his article, Hope sums up

New Zealand’s shortage of in-demand skills is one of the most important and difficult problems we face, and changes in education should be a hot topic.

We are a nation of immigrants and descendants of immigrants, and our economy needs ongoing migration to cope with the skills gap we have at present.

It is quite staggering to find the leader of (ostensibly) market-oriented business lobby group discuss the labour market, access to skills etc, and never once mention wages (sectorally, or across the board). His case might be more plausible if he stopped to engage with the counter-argument: why, over time, if there is a “shortage” of chefs (to take one of the leading skilled migrant categories) won’t relative wages for that set of skills rise, encouraging more people to (over time) shift towards those roles? None of these adjustments happen overnight, but the market process usually works if it is allowed to. But, of course, it is often just cheaper for firms to seek an overseas worker, than to lift returns to local labour across that set of skills. Or if he stopped to think macroeconomically for a moment – rather than simply at the level of the individual firm.

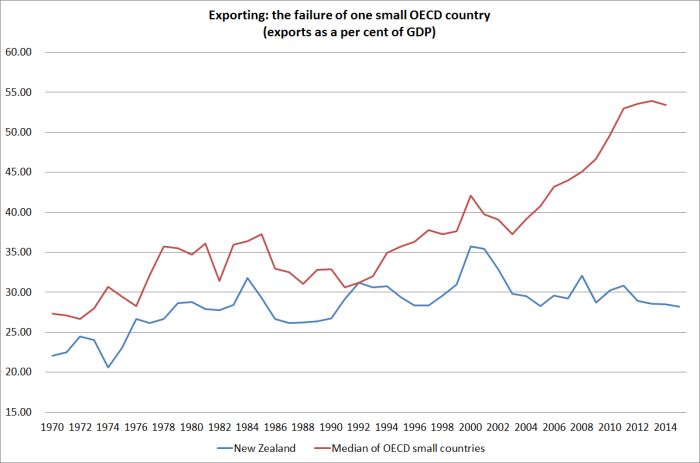

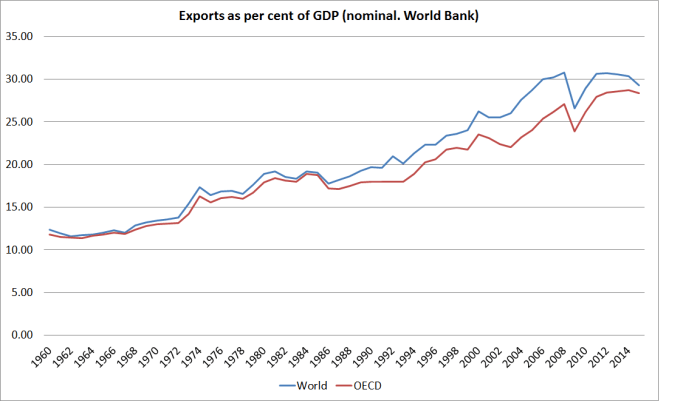

As for that final sentence, you have to wonder about which bit of the last 70 years of New Zealand economic history Hope missed. We have had high (by international standards) non-citizen immigration for most of that period, and yet constant employer complaints down through the decades about “skills shortages”. You’d almost suppose this was a really high-performing economy, with endless new outward-oriented opportunities and markets, crying out for people to tap those rapidly expanding markets. Instead, our relative economic performance has been in decline for almost the whole post-war period, and our exports as a share of GDP has gone nowhere – unlike almost every other advanced country – for the last 30 years. Perhaps BusinessNZ might like to reflect on the view – widespread among New Zealand economists in earlier decades (much to the dismay of Fred Turnovsky) – that large scale inward immigration programmes add more to demand than they do to supply in the short-term, and thus – at an economywide level – exacerbate rather than relieve “skill shortages”. Individual firms don’t experience it that way, but that is the value of macroeconomics.

I could go on, but I’d really urge BusinessNZ to think again, and if they do want to continue to champion really large scale immigration programmes, to find some credible arguments and evidence for the programme (specific to New Zealand), and to engage with the track record of New Zealand’s immigration programme and economic performance over the last 70 years. As they do, they might ponder the continued extremely high dependence of New Zealand on natural resource exports (perhaps 80 per cent on a broad definition), something that shows no sign of changing. Our stock of natural resources isn’t increasing, and there is little obvious reason to think that we’ve needed a lot more people here to make the most of what we have. Instead, we need to tap the smart and able people we do have, the strong institutions, and to get government out of the business of – unintentionally – persistently holding up the real exchange rate, and making it even harder than it should be to develop competitive firms based here. Markedly pulling back the immigration target – not just playing at the edges as the government has done this week – would be a big part of making that possible.

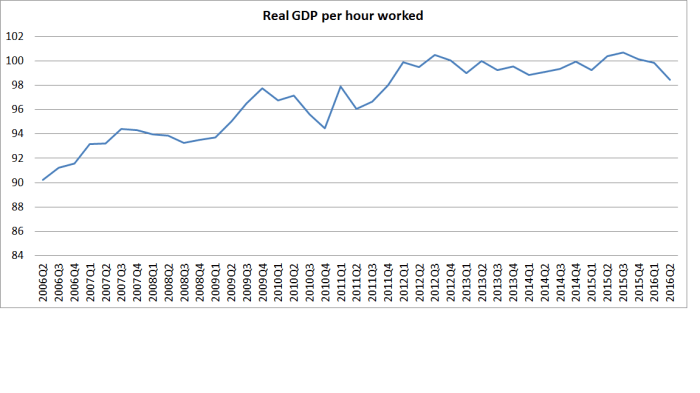

No productivity growth at all in the last four years or so (even ignoring the last observation, where there is an unfortunate discontinuity in the HLFS hours worked series).

No productivity growth at all in the last four years or so (even ignoring the last observation, where there is an unfortunate discontinuity in the HLFS hours worked series).