I noticed the other day a short piece on Treasury’s blog, written by one of their very able analysts, Mario di Maio, headed “How to get an export take-off“. It appeared to be prompted by the government’s now long-standing target to raise the export share of GDP by 10 to 15 percentage points by 2025. As I’ve noted before, the general sentiment behind the goal is probably broadly sensible – successful economics typically trade more (imports and exports) with the rest of the world. After all, the rest of the world is where the bulk of potential customers/suppliers are. Of course, the problem with this particular goal is that (a) it doesn’t look as though it is going to achieve itself (good bureaucratic technique can include setting goals for things that were likely to happen anyway, and then claim the credit when they do), and (b) the government is doing absolutely nothing to bring about the sort of transformation of the economy that might reasonably be expected to lift the export (and import) share of GDP. It is an old line, but no less true, that it is pretty crazy to keep on doing the same old thing, and expecting a different result. So perhaps they don’t really expect a different result….and perhaps they don’t even care greatly, as by 2025 no doubt the government will have changed, perhaps more than once, and Key, Joyce and English will be doing something else (as Clark and Cullen – who had similar vague aspirations – are now).

The Treasury note is worth reading. It takes a quick look at some countries (all now advanced) that have achieved a 10 percentage point increase in 10 years in the export share of GDP over the last 50 years or so. The author finds 14 such countries, and has a quick look for any common factors. Perhaps not surprisingly – in a note of three pages of text – he doesn’t find many. Indeed, he goes so far as to conclude

The diversity of the case studies cautions against drawing simple policy lessons from other countries for any New Zealand strategy to lift trade intensity. The diversity of approaches and circumstances means any single policy (or policy mix) would be misleading.

Personally, without a lot more background analysis – and perhaps Treasury has done the analysis but just not published it – that seems too strong a conclusion. If one were uncharitable, it could be seen as tending to avoid the real issues that specifically help explain New Zealand’s underperformance. But perhaps that wasn’t the intention at all, and all they really mean is that we have to think hard about the specifics of New Zealand, and not simply latch onto one or other favoured overseas country as an example. If so, I agree.

I’m not going to use this post to pick at specific points in the Treasury note, but wanted to come at a similar issue in a slightly different way.

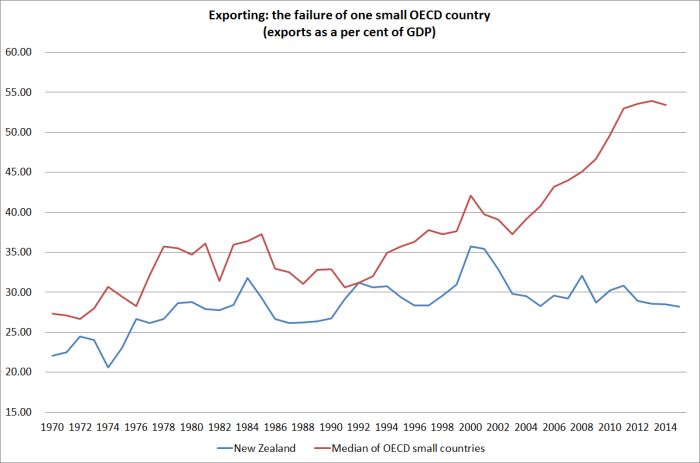

But first, lets remember quite how underwhelming New Zealand’s international trade performance has been. This is a chart I ran a few months ago, comparing New Zealand and other small OECD countries since 1970.

The foreign trade share of GDP has gone basically sideways for almost 40 years. It is hard – but not impossible – to get ahead with a performance like that.

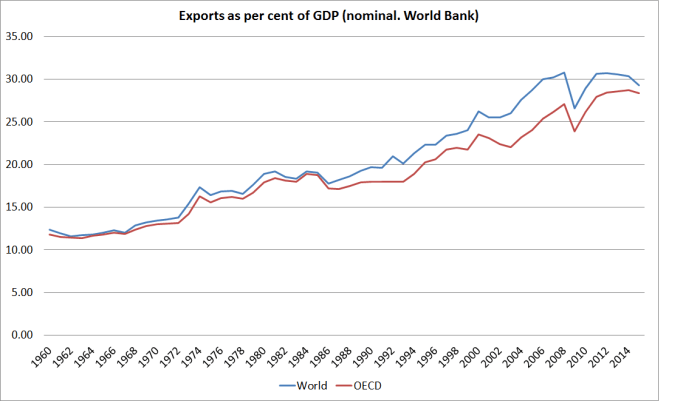

I usually use OECD data – as in the chart above – but the Treasury piece used the World Bank data, which has some advantages in capturing a wider range of countries. For some countries, and aggregates, they also have data going a bit further back.

Here is the World Bank’s estimate of exports as a share of GDP, for the whole world and for the OECD, back to 1960.

Over the 40 or so years when the export share of New Zealand’s GDP has barely changed, that for the OECD and the world as a whole has increased by between 10 and 15 percentage points. The trend – world, and advanced countries – has been strongly upwards, and somehow we’ve managed to defy that trend. Not all of that growth has been in export value-added, some has been the rise of global supply chains and the increased cross-border trade in componentry – something that is never likely to be a feature of remote countries’ trade – but that isn’t the bulk of the story by any means.

From the World Bank’s data, I picked out the advanced countries (OECD plus a few others), the emerging Asian countries, and Latin American countries (the latter mostly because they fascinate me, but also because they add a large number of countries that have underperformed for long periods). The official New Zealand export data start in 1971, so I had a look at how the export shares of the countries I had data for had changed from 1971 to 1975 to 2011 to 2015. Using five-yearly averages gets rid of some of the noise that arises from short-term exchange rate or commodity price fluctuations. Data don’t go back that far for most of the former Communist countries of Eastern Europe, but I was still left with a sample of around 45 countries.

Over that period, New Zealand’s export share of GDP had increased by 5.9 percentage points. Nine countries had had less growth in their export share than New Zealand.

| Change in export share of GDP : 1971-75 to 2011-15 (percentage points) | |

| Costa Rica | 5.70 |

| South Africa | 5.00 |

| Japan | 4.80 |

| Brazil | 4.30 |

| Guatemala | 3.70 |

| Israel | 2.90 |

| Norway | 2.80 |

| Colombia | 2.50 |

| El Salvador | -3.50 |

Of those countries, only Norway could be counted as am unambiguous economic success story over that period. All the others – like New Zealand – were underperformers at best. One might make an exception for Japan – until the late 1980s its economic performance was very strong – but then it is also worth remembering that at the start of the period exports as a share of GDP in Japan were only around 10 per cent of GDP (less than half of the export share in a small country like New Zealand). Over the period since the early 1970s, Japan has increased the export share of GDP by almost 50 per cent (from around 10 per cent to around 15 per cent) while the increase from New Zealand has been only around 25 per cent.

The Norway experience is a reminder that a large export (and import) share of GDP is not a necessary conditions for a sustained acceleration in economic (and income) growth. Then again, countries can’t count on discovering a huge new extremely valuable natural resource as a basis for improved prosperity. Typically the path to prosperity involves firms finding products and services they can sell successfully to the rest of the world. We’ve failed on that count, and that shows no sign of changing.

Although Treasury seems to want to play down the importance of the real exchange rate, I think that in the New Zealand context it is much more important than they suggest. One can never sensibly think of the real exchange rate is isolation from what else is going on in the economy. A country with fast productivity growth might find that its export share of GDP is growing even as the real exchange rate is high or rising – such is, say, the quality of the products or services firms in that country are selling.

But as everyone knows, New Zealand’s productivity performance over decades has been lousy, among the very worst in the advanced world. Sure we have a few years from time to time when things don’t look too bad, but the multi-decade pattern of underperformance is clear and shows no sign of reversing. Against that backdrop, it seems not just plausible – but entirely reasonable – to suggest that a real exchange rate that has been high or rising (rather than weak and falling) will, in the specific context of New Zealand, have been the main proximate contributor to the weak foreign trade performance (exports and imports).

I ran this chart recently. It only goes back 20 years, but over longer periods the picture is much the same. Our relative productivity performance deteriorated, but our exchange rate didn’t sustainably fall.

That sort of pattern typically happens only when some sort of domestic demand pressures keep holding up the real exchange rate (and domestic real interest rates). In a country with a modest national savings rate, government policies that result in rapid population growth are an example of just such a pressure. It is hard to foster an environment in which exporting is profitable/attractive when so much resource constantly needs to be devoted to meeting the (individually entirely reasonable) needs of a rapidly growing population.

Of course, “the exchange rate” can’t be fixed in isolation. It is a symptom of what else has gone wrong with the policies of successive governments. But like the old canary in a coal mine, the persistently strong exchange rate – in a country of such persistently weak productivity growth – is supposed to be a warning signal that something about economic policy is very wrong.

But why would we be surprised that nothing changes? The Opposition appears to have no compelling analysis or ideas, and we have a government run by a Prime Minister who in a recent interview declared that

Where would chairing the UN Security Council rank in your career highlights?

Right up near the top

I guess when there have been eight years of no substantive economic reform, no progress in improving the relative performance of the New Zealand economy, no progress in reversing decades of relative economic decline – just the pretence that somehow we are a global economic success story – we shouldn’t be surprised that chairing an ineffective meeting of foreign officials and ministers, dealing with an intractable problem in a far-away land, counts as some sort of career highlight.

Young New Zealanders, facing unaffordable houses, and the prospect of growing up in a country slowly drifting ever further behind, might perhaps have hoped for something rather more tangible rather closer to home.

Too much resource – capital, skills, labour – tied up in producer owned processing and marketing for our export sector to improve its performance. The hard question is how to change that.

LikeLike

NZ being isolated from the rest of the world has led to the development of a space launch pad for our latest homegrown satellite launching rockets. Perhaps the government should look at building on this cradle industry which seems to be perched on massive investment into the space tourism sector. Boeing has announced they will enter the race to put the first man on Mars, following SpaceX and China has announced similar lofty goals. I think there is a race on to get man to Mars within the next 10 years. SpaceX is planning to launch 1000 rockets each with 100 passengers to colonise Mars.

LikeLike

Nice to have you back, Michael. I hope you’re feeling better.

That wouldn’t be the first Treasury think piece I’ve seen that raises a really interesting question, then pulls its punches on the conclusion.

Contra the author, I thought there was a common theme to the countries they discussed, which is integration into trade with a larger economic entity, combined with a fierce desire to stay cost competitive (on an after tax, after exchange rate basis) relative to that large entity. It seems like they were prepared to pay a high cost for that competitiveness – it must have taken a lot of political capital for Korea to channel scarce capital to its export champions, for Ireland to maintain its low corporate tax and for Canada to deregulate – none of which are vote winning policies.

By contrast, I think your penultimate paragraphs nails how the political calculation has played out in NZ.

LikeLike

Thanks – getting back to normal slowly

I think that point about determination is an important one. Mind you, in the Canadian case – and Canada is another economic underperformer – the improvement wasn’t sustained. Exports/GDP now are about 32%, and were around 28% 30 years ago (with a quite a bit of variability in between).

LikeLike

Good to see you back Michael.

Re the comment the opposition party(s) not being up for much. There is an interesting speech from Phil Twyford obviously targeting a left wing audience but I think his core message will have a broader appeal. Basically he was saying that unaffordable housing is the political challenge of this generation. Much like responding to the great depression or the loss of trade links to the UK were challenges to previous generations of politicians.

http://www.labour.org.nz/housing_reform

Michael do you have any thoughts?

LikeLike

My ref to the Opposition parties was mostly about the overall economic underperformance/weak productivity growth. I quite like Twyford’s piece – without agreeing with all the details – and I’ll take him at his word that he is serious, but…..the National Party in 2008 used to put out quite good pieces of housing too , and of course they have done next to nothing. I hope the next Labour-led government really is different.

LikeLiked by 1 person

Yes loss of faith in politics/politicians is a growing problem. I think for the left it is more important to act in good faith as they have the more activist/progressive constituency, so if they do not follow through with promises it is more damaging to their ‘brand’. Whereas for the right, they are more about conserving the ‘status quo’ -so I think they get away with a greater degree of under delivery of promised progressive policies.

LikeLike

I wonder if there is much evidence that centre-left parties over the years have been more inclined to implement election promises than centre-right parties. I can think of plenty of individual counter-examples, but I’m not sure what the overall picture would look like. In this particular case, it is probably MMP I worry about more. Labour/Twyford have a particular set of policy preferences in this area, but they seem unlikely even to be the strongly-dominant partner in the next govt – plausibly they might have only 40-45 of the 61 seats, and the Greens have a different set of preferences. So one has to wonder (a) who will regard what as “bottom lines”, and (b) what a lowest common denominator housing policy might look like (perhaps lots of new state houses, in quite dense developments, within the existing boundaries of the urban area, and not much else?). I really hope not, and about how a next govt should be judged but – sadly – there still isn’t much sign of urgency (or traction for the message) over the housing disaster. Having done very little on anything, National is still polling much better than, say, Labour was in 2007.

LikeLike

I suppose my election promise proposition was a bit speculative, although given Phil Twyford is Labour’s campaign committee chairman then housing is likely to be a more important election promise compared to previous elections, so would be more difficult to renege on.

WRT MMP co-operation there is some evidence that Labour and the Greens can co-operate on housing issues. See this debate in Parliament, where they debated removing urban growth restrictions and on what grounds they could co-operate.

Phil Twyford http://www.inthehouse.co.nz/video/45199

Julie Anne Genter http://www.inthehouse.co.nz/video/45200

David Parker http://www.inthehouse.co.nz/video/45201

LikeLiked by 1 person

One thing I don’t really get: NZ has been importing capital for +20yrs despite a statistical productivity problem – surely superior short term real rates would be overlooked and ‘at some point’ the suppliers of capital would decide the the policy mix is wrong and divert their capital elsewhere? Or does the rising real exchange rate over the last decade ‘signal’ policy choices have been roughly right?

LikeLike

For each individual project, no doubt the returns are there – the non-tradables sector has grown quite rapidly in the last 15 years or so. but there hasn’t been much investment in the tradables sector – no growth in per capita tradables sector GDP for 15 years now.

Bear in mind tho that NIIP/GDP has gone roughly sideways for 20 years – in aggregate we haven’t been taking on lots of foreign debt.

Too me, all the high/rising exchange rate tells one is that there has been a lot of domestic demand, raising the prices of non-tradables (determined locally) relative to the prices of tradables (determined on world markets).

LikeLike

The high NZD is largely related to 3.3 million tourists spending up big requiring NZD to the tune of $11 billion a year. This then provides fundamental support to the speculation of $500 million NZD traded every single day by international speculators. NZD is the 10th most traded currency in the world.

LikeLike

A bit of a tangent. But thinking about exchange rate levels, I wonder what will show through in UK imports/exports/inflation in the next couple of years. Big devaluation in recent months related to perceptions about upcoming brexit, but actually no change yet. So it’s not like the typical devaluation example where exchange rate reflects actual economy or commodity prices.

So really just wondering what we may learn from the devaluation in due course.

LikeLike

Yes, it will be interesting, altho still hard to disentangle from the rest of the mix (policy uncertainty, expectations of higher trade barriers between Britain and the EU), and of course, who knows how long this weak spell will last.

The UK did get quite a lot of inflation following the 08/09 recession, reflecting the substantial fall then in the value of the pound.

At very least, tourism – not exactly a high productivity or high productivity growth sector – to the UK must be much more attractive than it was.

LikeLike

Michael, common sense tells me you have got lost in your numbers and have lost sight of the elephant in the room. Our population is tiny with only 4.5 million and our population growth is not even worth mentioning in the context of countries with billions of people. What you forget is we have 10 million dairy and beef cattle plus 30 million sheep. In total we have 40 million animals to care for, to feed, to supply water and to house.Dairy is resource hungry, nitrate leaching, dirty waterways contaminated drinking water, methane gas pollution and ozone layer depletion of the atmosphere. Our top export industry is not being fully costed. The costs of supporting the dairy industry is costing NZ more than the export revenue we receive.

The other elephant in the room you have missed is the 3.3 million tourists steadily increasing to 4 million tourists soon that is heavily subsidised. We do not charge sufficiently. Our National parks are provided free of charge. Our natural beauty and landscape is readily accesible at zero charge to the increasing tourist numbers But we bear the cost in providing accomodation in residential homes because there has been very tiny investment in hotels. Cost of cleaning up the mess falls onto the public purse and local councils.

LikeLike

(Unusually) I agree with most of what you are saying here, but I’m not sure the relevance to the discussion of NZ’s failure to achieve decent productivity growth, or to increase its trade share of GDP, over decades.

BTW, re tourists, do bear in mind that tourists pay GST on what they consume here, which is a tax windfall to us, covering some of the other costs. Of course, the offset is that NZers pay the equivalent of GST in other countries when they travel.

LikeLike

Because we are paying people to clean toilets instead of providing students free education to create.

LikeLike

An entire generation of students are burdened by debt and therefore restricted in being able to create new businesses providing new goods and services that add to GDP.

LikeLike

Thinking of the GST collected on tourism. In theory as an export sales there should not be any GST collected. Export sales is supposed to be zero rated. Lawyers and property managers do not charge GST on the fees associated with overseas owners or overseas purchases of property. In Australia the tax office is better organised with tax booths at the airport where you can provide your GST receipts and collect refunds. Our tax office just conveniently ignores this illegal tax take.

LikeLike

Don’t forget that if you buy goods at the airport they do not charge GST if you can show that you are an overseas traveller. In the local shops they are just ignorant of the zero rated nature of export sales and therefore collect GST from tourists.

LikeLike

[…] overall export share of GDP is less now than it was in […]

LikeLike