I’m still puzzling over the academic who told Radio New Zealand’s listeners yesterday that he didn’t agree with me that New Zealand was remote: “we are, after all, in the middle of this great ocean, the Pacific”. I keep looking at the globe, conscious that perhaps I have a eurocentric view of the world, but….we still look about as remote as they come. And it is a sort of remoteness which, historically, hasn’t been conducive to really high levels of economic performance for lots of people (see Tristan de Cunha, St Helena, Bouvet, and even Samoa, Kiribati, or Fiji). Henry Kissinger is reported to have described Chile as “a dagger pointed at the heart of Antarctica”. Much the same could be said of New Zealand, one of the Antarctic Rim countries.

But, on another topic, I noticed that Kiwibank and NZ Post were in the news this morning.

Late last week, Radio Live was reporting a story that Kiwibank was being prepared for sale, and they asked for my thoughts on that. That interview is here.

There was never a good economic case for setting up Kiwibank. Our banking market was, and is, pretty competitive, and there were few material regulatory barriers to new entrants. And the historical track record, here and abroad, is that government-owned banks are more prone to getting into costly trouble than private-owned banks (and some of them cause quite enough trouble). In a modern New Zealand context, think of the Bank of New Zealand, DFC, and the (different sort of case of the) Rural Bank. Overseas, examples abound.

But, of course, the case for Kiwibank was never mostly about economics. It was mostly about nationalism, and some mix of political product differentiation and the political circle turning. Jim Anderton has resigned from the Labour Party in 1989, having been suspended from Labour’s caucus when he refused to vote for the sale of the Bank of New Zealand (then still predominantly government-owned). And now Jim Anderton was back, as Deputy Prime Minister in a Labour-Alliance government. Not only could the government own businesses, but it could – so it was claimed – build good new ones. This speech by Jim Anderton captures the flavour. This centre-left government would be different from its predecessor, and the establishment of Kiwibank would be one important marker of that difference.

The Reserve Bank and (more importantly) Treasury opposed the establishment of Kiwibank. There weren’t obvious gaps in the market that other new entrants couldn’t fill, and establishing any new business is risky.

The National Party opposed the establishment of Kiwibank, but has never been willing to commit to selling it (in full or in part), even when Don Brash was leader in the 2005 election.

The actual track record of Kiwibank has been less bad than many of the opponents feared. NZ Post was able to recruit some capable people who have built a reasonably substantial bank, that now has around $19 billion of assets. Kiwibank grew very rapidly in its early years, and when institutions – especially new entrants – grow rapidly, it is wise to worry about the credit standards: it is most easy to write loans to people whom other lenders are reluctant to lend to. Kiwibank had a few ill-judged forays into particular market segments, but appears to have built a reasonably self-sustaining bank, which came through the recession of 2008/09 with little more damage than the larger banks sustained. My own reaction to that record was that, as taxpayers, we should be thankful for small mercies, and take the opportunity to sell before something went wrong.

But it has never been quite clear how much money Kiwibank has really made, and in particular whether it has ever sustainably succeeded in covering the cost of the taxpayers’ capital invested (and reinvested) in the bank. Banking is a highly leveraged business, and since the government’s finances are already heavily directly exposed to the overall health of the New Zealand economy, there were no obvious diversification gains for it in establishing a bank in New Zealand. We needed a good rate of return to justify the risk.

One of the reasons it has never been clear just how profitable Kiwibank has been is that Kiwibank and its parent NZ Post were intertwined, operating (most obviously) from the same physical locations. During the early years in particular, there was a lot of incentive for NZ Post (with its government appointed Board) to help ensure that Kiwibank was a success, and to err in favour of Kiwibank in any allocation of costs or charging for shared services. I got involved with these issues briefly in my time at Treasury and even then it seemed impossible for outsiders to know whether costs were being allocated appropriately. Several years on one might have hoped all these issues were adequately resolved, so I was a little surprised to see this comment from Bill English in the Herald this morning.

He said there had been discussions over whether NZ Post was subsidising Kiwibank.

“Certainly through the start-up phase it has been but NZ Post can’t afford to keep cross-subsidising the bank,” he said.

Which doesn’t give one a great deal of confidence that, even over the last few years, the Kiwibank accounts give a full representation of the returns from a standalone banking business. I don’t read the literature as suggesting that the economies of scale in retail banking are huge (so a small bank could be profitable) – and we have both big and small banks co-existing in the New Zealand market – but I doubt it could be shown that Kiwibank had been a good investment for the taxpayer. Fortunately, it hasn’t been a disastrous one.

So I’d be all in favour of Kiwibank being sold. There is just no good reason for the government to be involved in the business of retail banking. Even today, the barriers to new private sector entrants are quite low, and even if there is some independent concern about New Zealand-owned banks, then we have SBS, TSB, Co-op, and Heartland.

One key strand in New Zealand’s approach to banking is the idea that no institution, and no depositor/creditor, is totally immune from failure and the risk of losing one’s money. I don’t think that is a politically tenable stance, and am among those who favour New Zealand adopting some form of deposit insurance (as most other countries have done). But it is a particularly difficult model to sustain in respect of a government-owned bank.

Yes, governments have been willing to allow creditors of SOEs to lose money – the banks who had lent to Solid Energy most notably among them – but a handful of banks, mostly foreign, is a rather different matter than hundreds of thousands (800000 apparently) of retail depositors (and voters). Governments can say all they like that no one is guaranteed, but it isn’t obvious why anyone would – or should – believe them. After all, a standard element in the Reserve Bank’s approach is that if a bank gets into difficulties, the Reserve Bank will look to its shareholders to recapitalize the bank concerned. The New Zealand government owns all the shares in NZ Post, the immediate (struggling) parent of Kiwibank. The credit rating agencies also take that view: S&P, for example, noted last year that

we consider that Kiwibank has a “high” likelihood of receiving extraordinary support from the New Zealand government, reflecting the bank’s “very strong” link and “important” role to the government.

The unpriced implicit support Kiwibank has from the government skews the domestic banking market and undermines the efficiency of the financial system, all while continuing to pose material financial risks for the New Zealand taxpayer.

And it is not as if the governance of Kiwibank looks particularly strong either. I was quite surprised to find, looking through the list of directors, that not a single one of them has a background in retail banking.

At very least I think it would make sense to restructure the NZ Post group, removing Kiwibank and making it a standalone SOE in its own right. Going by the comments from the Minister, if the story Radio Live ran had anything behind it, that was the mostly likely form.

A sale would also make sense, but I don’t see any chance of it happening under the current government. One could conjure up all sorts of imaginative options that might mitigate the political uproar – recall the size of the petition around the partial sales of the government stake in three power companies – but I can’t see why this government would regard it as worth the political risk. And no potential coalition partner really cares enough to want to make a sale a “bottom line” in any deal – while NZ First might well care enough on the opposite side.

Kiwibank shares could, for example, be distributed to all adults – on current book value that might be around $300 each – so that it was truly the “people’s bank”. But then there would no single dominant shareholder, and the rating agencies would get nervous, and so would the Reserve Bank. It would have quite high direct costs, and the opposition parties would no doubt sell it (accurately) as prelude to those individual parcels being bought up by one or another of the other banks.

I’ve seen suggestions that perhaps the New Zealand Superannuation Fund should become a key shareholder in Kiwibank. I reckon that would be even worse than direct state ownership, since the NZSF faces neither market nor political disciplines.

I don’t really like the idea of a partial privatization, with the government retaining the majority shareholding. It still has most of the moral hazard/bailout risks associated with the current ownership model, with more risk that the private shareholders would seek to aggressively (and quite rationally) exploit such advantages. It was, more or less exactly, the model used with the Bank of New Zealand in the late 1980s.

In truth, the best value for the taxpayer probably lies in what is the least politically attractive option: a straight trade sale, probably to one of the existing large participants in the market. That was how the previous Postbank was sold, back in 1988. It is what happened to Trustbank in 1996, and to Countrywide a couple of years later. And, of course, Lloyds concluded that the best value from the National Bank was through a trade sale to ANZ. The government might get a price well above book value in such a sale, even recognizing that banks are less inclined to aggressive expansion than they were a decade ago, and that some of the Australian banks might be uneasy about overweighting their exposure to New Zealand. But even to propose such a sale would surely be seen by the government’s political advisers as an unadulterated gift to the Opposition.

And so it seems likely that, for the foreseeable future, the government will not just be the largest owner in New Zealand of dairy farms, funds managers, trains and planes, power companies, and legal firms, but will remain the owner of a modest-sized, not outstandingly successful, retail bank.

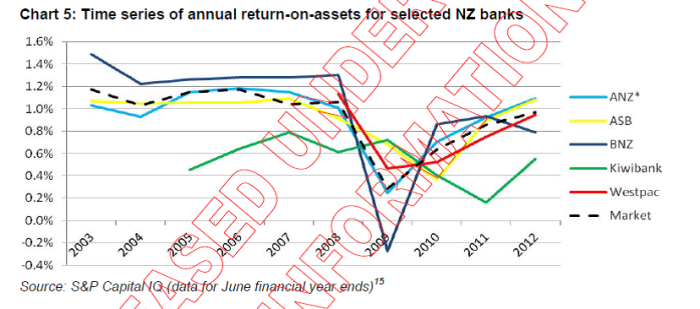

UPDATE: In casting around for any summary analysis that has been done/released on Kiwibank’s long-term performance, I found this chart of return on assets (not equity) in a Treasury report from a couple of years back.

The results shouldn’t be very surprising, but they do reinforce the point that even if Kiwibank is currently earning reasonable rates of returns (eg in the most recent year), it has a long way to go to deliver the sorts of cumulative returns to taxpayers that private sector shareholders might have expected (especially as none of the private comparators were start-ups).

Per Kiwibank financial results presentation pack for FY’15: return on equity 13.48%. If roughly right and given the excess over recent long term NZGB rates, seems decent to my mind especially given the absence of rate rigging, trading scandals, currency manipulation etc…..!

LikeLike

Yes, the latest year looks reasonable – altho 13.5 per cent in no higher than the sorts of returns Aus businesses generally were looking for (in that RBA survey and Bulletin article)

But (a) there are quite a few earlier years, and (b) the real question I was posing was about cost allocation, and the way the unpriced parental support has assisted in lowering funding costs.

It would be an interesting exercise for someone to do a careful analysis all the way back to 2002 and see how the overall returns look, both on a reported basis and with some plausible adjustments for such factors

LikeLike

13.5% is an excellent return vs. government cost of funding. Certainly global top quartile if not decile. I think your arguments may have had merit 14 years ago but that they are less relevant now. Despite the cassandras, KB has been a success and has largely avoided other potential messes like dairy. Now the housing market? Who knows? The fact that Kiwibank was able to pass on almost all the recent interest rate cuts is a function of a decent deposit base, less due to implicit government support. The other banks, notably ANZ, are now having to raise capital to pay back their parents. One of the single worst things NZ has done in the last 30 years is to lose more control of its inadequately regulated banking system. Anderton was right about BNZ. The basis cost of our perpetual need for capital due to bank outflows added to the extraordinary high real return is an implicit tax on any of our companies that need external funding.

LikeLike

I pose the question about overall returns on capital invested, and if it turns out that the true return over 14 years has been anything like 13.5% on average I’d be relieved. My real points are twofold: it should never have been set up by govt and should be sold, and (on the other hand) that seems most unlikely to happen, whether under this govt or the next. Kiwibank hasn’t been a disaster and all taxpayers should welcome that.

LikeLike

Oh dear Lord…. the cost of debt funding for the Govt is not a remotely useful measure for the financial performance of a business. The Govt will always have the lowest cost of funding because it has the first claim on your income. So based on that logic the Govt should own all businesses because it has the cheapest cost of funds.

The correct measure is the return from an alternative use, which is a cost of capital argument. Equity is not free. The cost of debt funding is always lower than the cost of equity funding because debt has a prior claim on the assets of an entity whereas equity holders are always the last ones to get paid. So is a 13.5% return good or bad?

In looking at Kiwibank’s return on equity you have to bear in mind that the banking system has moved through a period of higher losses/impairments that have depressed returns. So while 13.5% might sound good as a stand alone number on a business cycle analysis basis is may not be so. The other point to bear in mind is that because it is largely a residential lender the amount of capital it is required to hold is lower (all other things being equal) compared to the larger commercial banks.

So really we should be seeing a higher return from Kiwibank than 13.5%. Its an OK return, but not outstanding by any means. On a business cycle basis you could make the case that it is in fact underperforming, but as Michael Reddell points out its not clear how big the NZ Post subsidy has been or continues to be, so we can’t really see its true economic performance.

If the Govt has a policy of investing taxpayer dollars into banks then it should sell Kiwibank and invest in the best banks instead, however, I don’t see that as a policy objective of Govt. An alternative would be to sell Kiwibank and give the dosh to the NZ Super Fund. One thing the Govt will want is a dividend from Kiwibank otherwise it won’t be getting any more capital.

I suspect the reason for the restructure of the ownership of Kiwibank has more to do with the deteriorating position of NZ Post than about Kiwibank per se. I suspect that funding rates for Kiwibank are likely to move up and the credit rating come under pressure while it is still subject to a failing parent company. On that basis it is an entirely sensible move.

LikeLike

I am in favour of the government setting up businesses that should be sold for a substantial profit in privatisation. Let competition be rife and commercial profits decimated and the government walks in as a saviour to buy back the assets cheap and then to revive and recover the business with the prospect of reselling at a later stage.

Take Air NZ for example. Previously government owned with monopoly, sold to overseas interest eg Temasek Holdings, Singapore Super fund manager took a beating up as competition opened up with the NZ Air losing its monopoly position as the government opened up the airspace for competition and decimated Air NZ and Helen Clark bounces in with a rescue package and swoops on Air NZ when it sank to penny stock levels and now what a prime asset which the government should now look at reselling. Round 2 profits coming up.

I am always puzzled why people are concerned over government asset sales. Afterall we own the country and we set the rules. A tweak here and a tweak there and we buy back those assets cheap.

NZPost and Kiwibank should have been sold a couple of years ago and the government would have got a substantial premium. John Key did the right thing by selling those power companies. He should have sold the lot. Those power companies are a cashcow but with declining and aging assets. Pretty soon technology will move ahead and bye bye power companies. We are seeing that with email and text decimating the value of NZ Post as a business.

LikeLike

Watch Google decimate the parcel post business of NZ Post as they get permission to send out parcels on their automated drones right to your doorstep.

LikeLike

Well that assumes that only Google can operate drones… which does rather require the CAA to approve their use…

Say Amazon and NZ Post can operate drones as well…? So maybe we shouldn’t jsut assume that Google will conquer all before it.

You do realise that NZ Post has owned Courier Post for years… and its a pretty reasonable performer amongst a sea of trouble at NZ Post (exl Kiwibank)

LikeLike

NZ Post is going to sell 45% of Kiwibank to the New Zealand Superannuation Fund and the ACC for a combined total of $495 million.

Under the plan, announced by NZ Post chairman Sir Michael Cullen, the NZ Super Fund would take 25% and ACC 20%. The deal values the whole of Kiwibank at $1.1 billion.

http://www.interest.co.nz/business/80926/nz-super-fund-and-acc-proposed-new-minority-shareholders-kiwibank

LikeLike

[…] wrote about Kiwibank last week, noting that there had never been a good economic reason for the Crown to have established it, and […]

LikeLike