At the end of 2008 South Canterbury Finance was rated BBB- by Standard and Poors. Earlier that year, it has issued three year bonds (themselves rated BBB-) in the US private placement market. BBB- wasn’t such a bad credit rating for a small, not overly diversified unregulated domestic lender. But a year or two later, SCF failed spectacularly, at considerable cost to the taxpayer.

Today, S&P has come out downgrading the standalone ratings of three of the four big banks to BBB+. Of course, that is still two notches above SCF’s rating, but if it is really justified the news would have to be quite concerning. Note that the overall issuer credit ratings remain at AA-, reflecting the combination of probable parental support and the possibility of government support (for these systemically significant banks) in the event that they get into trouble. Their assessment of the risk of investors losing money hasn’t changed.

But it is the standalone rating that is meant to reflect the quality of each bank’s loan book.

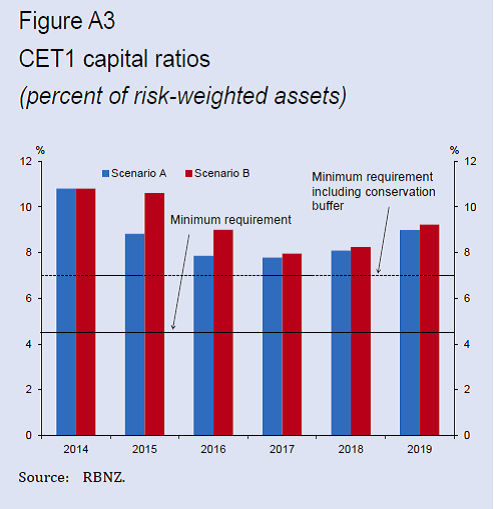

Recall that the RBNZ and APRA stress-tested the large banks only last year. The stress scenarios were very demanding – a 50 per cent fall in house prices and an increase in the unemployment rate larger than any seen in floating exchange rate countries in the post-war decades. And the banks’ loan books came through with flying colours, and the actual capital of each of the banks was not impaired at all (capital ratios fell because risk weights on the remaining loans rose).

Here is a chart of capital ratios from the stress test scenarios from the November FSR

If Standard and Poor’s are right there must be something very wrong with the Reserve Bank stress test results. Not that much has changed in the make-up of banks’ portfolios in the last 12-18 months for the difference to be about new, much riskier, loans being made. My bias is to run with the stress test results – perhaps they are a little optimistic, but probably not too much. But the Governor doesn’t seem to believe them, and neither apparently does one of the leading rating agencies. If the Bank is really sceptical then it is really past time for it to lay out any reasoning, and evidence, it has as to why the stress test results are not now a good guide to the standalone health of the major banks.

Michael…. can we trust S&P, Moodys, et al? I suspect in a general sense that all the major ratings agencies are very gun shy after they got things a tad wrong around things like sub prime, the mortgage insurance companies in America going back to the 2000’s

Do you think the RBNZ is that far out in their assessment?

LikeLike

My instinct is that the RB stress test results aren’t far wrong – with the caveat that, from memory, the dairy bit of the stress test may not be as “stressful” as the other dimensions. But that may reflect the likelihood that if we had the sort of severe recession that created real problems with the housing portfolio, the exchange rate would have fallen so far as to provide a lot of relief for indebted farmers.

I think the “gun shy” risk is a possibility, but at a quick glance some of the relativities between NZ and international banks look a little odd. I might come back to this next week.

LikeLike

Quick question Michael: given a 50% fall in house prices under the stress test scenarios doesn’t breach the ‘worrisome’ level then what sort of fall would give the banks (or us!) cause for concern over their capital?

LikeLike

The results become quite non-linear, so perhaps an increase in the unemployment rate to 15% and a 60% fall in nationwide house prices would make the difference. But for practical purposes recall that banks get into trouble when they increase their loan books rapidly and injudiciously (ie much lower credit standards). In NZ since 2007, as I illustrated the other day, credit growth has been as slow as the (weak) nominal GDP growth, and there is no obvious sign of widespread deterioration in credit standards. If those things change, then we should worry more.

LikeLike