Last week, I started showing a few charts about how New Zealand had done against various other advanced economies since 2007, the last year before the recession that engulfed most of the world in 2008/09.

Today I’m going to show the charts for investment and national savings, using the data from the IMF’s WEO database.

First investment.

Of this group of advanced countries, only four had a share of investment in GDP higher in 2014 than it was in 2007. That probably doesn’t come as a great surprise. 2007 was a cyclical peak, and by last year hardly any of these countries would have been considered to have been operating at capacity. Across the advanced world as a whole, population growth rates are falling, and lower rates of population growth mean less of GDP needs to be devoted to investment for any given level of technology.

But my main interest was the cross-country dimension. Perhaps unsurprisingly, the commodity exporting advanced economies have all been among the countries with the most strength in investment. But Germany comes between Australia and New Zealand, and I was surprised to find the United Kingdom, Japan, and Sweden doing better than either New Zealand or Australia. At the other end of the chart, the 18 weakest economies all either use the euro, or have a currency pegged to the euro.

The New Zealand story itself is a little less favourable than it might first appear. Recall that I noted last week that there had been no sign of a surge in New Zealand business investment in response to the high terms of trade. And, on the other hand, a significant amount of the strength in New Zealand’s investment in the last few years has been the repair and rebuilid activity in Canterbury. It counts as gross investment but, since it is mostly replacing capacity that was destroyed or severely damaged, it isn’t adding much to the capital stock.

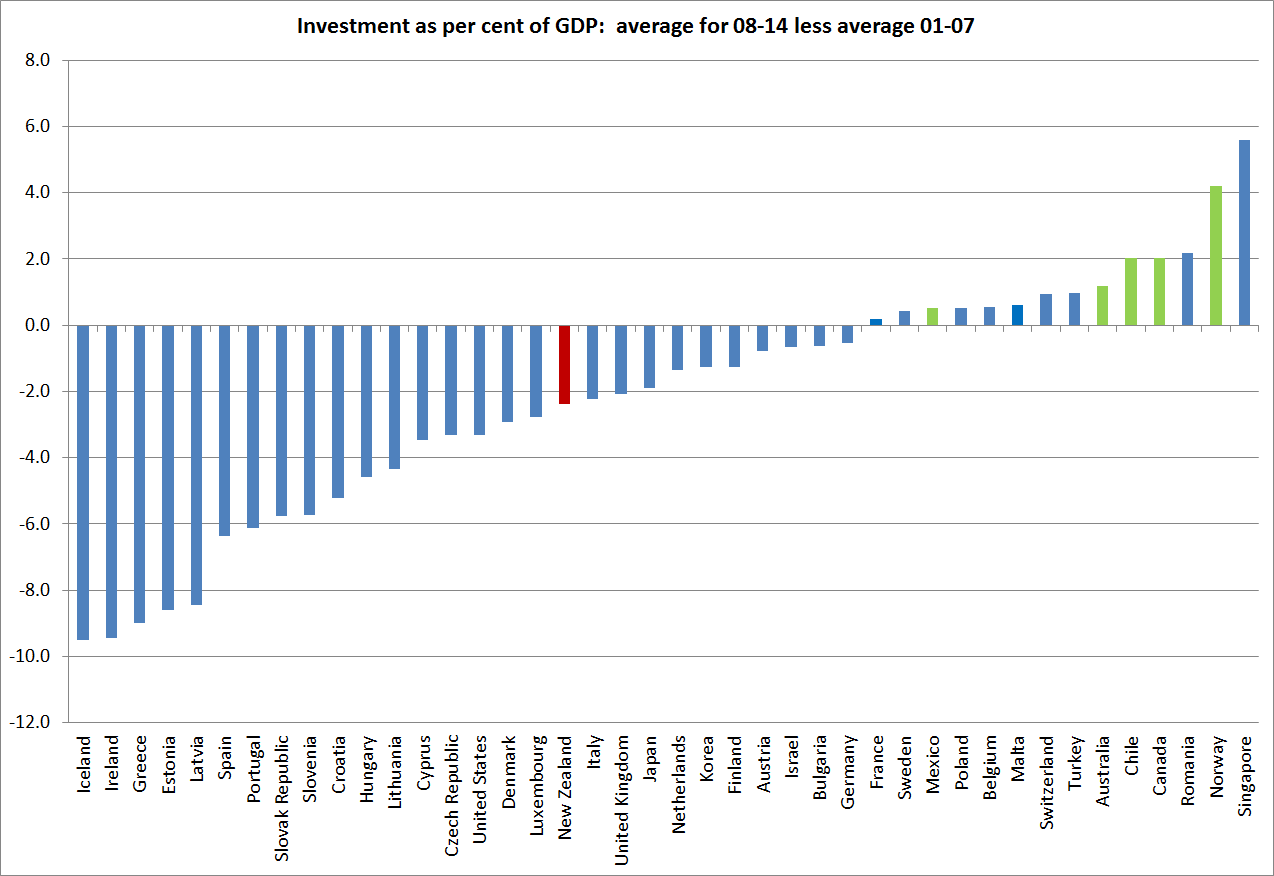

If we do the same chart comparing the average for 2008-14 with the average for 2001-07, New Zealand drops back to the middle of the field, and well behind the other commodity exporters.

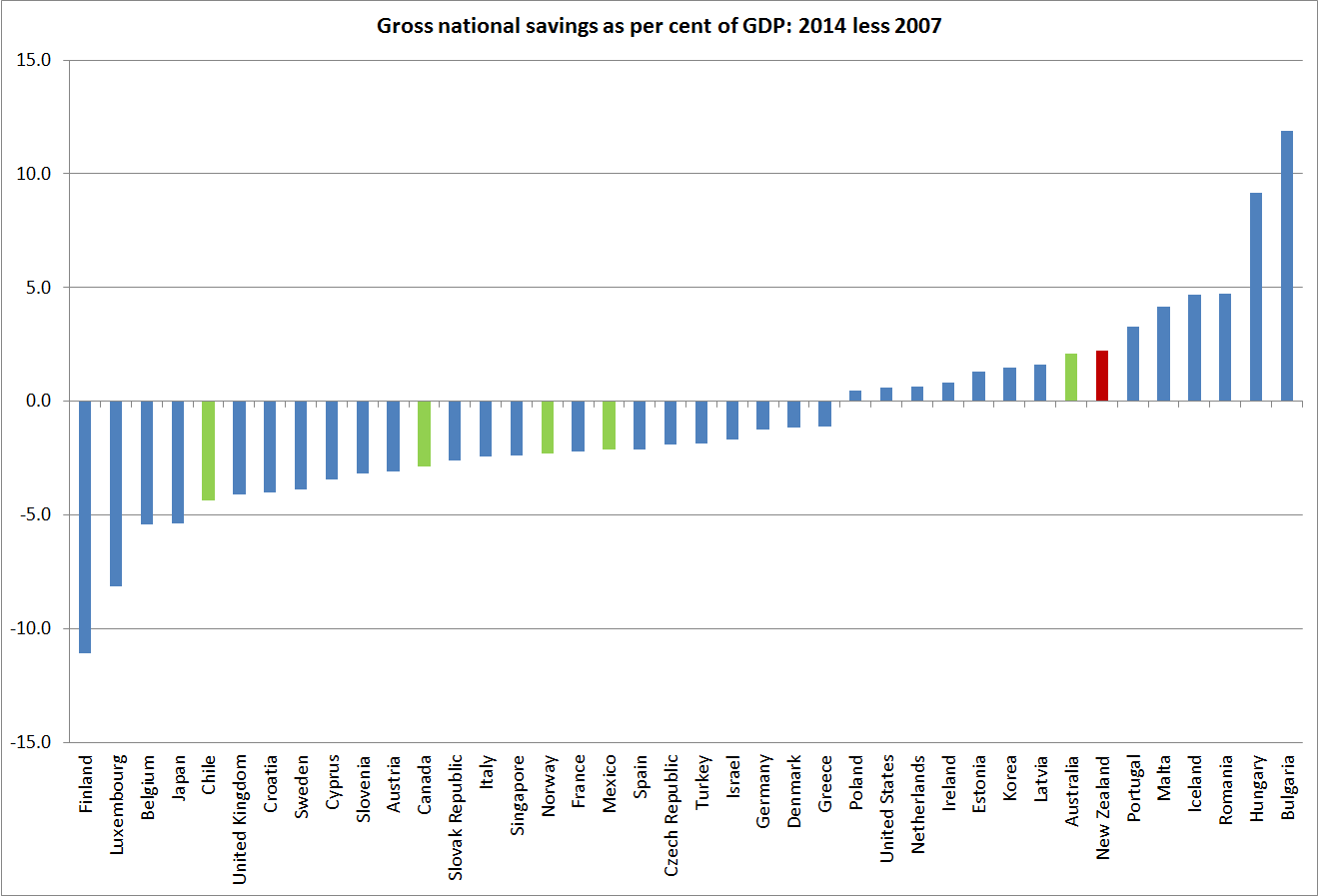

And what about national savings? On this chart, any patterns are much less obvious. Savings rates have fallen in more countries than they have risen, but 16 countries have had increases in their national savings rates. Euro area countries, for example, are not bunched at one end or the other, and New Zealand and Australia show up as among the countries with the larger increases in national savings rates.

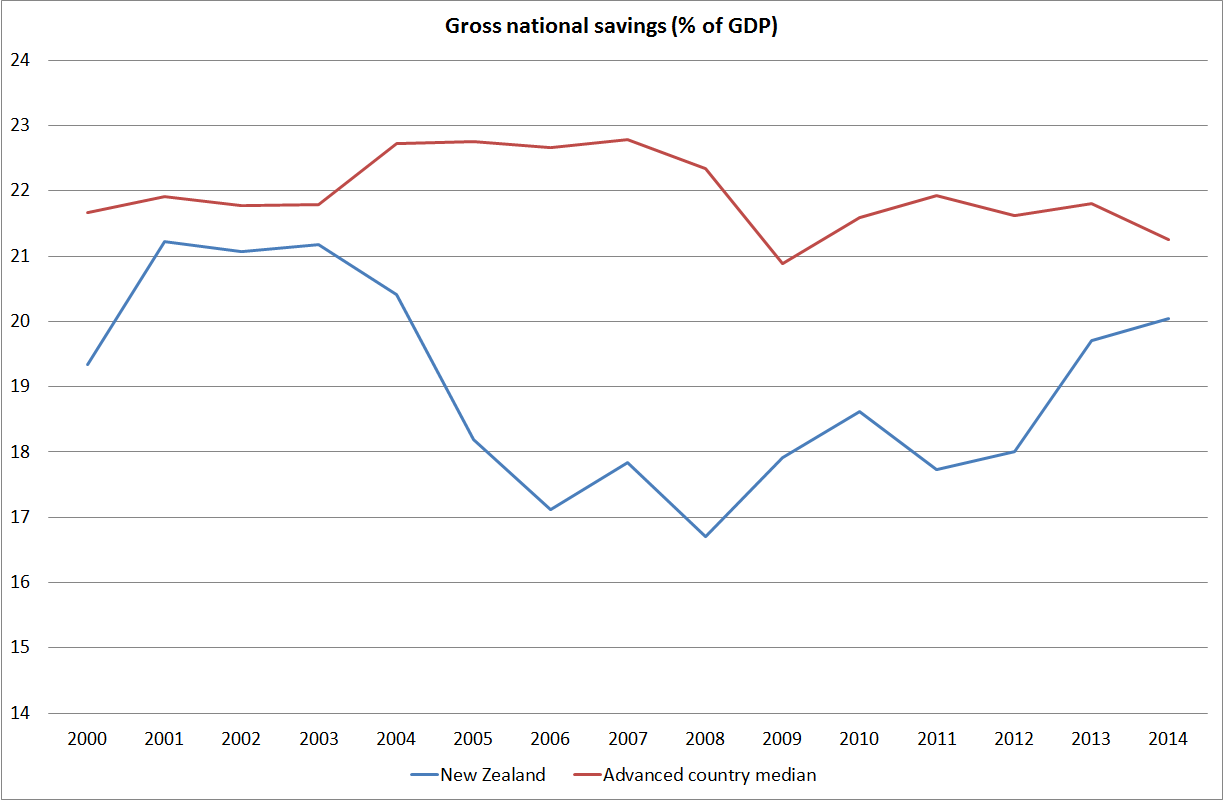

Before anyone starts getting excited about, for example, the impact of Kiwisaver, I should point out that when I compared savings rates for 2008-14 as a whole with those for 2001-07, New Zealand dropped right back to around the middle of the chart. Unlike the median advanced country in this sample, New Zealand’s national savings rate fell away sharply in the middle of the last decade, as public (and business) savings rates dropped away sharply. Our national savings rate is only now back to around the level seen in the early 2000s.

(And one final note, these are ratios of national savings to domestic product. In other words, the savings of New Zealanders as share of all that is produced in New Zealand, whether by New Zealanders or foreigners. In other words, the two series aren’t strictly comparable. For most countries the difference doesn’t matter, but here national income is materially less than domestic product (the difference is mostly the net earnings of foreigners on New Zealand’s negative net international investment position). Taking national savings as a share of national income, New Zealand’s national savings rate would be around the median of this group of advanced countries.)

As one of the few (the only?) Ricardian(s), I continue to believe it is helpful to look at private (ie business+hh) savings vs. public savings.

We can debate causality but the inverse correlation is striking – you might want to plot the two series (using say 3YMA to smooth out noise).

We saw hh savings rise as the public savings fell in the GFC and If history is any guide we could well see hh savings slow down/fall as the public sector returns to surpluses.

LikeLike

Thanks Grant. Yes, I agree that the inverse correlation is striking. I’m not entirely convinced it is all Ricardian in nature. I’ll come back to focus on the NZ specific savings and investment data in a week or two, when I get back to my explanation for why NZ real interest rates have been so high for so long.

LikeLike

Agree with Grant that it’s probably more sensible to look at HH+ Business saving together – the boundary between the two these days is just too blurred. (I have always been pretty skeptical of those big negative HH sector saving ratios.)

But I also share Michael’s skepticism that the inverse correlation is mainly a Ricardian thing. If households/firms are budget constrained and consumption smoothers, shouldn’t we expect fluctuations in government saving to be mirrored by, more or less opposite, fluctuations in private sector saving?

LikeLike