In its Financial Stability Reports, the Reserve Bank consistently highlights two other areas of risk:

- Dairy debt exposures of the banks

- New Zealand’s quite large net international investment position

In this post I want to offer some thoughts on the nature of these risks, highlight perhaps a bigger risk that has never received a mention in an FSR, and end with a few thoughts on how the Reserve Bank might better think about FSRs.

Dairy farmers owed banks around $35bn as at June 2014. That is more than the total capital of the banking system, and is the largest sectoral exposure of the New Zealand banking system. Since each dollar of farm debt is generally regarded as much riskier than a dollar of housing mortgage debt it can’t be ignored as a potential area of threat to the banking system. It also makes the New Zealand banking system different – when I checked a few years ago, farm debt in New Zealand was about one tenth that in the US, even though US GDP was perhaps 100 times that of New Zealand.

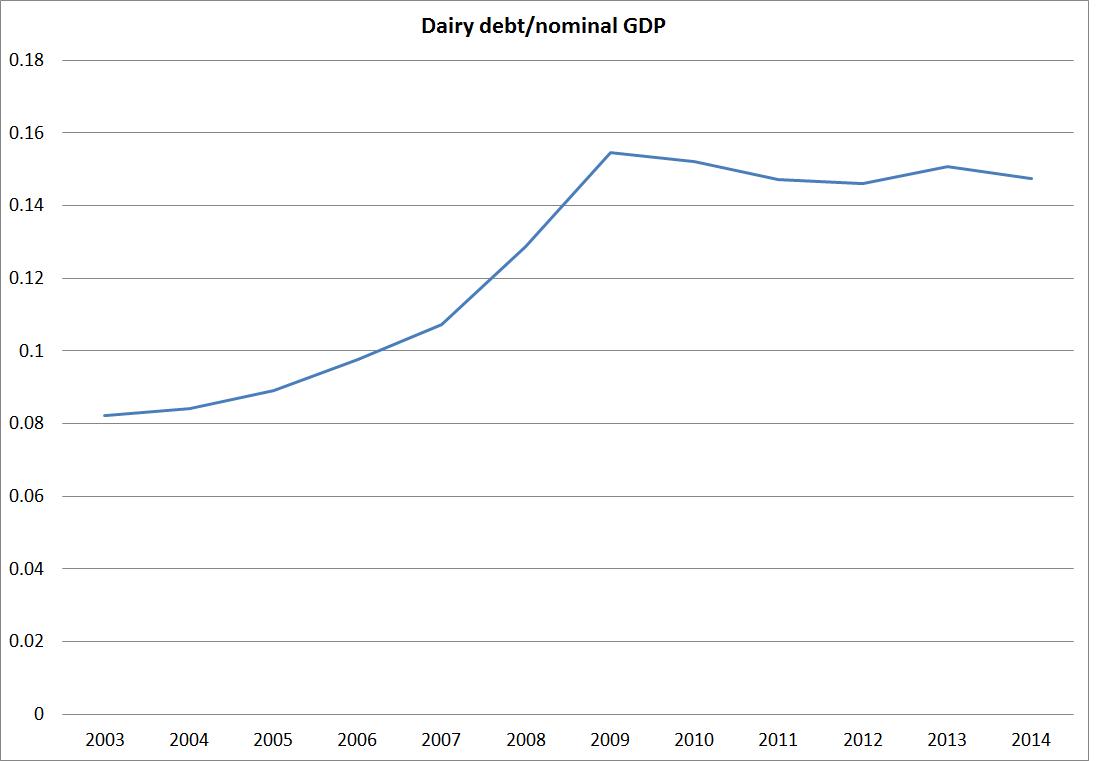

The Governor made much yesterday of the fact that dairy debt had trebled since 2003. What we didn’t hear so much of is when that debt increased. The chart below shows dairy debt as a percentage of GDP. It rose very very rapidly to 2009, and has gone nowhere – actually fallen slightly – since then.

During that boom period, dairy land prices rose very sharply. Land prices fell a long way in the recession and even in the last couple of years land prices have been below the previous peaks (even in nominal terms). It matters when the debt was taken on. The worst of the loans taken in the boom – and there were some pretty bad ones, as banks fell over each other to build market share, and buyers got sucked into some sort of bubble mentality – have already failed. Bank non-performing loans in respect of dairy exposures rose quite sharply over 2009 and 2010. They could easily have got a whole lot worse, if the payout had stayed down for longer, and if banks had not all quietly recognised that in an illiquid market like that in dairy farms in a downturn, selling up many clients would rapidly drive the value of collateral even lower.

I did quite a lot of work, and thinking, on dairy risks in 2009. I used to stir people up by describing dairy debt as potentially ‘New Zealand’s subprime’ – potential for bad debts, exposures ill-understood both by parent banks and by offshore funders, and a market for collateral that was highly illiquid and, hence, with little effective price discovery. And New Zealand has been down this path before – farm debt was a major problem in New Zealand, with all sorts of regulatory interventions, during the Great Depression. So I’m not complacent about the possibility of dairy risks. But timing matters a lot. Not only has the worst of the boom-times debt already failed, but bank parents got quite a fright in 2009, and banks have had plenty of opportunity to manage their exposures over the last five years or so, including encouraging – or forcing – clients to take advantage of the good years to reduce debt levels. I’m a bit of a pessimist on global commodity prices so it wouldn’t surprise me if farmers had a pretty tough few years ahead. And in any sector where there is a boom followed by bust, some people will be caught out, and some will exit the industry. But this is not 2009, and the chances of any material systemic threat, based on bank dairy books as they stand now, seems incredibly low. A fresh dairy credit boom and land price spiral would be something quite different, but the last one was years ago now.

But I had some sympathy with the call I heard this morning for risk weights on dairy exposures to be raised. My sympathy has nothing to do with the current situation, but with a fear that the weights were set too low in the first place. Back in June 2011, the Reserve Bank published two Bulletin articles about dairy debt in the same issue. One was a stress-testing exercise which used a plausible scenario that ended with 20 per cent of dairy loans having to be written off. The other described the work the Bank had done on recalibrating risk weights for farm loans. The authors reported that average risk weights on farm loans would in future be around 80-90 per cent. That meant banks would be required to hold capital equal to perhaps 7 per cent of farm exposures (given that the minimum total capital requirement is 8 per cent of risk-weighted assets). Requiring banks to hold insufficient capital to cover the Reserve Bank’s own contemporaneous stress test looked odd then, and still does now. As I noted, current risks don’t look that large, but capital requirements are supposed to be set to be robust to all different phases of the credit and economic cycles.

(Incidentally, this is an example of a more general problem. Would, for example, the Bank’s capital requirements for insurers be large enough that if the Christchurch earthquakes were repeated – a real world stress test if you like – AMI would not have failed? Given that the government chose to bail-out AMI at taxpayers’ expense, with the support of the Reserve Bank, and has shown no sign of regretting doing so, some questions might reasonably be asked.)

The Reserve Bank has long made much of New Zealand’s relatively large net international investment position (as a per cent of GDP). It doesn’t make Chapter 1 this time round (which is welcome) but it is still there in later chapters, including the “Systemic Risk and Policy Assessment”. New Zealand’s NIIP position is large by international standards, but it has been large for decades, and has shown no signs in the last 25 years of getting any larger. That is a very different position from where countries like Spain and Greece found themselves in the years leading up to the euro crisis, when NIIP ratios increased very rapidly. New Zealand’s NIIP position is a symptom of some persistent imbalances in the economy, but it is a chronic condition, not one that threaten crisis. In fairness, the Bank now mainly focuses on rollover risk for domestic banks’ foreign funding, but even here I think they overdo it. Even in the 2008/09 crisis, wholesale term funding markets were closed for only a relatively short period of time. There was never any sign of idiosyncratic concerns about the Australian and New Zealand banking systems, even though on any objective measures the risks must have greater then than now. Global market disruption – as, say, we might expect if the euro breaks up in a disorderly way – could increase the cost of borrowing (as happened in 2008/09) but that effect can largely be offset through a lower OCR. It just is not a first order risk for the soundness of the New Zealand financial system. Wholesale funding can be an indicator of systemic vulnerability, but usually when wholesale funding has been running up rapidly because lending growth is far outstripping domestic deposit growth. We went through that phase – and our financial system got through it largely unscathed – but it is not today’s risk.

I have been struck for some time by the absence of the word “deflation” from Financial Stability Reports. For all my relative comfort about the health of the New Zealand financial system, the one thing that could really threaten it would be a period of significant deflation. Why? This isn’t Fisherian debt deflation story, but simply a reflection of the fact that almost all private debt is nominal. If we were to experience a period of sustained deflation nominal asset prices could be expected to fall, and nominal wages (and profits) would also be expected to fall. Those holding financial assets would be better off, but those with financial liabilities could be in quite serious strife. For banks, the risks are entirely asymmetric – they don’t benefit from the increased real wealth of their depositors, but are heavily exposed to the increased real debt of those they have lent to.

Material or sustained deflation is not a high risk in New Zealand. No doubt 25 years ago the Japanese didn’t think so either. Deflation isn’t a non-existent risk for New Zealand either, especially in the current global environment – adverse demographics, the increasingly pervasive “bite” of the zero lower bound etc. I’m not sure why the Reserve Bank is so averse to discussing the nature of the risk, even as an extreme scenario. Yes, we know they have an inflation target of 1-3 per cent annual inflation, but there is no guarantee that a central bank will always be able to keep inflation up to current target levels and who knows what the future target will be. This is one of those areas where the Governor, in preparing the FSR, needs to take off his hat as monetary policy decision-maker and just deal with the possible threat to the banking system – remote, but not impossible.

This post has ended up a little longer than I’d intended. I want to finish with just a few thoughts on how I think the Reserve Bank should approach future FSRs. In assessing risk, they seem rather stuck in a pre-2008 environment. Back then, credit growth was very rapid across all classes of bank loan books, the finance company debacle was nearing its worst, asset prices generally were rising rapidly, banks were becoming progressively more dependent on short-term wholesale funding, and constant pressure was on to lower effective capital requirements (in the shift to Basle II). It was quite reasonable to have entered 2008 quite concerned about possible threats to the health of the system. But the New Zealand financial system came through that severe recession, and the aftermath of a big credit boom, largely unscathed. And almost nothing in the description of the pre-2008 years is relevant today.

Some of what has changed is just the result of market phenomena, but some is a result of worthwhile regulatory measures: higher minimum capital requirements, strong pushback against the pressure to erode risk weights, new liquidity and funding requirements and so on. Some years ago, senior staff of the Bank’s Prudential Supervision Department used to tell the IMF each year that they presided over the safest banking system in the world. That used to grate somewhat with the house pessimists (of whom I was one). And yet, as it happened, they weren’t so far wrong. The Bank should take some credit for the health and soundness of the financial system. Of course, a central bank needs to keep a watching brief on emerging threats, but needs to be able to differentiate when they pose real threats to the soundness of the financial system, and when they are just the sort of thing that strong buffers are already in place to contain. More energies might reasonably be put into reviewing the extensive regulatory net now in place – not just to “iron out inconsistencies” (the sort of approach in the current regulatory stocktake) but to ask, and to invite serious outside perspectives on, what bits of the regulatory framework are really adding material value to the statutory goal of promoting the soundness and efficiency of the financial system.

I would have to question your analytics. You show a chart of the dairy debt / nominal GDP. That says nothing about the dairy industries’ indebtedness. Other parts of the economy are not going to pay farmers debt. Use a proper measure of dairy industries incomes and the ratio will be rising big time.

LikeLike

yes and no. My income doesn’t pay a dairy farmer’s debt, any more than it pays any mortgage debt, but nominal GDP was just a denominator to highlight the point that even though commodity prices were strong the growth in dairy debt slowed very markedly after 2009 (and new debt is more prone to problems than old debt) but actually looking at debt relative to, say, dairy exports doesn’t suggest anything overly alarming either. The ratio rises sharply this year, but fell sharply last year.

LikeLike

[…] to 2009, and by around 4 per cent per annum in the six years since then. Last week I showed the chart of dairy debt to total nominal GDP – it rose sharply until 2009/10, and since then has fallen back a […]

LikeLike