The IMF’s twice-yearly World Economic Outlook has just been released. With it comes the very useful and accessible database, which has a wide variety of data (back to 1980) and forecasts (now out to 2020), especially for the 37 “advanced economies”. These are the sorts of places New Zealand often wants to compare itself against – although quite why tiny San Marino is in included has never been clear to me.

I had a quick look at some of the series.

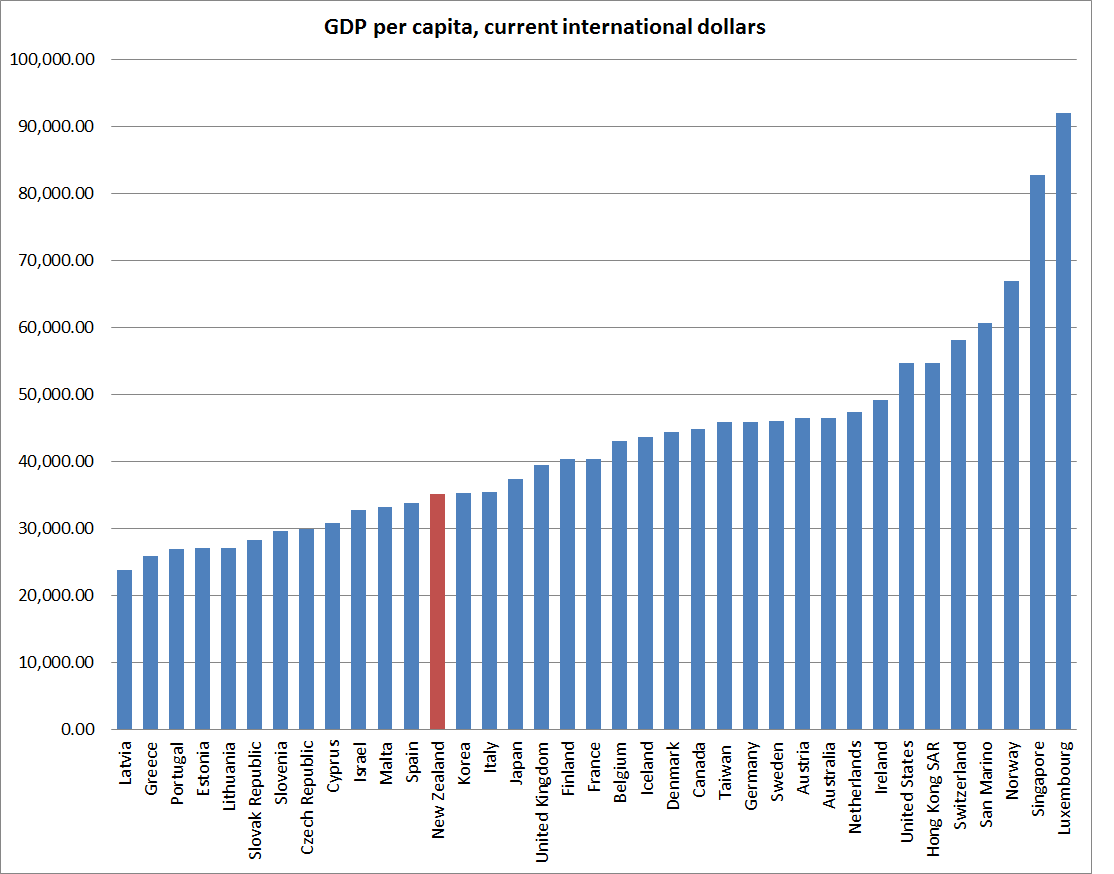

First was GDP per capita, in current international dollars for 2014. That measure of purchasing power parity captures the effects of New Zealand’s record terms of trade last year. 12 of these countries had lower GDP per capita than us last year. That is an improvement from the last pre-recession year, when only 10 countries were poorer. Since 2007 three euro area crisis countries have dropped below us, while Korea has moved above us.

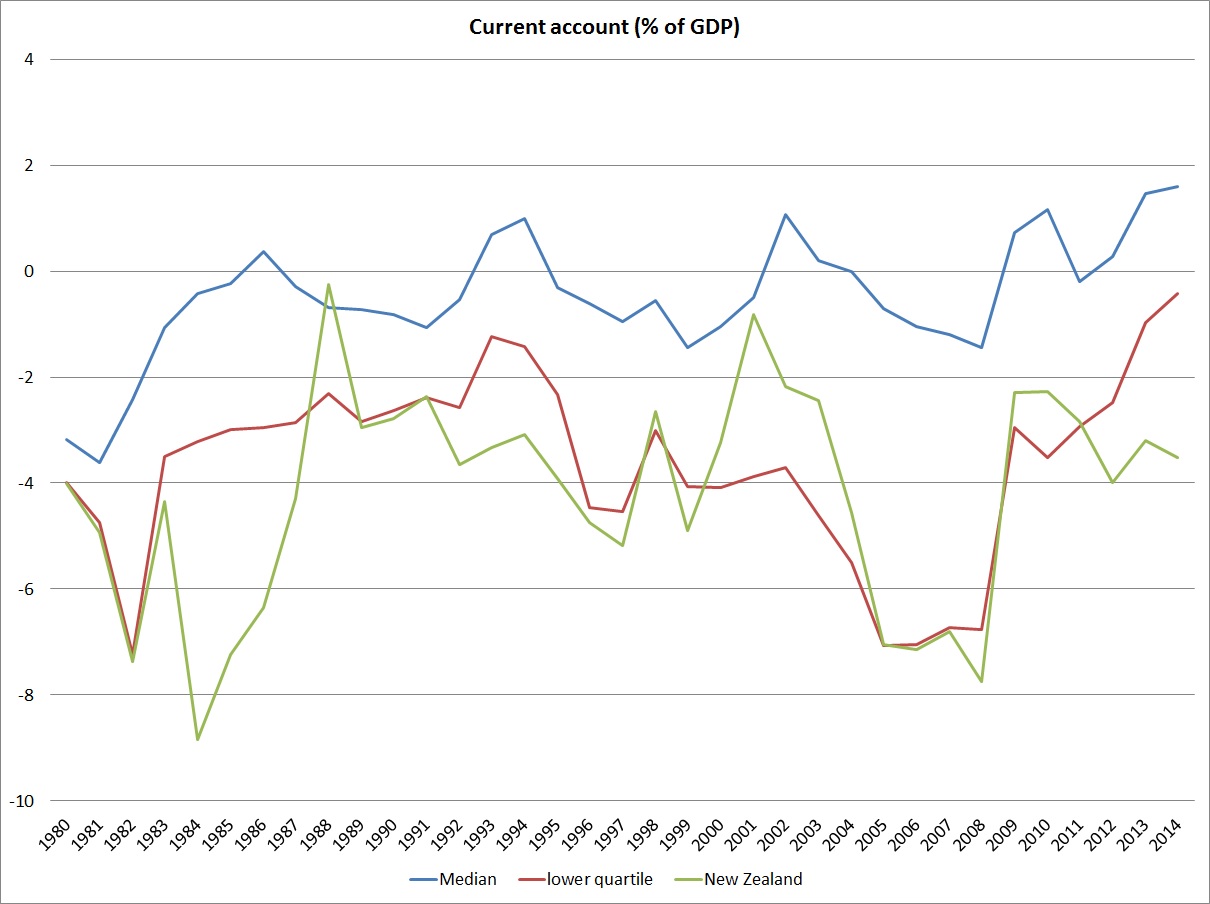

Second is the current account deficit. When he was Opposition Finance spokesman David Parker was fond of highlighting the WEO forecasts for the current account deficit. In recent years those for New Zealand were often the largest in the advanced world, and they still are. That comparison was never overly enlightening, mainly because the IMF’s methodology assumes an unchanged exchange rate. But what about actual data? In 2014 we did have the second largest current account deficit among the advanced economies (only the UK had a larger deficit). And over the longer-term we’ve had current account balances averaging around the lower quartile of OECD countries.

Current account deficits (or surpluses) aren’t good or bad in and of themselves. Context matters. Large current account deficits make a lot of sense in a country with rapid productivity growth and lots of productive investment opportunities – borrowing from abroad to finance high levels of investment, without unduly constraining current consumption is a sensible choice. But, as is well known, New Zealand’s productivity growth has been poor for decades.

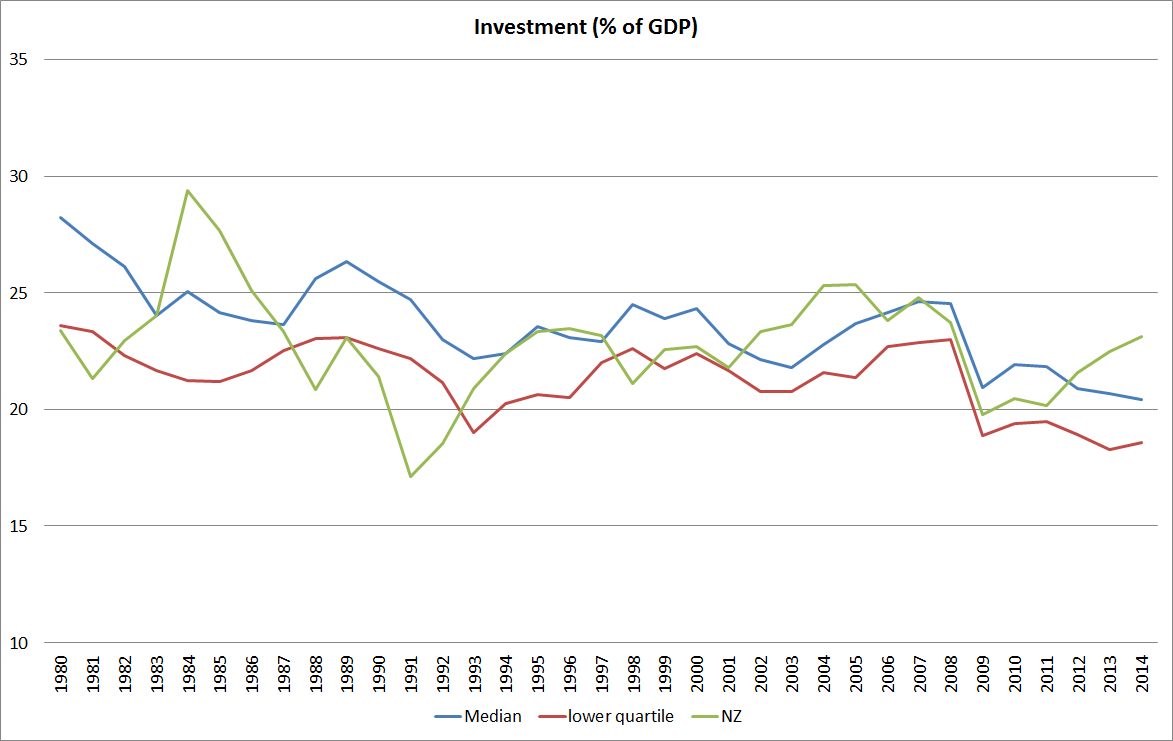

Another way of expressing the current account is the difference between investment and savings. Investment as a share of GDP in New Zealand has increased quite markedly in the last couple of years, accounting for the widening in the current account deficit. Much of that has been the spending on the repair and rebuilding process in Christchurch. That spending had to happen, and we were fortunate that offshore reinsurance covers much of the cost, but it doesn’t lay the foundations for future prosperity.

What about fiscal policy? The IMF’s main measure is general government net lending/borrowing as a share of GDP

New Zealand doesn’t look too bad on this measure, but it isn’t that good either. Roughly a third of the advanced economies had smaller deficits or surpluses than we did in 2014, and that is despite New Zealand’s record terms of trade (a windfall gain to the budget, and unlike to be repeated as the global commodity “bust” deepens) and the view (embedded in the IMF numbers) that our economic recovery was more advanced than those in many other countries. The government has made a lot of the idea of gradual adjustment to support the recovery, but faster fiscal consolidation might have eased pressures on the real exchange rate.

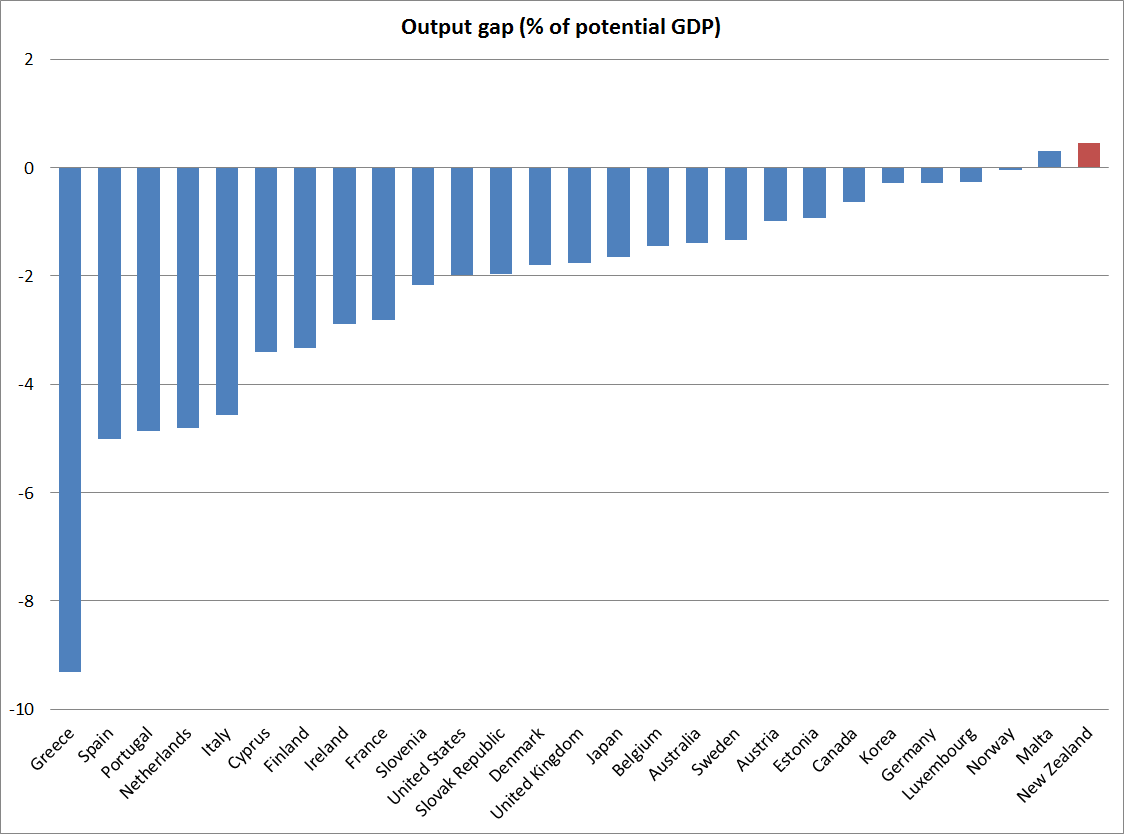

And, finally, the output gap. All recent numbers are subject to revision, but output gap estimates are more rubbery, model-dependent, and subject to substantial reassessments than most (a recent Reserve Bank Analytical Note illustrated this in the New Zealand context). The IMF doesn’t produce output gap estimates for all the advanced economies (nothing for San Marino for example), but of the 27 countries for which there are estimates, New Zealand and Malta were the only countries currently estimated to have had a positive output gap last year. Indeed, if you believe the IMF New Zealand’s spare capacity has essentially been all used up for at least three years.

Believe it if you will (the Reserve Bank has certainly been running policy on a similar view of New Zealand), but when output is almost 15 per cent below pre-recession trends, business investment (outside Christchurch) is pretty subdued, wage inflation shows no sign of picking up, unemployment is still 5.7 per cent (and there is considerable underemployment), inflation is well below the middle of the Reserve Bank’s target range, credit growth is pretty subdued, and inflation expectations are falling, it is questionable what meaning can be placed on estimates that suggest that all the spare capacity in this economy has already been used up. We certainly aren’t Greece or Spain, but it is less clear to me that we are so different from a swathe of countries in the middle of this chart – perhaps from Slovenia to Sweden.