Some years ago the Reserve Bank started collecting weekly data on housing mortgage approvals by the main lenders. It is a great resource, partly because it is so timely – the data released yesterday were for approvals granted last week.

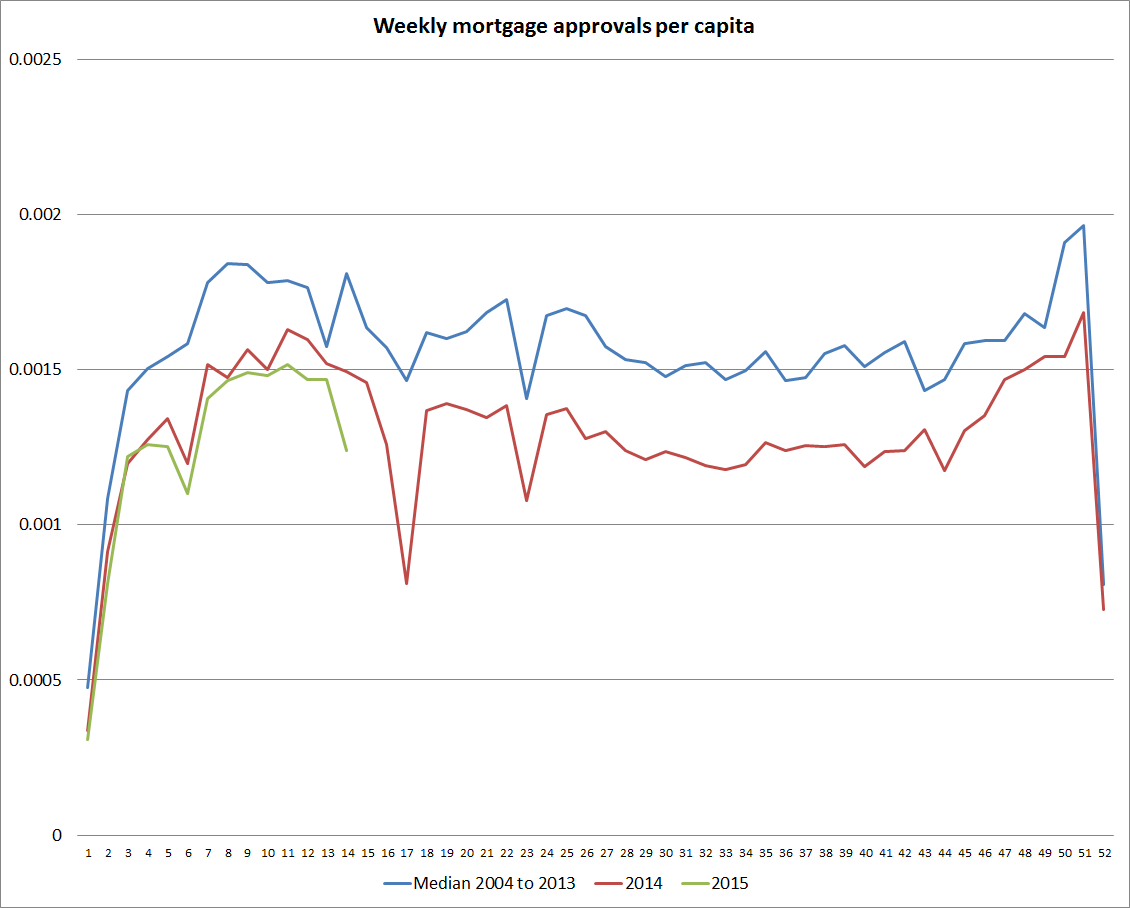

The data aren’t seasonally adjusted, and so for a while I’ve been keeping an eye on a version of this chart, tracking the number of mortgage approvals per capita in each of the 52 weeks of the year. New Zealand’s population is steadily growing, and so I’ve used an annual population estimate to produce an approximate series of housing mortgage approvals per capita. You can see the holiday periods clearly – not just the great Christmas/New Year dip, but also those for other public holidays (Easter accounts for last week’s dip). It is easy to see how mortgage approvals are running relative to the same period in earlier years.

The chart shows three lines. The first is the median for the first 10 years of the series, 2004 to 2013, which encompassed the last few years of the boom, and the very weak few years after 2007. The second and third are the series for 2014 and 2015 to date. The number of mortgage loan approvals last year ran consistently well below the median for the previous decade. And this year, the number of approvals per capita has been tracking a little lower again. So far only 2010 and 2011 have been lower than this year.

Consistent with that, the total stock of loans to households has been growing at a touch under 5 per cent per annum – barely above a plausible trend rate of growth in nominal GDP (say 2 per cent inflation, and 2.5 per cent potential real GDP growth).

The value of mortgage approvals is quite close to an all-time high. That largely reflects the high level of house prices. But activity in the nationwide house finance market remains very subdued.

A final thought: it is very rare indeed for serious financial stability risks to develop, in a system with nationwide lenders, when overall lending activity is subdued, and when there is such modest credit growth. The burden of proof should be on any institution pondering (further) regulatory interventions in the housing finance market, given the inefficiencies such restrictions encourage, and distributional consequences of such measures.