I noticed the other day a tweet from the chair of the Productivity Commission calling attention to the fact that New Zealand once again tops the World Bank’s ease of doing business index. The top five this year were New Zealand, Singapore, Denmark, Hong Kong, and South Korea.

New Zealand has ranked at or near the top of this index for some time (in fact, ever since it was created about 15 years ago). From their country note on New Zealand these charts show New Zealand’s data in more detail (the first showing our rank on individual components, and the second our absolute scores) .

No doubt there are people in MBIE who know all about why we score poorly on some of these sub-indices, and what could or should be done to improve (and even perhaps, on occasion, why what the World Bank is measuring isn’t necessarily what they think it is).

But New Zealand has consistently scored well on this measure. That is noted regularly in analyses of our economic performance. Generally, we want to have a good regulatory etc environment in which it isn’t difficult for someone with an idea, someone spotting an opportunity, to set up and run a business. I haven’t dug more deeply into the index to understand why, but I was interested to see our one perfect score was on “getting credit” – this being about business credit, not housing.

Scoring highly in this index is almost certainly better than scoring poorly. Contrast the top five with the bottom five countries; Libya, Yemen, Venezuela, Eritrea, and Somalia. But if there is some causation at work in the implied direction (improve your score on this index and your economy is likely to improve) there is probably also some (weaker) causation in the opposite direction: rich and well-governed countries are likely to score better on an index that often looks at sophisticated features of a regulatory system.

Whatever the aggregate story, there is no simplistic one-to-one mapping from a good score on this World Bank index and better economic performance. New Zealand is the standout illustration of that point.

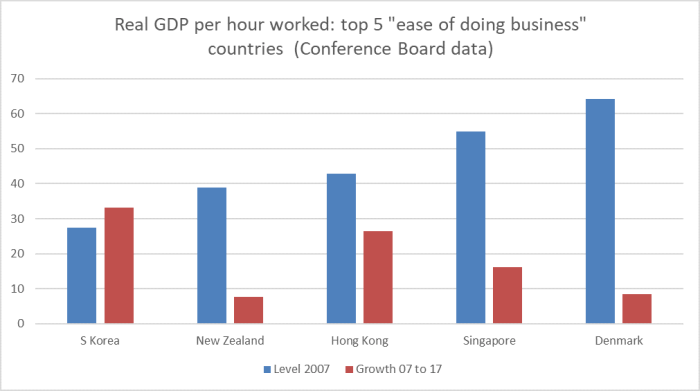

In this chart, I’ve shown labour productivity (real GDP per hour worked) levels and growth rates for the top 5 countries for the decade from 2007 to 2017, using the most recent version of the Conference Board’s database. If the benefits of a high “ease of doing business” score show up anywhere in official data it should be here.

South Korea wasn’t in the top five a decade ago (in fact, it was only ranked 21st). Probably the various reforms they’ve done over the last decade, which have improved their score in the World Bank index, have contributed to productivity growth. That is part of how they have been catching up and converging.

But what I found interesting about the chart is that – for this small group of countries/territories – the productivity growth pattern has been about what you would expect. The countries with the highest initial levels of labour productivity had slower growth rates than those with lower initial levels of productivity. The exception, of course, is New Zealand.

Take a bigger sample and there will be other exceptions (the UK, for example, ranks number 9 and – after a good couple of decades, but only middling levels of advanced country productivity – has had a really poor productivity growth performance in the last decade. But my focus is New Zealand.

We score quite well on all manner of such international surveys. Take skills for example. A year or two back, the OECD adult skills data suggested New Zealand workers were among the most highly-skilled in the OECD. And yesterday I noticed a report suggesting that New Zealand was in the top 3 countries in the world, behind Finland and Switzerland.

Again, it is presumably better to be near the top of such a list than at the bottom

The WEFFI report, by the Economist Intelligence Unit, looks at policy initiatives, teaching methodologies and the socio-economic environment of 50 countries. It found the five worst-ranked countries to be Egypt, Nigeria, Algeria, Iran and Pakistan.

But it doesn’t seem to bear any relationship to getting to the bottom of New Zealand’s specific economic underperformance – not just over the last decade, but over most of the last 70 years.

One of the odder features of New Zealand public service life is the number of top-tier public servants who now seem to run Twitter accounts and disseminate material through those accounts. I’m old-fashioned enough to think that senior public servants shouldn’t really be seen or heard except by Cabinet ministers (to whom they give their advice, and implement decisions taken by political masters). More pointedly, public servants’ Twitter accounts are at grave risk of being, in effect, party political broadcasts for their masters since senior public servants can’t really be out openly disagreeing with the Minister so anything that is tweeted is not going to upset the Minister or his/her office, and yet it bears the imprimatur of a supposedly-neutral public servant.

On the other hand, these accounts can shine a little light on what top public servants are up to and what causes they are championing.

One of the tweeters is the (fortunately soon to have departed) Secretary to the Treasury, Gabs Makhlouf, who has spent the last eight years presiding over – perhaps even inspiring – the degradation in the capacity of what should be the government’s lead economic advisory agency. In his most recent tweet a few days ago he linked to a piece by the (often stimulating) academic economist Dani Rodrik. There is a lot to disagree with in Rodrik’s piece, but I just to quote his conclusion.

…economists are well positioned to develop institutional arrangements that go beyond what already exists, their habit of thinking at the margin and sticking close to the evidence at hand encourages an aversion to radical change. But, when presented with new challenges, economists must envision new solutions. Imagination is crucial. Not everything we try will succeed; but if we do not rediscover the value of FDR’s credo – “bold, persistent experimentation” – we will certainly fail.

One can only assume that Makhouf agrees. But there is just no sign of The Treasury under his leadership having seriously re-thought the New Zealand productivity failure. If there is any bold thinking (and here “thinking” would be a polite description) it is around avoiding confronting that failure at all, chasing off after the insubstantial living standards framework and the associated “wellbeing Budget”. Feel better, I suppose, even if we can’t do better. It is perhaps great as a political distraction – politicians do that sort of thing – but we should expect something much better from a premier economic agency than turning away from the most striking economic failure in our history, and playing distraction in the hope no one will notice. In principle perhaps the two – “wellbeing budgets” and some serious fresh thinking on productivity, specific to New Zealand – could both be done, but (a) resources are limited and (b) nothing in any Makhouf speech has ever really suggested a desire, or an ability, to confront the specific productivity challenges here. One can only wistfully hope – with no reason for optimism, given who (SSC and Grant Robertson) does the selection – that his successor will be different.

As for my own alternative story? I don’t have any particular problem with the rankings people like the World Bank come up with – from a regulatory perspective doing business in New Zealand probably is easier than in most places – but those indexes just don’t shed light on the salient issues for New Zealand. Citing them, as anything more than a stepping off point – “despite this high ranking…..” – is akin to looking for lost keys under the lamppost because that is where the light is, rather because there is reason to suppose it is where the keys are. From a regulatory perspective, New Zealand probably isn’t a bad place to do business – although there always many things that could be improved – but from a more fundamental perspective New Zealand – most remote significant inhabited land mass on the planet – looks like a pretty awful place to do business from, in anything much other than utilising the limited natural resources. Were it otherwise, we’d have seen more investment, more exports (and imports), more globally-oriented firms basing themselves here.

Against that backdrop, actively pursuing an ever-bigger population through a large-scale immigration policy that is championed across the bureaucracy – including by Makhlouf’s Treasury – is fundamentally damaging to the longer-term economic interests of New Zealanders as a whole. (And, as I’ve noted, many times before that is so whether the migrants – mostly decent and well-motivated people – come from Brisbane, Bangalore, Brahmanbaria, Buenos Aires or Birmingham.) Unless and until our political leaders are willing to confront this – and at present all parties in Parliament are signed on to one of the largest (per capita) immigration programmes in the world, there is very little likelihood of those high rankings – ease of business, teaching skills, or whatever – translating into material living standards to match those in other countries at or near the top of these indices.

Australia faces many of the same issues New Zealand does in this regard, but the economic constraints are – at least temporarily – less binding because of the newly-developed abundant mineral resources they are able to bring to market. It was interesting to read in The Australian this morning that the government there is planning to cut their permanent migration intake. The reported number would still be high by international standards, but in per capita terms would be only about three-quarters of the target in place in New Zealand – and that in a country with more opportunities and more wealth. Of course, the current government is almost certain to lose this year’s election – and some other aspects of the reported package are just daft (trying to compel immigrants and even students to the regions – so it may never happen. But it suggests a more serious willingness to engage than has been evident from either main party in New Zealand.

Continuing to look under the lamp post, rather than look for actual diagnostic answers and policy solutions, is just a recipe for keeping on failing economically.