In a few weeks time Christians will begin to mark the season of Advent. One of the texts often read in liturgies in that season is from the prophet Isaiah.

The people walking in darkness have seen a great light; on those living in the land of deep darkness a light has dawned.

At The Treasury yesterday, a visiting academic proposed such a vision for New Zealand’s place in the world, as the Pharos state.

Bernard Cadogan is a New Zealander now living in Oxford. According to his bio

Dr Bernard Cadogan has his doctorate from Oxford University on Empire Studies and constitutional theory. He served Hon Bill English (1996-1999, 2005-8), the National Party Opposition (1999-2003), Hon Trevor Mallard (2003-5). He lives at Oxford UK with his wife and three children.

He was also, apparently, a foreign affairs adviser to Bill English in the latter’s brief stint as Prime Minister and has been a consultant to The Treasury on various occasions and issues. He is formidably well-read, very fluent, often stimulating….and yet, so it seems to me, much better on history than on contemporary politics/policy, and really rather at sea when it comes to economics and economic policy.

I thought I’d written about his previous, extraordinary, Treasury guest lecture in 2016, given just a week after the Brexit referendum (a topic on which he had been providing consultancy services to Treasury), but it seems I never got round to it. My notes record talk of “pogroms by ballot box”, of an EU that is “virulently alive” while there is “something dead in the British Isles”, comparisons with the Glorious Revolution of 1688, a summary remark along the lines of “darkness won: the fog has rolled back in”, the Brexiteers as “sons and daughters of the counter-enlightenment”, depriving young people of “a second European homeland so that some might have a Narnia”, and so on. As it happens, the text of that earlier address is still on Treasury’s website – which enables me to quote in its full “glory” this quote, only the gist of which I’d managed to jot down at the time.

Irrational romantic nationalism and the archaic narratives of historians and of the nationalist culture industry have prevailed over rational economic argument. Grub Street and Grub Street politicians from “Spectator-land”, with the prose skills of another era, have worsted the experts and the technocrats, and rendered nugatory the best quantitative techniques.

You get the sense that Dr Cadogan wasn’t very keen on Brexit.

In yesterday’s address there was none of that tone at all. It was quite a remarkable transformation, especially when Brexit still hasn’t happened – if I heard correctly that might have something to do with consultancy services Cadogan is now offering to parts of the UK government. But it seemed to be there by counterpoint, in his theme that in this troubled and turbulent world

Throughout his talk Dr Cadogan uses the image of the great lighthouse of Alexandria to represent New Zealand’s personality in global affairs, as a source of hope and comfort to countries and peoples sailing turbulent waters.

It was bringing to mind more of Isaiah

40 Comfort ye, comfort ye my people, saith your God.

2 Speak ye comfortably to Jerusalem, and cry unto her, that her warfare is accomplished, that her iniquity is pardoned: for she hath received of the Lord‘s hand double for all her sins.

3 The voice of him that crieth in the wilderness, Prepare ye the way of the Lord, make straight in the desert a highway for our God.

4 Every valley shall be exalted, and every mountain and hill shall be made low: and the crooked shall be made straight, and the rough places plain:

It was, and is, more than a bit of a mystery as to why anyone much – at least in the advanced world – should look to New Zealand for anything, let alone “hope and comfort”. Cadogan never did address that point, apart from some quick passing reference to questions he gets abroad – presumably from people within his own ideological bubble – about “how does New Zealand do it?”. “It” here also never being defined, but I presume it had something to do with the popular adulation, in a few quarters abroad, for our current Prime Minister (shorn of any actual policy programme).

The lecture began with a painting by Nicholas Poussin in which the (small) servant Cedalion guides the giant Orion towards the sun, and healing. Small nations may, Dr Cadogan asserts, have special powers – at least if they can avoid getting stomped on by giants. And New Zealand….oh New Zealand,

- that radical democracy (the “most radical”)

- exemplary in so many respects

- admired for our democracy, values, responsibility, human rights, decency

- a successful market economy,

- excellent institutions,

- where the Treaty of Waitangi combines utopianism and justice,

- and where there is no hatred, no contempt, no ideologues (he seemed particular exercised here about some UK former junior minister, now ennobled as Lord Freud).

(He claimed that Henry Kissinger had once said that law was New Zealand’s greatest gift to civilisation. I’m not sure if someone was getting confused with Solon, or even Coke or, say, Blackstone.)

We, in Cadogan’s view, have a story to tell the world, we could be a “moral realist” “force multiplier” to the world.

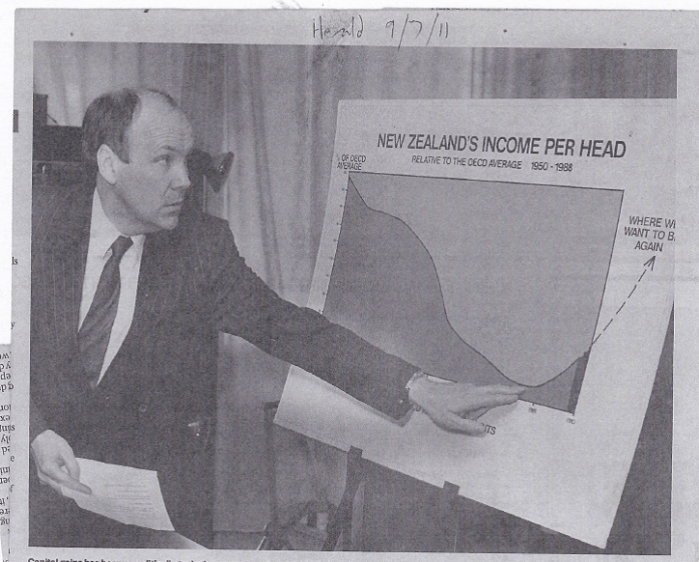

There have been times in our past when a good number of serious people abroad have looked to New Zealand as some sort of exemplar. Like them or not, the reforms of the Liberal governments in the 1890s attracted many visitors and attempts to explain the New Zealand story over the next couple of decades. Probably not entirely unrelatedly, New Zealand was also among the handful of most prosperous places on earth.

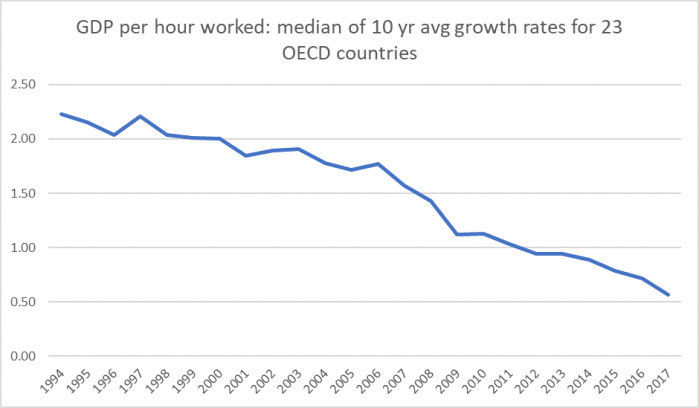

There was a somewhat similar effect in the wake of the reforms of the late 80s and early 1990s. Like them or not, they were adopted with energy, verve, vigour, rigour and with some genuine innovation. By this time, people – here and abroad – knew that New Zealand had fallen well behind (economically, and in terms of what a strongly performing economy could offer) and the reforms were some sort of beacon of hope, that would put New Zealand back on a high-performing path. You still find the occasional residue of that sort of sentiment – although mostly from people who haven’t looked at any data for the last 25 years. In that period there was, at least among some on the left, some admiration for the New Zealand ban on nuclear ships – some genuinely hoping that it would show the way to other countries (typically it didn’t).

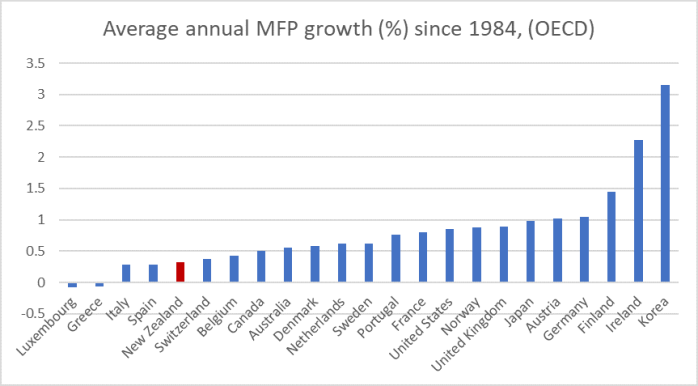

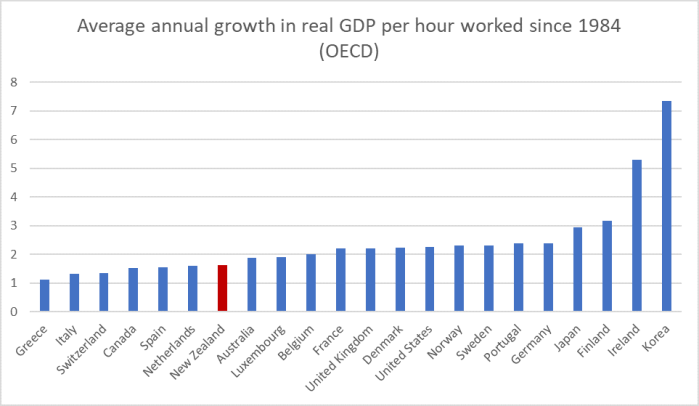

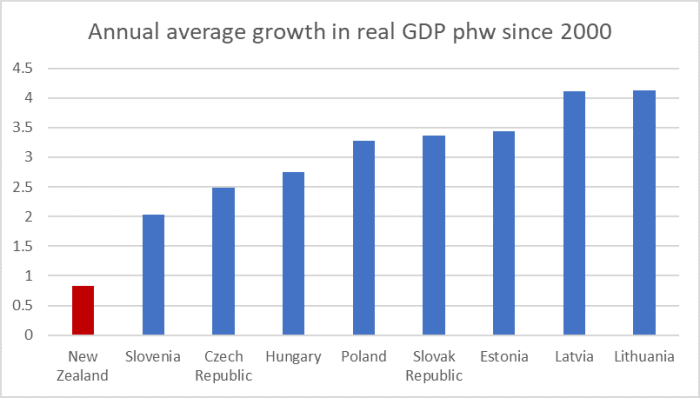

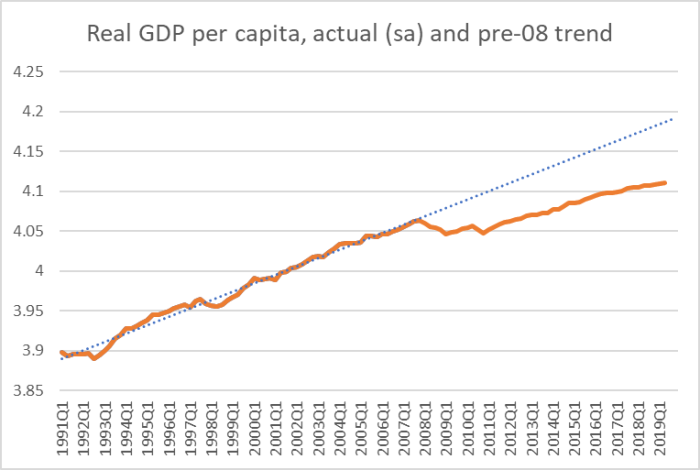

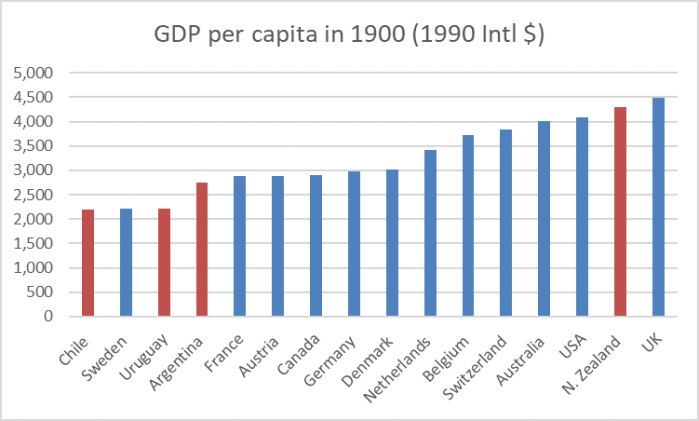

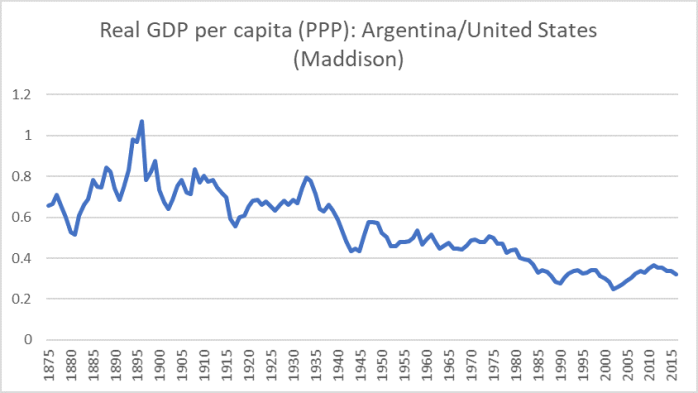

But quite what are we to suppose that people – elsewhere in the advanced world – should look to us now and admire or envy? I’m at a loss. A questioner in yesterday’s seminar pointed to the disgrace that is our housing market, the rise of homelessness etc. I’d, of course, frame the issue more broadly, and highlight our continued relative economic decline. In 1900, you might have missed great art and architecture, museums etc if you came to New Zealand, but at least average incomes would be as high as on offer anywhere. Now, you face distance, a pretty thin representation of the best of our civilisation, and you get to be materially less well-off than you’d be in most other advanced countries. Are we “leading the way” on climate change, or any other left-wing causes? Not that I’d noticed. No doubt there are niche areas where New Zealand people are well-regarded (one hears it re trade negotiations, but then again why not unilateral free trade?) and few people are ever likely to express much angst about New Zealand (a threat to no one). But a light to the world? Really? Who is looking? Who cares? Where, for that matter, are these “values” Cadogan talks of – none that are admirable on display re the PRC (and for a lecture supposedly on geopolitics, there was almost no mention of China).

Another questioner noted that for all Cadogan’s praise of our democracy, actually there were few checks on the executive, great concentrations of power, and little effective accountability. It more or less stumbles on, but to what end? And how resilient would it prove to be if really put under pressure? The questioner might have added specific points about how weak the media generally is, the limited range and poor quality of much of the public debate, the weak role academics and think-tanks play here, and the degradation of the capability of the upper reaches of the public service.

Yet another sceptical questioner – Prof Girol Karacaoglu from Victoria University – noted that for all Cadogan’s talk about New Zealand exceptionalism, he (Karacaoglu) was reminded of a line from a book he’d read – John Gould’s The Rake’s Progress – soon after coming to New Zealand 40 years ago, suggesting that things in New Zealand both good and bad tended to follow, perhaps 15 years behind, trends from abroad.

Are there valid points in what Cadogan was saying? Yes, although some probably don’t carry much substance. Are we a great power or a small player? A small player. Ever was and probably ever will be. Do small countries survive the rise and fall of great powers? By and large, yes. And are there areas in which it is more likely that we can learn from other small countries – and perhaps work effectively with them – than from very large countries? No doubt.

Cadogan urges a peripatetic “colloquy” of small countries – he listed Norway, Sweden, Finland, Denmark, Netherlands, Portugal, Switzerland, Ireland, Australia and Canada (the latter two far from small) and “perhaps” Uruguay. This grouping could, he suggested, learn from each other. It is hardly a new idea, and of course in many areas of policy there are just such groupings (eg a “small inflation targeters” grouping of central banks). But it wasn’t really obvious what New Zealand had to offer or – at least on some key issues – learn. Our strategic position is very different from almost all these countries. Which is a variant on the point that our geography is very different – incredibly remote – and there are few/no relevant national comparators (and not very encouraging subnational ones) when one contemplate the implications of that remoteness. Perhaps Uruguay fits the bill, but for all its relative success in the last decade or so, it remains materially poorer and less productive – with less of a record of political or economic stability – than New Zealand.

Cadogan seemed very taken with Ireland – he’s an Irish citizen too apparently – but showed no sign of appreciating that for all of Ireland’s exaggerated GDP per capita, once you look at the bit of economic activity benefiting the Irish people, Ireland’s story (prosperity) is nothing out of the ordinary: it is a fairly prosperous (but not first rank) European economy, and if there are lessons for New Zealand they are mostly about what we can’t do (not being a short distance from hundreds of millions of other very prosperous people).

There was upbeat talk about what a difference a New Zealand Nokia – a big brand signifying New Zealand – might make: Cadogan saw such a brand as a “sports lifestyle” one that would “walk through the walls that ideology imposes”. Perhaps, but isn’t this just wishful thinking? A bit like the talk, inspired by mention of the top Swiss universities, of what a difference it might make if New Zealand had two really good universities, one in sciences and one in humanities. And yet, starting relatively poor and very distant, there was no hint of how this alternative world might come to be.

There are plenty of places in the world worse than New Zealand. But the notion of the world – advanced world – looking to New Zealand as some sort of lead, exemplar or guiding light seems little more than ludicrous in our current diminished state. If anything, we might be a bit of an embarrassment – the nice little country, that did so many reforms, and yet look at them now, still drifting ever so slightly further behind, without even a political system or civil society to insist on something better, to set a different course. And so remote that we don’t ever matter much to most of the rest of the world. Sure, we don’t have Donald Trump – but, fortunately, neither does anyone else. But we have a (former?) CCP member, former member of the PRC military intelligence system in Parliament (chairing a Select Committee no less), and no one in the establishment here says a word – at least in the US there is disquiet, and more, about Trump.

Lighthouses – grand or otherwise – warn sailors off rocks. I noticed in the NZ History Twitter feed that yesterday was the anniversary of a dreadful maritime disaster here in 1894 (one of the two or three worst days, per capita, for the peacetime loss of New Zealanders in history) – no mention of a lighthouse in the write-up. If New Zealand is any sort of lighthouse to the world – on these rocks pointed at the heart of Antarctica – it is perhaps in the form of the salutary lesson: don’t do as we did, don’t end diminished as we now are.

Fluent and stimulating as Cadogan can be, it might also be a bit more encouraging if our Treasury itself showed signs of leading the way towards a much better-performing economy. Perhaps we never again can lead the world – as we were doing 100 years ago – but whether it is economic policy, housing, or just the quality of our diminished government institutions themselves, we have to be able to do better than we are now.