Yesterday’s post unpicked some of Reserve Bank Deputy Governor Geoff Bascand’s speech in Sydney earlier this week. As I noted, the goal of the speech seemed to be to leave readers with a sense that there really were good grounds for New Zealand to impose materially more onerous core capital ratios on locally-incorporated banks (recall that none of these requirements apply to any other lenders, banks or otherwise) than those imposed in Australia. The gist of the case was, we were told

Our conservatism, relative to Australia, in our bank capital proposals reflects the higher macroeconomic volatility that we have endured, as I pointed out earlier.

Even over the nearly 30 years Bascand asked us to focus on, this wasn’t a very convincing argument.

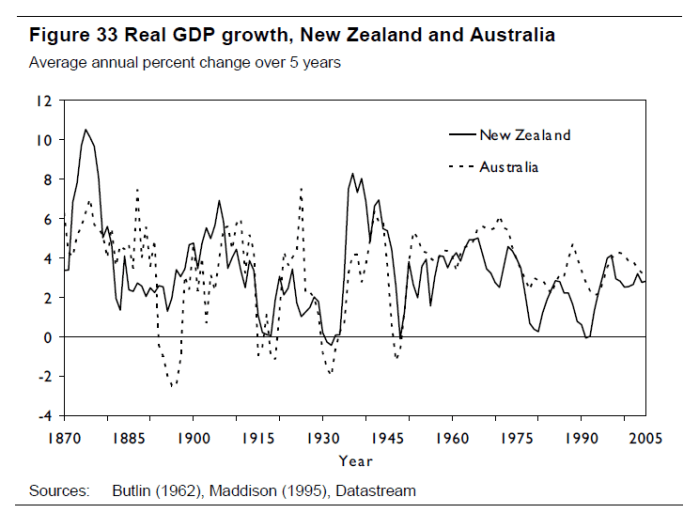

As I pondered further the claim that New Zealand was exposed to materially more macroeconomic volality than Australia – and the differences have to be “material” to support the material differences in proposed core capital requirements – and conscious of the huge and wrenching Australian crisis of the 1890s, I’d just decided to look at a rather longer run of data when a reader, an academic economist, sent me an email making exactly the same point, and conveniently drawing my attention to this chart (from the Phil Briggs NZIER compilation of charts and text in New Zealand economic history).

It uses smoothed data because the estimates for the earlier decades, for both countries, are incredibly noisy.

But, if anything, over that 150 years, the Australian experience was more volatile than that of New Zealand. Their financial crisis was much more severe than ours in the 1890s, and their experience of the Great Depression (including in the financial sector) is generally regarded as having been worse than ours, as examples.

You’ll recall that the Governor has chosen to attempt to calibrate his capital requirements so that, in principle, New Zealand experiences a financial (banking) crisis no more than once in 200 years. We don’t have 200 years (of data, or experience) for New Zealand – although the Australian data start from 1820 – but if you want to mount arguments that we are (and will be) exposed to materially higher macro volatility than another country, it surely is only reasonable to look at as long a history of those two countries as one can reasonably get. Unless, that is, one is using statistics/history for support – for the boss’s whims – rather than for illumination.

One can always discount history – this, that or the other thing will always have been different, even if human nature isn’t – but to mount a major policy case on a carefully chosen subset of history seems more akin to propaganda than to good policy process.

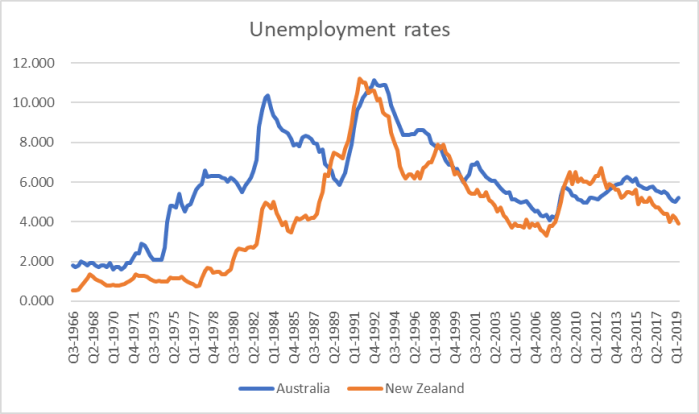

Or here is another chart. Bascand included in his speech a chart on New Zealand GDP since 1965. Here are the unemployment rates for the two countries since 1966 – the official Australia data starts then and our series was backdated (from when the HLFS started in 1986) by Simon Chapple. Not 200 years of data, but more than 50.

Do those look like two economies prone to materially differing degrees of macroeconomic volaility? If anything, Australia might have been a bit more volatile (over this particular period). Peak unemployment rates in Australia in the Great Depression also appear to have been higher than those in New Zealand.

But I don’t want to mount an argument that Australia is more exposed to macroeconomic volatility than New Zealand is. If anything, rather the contrary. Over long periods, New Zealand and Australia have been two of the more similar countries on earth. The modern countries emerged at much the same time, for almost all their histories they’ve had much the same exchange rate regimes, they’ve had strongly overlapping banking systems, they’ve been heavily dependent on foreign capital (especially in the development phase), they liberalised again at much the same time, they both run public debt sky high at much the same times, they both turned fairly inwards for a time, they’ve had pretty similar migration policies, they’ve mostly had very similar terms of trade cycles, and they’ve both had the rule of law (and similar legal systems) and democratic government throughout their modern histories. They’ve been tolerably well-governed, tolerably successful in economic terms (Australia more than us in recent decades), with a high degree of financial stability in both countries for now well over 100 years – with the sole exception of the brief period of shared craziness immediately after the 1980s liberalisation when no one (regulators, lenders or borrowers) really knew quite what they were doing.

So if Adrian Orr and Geoff Bascand really want to mount a case for putting much more onerous capital requirements on in New Zealand than in Australia, it is simply absurd and untenable to mount it on the basis of some intrinsic greater level of economic risk in New Zealand than in Australia. It hasn’t been so in history, and they’ve not even sought to advance an argument for why it might be so in future.

Perhaps the Australians really have it wrong and superior wisdom rests with Messrs Orr and Bascand. But, frankly, it seems unlikely. Not only are the key Australian officials much more experienced in these matters than ours, and they have the additional worry that there is no prospect of parental support for their banks, but it is the New Zealand proposals which appear to put us out of line with (above) international benchmarks, despite the impressive long-term track record of financial stability here, the floating exchange rate regime, and a now well-established history of keeping governments out of credit allocation.

More generally, in banking systems that have so much in common, in economies with so much in common, surely we should have looked to our authorities to have worked closely with the Australians to have developed as common a regime as possible, recognising (inter alia) that if and when anything really goes wrong with any of the big 4 the problems will be trans-Tasman in nature and are likely to be resolved – and be best resolved – at a trans-Tasman political level. I’m not suggesting Australian officials and politicians have our best interests at heart. Both sides need to look after their own national interests, but those interests can be protected – probably better protected – by working closely together, on as common a framework as possibly, consistent with maintaining/pursuing an unquestionably strong banking and financial system.

As for New Zealand citizens and voters, we really should be demanding much higher standards from our top central bankers, who seem unable or unwilling to answer simple questions and challenges about what the Governor is proposing, or to do so in ways that are straightforward and reasonably defensible That really should worry Grant Robertson, who is responsible for these men and for the institution.

New Zealand has under-performed Australia on an absolute GDP growth and per capita GDP growth basis for many years. But the relative volatility of the two economies is quite similar with Australia’s economy slightly more volatile than NZ – hard commodity shocks tend to be worse than soft – so it’s hard to argue that we need higher capital buffers to insulate against economic volatility.

Our currency volatility is arguably a problem but measures to reduce short term funding and the falling NIIP/GDP have gone a long way to help.

Given our NIIP/GDP ratio, arguably, we’ve been a massive beneficiary of global ZIRP.

LikeLike

Michael

You have been very successful in exposing the fragility of the RB Governors position when it comes to increasing the trading bank’s capital reserves, and rightly so.

My only concern now is that having been humiliated, he is likely to double down on his position rather than engage in a late policy U turn. This means that you/we are now relying upon his Board to reign him in. I’m not sure that as a strategy this is a secure bet.

LikeLike

I don’t think anyone expects the Governor to change course, or (for now at least) for the Board to insist on higher standards. The only person who could demand better is the Minister of Finance and I doubt he is interested/willing.

At this stage I think all the sceptics (like me) believe is that one has to go one trying to do the right thing, point out problems etc. perhaps in the longer term it will help lay the groundwork for change, or for the many senior people who are disillusioned with Orr but not yet willing to speak out, but if not…..well, at least we’ll have done what we could.

LikeLike

1. Second last paragraph agree

2. Look at it through the eyes of the Australian Government. Has the NZ Government considered the extent to which NZ benefited from the GFC program the AU Govt pumped into its economy to stabilise the AU banking system. A great deal. Very easy to sit back and say – geez no problems here

3. As the AU Government has reminded us their illegal refugee programs indirectly benefit NZ

4. APRA total silence about Orr’s program is deafening

5. Looked at through the eyes of APRA you have to wonder

6. Look at Bascand’s address through the eyes of APRA, RBA, AU banks and AU Govt – not pretty – do not expect a good response

7. NZ should have a royal commission into the banks while it had the opportunity. The self-serving self-reporting program mounted by Orr and FMA was less than convincing

8. The whole thing has been unprofessional

9. You may not like it, but as I advocated some years ago the smart thing would be for the Govt to charge the banks an annual licence fee and put the proceeds into a sinking fund to accumulate over time to meet the crisis. That’s the sensible business approach

10. Orr’s complaints about the profitability of the banks is a matter for the Commerce Commission not the RBNZ

11. The Orr-Everett RBNZ-FMA form-filling exercise was stupid and half-baked

12. Read your article above through the eyes of AU institutions and you’ll see what I mean

LikeLike

Just two points in response:

– re your 9, that is essentially what deposit insurance, paid for with annual levies, would do. I’ve supported that for years, so no partic problem

– re your 2, I disagree, but I’m not fully clear whether you are talking about the guarantees (where Aus bounced us into guarantees that ended up costing us quite a bit – via the SCF failure) or the fiscal/monetary stance. On the latter, their stimulus was of similar scale to our own (as I’ve shown in previous posts) – the sort of things all economies did for themselves. The thing that made a big difference to Aus was the China stimulus and the huge new investment surge. Both Australia’s downturn and quick rebound had complex effects on NZ because of the impact on the net flow of NZers to Aus (sharply drops – boosting demand here – when Aus lab makt conditions deteriorate, and vice versa).

LikeLike

This is my just recollection through my eyes – I was there

RE: #9

I’m drawing a distinction between an annual licence fee charged by the NZ Government to the banks and quarantined in a “sinking fund” and managed and reported much like ACC or NZ Super as distinct from a deposit insurance scheme operated by the banks themselves. Sure, the end cost of both schemes could (emphasis on could) be borne by “depositors”, but would be more transparent. Annual insurance premiums tend to have a habit of disappearing into the ether.

RE: #2

I was thinking about the counterfactual – what would have happened if the Australian Government had not implemented a bank guarantee and had left the AU banks to sink or swim on their own. The immediate issue was the freezing of the financial system. The banks were common to both countries. If one or two of the AU banks closed their doors for a couple of months while the crisis settled and things returned to normal would the actions of the NZ Government and RBNZ have succeeded the same? It is recalled that you had prepared your own independent plans. The question is would you have proceeded with them had Rudd not come calling. It is on that basis that it is suggested that the stabilisation of the AU financial system provided an overflow comfort to NZ that would not have otherwise occurred.

Of course, if the NZ banks were not subsidiaries of the AU banks that would be a different set of conditions

AU did not have an NZ like Finance company problem. From memory only 2 AU property developers went bust, Westpoint in WA and 1 in NSW. There was a 3rd one in Queensland operated by a NZ’er that took a couple of years to play out. Australia coupled the bank guarantee with a $15 billion Building Education Revolution (BER) infrastructure package plus its disastrous nationwide pink batts insulation fiasco

Don’t recall anything about a benefit from Chinese stimulus. I do recall comment some years later how lucky AU had been from continued Chinese trade activity. That was a retrospective view. It was not a contemporaneous view circulating in 2008

LikeLike

I certainly wasn’t arguing for a dep insurance scheme run by banks, but (as in most countries) one run by the govt, paid by banks (and depositors).

Re 2008, (a) the big Aus banks would not have failed without the retail guarantees, and (b) your argument seems to be that if the Aus authorities had not done their job we would have been worse off. On the latter, no doubt, but that is also true if other authorities (eg the US) had also not done their job. Countries adopt policies for their benefit (judged rightly or wrong). There are spillovers but they are incidental.

The Chinese stimulus (huge) was more an issue for the fairly rapid (if shortlived) recovery in Aus. Without it, the RBA might well have had to cut interest rates more deeply.

Re dep guarantees, yes we were developing our own plans independently (the Aus authorities having refused to collaborate). Whether we would have used them without the Aus rushed announcement is impossible to tell now, but if we had there would have been more opportunity to haggle over details with ministers, in ways which might (only might) have reduced our fiscal costs.

I guess my bottom line is that we don’t have any special reason to be grateful to the Aus authorities over 2008/09. At a more general level however we should be grateful that Aus is a tolerably well-governed country, tolerably stable, and with banks that have a pretty long track record of operating reasonably soundly (through some mix of their own choices and the regulatory framework imposed on them).

My own bottom line is that we benefit from having a substantially Australian-owned banking system, with subs that have been quite integral to the parents. We don’t hear that enough (barely at all) from the RB,

LikeLike