If people had wanted a centre-left government, one might suppose that they would have voted for the real thing. Despite the additional redistribution announced in yesterday’s Budget, perhaps they still will.

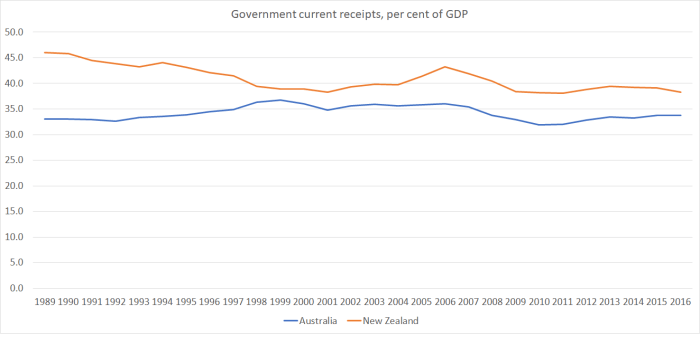

Still, for all the headlines about money being put (back) in people’s pockets, it is worth keeping the overall numbers in perspective. Core Crown tax revenue as a share of GDP was 27.8 per cent last year, is estimated at 27.7 per cent of GDP this year, is forecast at 27.5 per cent in 2017/18, and in the final forecast period it is predicted to be 27.7 per cent. The government isn’t yet shrinking its pre-emptive claim on overall economic resources. Expenditure as a share of GDP is forecast is gradually shrink, and if that was sustained – which will be a challenge, including because of the reluctance to act soon on NZS – it could open the way to future real reductions in the tax burden.

It is sad to reflect that much of the increased spending announced yesterday was simply a palliative for the failures of the government. The cost of housing is, pure and simple, the fault of successive governments’ land-use regulation. In a country with plenty of land, and the lowest real interest rates for decades, housing should be more affordable than ever. That it isn’t, should be something governments are held accountable for (and although governments of both parties have had much the same flawed policies, the current government has now been in power for almost nine years). And the lack of productivity growth – recall that we have had none at all for five years now – is the biggest single thing that holds back the income growth of working people. With a well-functioning housing market, and an economy with robust productivity growth, many of the pressures that led to increased spending yesterday would simply have been unnecessary.

As for tax, how many more decades will we have wait before a simple reform like inflation-indexing the income tax brackets is enacted? Even the United States, with its enormously complex and distorted tax code, manages that one.

Perhaps more importantly, for all the rhetoric about encouraging enterprise – and more subsidies for favoured uneconomic industries (film, rail and so on), there was no sign at all of action to lower what is probably the most costly and distortionary major item in our tax system – the company tax rate. It is curious to reflect that the previous Labour government cut the company tax rate more than the current government has.

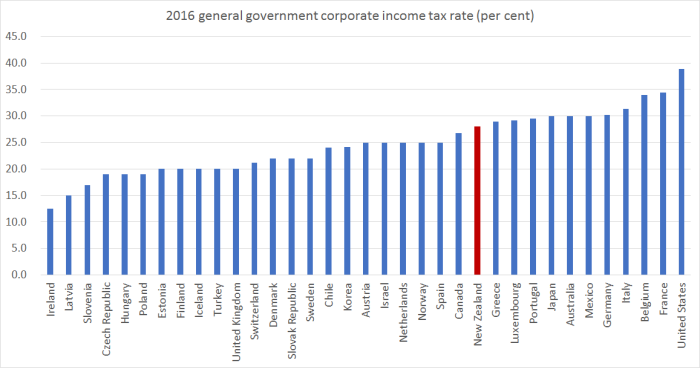

I ran this chart a few weeks ago

New Zealand’s company tax rate is in the upper third of OECD member country rates. For a country that talks a good game about welcoming foreign investment, and supposedly aspires to reverse the decades of productivity underperformance, it simply isn’t good enough. Politicians seem afraid of making the well-established economic point that taxes on businesses are typically borne substantially by wage-earners, not by owners of capital. Less investment than otherwise means fewer high productivity and, thus, high wage jobs. And if our company tax rates are high, it makes it harder for overseas investors to justify locating an operation here rather than in a lower tax country. For a country with a pretty disadvantageous location to start with, it is the sort of additional burden we shouldn’t be putting on enterprise. (I’ve focused this paragraph on foreign investors. Taxes also discourage domestic-owned business investment, but for owners of those businesses, the maximum personal tax rate is ultimately the important consideration, rather than the company tax rate itself).

Anyone who listened to, or read, the Budget speech itself was clearly supposed to come away with a message about how well the New Zealand economy was doing. There on the very first page was the Minister’s claim

“Our economy is 14 per cent larger than it was just five years ago”.

Yes, but the population is about 8 per cent larger. That would leave an annual average growth in per capita terms of 1.1 per cent. Better than nothing, to be sure, but not the sort of stuff most finance ministers would want to boast about.

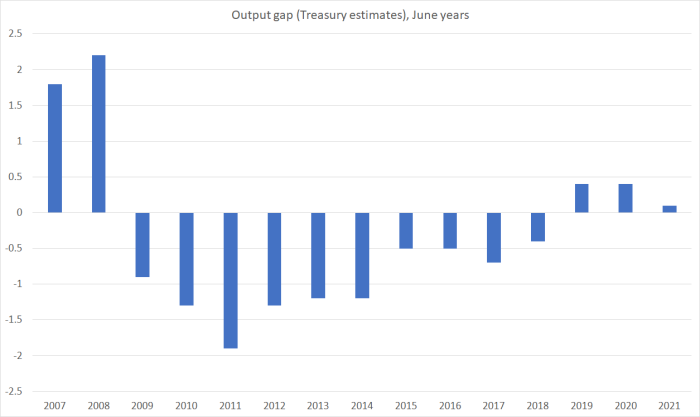

And Treasury’s own numbers – done at arms-length from the Minister – don’t really back up the Minister’s story, whether cyclically or structurally.

Take the cyclical position first. Here is Treasury’s estimate of the output gap (positive numbers suggest activity and demand are running a bit ahead of what is sustainable – “potential GDP” – and negative numbers suggest there is still slack in the economy).

On these estimates, New Zealand will have had a negative output gap – resources being underutilised – for 10 consecutive years, including the whole of this government’s term to date, and the next year as well. One can argue all one likes about what governments should or shouldn’t have done to lift potential productivity growth, but these estimates just take for granted what actually happened with structural policy and look at the cyclical position. And there is really no excuse for putting the economy through such sustained period of resource underutilisation. I can’t think of any time in modern New Zealand history, when the output gap would have been negative for so long.

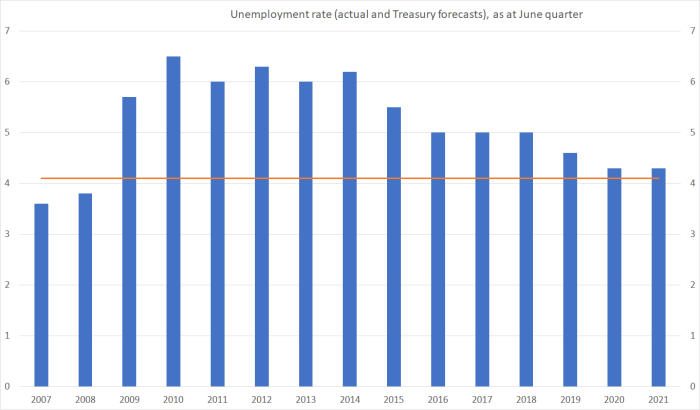

Output gap estimates are pretty bloodless things, that don’t necessarily resonate with a wider audience. They also can’t be observed directly. But here are the unemployment rate numbers (actual and Treasury forecasts).

Last year, Treasury told us that they thought the

Treasury takes the view that the unemployment rate consistent with full employment (the nonaccelerating inflation rate of unemployment or NAIRU) has also fallen over time, so that…. it would be closer to 4.0%

I’m not sure precisely what number they had in mind, although in a chart included in that 2016 paper, the unemployment rate levelled out at around 4.1 per cent, so I included an indicative NAIRU line in my chart at 4.1 per cent. But whatever the precise estimate, on official numbers and Treasury estimates we are looking at 10 years (or perhaps 11) with an unemployment rate higher than necessary to keep inflation in check. The government has consistently presided over less than full employment. That is simply poor economic management, and since we know that having a job is one of the best ways to secure better life outcomes, it is pretty poor management more generally.

Perhaps such unfortunate results might be excusable in a country that had no discretionary monetary policy leeway left (interest rates were already at or just below zero), or which was in fiscal crisis and had no borrowing capacity left. Places like Portugal spring to mind. But not New Zealand. We have a floating exchange rate and our OCR has never got below 1.75 per cent (and even if that capacity had been exhausted, our public debt has been relatively modest).

It is also easy – and right at one level – to blame the Reserve Bank. They do short-term macroeconomic management. But only as agent for the government and the Minister of Finance. The Minister sets the targets and is ultimately responsible to citizens for their performance. I do hope that Treasury, in offering advice to the Minister of Finance (whoever he or she may be after the election) on the appointment of a new Governor, and the design of the PTA, will take seriously the record of underperformance over the last decade. This isn’t some trivial inside-the-Beltway governance issues. These are real lives and opportunites that are unnecessarily blighted.

The government also likes to pretend that New Zealand’s economy is doing very well by international standards. Thus, we are told by the Minister that

“we are at the moment growing faster than the United States, the UK, Australia, the EU, Japan and Canada”

One would certainly hope so. Our population is growing materially faster than the population in any of those countries/regions.

But what about per capita growth?

I noticed various commentators yesterday suggesting that Treasury’s growth forecasts looked a bit optimistic. I had some sympathy for that view, but here I’ll just take them at face value. And I wondered how their forecasts for real per capita GDP growth compared to those the IMF has recently published for each advanced economy.

Treasury forecasts on a June year basis, and the IMF numbers are for calendar years. Over a forecast horizon of four years (Treasury’s horizon), it shouldn’t make much difference. In the chart below I used Treasury’s forecasts of real per capita growth for the four years to June 2021, and compared them to the average of the IMF’s forecasts for the four years to December 2020 and the four years to December 2021.

If the Treasury numbers are right for New Zealand, our growth in real GDP per capita would be just slightly below that of the median advanced country over the next four years. I guess that isn’t that bad, but it isn’t much to boast about either.

After all, our per capita incomes are a long way down this list of countries. On the IMF’s numbers

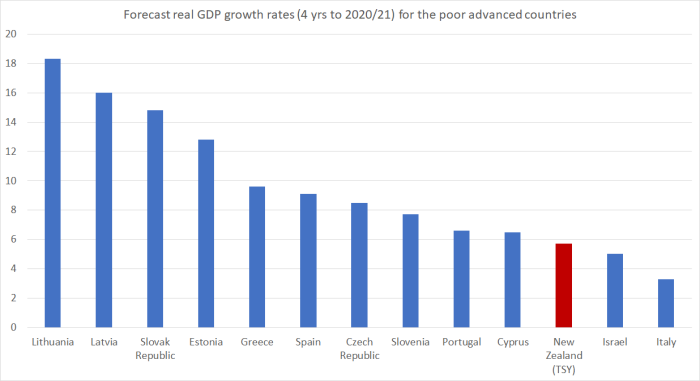

The aim – supposedly – for a very long time has been to catch up again with those top tier countries, almost of whom we were richer than not that long ago. And catch-up or convergence certainly isn’t unknown, or unexpected, for other countries. Here is how those Treasury forecasts for New Zealand’s real per capita GDP growth compare to the IMF’s for the 12 countries poorer than us.

We only manage to beat two of those countries. In fairness, of course, some of those poor advanced countries are recovering from savage recessions. But even if one just focuses on the six former eastern-bloc countries, all but one is forecast to not only manage faster per capita growth over the next few years, but also to have achieved faster growth than New Zealand for the whole period from 2007 (just before the global recession) to 2021. They are catching up. We aren’t.

(Compared with the richest 12 advanced countries, we are forecast to match the median per capita growth rate of those countries over the next four years, but the eastern Europeans are actually catching up.)

In wrapping up his Budget speech, the Minister of Finance claimed that

“we have a strong and growing economy built on a strong economic plan. We must maintain our focus on growing the economy and sticking to the plan”

Earlier he had claimed that

Under the Government’s strong economic leadership, New Zealand is shaping globalisation to its advantage. We’ve embraced increased trade, new technologies, innovation and investment.

All this in a country where exports as a share of GDP have been shrinking. And productivity growth has been all-but-non-existent for years.

The bare-faced cheek of these assertions should be breath-taking. Sadly, it seems like just another episode in a long succession in which the government simply makes stuff up.

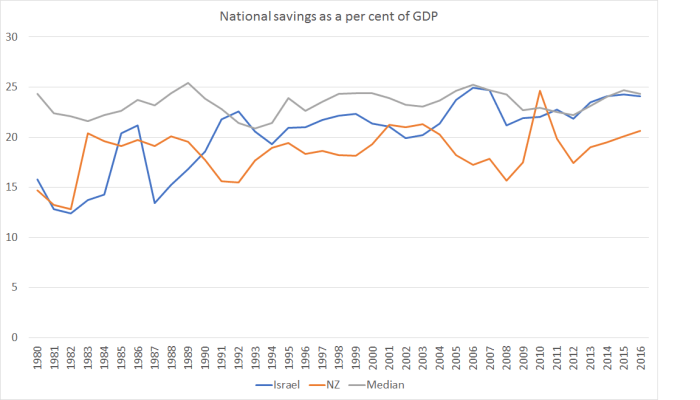

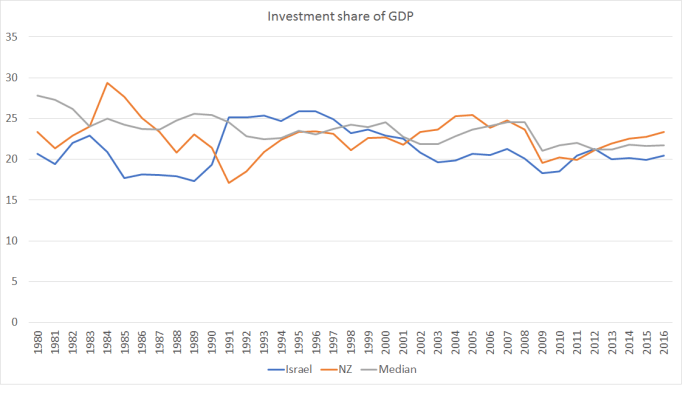

There is plenty of cyclical variation, but in both countries on average over this period, the share of investment spending in GDP has been a bit lower than advanced country median. Given all the resources that needed to go to meeting the needs of the fast-growing populations (simply maintaining capital per person), there will have been materially less “left over” for capital deepening, or for new businesses and ideas. It isn’t a mechanical rationing process, but just a response to the opportunities and the relative prices.

There is plenty of cyclical variation, but in both countries on average over this period, the share of investment spending in GDP has been a bit lower than advanced country median. Given all the resources that needed to go to meeting the needs of the fast-growing populations (simply maintaining capital per person), there will have been materially less “left over” for capital deepening, or for new businesses and ideas. It isn’t a mechanical rationing process, but just a response to the opportunities and the relative prices.