The government’s target for a substantial increase by 2025 in the share of exports in GDP has been something of a hobby-horse issue of mine. I’m sure it was well-intentioned (the thinking behind it probably recognises that successful economies, catching up with the most highly productive countries, typically experience a more rapid increase in exports than in GDP as a whole). It isn’t that exports are special, just that (among other things) one measure of the success of one’s firms/industries is the ability to sell more and better stuff on the (much larger) wider world market. That, in turn, enables us to import lots (more) of stuff from the rest of the world.

In parliamentary questions earlier in the week (number 8 here), Labour’s Finance spokesperson Grant Robertson was asking the Minister of Finance about that export goal, now expressed as aiming for real exports as a share of real GDP to get to 40 per cent by 2025. Unfortunately, the government’s record on this item is so poor that one could almost feel sorry for the Minister, except that he devised the target and has repeatedly championed it. He has also been the man behind such questionable “export subsidies” as the amped-up assistance to the film industry, and the large scale pursuit of foreign students attracted not so much by the excellence of our institutions as by the work and potential residence opportunities dangled in front of prospective students. Export subsidies are just a bad idea, but export targets increase the risk of being tempted by such bad policies.

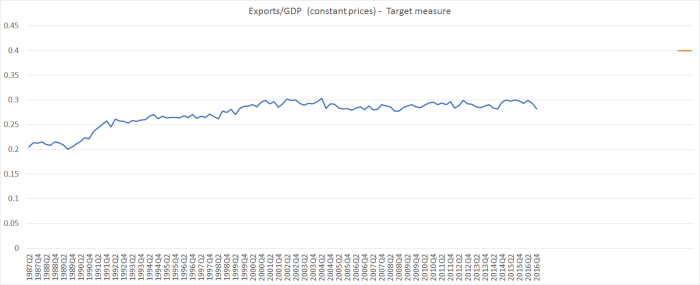

Statisticians (including those at Statistics New Zealand) advise against using ratios of real variables over long periods of time. I know why the government and MBIE do it for exports (it abstracts from the direct effects of fluctuations in export prices and in the exchange rate), but it still isn’t really kosher. Nonetheless, that is how they’ve expressed their target. And here is the data, all the way back to 1987, and with the target level for 2025 highlighted in orange.

In his answer in Parliament, the Minister noted that the export share had been “remarkably stable for the last 10 or 12 years”. Actually, make that more like 16 years.

Now somewhat oddly, in his answer the Minister of Finance kept referring to the recent drop in dairy export receipts as some sort of mitigating factor. But that has been largely a result of the drop in prices, and the main reason for using the real exports to real GDP measure in the first place was to focus on volumes and abstract from the influence of fluctuations in global prices. The drop in dairy prices is, for these purposes, simply irrelevant.

Incidentally, within that real exports measure we can break out the data on exports of services. Between the political rhetoric around foreign students and tourism recently one might have supposed those bits would have been doing well. And we are often told that “weightless” services exports are part of the way of the future. But here are real services exports as a share of real GDP.

There was a bit of a pick-up a couple of years ago, but the current level is around a level first reached in 1995.

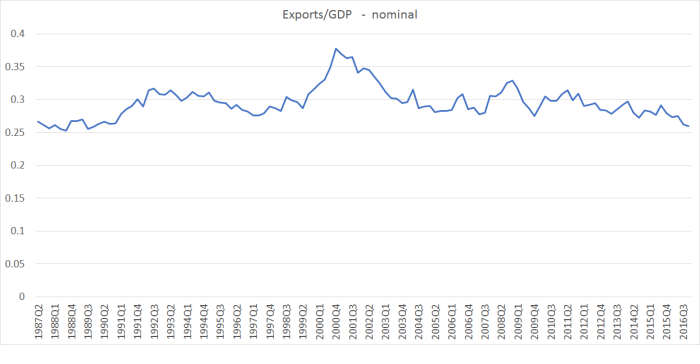

As the statisticians recommend, I prefer to look at ratios of nominal exports to nominal GDP. There are no deflator problems, just the straight dollar value of what is exported from New Zealand and the dollar value of New Zealand’s GDP. The trade-off is that there is bit more noise in the series. Since neither series is mechanically controllable or even directly targetable in a market economy, I don’t think it is much of a loss. Here is the chart of nominal exports to nominal GDP, again back to 1987.

Here the fall in global dairy prices does matter, but even then not in a straightforward way. After all, all else equal, when the price of our largest export falls one might expect the exchange rate to fall. On this measure – the simplest measure – exports as a share of GDP are at a level not seen since the very last quarter of the 1980s. A generation ago.

The Minister of Finance was also at pains to point out that over the last decade or so the pace of growth in world trade has slowed, and that is true (although a significant part of that has been the rebalancing of China’s economy). So perhaps no one would hold it against him if the progress towards his own 2025 target – now, as he notes, only eight years away – was lagging a bit behind expectations. But on his preferred measure there has been no progress at all. On the better, if a little more volatile, measure things have been going backwards. And yet this was the government that once had the ambition of closing the income and productivity gaps to Australia.

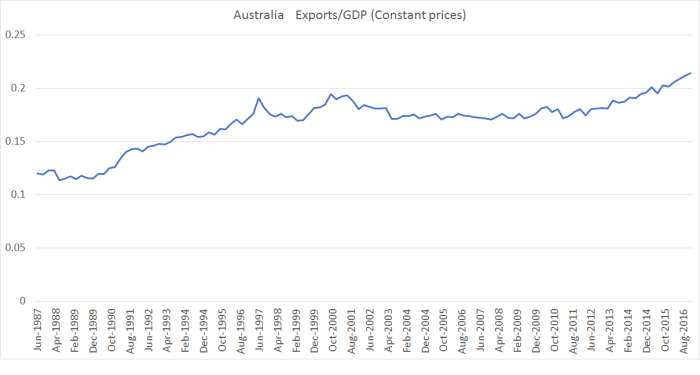

Australia provides an interesting comparison. Here is the constant price ratio for them (the measure our government prefers for NZ),

Historically, Australia had a materially lower export share of GDP than New Zealand – as one would expect in a larger country (where there is more scope for efficient profitable trade within national borders). And for a decade or so their real export share of GDP also went sideways, but for the last few years it has been rising again quite strongly.

They are also affected by changing commodity prices and exchange rates. But here is the simple chart of nominal exports to nominal GDP.

It hasn’t been rising for some time. But whereas our export share of GDP is back at 1989 levels, in 1989 Australian exports were about 15 per cent of GDP, now they are about 20 per cent.

That is the sort of change our government needed to be seeing (roughly a one third increase in the export share of GDP) if its 2025 exports target was to be met. It looks exceedingly implausible at present. There was no progress under the previous government, and has been none under the current government. That strongly suggests something wrong with the policies both governments have been pursuing.

I like to think I’m an equal opportunity sceptic. There is a little sign of the sorts of policies from the current government that will change this picture. But while it is fine – and no doubt fun – to tease the Minister about the failure of his policies, we don’t yet know what policies, if any, Labour and the Greens will advance to have the economy change course, and shift to new higher levels of international trade. Without something that does that, our prospects for closing sustainably any of the productivity or income gaps are slender to non-existent.

Another Wellington slant

10 April 2017 – Bernard Hickey – Newsroom

Export Target 40% quietly shelved

‘https://www.newsroom.co.nz/2017/04/09/18670/economy-target-exports

The Government’s once-central target of lifting exports from 30 percent of GDP to 40 percent of GDP by 2025 has gone missing in action in recent months with little progress seen after nearly eight years in power and senior ministers quietly stopping referring to it

LikeLike

Thanks. HOwever, Steven Joyce did (in answer to Robertson’s PQ) reiterate that the target still exists and will be in the next update of the Business Growth Agenda.

LikeLike

Government’s Business Growth Agenda is political – aimed at Staying in power

Mood of the Boardroom: Time to refresh growth agenda

“The Government gives every impression of being primarily focused on staying in power, and has taken no steps to accelerate economic growth

-http://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=11716940

LikeLike

That’s not correct. The government has pulled every lever to get the economy growing and they have been extremely successful. GDP is running at 3% plus. Building activity is at record levels. Housing building is at record levels. Anyone that is interested in working is working. The NZ economy has diversified away from farming cows and is a lot more resilient than it has ever been.

Business confidence is very high.

LikeLike

“government 40% export target going nowhere”

It can never go anywhere but backward while immigration into New Zealand runs at 100,000+ pa and new arrivals are not “required” to work in the export sector as a condition of their Visa

It’s in the mathematics. – Government pursued twin policies that opposed one another until one failed

Immigration has the effect of increasing GDP. We know that the increase in population is a world leading number. However, one mitigating factor is GDP is not increasing comensurate with the population increase

While exports remain static or increase at a rate less than the rate of growth in GDP then Exports as a share of GDP must decrease

LikeLike

Immigration of 100,000 plus includes international students who contribute to the $5 billion in export GDP, the 40,000 foreign construction workers that contribute to the $20 billion rebuild of Christchurch and Kaikoura, and also the $5 billion in Aucklands intercity Rail, the $3 billion in construction for more housing.

LikeLiked by 1 person

Don’t forget the 30,000 returning New Zealanders also included in the 100,000 plus immigrants.

LikeLike

Tourism export dollars directly translate to domestic GDP spending. Therefore Tourism export GDP as a percentage of Total GDP will never shift the proportion in favour of export GDP.

LikeLike

What?

All export receipts appear in the domestic economy as spending (a dairy farmer buying groceries or paying a contractor for example) so what makes you say a tourist spending foreign dollars is different? Exports and imports are separated out when calculating GDP which is turnover plus exports less imports. Or is tourist spend somewhat like a snake eating it’s own tail.

LikeLike

Yes indeed what?? The sad reality is the Export GDP of our farmers is not spent in the local economy. Farm debt is around $60 billion. Interest payments on that at commercial interest rates of say 7% amounts to a whopping $4 billion. Palm oil kernel and other supplements, antibiotics, chemical wash for ticks would be imported would be say $2 billion. Farm machinery and equipment, automating the suction components, switches, push buttons, electrical components are either Rockwell, Siemens or ABB. say $1 billion.

Also farm debt has to be repaid which equates to say $3 billion a year in debt repayments. Oh wow that adds up to external costs of $10 billion. The export GDP of farmers is around $15 billion.

Therefore the amount.available to be spent in the local economy by a farmer is a grand whopping 30% of export GDP compared to tourist GDP which is 100% spent in the local economy.

LikeLike

You can’t just look at one side of the ledger to try and excuse your prior comment GGS.

The obvious problem with your argument is that the tourist industry has debt as well; debt to help pay for all the camper vans, hotels, aircraft and so on. It also uses imported fuel, food, foreign staff and tour guides and a lot of the hotels and activities are foreign owned but just like the farmer none of that matters to the export figure as it only shows up in the current account. Our sick net overseas position and 45 year continuous current account deficits are the real cause for concern. I blame Auckland.

BTW the amount the farmer or tour operator receives is added to GDP in the first instance, it is counted again once it is spent in the local economy and again when it is spent by the contractor, shopkeeper or bank depositor and so on ad infinitum. Comprendé.

LikeLike

No you are wrong. You have extended the discretionary spending model into level 2 for Tourism. You have to stick to comparing apples with apples. A farmer has discretionary spending of only 30% of export GDP into level 1 discretionary spending. This is the same discretionary spending he would make as a tourist will make at level 1. That farmer will use exactly the same services that a tourist will use. The tourist will make 100% discretionary spending in the local communities. The farmer will only make 30% discretionary spending in the local communities. That is level 1 discretionary spending. Level 2 is the spillover from that level 1 discretionary spending. You forget that a farmer is a person like a tourist is a person and will use the same services, restaurants, cafes, supermarkets the same pubs. Perhaps not hotels as he has his own home. But his own home will have interest on residential debt which is on top of farm debt to pay and that offsets the interest that hotels pay on their debt. But a farmer will take holidays in NZ and would be counted as a domestic tourist.

LikeLike

You can blame Auckland as much as you like but again you are wrong. 1.5 million people in Auckland generate a GDP of $75 billion. 10 million cows generate only $10 billion in export GDP but produces the dung waste 20 times a average person which is the equivalent of 200 million people. The end result is dirty waterways, unswimmable lakes and rivers, contaminated water supplies, coastal Algae bloom, decimated coastal fishing stocks from nutrient leaching and of course global climate change from Methane gas emissions, ozone depletion. Etc.

LikeLike

Where this idea first came up, I was work in a certain place. I mentioned that to a 10% increase in exports as a percentage in GDP but also requires imports to go up by the same measure. No one had any idea what I was talking about; that the trade balance must balance; that the balance of payments must balance.

LikeLike

I don’t if that’s correct either Jim, we’ve got countries (China, Germany ) running massive trade surpluses and others (USA, Britain) running trade deficits. The deficit is supported by borrowing from (or selling assets to) the creditor nation – the current account. We have often had a trade surplus but haven’t had a current accounts surplus for forty five years and counting. This is mostly due to our useless cities propensity to spend way more than they earn.

LikeLiked by 1 person

I do not think New Zealand needs to run a trade surplus equal to 10% of GDP and therefore will be a massive capital exporter.

LikeLike

We don’t need to run a 10% trade surplus Jim but we really do need to do something about the current account deficit which, as I said has been in the red for most of our lives. The deficit has been up around 8 or 9% of GDP which represents a massive loss of wealth bleeding away each year. It’s not too bad at the mo thanks to low interest rates (about 3% of GDP) but we still need substantial trade surplus just to stand still and to help balance the heavy outflows to our foreign owners. The effect of decades of C.A. deficits can be seen in the overseas investment balance so we have a very long way to go before we are exporting capital as far as I can see.

LikeLiked by 1 person

If you include sales of houses to foreigners in the current account then NZ would have a positive current account. The annual sales of houses in total is $60 billion. IRD records indicate that 4% of sales are to non residents which equates to $2.4 billion. If you believe Labour’s Phil Twyford, then sales to foreigners is 30% of house sales which equates to a whopping $18 billion. Most economists believe it is likely closer to 10% which would add $6 billion to the general wealth of New Zealanders.

That’s probably why city folk do not feel poor even though poverty stricken farmers do feel poor and provincial towns are shrinking. Provincial towns should thank the National government for injecting tourist dollars into dying provincial towns.

LikeLike

I wish I could honestly say “incredible”. Sadly, it is all a bit too believable.

LikeLiked by 1 person

I had a bit of a look around but I cannot find any calculations of the maximum size of the import sector of the New Zealand economy to see if it was less than 40%. If we imported every possible good and service, how much of GDP with that be?

LikeLike

GDP measures the Gross so it is not net of imports. We import and GDP is the margin on top of imports to work out GDP.

LikeLiked by 1 person

There isn’t an answer is there? It must depend substantially on the import component of exports (thus some places have import and export to GDP ratios of 100% or more).

LikeLiked by 1 person

I think it was political madness to have even announced a export target, the govt has just opened themselves to being beaten around the head.

We are an open economy, our exports are the result of a myriad of decisions made by thousand of business people, not a 5 year leap forward to 40% exports like a Marxist economy.

Like most people I would like to see more value add, and a deeper and broader range of product, but nice to see the value of our wine exports have exceeded Australia’s in value terms to the US market.

Perhaps we need negative interest rates so our real (and nominal) exchange rate will drop to encourage the xport sector 🙂

What lessons can we learn from Germany, many I suspect, but as I say we choose to fail (be ordinary) or do we suffer from the South Pacific disease….Island Time?

LikeLike

Negative interest rates might be an odd thing to wish for. I suspect all we need is interest rates similar to, or even just slightly below, those of the other advanced economies. Why hold NZD for the same yield you can get on a much more liquid asset in the US, euro area or wherever. The gist of my macro analysis argues that sharp cuts in the immigration targets are a way to bring that about.

Not sure about lessons from Germany. They are severely distorted in the other direction: outside the euro it is likely a new DM would soar in value, and Germany’s export share (and current account surplus) would drop back to more normal levels.

LikeLike

The government pursued an export solution in international students and in tourism which are now our largest export industries that gave our export GDP a huge boost with annual increases around 12% to 15%. Because our economists are so very poor advisers, they did not realise that the spillover into the local economy in domestic GDP was just as high because 100% export GDP of international students and tourists spillovers 100% into local discretionary spending in the domestic GDP. You can never ever have export GDP rising as a percentage of total GDP while you are focused on international students and tourists. But bugger what economists say. It’s real foreign cash we all get to spend it at our discretion.

LikeLike

I would hate to see negative interest rates in NZ, it was a tongue in cheek comment, if we get there it is definitely the beginning of the end, or the end of the beginning.

My point exactly, all the RB committee can do is hold interest rates above the “advanced” economies, and if they go negative then they will crap their pants, coz it must be their worst nightmare. So what choice do we have but to follow them down, and down and down but look like we are making intelligent decisions. I’d be buying gold myself, not some shithouse currency called the USD or the Euro, with all that QE in both currency areas can you tell me what their “true value ” is…. I doubt it.

The lessons from Germany are their education system, their industrial policy, their business attitude, their engineering skills, their IT skills as applied to machine mechanisation, their attention to detail, their attention to business basics, their attention to customer relationships. These like the Swiss currency would survive the Euro soaring, or the reversion to the DM in their case as nothing beats quality, eg machine tools

LikeLike

Any gains on buying gold is considered a taxable profit. So you have to factor in the tax payable in your holding cost.

s CB 4

In the Commissioner’s view, gold bullion bought as an investment will necessarily be acquired for the purpose of disposal and consequently any amounts derived on its disposal will be income. The Commissioner considers that the very nature of the asset leads to the conclusion that it was acquired for the purpose of ultimately disposing of it. Such a commodity does not provide annual returns or income while being held and has use or value only in its ability to be realised.

Click to access pub00227.pdf

LikeLike

It really is amazing; to think NZ has had this target for so long, and by your preferred nominal measure we are actually going backwards. Looking at some other countries, such as Poland or Slovenia, they all have measures around or above 50%:

http://www.tradingeconomics.com/poland/exports-of-goods-and-services-percent-of-gdp-wb-data.html

http://www.tradingeconomics.com/slovenia/exports-of-goods-and-services-percent-of-gdp-wb-data.html

And yet they both have low population growth (basically flat) for the last 25 years. Its also worth noting the peak of NZ exports as % of GDP; as expected its around year 2000 and when the twi exchange rate was at an all time low: http://www.rbnz.govt.nz/statistics/key-graphs/key-graph-exchange-rate

If the government was serious about this target it should do something to lower the exchange rate…. hey maybe like lowering migration?

LikeLike

Richard Boyes I don’t see the relevance of Poland, one of the poorest countries in Europe. It has some of the lowest spending on health and education in Europe.

Between 2000 – 2005 the second biggest emigration in the world was Poles to Germany, 800,000 Poles live in the UK alone. 11% of the population emigrated!!!. Replaced by Ukrainians!

It only makes up 2.5% of the EU GDP and has the 6th lowest labour costs in the EU as well. Of the 50 weakest economic regions in the EU Poland fills most from the positions 40-50.

80% of its exports are sold to the EU. Hardly a stellar performance that we want to emulate.

Unlike NZ where we have to ship our exports 15,000 – 24,000 km around the world.

Poles also think their Govt is one of the most corrupt in Europe, or least trustworthy

LikeLike

Imports arrive at our doorstep travelling those 15,000km which our local manufacturers with only 100km travel distance can’t compete with. It is not about distance because our imports prove it is not about distance. It is about economies of scale. We adjust do not have a large enough local market to produce cheap enough to compete with our global competition with larger domestic markets.

LikeLike

Its not a like for like story, but its a country that has gone from 50% of NZ’s GDP per capita to close to 70% in the last 15 years, as Michael pointed out here:

https://croakingcassandra.com/2015/11/25/a-cause-for-great-celebration/

Its a point Michael is trying to make; having a flat or falling population does not mean a decline in living standards and can improve things.

Our government and others before it have done nothing in terms of catching up with Australia, even though it has been a stated aim for some time; it is failing. Many other countries are catching up to the living standards in western europe, and will soon be overtaking us. Perhaps we can learn something from this?

LikeLike

Nah we had negative population between 2007 through to 2011. Lots of empty houses. Poverty stricken economy. Record mortgagee sales. No thanks. Give me growth any day over decline.

LikeLiked by 1 person

Getgreatstuff , yes I have no problem with that, dividend on shares is taxable, as is other sources of income.

Like any prudent investor I have a range of investments against debasement of the currency.

As Michael, I think, has explained, you don’t actually own the money you have deposited at the bank, they issue you with an IOU essentially. A promise to pay if you want it back

As Michael as also pointed out before, the Reserve Bank Act allows the bank to haircut your deposits to save the Big 4 banks from collapse as a result of their own stupid investment decisions. Bet as an individual they wont be a tax deductible expense, unlike some facets of gold ownership.

Suggest you read some of James Rickards books, eg “Currency wars” to give you a flavour other than the Neo Classical economist view 🙂

LikeLike

A currency war is being fought at the moment. It just took the USA a long time to finally fight back with QE. NZ is just a small cork floating in a large ocean. Our problem is that we think we are a mighty oil tanker with enough horse power to cut through these stormy seas. When the US started QE we should have responded with a QE of our own. That would have led to a lower NZD, lowered interest rates against our global competition and likely sparked a revival of our industries.

LikeLike

Really GG stuff I can seriously believe you are suggesting this as a serious policy prescription QE?

The GFC happened because the US banks, investment houses and any rag bag assortment of quasi financial institutions balance sheets were beyond ruined.

The Fed, who you should know, are a bunch of wall street bankers, not “theoretically” independent like our RB, they introduced QE to save their sorry “asses”, or rather their balance sheets. Having first shattered America’s “real” economy, that is the part that produces real wealth..not Wall Street assholes!

It is purely “the great experiment”, nobody knows where it is going, or how it Is going to end, but most commentators would suggest in tears. It is purely a method to allow them, the bankers , to rebuild their balance sheets before the real crap hits the fan.

For such a comment, and I assume you are an American, I would revoke your residency permit!. For NZ to follow this piece of financial engineering would be crazy. But of course we have had to, as Michael will tell you, every 3 months our RB governor meets with his learned colleagues, and pretends to the rest of us that they are making informed, independent decisions about interest rates, as they follow US rates down.

As I mentioned in a post before they must lie awake at night wondering what the hell they will do if rates go negative or the Dairy sector implodes and destroys the 4 big banks! Good bye savings dear NZ citizens…

So GGstuff in summary, stoopid, as you yanks say, our industries must learn to live and fight at a higher exchange rate, like the Swiss, like Germans, if we want to succeed as a nation.

LikeLike

Switzerland’s central bank shrugged off criticism of its negative interest rates, sticking to its recipe of ultra-loose monetary policy and currency intervention on Thursday amid “considerable” economic uncertainty in Europe.

http://www.reuters.com/article/us-swiss-snb-rates-idUSKCN11L0N7

LikeLike

Germany became on Wednesday the second G-7 nation after Japan to issue 10-year bonds with a negative yield, highlighting a willingness among investors to hold top-rated debt even as yields across the world collapse.

http://www.cnbc.com/2016/07/13/germany-becomes-second-g7-nation-to-issue-10-year-bond-with-a-negative-yield.html

LikeLike

Ross Mc. so you must think all the Central Bankers around the world are wrong and stooopid and New Zealand central bank is the smartest Central Banker in the world? Does that not sound like my cork in an ocean analogy? And you wonder why we do not have high productivity industries left? Don’t forget interest rates is an input cost to a business. The higher the input cost the less profitability. Lack of profitability equates to inability to pay high wages. Lack of profitability equates to zero spend on research and development. Lack of profitability means can’t afford to train apprentices.

That’s why we are left with industries like milking cows, international students and tourists and not much more than that.

LikeLike

Some examples of negative interest rates are central bank policies. In the eurozone, in Denmark, Sweden, Switzerland and Japan, central banks have decided to have a negative rate on commercial banks’ excess funds held on deposit at the central bank. In effect, private sector banks have to pay to park their money.

http://www.bbc.com/news/business-32284393

LikeLike

GGstuff I referenced your cork analogy with my comment about our interest rates, “following the Fed down” its self evident so I didn’t bother commenting on it.

So what were these high productivity industries you mention? As for your disdain “like milking cows, international students and tourists and not much more than that” I cant understand your logic here.

We are the best cow milkers in the world, the most efficient, the most educated, the most productive, and yes we add value, A2 milk, Fontera, cheeses, etcetc

Similarly with our beef, our lamb and wine, and other agricultural exports.

As for students and tourists I love them, Australia love them too and gloat over both as a significant contributor to their export returns and economic activity, $45 billion dollars.

While Michael has used Australia as a comparison it should be noted that over 40% of their exports are minerals, coal and iron ore. Hardly a stellar value add is it ?, compared to our wonderful farming sector.

As for the US economy “The vast majority of U.S. economic output is services – including knowledge-based sectors such as information technology, financial services, logistics and distribution, education, marketing, legal and a host of other high-end professional services where America has no equal.” Source is tradevistas web site.

As for negative interest rates, yes I am well aware of all that nonsense, just because the ECB follows the Fed doesn’t make it right. So where is the market clearing interest rate then, -5% or -10% perhaps -15%, in 10,000 years of commerce nobody with any sanity has tried running business or commerce, or a country on negative interest rates.

LikeLike

I was working for Fletcher Challenege Ltd 30 years ago when Fletchers was the largest company in NZ with diverse activities. Fletcher Challenge Ltd., New Zealand’s largest group of companies, specializes in transforming resources into value-added products that were marketed both domestically and around the globe.

Eg. BlueScope Steel, Australia’s largest steelmaker and owner of the New Zealand Steel mill, has agreed to buy assets of Fletcher Building’s Pacific Steel in a $120 million deal that will lead to the closure of Fletcher’s steel mill at Otahuhu at the end of 2015.

Today it is just a building company and Fonterra dominates.

Fisher and Paykell used to be a NZ company that manufactured and exported white ware from NZ. Now it is just a research department of Haier, a Chinese company.

Carter Holt Harvey sold its pulp and paper manufacturing to Oji , a Japanese company.The PPP Business principally comprises the Kinleith pulp & paper mill, Tasman pulp mill, Penrose paper mill, and the CHH Group packaging businesses in Australia and New Zealand.

By the late 1980s, New Zealand Breweries had developed into one of New Zealand’s largest companies. In 1988 Lion Breweries took over LD Nathan & Co, New Zealand’s largest retailer. Lion Nathan is now owned by Kirin, a Japanese company.

LikeLike

After years of speculation and concern, the Cadbury factory in Dunedin will finally close next year, leaving about 350 people facing an uncertain future.Our people in Dunedin are among the best performing teams in the region and, if it weren’t for their dedication and outstanding performance, the factory might have closed some time ago. Tourist attraction Cadbury World will remain open despite the planned closure of Cadbury’s manufacturing plant. The company said it remained committed to Cadbury World, which attracts 110,000 visitors a year.

Is it about distance? No because products will still be sold into NZ and will travel the longer distance to get to markets in NZ

Is it about productivity? No because the people are some of the best performing in the world.

Is it about the NZD? Perhaps, NZ with higher interest rates than Australia have resulted in a higher NZD. The NZD is almost on par with the AUD. we have lost our our exchange rate competitive advantage.

Is it about economies of scale? More than likely. With a larger Australian domestic market it makes sense to have more automation and a larger factory to service a larger market in Australia and the reduced unit cost with lower interest rates on funding in Australia and the higher NZD meant that it was cheaper to manufacture in Australia.

LikeLike

It’s not that I have any disdain for our milk production. I was in awe of NZ milk production. The largest exporter in the world. I started looking closely when Michael came up with charts that migrants in Auckland is an anchor to NZ. I could not believe that a top advisory consultant could even think that a cow was more productive than a human being. Evolution suggests otherwise.

That was when I realised that productivity and GDP per capita was a load of rubbish when you start looking at the other side of the equation which is what does it cost to actually be the largest exporter of milk. It meant that we had to have 10 million cows to only generate $10 billion in Export GDP. And it has severe limitation as a growth product as it was limited by the amount that a cow eats (ie land constrained) and of the waste that is produced by a cow. Cows eat and create dung waste to the equivalent of 20 people ie the equivalent of a country with 200 million people. 200 million people don’t just sit around and do nothing. Humans are creative and do things and make things. Cows just make milk. This meant that 200 million people in NZ will create GDP in excess of tens of trillions compared to the $10 billion that cows generate.

LikeLike

Your comment “negative interest rates are nonsense” again brings up the cork in the ocean analogy. It does not matter whether it is right or wrong. We are too tiny to decide what is right and wrong. If the big central banks are doing it, it is because they realise that their respective industries cannot compete. Right or wrong it is about the survival of your manufacturing industries and survival in global competition. Lowering debt interest lowers the input cost to your industries and makes them more competitive. No point doing the perceived right thing and find you don’t have many industries left standing as we have done.

LikeLike