My honeymoon was paid for by a week or so helping an arm of the expansionist and repressive Chinese government (the IMF was paying, and it involved helping run a course in some obscure provincial city on liquidity management and the implementation of monetary policy). In more recent times, I’ve also done a couple of lectures on New Zealand economic management, under the auspices of the Australia New Zealand School of Government, for groups of up-and-coming Communist Party officials – ANZSOG had wanted Graeme Wheeler, and they got me instead. Indeed, to my own bemusement, for a time I even held a security clearance that (I was advised) meant that if, for example, I wanted to take a holiday in China, I needed to give advance notice to, maybe even seek approval from, our intelligence agencies.

These days it is hard for many people in the public sector to avoid sullying themselves with contact with Chinese government/Party representatives. Some of that, no doubt, is just an inevitable part of state to state diplomacy. But when the opportunities arise, there is also the fascination with an ancient culture, and its modern manifestations, and with a country that is home to perhaps a fifth of the human race. Perhaps it was like that for the Soviet Union in earlier decades? Or Germany in the 1930s? It is easy to say now, but with hindsight I now regret the (very small) assistance I provided to the Chinese government and their officials. However amiable and intelligent individuals might be – and there were many such in Soviet Russia and Nazi Germany – they worked for, and advanced the cause of, a state which is the enemy of freedom, and the enemy of the values that made this country, and countries like it, what we are. A state with an active aggressive agenda, propounding internationally an alternative authoritarian vision of governance, and brutally suppressing those who disagree with them. A state ruled by a Party which actively connived in the murder and starvation of tens of millions of its own people.

Which is why those people (including the man himself) attempting to dismiss the concerns raised in the Financial Times/Newsroom stories about National MP Jian Yang as somehow “racist” are just playing distraction and trying to avoid the real issues, and real questions.

Would I be worried if, say, the National Party (or any other party for that matter) had made as one of its MPs someone with an equivalent background in the former ruling parties and military intelligence institutions of former authoritarian states like, say, Paraguay, Zambia, or Serbia? Well, yes I would to some extent. Such a background would speak of the values of the individual concerned – and there has been no suggestion Jian Yang was forced to work for military intelligence or join the Communist Party; instead he will have been judged “reliable” to have been allowed to do so. It would also say something about the values of a New Zealand political party which treated so lightly our own historical values and freedoms as to recruit someone like this. Perhaps prioritising party fundraising over the values and freedoms of New Zealanders?

But in those cases, (a) the authoritarian states are now democracies, and (b) they are countries (chosen deliberately) with no particular interest in, or wish to exert influence on, New Zealand.

What about people with backgrounds in the intelligence services of the United States, the United Kingdom or (to use the example an FT columnist cites) Italy? Frankly, I would have some concerns about the ability of someone who has ever worked in the military and intelligence establishment of another country to ever completely relinquish those loyalties and put the interests of New Zealand first. Then again, such countries – whatever their faults – have been our allies over many decades. The potential for serious conflicts of interest are much less than they are for some other regimes.

In other words, these things are points along a spectrum. I’m not sure that former members of foreign intelligence services ever have a place in our Parliament, but those of Australia or the UK worry me less than those of the US, which worry me less than those of Singapore, Paraguay or Serbia, which worry me less than those of Russia or China. The latter two are (a) large, and (b) aggressive powers. Of the two, China is much more of threat in this part of the world than Russia. But in the 1970s, the order might have been reversed. Imagine a former KGB officer serving in the New Zealand Parliament in the 1970s, advocating the interests and view of the Soviet Union, and hob-nobbing with representatives of the Soviet Embassy.

Some people come out of the establishment of brutal aggressive authoritarian states and recant completely their former loyalties. Their eyes have been opened to the evil that state represented, and often such people become leaders in the cause of urging people in the West to recognise the threat. Sometimes, even, with the zeal of a convert their opposition to the state of their birth can be uncomfortable or even a little embarrassing. And I don’t suppose that after his defection Oleg Gordievsky spent much time with the Soviet Embassy in London.

But what of Jian Yang? I had a look yesterday at his maiden speech in Parliament, delivered in February 2012. Maiden speeches are often an occasion for a new member to outline their personal philosophy, and the things that made them who they are, and led them to seek to enter politics. A few are classics – I recall being taught from Sir John Marshall’s in my first year politics course decades ago. But what of Yang’s?

Read without knowing he’d been a member of the Communist Party (well under 10 per cent of China’s citizens are), or had been a serving participant in the intelligence establishment, it might seem inoffensive enough, although still a little surprising. To serious champions of liberty, the Tianamen Square protests, and subsequent government massacres, stand as a continuing charge against the Chinese state and Party. How does Yang deal with them (they disrupted his plans for graduate study abroad)? They are nothing more than “student demonstrations”.

He can safely be mildly critical of the Cultural Revolution – his parents were apparently sent to the countryside for “re-education” – but never mentions the dreadful evil of the Great Famine, one of the worst man-made (Chinese government made) disasters ever. There are boilerplate references to his support for opportunity and choice, but no attacks on the evil of the one-child policy, still in place at the time Yang gave his speech. Nothing about the lack of freedom of expression, the lack of freedom of religion, the lack of any free alternative to the Communist Party in China. Instead, we get paeans to the “success” of the Chinese government in “lifting millions of people out of poverty”, as if the same government hadn’t driven them unnecessarily further into poverty in the first place – and he has the gall to suggest that “reflecting on the way in which China has achieved its positive change and development gives me a firm belief that the policies of the National Party are in the best interests of New Zealand.” And for someone with an academic background in international relations and an expressed interest in contributing on foreign affairs matters in Parliament, nothing at all about Chinese expansionism in the South China Sea, or its advocacy internationally of alternative visions of governance antithetical to liberal democracy.

It is one thing to be proud of your ethnic background – and China has an ancient culture that once led the world – but Yang showed absolutely no sign of having turned his back on, or a desire to call out, the evils of a repressive authoritarian party and government that has never recanted its mistakes, that has failed economically (compare Taiwan and China for example) and which represents a threat to us, and to countries (and believers in freedom) throughout east Asia.

And it wasn’t just the maiden speech. As the Financial Times notes, since entering Parliament

He has consistently pushed for closer ties with Beijing and for international policies and positions echoing those of China’s Communist party.

In one of the FT articles on this story, there is photo of Yang posing with the Chinese defence attache at a celebration a year or two ago of the anniversary of the founding of the Chinese army. Perhaps a Minister of Foreign Affairs more or less has to attend such functions. Backbenchers don’t, and they certainly don’t need to be posing with military representatives of aggressive foreign governments, unless doing so speaks of their ongoing sympathies. There is simply no sign of Yang having recanted his active involvement in the Chinese intelligence establishment – indeed, until yesterday that inolvement was not generally known,

If, say, Russel Norman or Julie-Anne Genter (adult migrants who subsequently became NZ MPs) had been as actively involved in advancing Australian or US government causes (respectively) there would also have been considerable grounds for concern, mitigated to some extent by them not having been serving members in the intelligence regimes of the countries of their birth.

Who knows quite what the nature of Yang’s ongoing association with the Chinese authorities is. But as the FT report notes, China has been increasingly active in placing and cultivating people in Western democracies and helping them gradually reach positions of political influence, and it reports concrete areas of concern in Canada (including from the intelligence authorities) and Australia. Perhaps Yang doesn’t fit that bill at all, but if so his case would be a lot more convincing if he’d had a track record of being consistently and openly critical of the Chinese government and the Communist Party. Instead, as the FT notes, in an interview recently he repeatedly requested the journalists not to include information about his intelligence background in articles about him. You’d think it might have been an opportunity to openly criticise the authoritarian regime (being able to use the insider’s perspective he’d gained in his misguided youth) that he had turned his back on in choosing to come to New Zealand. But apparently not.

It really is a quite extraordinary story. On the one hand, quite remarkable that it has taken six years in Parliament for the media to look into the background of this MP – one has to wonder why these stories weren’t being written in 2011 when the National Party first put him on the list. Perhaps there would have been more scrutiny if he’d been attempting to become a constituency MP?

But more concerning is the seeming indifference of the National Party to Mr Yang’s background. He was/is (we are told) a very effective fundraiser for the National Party, and politics isn’t cheap. Once upon a time the National Party could be counted on for a fairly hardline on defence and security. But these days, if this story is illustrative, do they just no longer care, so long as they can maintain a cosy relationship with the Chinese establishment and host visits from Chinese leaders and Chinese warships? It is easy to downplay geopolitics when one is as physically remote as New Zealand. But the issues and threats to us, and to like-minded countries, are real nonetheless.

On a similar note, shouldn’t it be somewhat concerning that the largest donor to the National Party is an entity called the Inner Mongolian Rider Horse Industry (NZ) Ltd. I suppose we should be grateful the donation was made in a way that it was disclosed, but this is a company which has a small New Zealand operation, subsidiary of quite a large Chinese parent owned by a Chinese billionaire.

I have no way of knowing if the National Party is worse on such matters than the Labour Party would be (or for that matter, New Zealand First, which now has a prominent candidate Shane Jones of Bill Liu citizenship shame.) But Jian Yang is a member of the National Party, and the National Party has now led the government for nine years. For now, the hard questions seem to need to be asked of them. If they didn’t know Yang’s background before recruiting him, that was slipshod or deliberately indifferent, and if they did know but just didn’t care – and stuck him on the Foreign Affairs committee nonetheless – it risks looking like just another form of depraved indifference, whether through blindness to the threat China poses to things we (and people like us, from Taiwan, from Canada, from the UK or wherever) have held dear, or just a focus on keeping the donor money and votes flowing in.

I’m no New Zealand First fan, but the slogan on their campaign billboards “Had enough?” sums it up for me. After the housing disaster, the economic failures (and worse, the near lies about them), and episode after episode that speaks of the degradation of standards of public life in New Zealand, for me it is just another nail in the coffin. More nails than timber now.

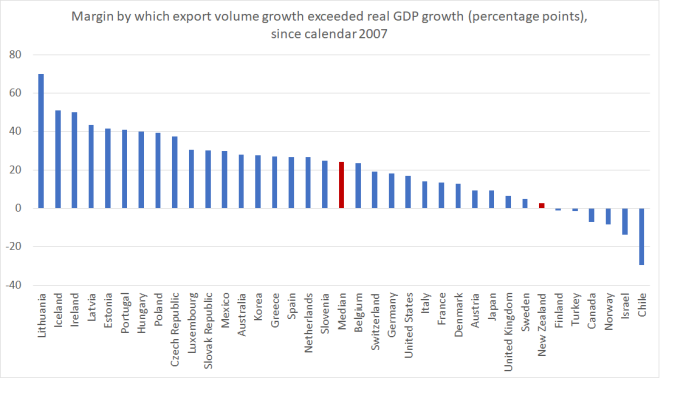

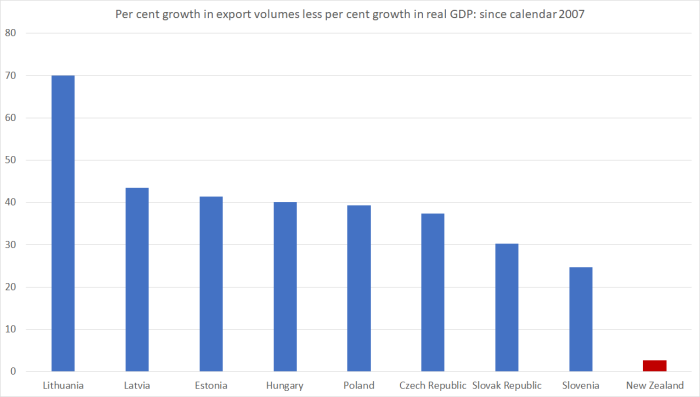

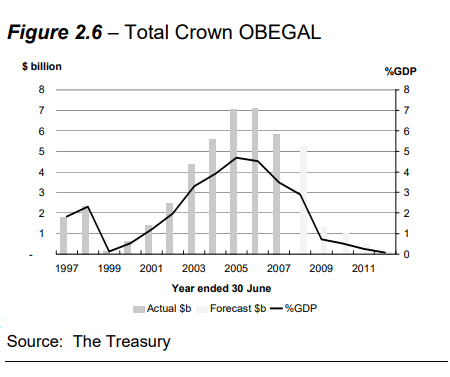

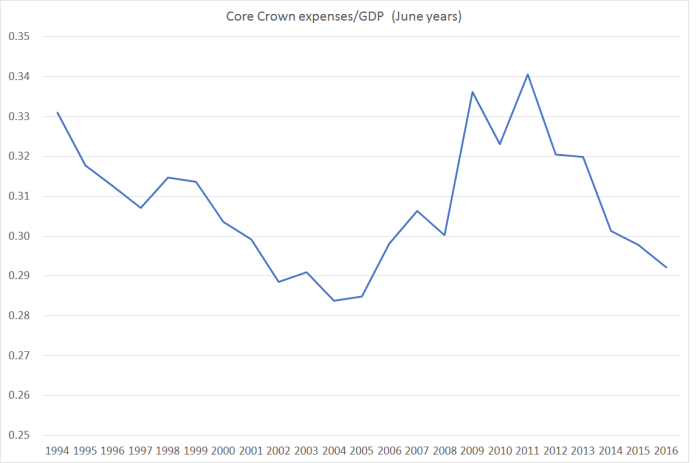

When net core Crown debt is already as low as 9.2 per cent of GDP – not on the measure Treasury, the government and Labour all prefer, but the simple straightforward metric – what is the economic case for material operating surpluses at all? With the output gap around zero and unemployment above the NAIRU, it is not as if the economy is overheating (the other usual case for running surpluses). Even just a balanced budget would slowly further lower the debt to GDP ratios. One could mount quite a reasonable argument for somewhat lower taxes (if you were a party of the right) or somewhat higher targeted spending (if you were a party of the left, campaigning on structural underfunding of various key government spending areas).

When net core Crown debt is already as low as 9.2 per cent of GDP – not on the measure Treasury, the government and Labour all prefer, but the simple straightforward metric – what is the economic case for material operating surpluses at all? With the output gap around zero and unemployment above the NAIRU, it is not as if the economy is overheating (the other usual case for running surpluses). Even just a balanced budget would slowly further lower the debt to GDP ratios. One could mount quite a reasonable argument for somewhat lower taxes (if you were a party of the right) or somewhat higher targeted spending (if you were a party of the left, campaigning on structural underfunding of various key government spending areas).