Almost 1300 years ago, the English missionary priest and bishop Saint Boniface confronted the belief of some pagan German villagers in Thor, god of (among other things) oak trees. Tree gods (or beliefs in them) were vanquished, and Boniface became known as the apostle to the Germans..

Pre-evangelisation, Maori had their own tree god, Tane Mahuta. As far as I can tell, not many believe any longer in this local tree god: when I looked up the 2013 Census data, there were lots of Maori recording no religion, and there were plenty of Catholics and Anglicans. But there wasn’t a category shown for tree gods, or any of the other deities (Wikipedia has a list of at least 35 of them).

But the Governor of the Reserve Bank seems intent on bringing them back.

Tomorrow will mark six months since Adrian Orr became the most powerful unelected person in New Zealand, as Governor of the Reserve Bank. Six months on we’ve had not a single serious and substantive speech on the policy areas he is responsible for, and where he exercises a huge amount of barely-trammelled power. No speech on monetary policy, no speech on banking regulation, and nothing either on the less prominent things the Governor is responsible for – such as, for example, insurance prudential supervision, a New Zealand insurer having failed, regulated by the Reserve Bank just before the Governor took office. He hasn’t substantively and openly engaged with, or responded to, the damning survey results on the Bank’s performance as a financial system regulator.

Instead, we’ve heard the Governor on almost everything else. There was infrastructure, climate change (repeatedly), the failings of capitalism, geopolitics, women in economics, and of course bank “conduct” (playing distraction from his institution’s own failings, by trying to butt into a field for which the Bank has no statutory responsibility). There have been lots of words, but not much sign of in-depth reflection or distinctive insights, and even less sign of doing him well, and being open about, the jobs Parliament has actually given the Bank. Throw in some considerable complacency about monetary policy and it should be a pretty disquieting picture.

Some of it is probably just the Governor’s well-known propensity to talk. Some of it might even be an understandable (if misguided in application) desire to lift the esprit-de-corps at the Reserve Bank after the demoralising Wheeler years. And a lot seems to be about winning the turf battles, ensuring that in the reviews of the Reserve Bank Act that the government has underway as much as possible of the Bank’s powers are kept, in effect, under the Governor’s control, and that the existing powers and functions of the Reserve Bank are all kept in the Reserve Bank. Part of that seems to be about openly subscribing what should be a non-partisan agency to every trendy left-wing cause that is going (and which, presumably, the Governor believes in personally.) A power play in other words – and, with a weak government that probably doesn’t care much, quite likely to succeed, somewhat to the detriment of New Zealand.

The latest example was the release on Monday of a rather curious 36 page document called The Journey of Te Putea Matua: our Tane Mahuta. Te Putea Matua is the Maori name the Reserve Bank of New Zealand has taken upon itself (such being the way these days with public sector agencies). It isn’t clear who “our” is in this context, although it seems the Governor – himself with no apparent Maori ancestry – wants us New Zealanders to identify with some Maori tree god that – data suggest – no one believes in, and to think of the Reserve Bank as akin to a localised tree god. Frankly, it seems weird. These days, most New Zealanders don’t claim allegiance to any deity, but of those of us who do most – Christian, Muslim, or Jewish, of European, Maori or any other ancestry – choose to worship a God with rather more all-encompassing claims.

But the Governor seems dead keen on championing Maori belief systems from centuries past. In an official document of our central bank we read

A core pillar of the evolving Māori belief system is a tale of the earth mother (Papatūānuku) and the sky father (Ranginui) who needed separating to allow the

sun to shine in. Tāne Mahuta – the god of the forest and birds – managed this task after some false starts and help from his family. The sunlight allowed life to flourish in Tāne Mahuta’s garden.

This quote appears twice in the document.

All very interesting perhaps in some cultural studies course, but what does it have to do with macroeconomic management or financial stability? Well, according to the Governor (in a radio interview on this yesterday) before there was a Reserve Bank “darkness was on our economy”. The Reserve Bank was the god of the forest, and let the sun shine in. Perhaps it is just my own culture, but the imagery that sprang to mind was that of people who walked in darkness having seen a great light. But imagine the uproar if a Governor had been using Judeo-Christian imagery in an official publication.

On the same page we read

Many of these birds feature on the NZ dollar money including the kereru, kaka, and kiwi – core to our belief system and survival.

I’m a bit lost again as to who “our” is here. I’m pretty sure I’m like most New Zealanders; I never saw a bird as “core” to my “belief system”. Perhaps the Governor does, although if so we might worry about the quality of his judgements in other areas.

As I say, it is an odd document. There are pages and pages that have nothing whatever to do with monetary policy or the financial system. Some of it is even quite interesting, but why are we spending scarce taxpayers’ money recounting stories of New Zealand general history? There is a page about the Maori navigators and, somewhat out of order, an earlier one about what early Maori ate and what the tribes traded among themselves. And there is a whole page about Kate Sheppard who, admirable as she was, has nothing whatever to do with New Zealand economic or financial history and policy. There is questionable history: simple matters of fact (eg Apirana Ngata wasn’t the first Maori Cabinet minister and didn’t first hold office in the 1920s – James Carroll, who held high office for a long period (twice as acting Prime Minister), preceded him), highly questionable and tendentious economic history, and overall a tone (perhaps comforting to today’s liberal political elite) that seems embarrassed by the European settlement of New Zealand. There is lots on the difficulties and injustices that some Maori faced, and little or nothing on the advantages that western institutions and society brought. Reasonable people might debate that balance, but it isn’t clear what the central bank – paid to do monetary policy and financial stability – is doing weighing in on the matter.

As I noted earlier, in a radio interview yesterday the Governor claimed that prior to the creation of the Reserve Bank ‘darkness was on our economy’, that the Reserve Bank had let the sunshine in, and that Australia and the UK had somehow turned their backs on us at the point the Bank was created. In fact, here it is – Reserve Bank as tree god – in the document itself.

The Reserve Bank became the Tāne Mahuta of New Zealand’s financial system, allowing the sun to shine in on the economy.

I think there was a plausible case for the creation of a central bank here, but to listen to or read the Governor you’d have no idea that New Zealand without a Reserve Bank had been among the handful of most prosperous countries in the world. Here from the publication, writing about the period before the Reserve Bank was created

The infrastructure funding was further hindered by the banks being foreign-owned (British and Australian) and issuing private currency. Credit growth in New Zealand was driven by the economic performance of these foreign economies, unrelated

to the demands of New Zealand. Subsequent recessions in Britain and Australia slowed lending in New Zealand when it was most needed.

Very little of this stands much scrutiny. You’d have no idea from reading that material that the New Zealand government had made heavy and persistent use of international capital markets, such that by 1929 it – like its Australian peers – had among the very highest public debt to GDP ratios (and NIIP ratios) ever recorded in an advanced country. You’d have no idea that New Zealand was among the most prosperous countries around (like Australia and the United States, neither of which had had central banks in the decades prior to World War One). You’d have no idea that the economic fortunes of New Zealand, trading heavily with the UK, might reasonably be expected to be affected by the economic fortunes of the UK – terms of trade and all that. Or that economic cycles in New Zealand and Australia were naturally quite highly correlated (common shocks and all that). And of course – with all the Governor’s talk about how we could “print our own money” – within five years of the creation of the Reserve Bank, itself after recovery from the Great Depression was well underway, that we’d not unrelatedly run into a foreign exchange crisis that led to the imposition of highly inefficient controls that plagued us (administered by the evil twin of the tree god?) for decades. Or even that persistent inflation dates from the creation of the Reserve Bank

One can’t cover everything in a glossy pamphlet, even one that seems to purport to be aimed at adults (including Reserve Bank staff according to the Governor), but there isn’t much excuse for this sort of misleading and one-dimensional argumentation, aka propaganda.

The propaganda face of the document becomes clearer in the second half. Among the issues the government’s review of the Reserve Bank Act is looking at is whether the prudential and regulatory functions of the Bank should be split out into a new standalone agency, a New Zealand Prudential Regulatory Authority. I think that, on balance, that would be a preferable model. It also happens to be the model adopted in much of the advanced world, including many/most small advanced economies. There are arguments to be made on both sides of the issue, but you wouldn’t know it from reading about the Governor’s vision of the Bank as a Maori tree god, where one and indivisible seems to be the watchword. Everything is about “synergies”, and nothing about weaknesses or risks, nothing about how other countries do things, nothing about the full range of criteria one might want to consider in devising, and holding to account, regulatory institutions for New Zealand.

I don’t have any problem with officials, including from affected agencies, offering careful balanced and rigorous advice on the pros and cons of structural separation. But that is a choice ultimately for ministers and for Parliament. And among the relevant considerations are issues of accountability and governance. Neither word appears in Governor’s propaganda piece. But then tree gods probably aren’t known for accountability. New Zealand government regulatory institutions should be. If ministers and Parliament decide to opt for structural separation, I wonder how the Governor will revise his document – his tree god having been split in two.

Among the tree god’s claims about financial regulation and what the Bank brings to bear was this breathtaking assertion, prominently displayed at the head of a page (p27).

The Reserve Bank is highly incentivised to ‘get it right’ when it comes to prudential regulation. We have a lot at risk

It is an extraordinary claim, that could be made only be someone wilfully blind – or choosing to ignore – decades of serious analysis of government failure, and the institutional incentives that face regulators, regulatory agencies, and their masters.

There is nothing on the rest of that page to back the tree god’s claim. On any reasonable and hardheaded analysis, the Reserve Bank has very weak incentives to “get it right”, or even to know – and be able to tell us – what “get it right” might mean. When banks fail, neither the Reserve Bank Governor nor any of the tree god’s staff have any money at stake (at least in their professional capacity, and as I recall things, Reserve Bank staff – rightly – aren’t allowed to own shares in banks). It is all but impossible to get rid of a Reserve Bank Governor, and it is even harder to get rid of staff (for bad policy or bad supervision). Most senior figures in central bank and regulatory agencies of countries that ran into financial crises 10 years ago, stayed on or in time moved on to comfortable, honoured (a peerage in Mervyn King’s case) retirements, or better-remunerated positions in the private sector.

And when the Reserve Bank uses its powers in ways that reduce the efficiency of the financial system, or stopping willing borrowers and willing lenders writing mortgage contracts, where are incentives on the Reserve Bank to “get things right”. There are no personal consequences – the Governor and his senior staff either won’t have, or would have no problem getting, mortgages. The previous Governor got to exercise the bee in his bonnet about housing crises, and to play politics, with no supporting analysis and no effective accountability. The current head of the tree god opines that lenders and borrowers can’t be trusted – but tree gods apparently can – but when challenged produced no analysis to support his claim. That sort of system creates incentives for sure, but they aren’t to “get it right”. Officials have incentives to keep things secret, and we saw that on full display with the Bank’s supervision of CBL Insurance last year – they might argue it was in the public interest, but even if so, it was clearly in their private interests, and against the interests of many members of the public.

Another word that hardly appears at all in the document is “transparency”. If you wanted to call yourself a tree god who sheds light upon the dark world that was pre-1933 New Zealand (or, presumably, a modern New Zealand without our current Reserve Bank) you might think there would be at least some self-awareness of the other side of letting the light in: letting in the light on the Bank’s own operation. As I’ve documented here over the years, the Bank is quite open about what it wants to be open about. But what credit to them is that, everyone releases what they want to release: the essence of transparency is readily and willingly releasing material that they might, in some senses, prefer to keep to themselves, to make for an easier life for the tree god. Our Reserve Bank – the Governor’s pagan tree god – is notoriously secretive and obstructive, consistently pushing to and beyond the limits of the Official Information Act. Only a few weeks ago the Ombudsman’s office had to intervene to remind them that simply invoking “Chatham House rules” doesn’t enable you to keep things secret. And with even the Cabinet having promised pro-active release of Cabinet papers, and pro-active release of Budget background papers and advice, the Reserve Bank looks not like a tree god shedding light in dark places, but like some more malevolent self-interested dark deity.

The Governor also tells us he has adopted an ever more ambitious goal than the previous Governor’s one. Graeme Wheeler articulated a vision of the Reserve Bank as “best small central bank” in the world. It was pretty empty. There was no sign that citizens or other stakeholders had asked him to be the “best small central bank” – richer countries than us will often choose to spend a lot more (and with less accountability) on their central bank. In any case, when challenged a few years later, it turned out that there was nothing going on to benchmark themselves against that ostensible aspiration. But Orr’s aspiration for his tree god is an unqualified “best central bank”. The institution is a very long way from that at present – and getting further away if Orr uses the Bank as a platform for pushing for his personal political agendas, well beyond the Bank’s statutory responsibility. It isn’t open, it isn’t excellent, it is accountable. It should do much better (although I’m still not convinced that a small poor advanced country should be expecting, ir aiming, ot have best central bank there is.)

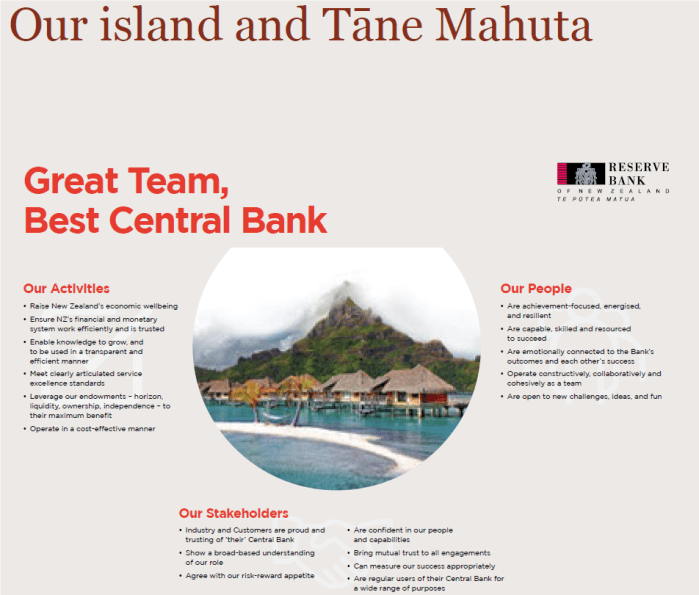

And finally, among the oddities of Orr’s apparent aspirations is something about an island. There is a full page under the heading “Our island and Tane Mahuta”, complete with lots of (mostly) worthy (if sometimes threatening, for staff ) aspirations, and this picture.

It appears to be the island where the imaginary tree god dwells. But, here’s the thing, it doesn’t look a bit like anywhere in New Zealand. And the Reserve Bank of New Zealand is supposed to be primarily about New Zealand and New Zealanders. Has the tree god flown the coop (so to speak) and fled to some poor Pacific Island where – perhaps – well paid senior central bankers take their winter holidays and commune with the deity? I’d prefer a central bank – even one deluded that it is a tree god – to think New Zealand, New Zealand people, New Zealand places.

Better still, ditch the pagan religion – not (according to the Census) taken seriously by Maori, and never part of the heritage or beliefs of most New Zealand – leave it to the cultural studies textbooks, and get on with doing your job, openly, accountably, excellently.

And, as part of that, abandon the complacency about monetary policy, expressed again by the Governor is his Radio NZ interview yesterday. The next serious recession is, according to him, nothing to worry about. Monetary policy faces no serious constraints. Which, presumably, is why all those other countries who did find themselves at the effective lower bound last time round were able to rebound so quickly and effectively, and deliver inflation consistently near target. Or perhaps that is only in a false tree god’s imaginary world?

UPDATE: I meant to include, but accidentally left out, reference to the fact that the Bank of New Zealand had been majority New Zealand government owned from 1894, forty years before the Reserve Bank was formed. Surely the Governor was aware of that?