It is six months today since Adrian Orr took office as Governor of the Reserve Bank, the latest (and last, given forthcoming legislative reforms) in a line of people who over the last 30 years have held office as the single most powerful unelected person in New Zealand (more powerful individually than most elected people).

When it comes to monetary policy, I’ve had no particular problem with the Governor’s bottom-lines. In fact, if he’d stuck to those, the contents of this blog in recent months would have been quite different.

Here was the bottom line in May (the Governor’s first OCR decision)

The Official Cash Rate (OCR) will remain at 1.75 percent for some time to come. The direction of our next move is equally balanced, up or down. Only time and events will tell.

in June

The Official Cash Rate (OCR) will remain at 1.75 percent for now. However, we are well positioned to manage change in either direction – up or down – as necessary.

in August

The Official Cash Rate (OCR) remains at 1.75 percent. We expect to keep the OCR at this level through 2019 and into 2020, longer than we projected in our May Statement. The direction of our next OCR move could be up or down.

and here is the Governor today

The Official Cash Rate (OCR) remains at 1.75 percent. We expect to keep the OCR at this level through 2019 and into 2020. The direction of our next OCR move could be up or down.

As one of the only (perhaps the only) commentators who has been consistently on record in thinking a lower OCR would have been a good idea, and who has argued that if there is a move in the next 12 months it will be a cut, I’ve welcomed the fact that – unlike most market economists – the Bank’s focus doesn’t appear to have been on when the next OCR increase happens. Too much focus in that direction misled both the Bank and the market economists for much of the last decade.

Thus far, well done Governor.

The bit in those “bottom line” statements that has left me a little uneasy is the apparently confident statements about the future: in March, the OCR would stay at 1.75 per cent “for some time to come”, and in the last two releases it has been even more specific about dates if less dogmatic in tone (“we expect to keep the OCR at this level through 2019 and into 2020”). But none of us knows the future. Macro forecasting is pretty futile more than perhaps a quarter or two ahead, and yet the Governor spends resources and puts his reputation somewhat on the line as if he were some sort of oracle, granted insight into the far – by monetary policy standards – far future. It is bizarre and unnecessary.

But perhaps equally surprising is the way the market economists play the game. Their commentaries are full of discussions around whether the next adjustment is more likely (say) 12 months out or 15 months out, as if they too are oracles, blessed with some particular insight. I suppose they have clients who want this sort of stuff, but you might think that at least some of the better clients would appreciate being told the truth: there is almost no chance of the OCR changing in the next three months, and beyond it is really anyone’s guess, almost inherently unknowable. Words like those in the Governor’s first statement: only time and events will tell. Crisp and honest.

And yet I’m conscious that much of my experience was in periods when interest rates moved round a great deal. And these days they seem not to.

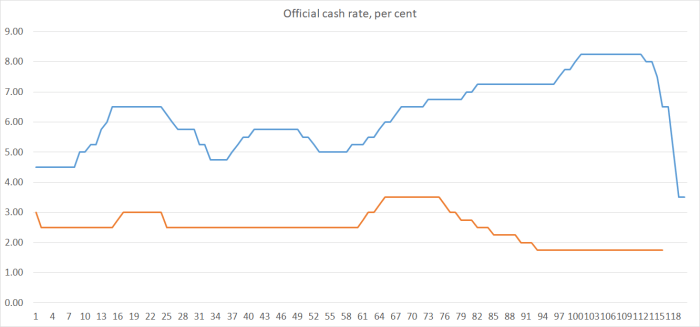

The OCR system itself is almost 20 years old. The first OCR was set in March 1999. In this chart, I’ve shown the first 10 years of data (to February 2009) and the subsequent 9.5 years to now.

In the first 10 years, the range from low to high was almost 500 basis points. In the rest of the 1990s, the amplitude of fluctuations in the 90 day bank bill rate was similarly large.

And the last 9.5 years? The total range within which the OCR has fluctuated is only 175 basis points, and it was only even that wide because of the msisguided enthusiasm for tightening in 2014.

That is quite a difference.

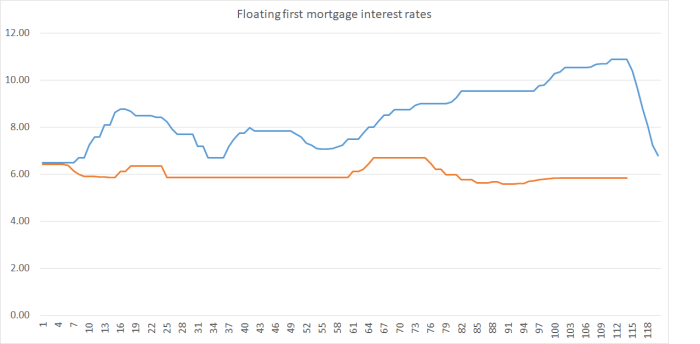

But the difference is even more stark if we look at retail interest rates. Here is the Reserve Bank’s floating first mortgage rate series for the same two periods.

Over the last 9.5 years, this mortgage interest rate has moved within a total range of only about 110 basis points.

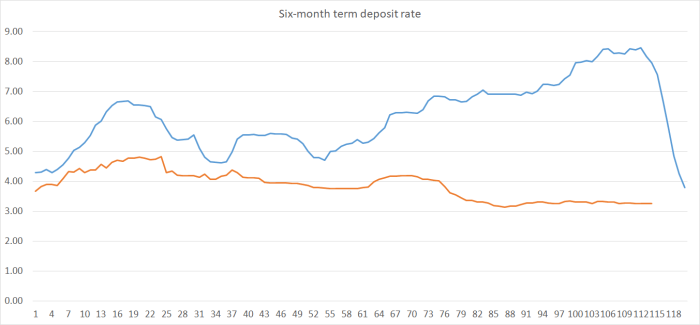

And here is the same chart for the Bank’s six-month term deposit rate series.

The range from high to low is about 170 basis points (similar to that for the OCR), but the peaks were a very long time ago now (back in 2010/11). For years now, term deposit rates (on this indicator) have fluctuated little, between just over 4 per cent and just over 3 per cent.

I don’t have a good hypothesis for why we have seen such a dramatic change in the variability of interest rates. It doesn’t surprise when one sees such patterns in countries that hit the effective lower bound on nominal interest rates – unable to cut further, inflation lingers low and there is little reason then to raise rates. But that isn’t the New Zealand story at all – the lowest the OCR has got is the current 1.75 per cent and everyone recognises it could be cut further if necessary.

Has the economy really got so much more stable than it was in the previous couple of decades? It seems unlikely, perhaps especially in New Zealand (with, for example, record swings in population, big earthquakes, and big terms of trade changes). Perhaps, to some extent, the Reserve Bank has simulated the sort of behaviour seen in the lower bound countries: always reluctant to cut (even though they always could have), inflation has stayed too low, and the economic upswings have, partly as a result, been pretty muted by historical standards and not very inflationary. I’m genuinely puzzled. Who knows, perhaps the Governor could offer the benefits of Bank research and analysis on this point whenever he finally gets round to deigning to give a substantive speech on his primary (according to the Act) responsibility, monetary policy?

Changing tack, in yesterday’s post I had a bit of fun taking the Governor to task over his attempt to articulate the story of the Reserve Bank as if it were some obscure mythical tree god, Tane Mahuta. Late in that post, I noted that they had adopted some imagery of an island, as what the Bank was working towards. In their own words

“We have visualised ‘our island’ that we are moving towards on the horizon, one that all New Zealanders can be proud of and that Tane Mahuta – our Bank – can stand tall on.”

And this was the page with the picture I showed.

I noted yesterday

It appears to be the island where the imaginary tree god dwells. But, here’s the thing, it doesn’t look a bit like anywhere in New Zealand. And the Reserve Bank of New Zealand is supposed to be primarily about New Zealand and New Zealanders. Has the tree god flown the coop (so to speak) and fled to some poor Pacific Island where – perhaps – well paid senior central bankers take their winter holidays and commune with the deity? I’d prefer a central bank – even one deluded that it is a tree god – to think New Zealand, New Zealand people, New Zealand places.

A diligent reader took the photo and did a little digging with the help of Mr Google. Turns out that the Governor’s island is Bora Bora, a very expensive resort location in French Polynesia. I guess it is the sort of place the Governor and his chums flit off too – although I’d been under the impression the Governor’s destination of preference was the Cook Islands – but the weird thing is that it is in a quite different country. Even more oddly, given his distaste for the colonial experience – suffusing his official document – it is a territory of an old European empire. Don’t we have any islands in New Zealand?

But we do, of course. The Governor can probably see Somes Island out his office window. I live in a suburb named for its island. And all of us live on these islands, the myriad of them that make up New Zealand.

I guess it was just a silly slip – though you wonder how no one picked it up – but it does seem all too consistent with the Governor’s style: once over lightly, and more focused on the issues he isn’t responsible for (recall not long ago he told us we were lucky as a country not to export fossil fuels) than on the narrow range of things he is responsible for. Perhaps he could put aside the tree god stuff and get back to (what a commenter this morning urged me to) the “dry old world of money”. There is more interesting and important stuff in the world, but “money” is the Governor’s job, and it needs to be done well, and in a way that commands respect.

And, finally, regular readers might recall a post from a month or so ago, in which a reader had passed on a report of the Governor’s address (off the record – and thus only the favoured few had access) to an INFINZ financial markets function in Wellington in late August. It was reported that the Governor has been typically loquacious, but offering up potentially quite highly market-sensitive information to his favoured audience.

Typically loquacious but, so the report suggests, perhaps going rather beyond the Bank’s public lines on monetary policy as articulated in the August Monetary Policy Statement, in a very dovish direction. And weighing in on what sort of person he wanted (and did not want – economists apparently not wanted) on the new Monetary Policy Committee – the one where the Minister supposedly makes the appointment, the one where the legislation has not yet been dealt with by the relevant select committee.

It seemed rather undisciplined and inappropriate, and I reminded readers again of the contrast with the Reserve Bank of Australia where speeches by the Governor and senior staff are typically on-the-record, usually with a published record of the subsequent Q&A session as well. The difference doesn’t matter much when off the record speeches are totally anodyne, and people answer questions in a similar unrevealing way, but that certainly isn’t Orr’s style.

On this occasion, so the report I received suggested, it wasn’t just monetary policy things the Governor was free and frank about. There was, for example, reportedly stuff about how if banks didn’t change their ways he’d change them for them, by setting up a Royal Commission here [something the government would surely not be keen on given their difficult relationship with the business community, and plethora of reviews/inquiries], and a totally dismissive approach to the recent failure – on the Bank’s watch – of CBL Insurance.

I put in an Official Information Act request to the Bank about this speech. I didn’t expect much – it seemed unlikely the Governor was working from a text, but (given his style) it was at least possible (it would be prudent more generally) there might have been a recording. There wasn’t apparently.

But I also asked for copies for briefing notes or emails related to the content of the speech. And there was some material there in the response I got back this morning. The full response will apparently be put on their website before long (now here). What was interesting was a request sent out on behalf of the Governor to several Bank staff who had been at the function inviting any feedback (the request was for anything, good or bad, but perhaps not surprisingly none of the staff offered anything sceptical or critical, to a Governor not known for welcoming challenge). In those comments we learn from one

My impression from the crowd was that they also enjoyed the speech and are really starting appreciate that having a longer-term vision and focus is important. I like that you gave the audience practical examples such as the United Nations Sustainable Development Goals, Carbon Disclosure Project, and Principles of Responsible Investing that they can start using/working toward now – they have no excuses for inaction!

The SDGs have nothing whatever to do with the Reserve Bank or its responsibilities.

And from another

For example, Adrian discussed climate change and short-term vs. long-term thinking.

Nor, of course, has climate change. Short-term vs long-term thinking is one of his hobbyhorses, but as I’ve noted previously the Bank has done nothing substantive on this claim.

It sounds as if the speech was all over the show, and mostly (as we’ve come to expect) not on the things he is paid to be responsible for. It is undisciplined and unfortunate, and won’t help wider confidence in him or the tree god (though those who like his leftist political analysis may, shortsightedly, welcome it). And none of it is transparent and open, more like a locker-room chat to his buddies in the financial sector. He tells us the economy sat in darkness before the advent of the Reserve Bank. Maybe, maybe not, but assuredly we all too often sit in darkness when it comes to the activities of the Bank itself. That simply shouldn’t be acceptable. Openness, and equal information for all, should be the watchwords of a modern accountable central bank and its Governor.

I’d like to tell Mr Orr that ‘darkness’ before the advent of the Reserve Bank and fiat money was called a free market with market price signals – way better than this command state asset bubble machine that runs over elderly and prudent savers so dairy can build speculatory shit ponds all through Canterbury at the expense of a bio-diverse rural economy.

You probably won’t agree, Michael 🙂

LikeLike

I half agree about the history Mark (as i noted in yesterday’s piece, NZ pre RB was both prosperous and not particularly prone to financial crises. That said, there is a rather important caveat to your story: from 1914 to 1934 our money was privately issued fiat money (not convertible into, or formally backed by, anything). It wasn’t a sustainable model, but it more or less worked over that period.

On my telling, without a Reserve Bank – here or abroad – term real interest rates would be around what they are now. They are a real phenomenon not a monetary one.

LikeLike

And negative interest rates at BOJ, ECB, etc? There’s nothing ‘real’ about that surely?

I disagree, respectfully, with your last paragraph. Dairy, esp, to the peril of many I think, viewed the last decade’s low-interest rate as essentially free money for conversions and I don’t think banks, given the low OCR, have been factoring ‘real’ risk into their lending to that and many other sectors. And risk is an important signal to interest rates.

But forget that; I’d be interested in your comment on central bank negative interest rates vis a vis ‘real interest rates’?

LikeLike

There is nothing to prevent negative nominal or real interest rates in a commodity-backed money context. Real interest rates reconcile savings and investment intentions and desires and if, for example, demographics are such that there is a high desired savings rate and a low need for investment on account of population growth (as in much of the world now), or weak productivity growth reduces business investment demand, there is nothing to stop rates going negative in a pure market system (they probably can’t go very negative for very long, because there are natural assets with positive yields – eg fruit trees – but something like minus 1 or 2 per cent for a decade wouldn’t be a problem). Central banks can drive short-term rates away from the real equilibrium factors, which is why it is useful to look at very long-term rates: a 10 or 20 year rate is usually telling you mostly about actual and expected long-term fundamentals.

LikeLike

One or two of us market economists picked that rates were not going up. Been very profitable for my clients to receive rates either outright or agains paid positions in the US.

😉

LikeLike

Yes fair comment, although my comment was only about those whose views were in the public domain.

And if I recall rightly, a year or so ago even you were briefly rattled about upside inflation risks weren’t you?!

LikeLike