That was the title of a ten page piece published last week by the ANZ economics team (chief economist Sharon Zollner and one of her offsiders, who appears to be a temporary secondee from the Reserve Bank). You can find a link to the paper here.

The gist is captured in the paper’s summary

I found the first line of that final bullet rather jarring – the balance of payments not having been any sort of policy focus for decades now (really since the shift to a floating exchange rate) in 1985.

But what really puzzled me about the note was how little macroeconomics there seemed to be in it, or behind it. It isn’t that there was no interesting material in it; in fact there were a variety of interesting charts on developments and issues in individual sub-sectors, and for anyone interested in these issues it is worth a read. But I thought I’d throw in a few macro perspectives.

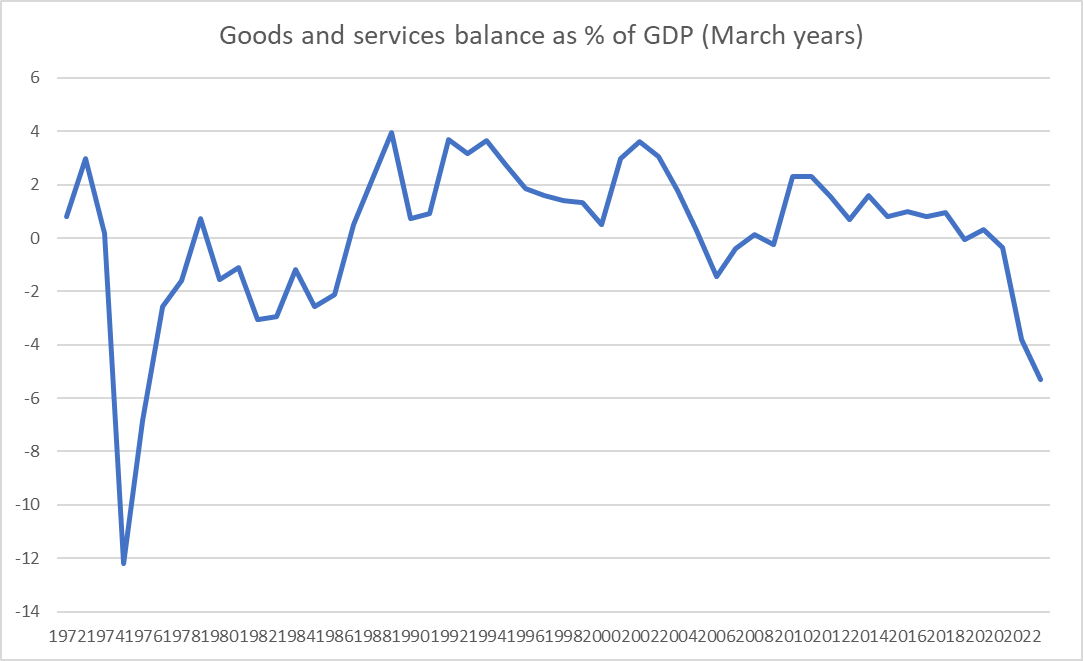

The paper starts with this chart

which is a rather different picture than the one (for the current account) we usually look at. The current deficit as a share of GDP got to about current levels in 2007, but looking just at the goods and services balance what we’ve seen in the last couple of years is without precedent for many decades. Here is the same chart with the longer run of annual data.

I’m not entirely sure why ANZ chose to focus on the good and services balance. It is akin to the primary balance in a fiscal context, which I argued here a few weeks ago it made sense to give more prominence than is often done in New Zealand for a number of reasons. If as a country you are running a goods and services balance (or surplus) it is unlikely that the NIIP position (as a share of GDP) is going to get away on you. (Of course, there isn’t anything necessarily wrong with a widening negative NIIP position – as so often, it depends what is causing the change.)

But one other positive feature of focusing on the good and services balance is that it helps to make clear that the recent sharp widening in the current account deficit – to one of the widest among OECD countries – is down to the spending choices of New Zealanders. The other big component of the current account is the income deficit (primarily in New Zealand, investment income – interest and profits). Interest rates have risen a lot in the last couple of years. But I’d have to confess I hadn’t really noticed that, thus far, the income deficit has not widened much at all as a share of GDP. If interest rates stay around current levels for long that will probably change.

So if it is spending choices that – compositionally – explain the sharp widening of the current account, where do we see that.

Well, the badly mis-forecast sharp increase in core inflation is one place. But step back a little further.

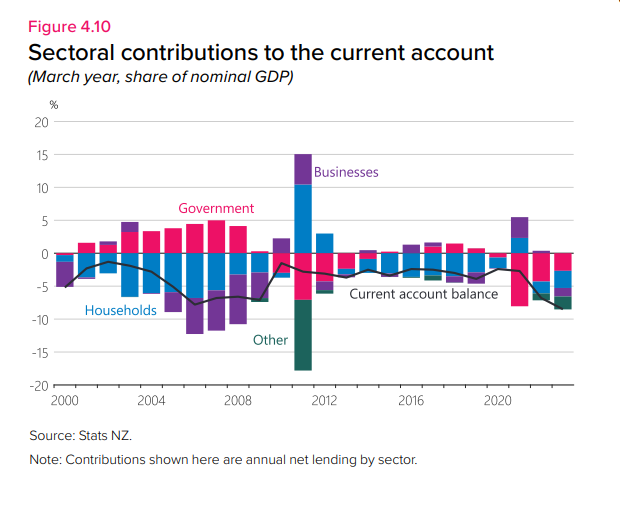

Here, from the IMF WEO database, are investment and (gross) national saving as a per cent of GDP, in annual terms included estimates for calendar 2023.

Another way of looking at the current account deficit is as the difference between saving and investment. And here you see that investment as a share of GDP last year and this has been at the highest we’ve experienced in decades (since the days of Think Big), and while the savings rate isn’t at any sort of record level it has been quite a bit lower than what we’d seen in New Zealand over half decade or so pre-Covid. Saving here is national savings – household, business, government – and we know that government dissaving – substantial operating deficits – has been a feature of the last few years, never more so than in 2022 and 2023 by when the economy was already running beyond capacity.

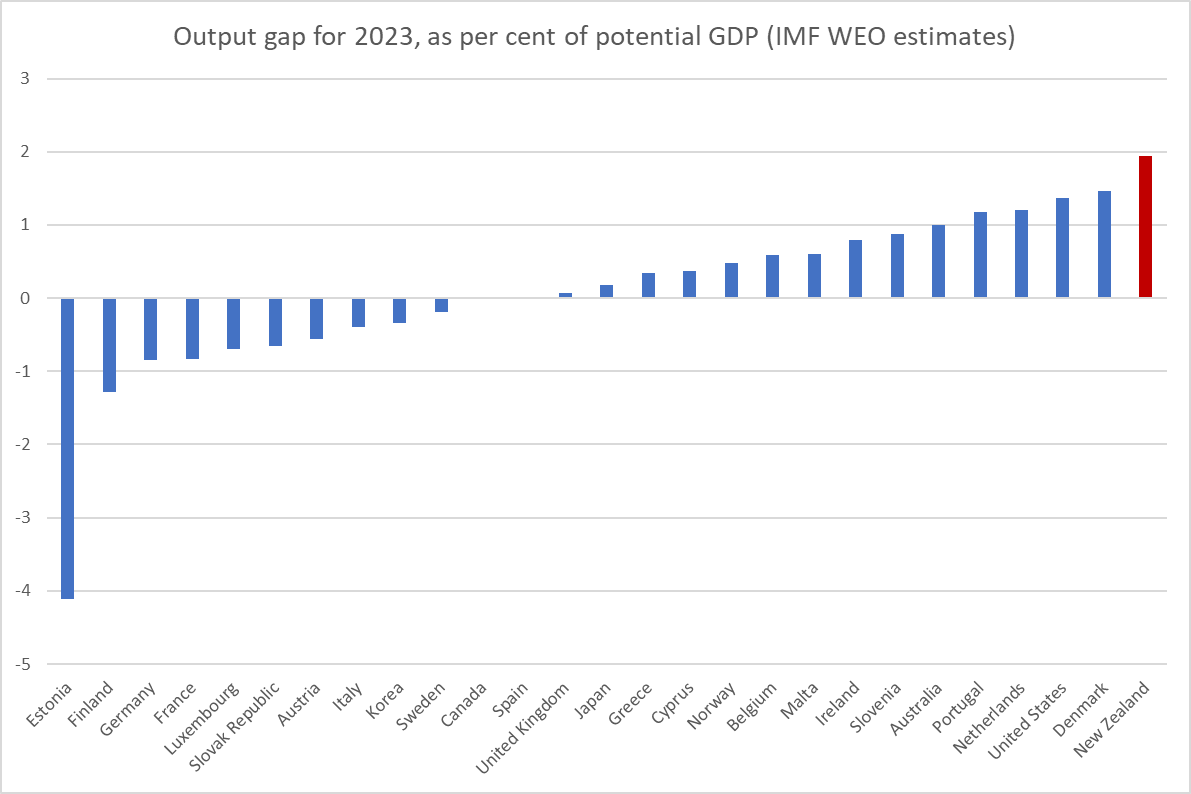

Beyond capacity? Well, we know the labour market has been stretched beyond sustainable (in the RB Governor’s own words) and both the Reserve Bank and Treasury have talked of positive output gaps.

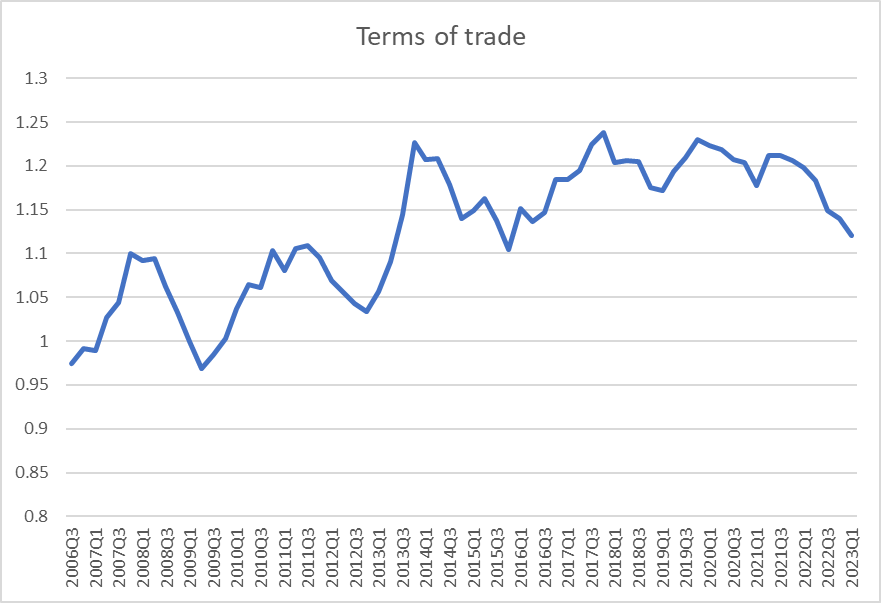

But absolute numbers for local output gaps don’t get much coverage or grab the imagination. But this chart is from the IMF’s World Economic Outlook a couple of weeks back. The good thing about the IMF numbers isn’t that they are right – few forecasters consistently are – but that they take a fair common approach across a whole bunch of countries. And on their reckoning even this year on average the New Zealand economy is seen as the most overheated – “overheated” means prone to larger than usual balance of payments deficits and higher than usual inflation – of any of the advanced countries they do such estimates for. And that without any surge upwards in the terms of trade of the sort we were enjoying when the economy was last this stretched – in output gap terms – in 2007.

And then here is another chart I’ve shown before to highlight just how unusual domestic demand has been here in recent years.

Domestic demand needed to increase to some extent to fill a void left by the slump in net exports (most notably net services exports) if the economy was to remain fairly-fully employed, but policy (mostly monetary policy, which takes fiscal policy as given) was set so badly that we’ve ended up with astonishing levels of domestic spending, and with it……high core inflation, and a really marked widening in the balance of payments current account and goods and services deficits.

But, and here’s the thing, we still do not need specific balance of payments. Not from government, and not even from you and me thinking we’d best do our bit for the nation. Rather, as the government (eventually) gets the deficit back down again, and as the Reserve Bank eventually does its job, we can expect these imbalances largely to sort themselves out, and certainly not to end up posing severe risks to anything much. And if perhaps Chinese tourism exports never fully recover, we can expect private domestic spending to adjust, as it tends to when (for example) the terms of trade fall and people find themselves less well off than they had thought.

Of course, we shouldn’t rule out an exchange rate adjustment at some point, but we’ve come to forget how common they used to be in New Zealand – common, without being highly disruptive or prompting higher interest rates again. For a couple of decades at the RB we used to spend huge amounts of time trying to make sense of some of the biggest real exchange rate swings in the advanced world…..and then they just stopped (the reasons for that aren’t, I think, well understood or even extensively studied).

The ANZ paper ends with this line

The bottom line is, ‘something’s gotta give’, as the saying goes. We can either be the collective architects of that change or we can wait for changes to be imposed on us by foreign creditors and financial markets.

That seems overwrought, but we should expect our macro policymakers to do their jobs rather better than they have in the last 3 years or so. But perhaps it isn’t the done thing for market economists to call out policymakers too vocally?

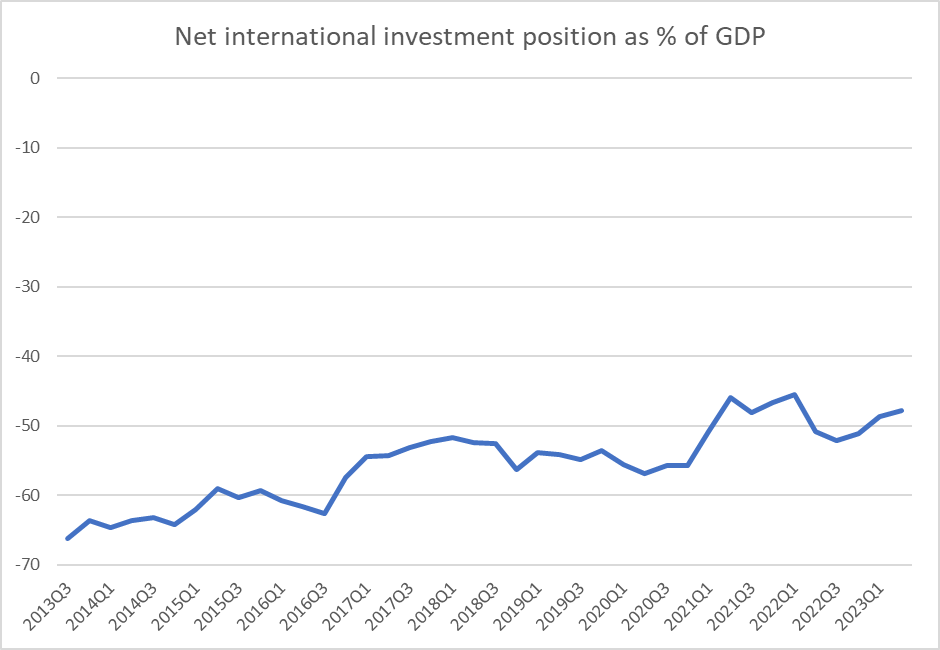

UPDATE: Oh, forgot to include this chart, which does put the last couple of years’ external imbalances in some perspective.

The rest of the world’s net claims on New Zealand residents have, if anything, shrunk a little further as a share of a GDP over the Covid years. It seems unlikely the creditors will be dunning “us” any time soon……which is not to say that if our interest rates end up lowish relative to the rest of the world there might not be some fall in the exchange rate.

On Saturday dozens of candidates for the governing Labour Party stood for election to Parliament. The aim was to form (at least a big part of) the next government. They didn’t succeed. People will debate for decades precisely what motivated the public as a whole to vote as we did, but having governed for the last three years, they (Labour) lost. It is perhaps the key feature of our democratic system, perhaps especially in New Zealand with so few other checks and balances. You (and your party) wield great power, and if we the public aren’t satisfied – think you’ve done poorly, think another lot might be better, or simply wake up grumpy on election day – you are out. It is your (and your party’s) job to convince us to give you another go. If you don’t convince us you are out (and typically when a party loses power a satisfying number of individuals – even if rarely Cabinet ministers – actually lose their job (as MP) altogether). And if you are a disappointed Labour voter this morning, the beauty of the system is that no doubt your turn will come again. It is accountability – sometimes crude, rough and ready, perhaps even (by some standards) unfair or wrong – but the threat and risk is real, and the job holders keep it constantly in mind.

Many other people in the public employ also wield considerable amounts of power. In some cases, that power is quite tightly constrained and often (for example) there are appeal authorities. If a benefit clerk denies you a benefit you are clearly legally entitled to you will probably end up getting it, and if the clerk’s mistake is severe or repeated often enough they might lose their job. Less so at more exalted levels. When, for example, the wrong person is put in prison for decades typically no one responsible pays a price. When the Public Service Commissioner engages in repeated blatant attempts to mislead to protect one of his own, it seems that no pays a price.

And then there are central banks.

Every few months I do a book review for the house journal of central bankers, Central Banking magazine. They are often fairly obscure books that I otherwise wouldn’t come across or wouldn’t spend my own money on (at academic publishing prices). A few months back I reviewed Inflation Targeting and Central Banks: Institutional Set-ups and Monetary Policy Effectiveness (hardback yours from Amazon at a mere US$170 – yes, there is a cheaper paperback if anyone is really interested), by a mid-career economist at the Polish central bank, in turn based on her fairly recent PhD thesis. The focus isn’t on the question of what difference inflation targeting makes but on what institutional details, which differ across inflation-targeting central banks, seem to make a difference. Sadly for the author – these things happen – her thesis was finished before the outbreak of inflation in much of the advanced world in the last 2-3 years.

At the core of the book is a set of painstakingly-compiled indexes on various aspects of inflation-targeting central banks which might be thought to be relevant to how those central banks might perform in managing inflation. There are ones for independence, ones for transparency, and so on, but the one that stuck with me months on was the one for accountability. Accountability used to be thought of as an absolutely critical element – the quid pro quo – for the operational independence that so many countries have given to central banks in the last few decades. With great power goes great responsibility, and ideas like that. The Reserve Bank itself was very fond on that sort of rhetoric. In fact, there used to be a substantive article on that topic by me on their website, in which I waxed eloquent on the topic (after it was toned down when my original version upset the Bank’s then Board by suggesting that for all the importance of accountability it was more difficult in practice than in theory). At a more casual level my favourite example has always been a radio interview then-Governor Don Brash did in 2003, the transcript of which the Bank chose to publish, in which there is a snippet that runs as follows:

Brash: ….we were concerned……we were running risk of inflation coming in above 2 per cent which is the top of our target

Interviewer: And then you’d lose your job?

Brash: Exactly right.

I was working overseas at the time, and can only assume my colleagues gulped when they saw it put so unequivocally. But it wasn’t inconsistent with a meeting the handful of senior monetary policy advisers had with Don in one of his first days in office. He eyed us up – chief economist, deputy chief economist, and manager responsible for monetary policy advice – and said (words to the effect of) “you know we are going to introduce a new law in which if inflation is away from target I can lose my job. Just be sure to realise gentlemen that if I go, you are going too.” Not ever taken – at least by me – as a threat, but as a simple statement of the then-prevalent idea (crucial in the public sector reforms being done at the time) that operational independence and authority went hand in hand with serious personal responsibility and potential personal consequences. It was part of the logic of having a single decision-maker system (an element of the New Zealand system that no one chose to follow and – in one of Labour’s better reforms in recent years – was finally replaced here_.

But that was then.

By contrast, these are the components of the Accountability sub-index in the recent book I mentioned

There is nothing very idiosyncratic about the book or the work in it; indeed, she seeks to be guided by the literature and current conventional understanding. And if you look down that list of items – which is the sort of stuff central bankers often now seem to have in mind when they ever mention “accountability – you’ll quickly realise that there is really a heavy emphasis on transparency (a good thing in itself of course) and almost none of them on any sort of accountability that involves real consequences for individuals, anyone paying any sort of price. The only one of these items that represents anything like that sort of accountability is item 6.7 but even there the provision is about whether Governors/MPC members can be dismissed for neglecting their work (not turning up to meetings etc), not for actual performance in the job.

But if there are no personal consequences for failure and inadequate performance, why would we hand over all this power? I’ve written here before about former Bank of England Deputy Governor Paul Tucker’s book Unelected Power – which ranges much wider than just central banks – where his first criterion for whether a function should be delegated to people voters can’t themselves toss out (eg central bankers) is whether the goal – what is expecting from the delegatees – can be sufficiently specified that we know whether outcomes are in line with what was sought. If there is no such clear advance specification either there will be no effective accountability or such accountability will at best be rather arbitrary.

As it happens, almost no one believes the over-simplified accountability expressed in that 1993 Brash quote above makes sense, even if expressed in core inflation terms (I don’t think most people involved really did even in 1993 – although there was a brief period of hubris where it all seemed surprisingly easy – and certainly as soon as inflation went above the target range in 1995 there was some hasty rearticulation of that sense).

But if we have handed over all this power – and central bank monetary policy decisions, good ones and bad, have huge ramifications for the economy as a whole and for many individuals – we should be able to point to behaviours or outcomes that would result in dismissal, non-reappointment, or other serious sanctions. Or otherwise in practical terms central banker inhabit a gilded sphere of huge power and no effective responsibility at all. And central banks aren’t like a Supreme Court, where we look at judges to be non-corrupt (including conflicts of interest) and able……but the desired products are about process – judging without fear or favour – not about particular outcomes, or decisions in a particular direction. It is right that it should be hard to remove a Supreme Court judge. It is less clear it should be so for central bank Governors, MPC members etc. The jobs are at times difficult to do excellently, but no one is forced to take the job, with its associated pay, power, prestige and post-office opportunities.

The problem – power has been handed over, but with no commensurate real accountability – isn’t just a New Zealand phenomenon, but one evident across the entire advanced world (the ECB at the most extreme, an institution existing by international treaty rather than domestic statute).

When I wrote my review I noted that “it isn’t clear that any central bank policymaker has paid any price at all for the recent stark departures of core inflation from target. It tends not to be that way for corporate CEOs or their senior managers when things go wrong in their bailiwicks.” It is possible there is now one exception to that story – the decision by the Australian government not to reappoint Phil Lowe on the completion of his seven year term – but even there it isn’t clear how much is about specific policy failures and how much about a more general discontents with the organisation and a desire for a modernised etc RBA structure, and the desire for a fresh face atop it. The promotion of a senior insider – not known to have sharply dissented from what policy mistakes there were – is at least a clue.

It increasingly looks to me as though delegation of discretionary monetary policy to central bankers should be rethought. I have long been fairly ambivalent but when the system is faced with its biggest test in decades – in all the years globally of delegating operational independence – central banks fail (the only possible to read recent core inflation outcomes relative to the targets given them) and no one pays a price (with just possibly a solo Australian exception) it begins to look as though we should leave the decisions with those whom we can toss out – Grant Robertson’s fate on Saturday – and keep central banks on as researchers, expert advisers, and as implementation agencies, but not themselves being unaccountable wielders of great powers.

The outgoing New Zealand government has made numerous bad economic choices in the last couple of years. Prominent among them were the decisions to reappoint MPC members, to allow the appointment to the MPC of someone with no relevant professional background or expertise, to reappoint the chair of the RB Board (while surrounding him with a bunch of non-entities, none of whom had any relevant expertise) and (above all on this front) the decision to reappoint the Governor. The latter decision was most especially egregious because it was Robertson himself who had amended the law to require parliamentary parties to be consulted before a Governor was (re)appointed, and when the two main Opposition parties both objected, Robertson went ahead anyway. If the operational independence of a Governor, appointed to a term not aligned with parliamentary terms, means anything, it surely should at least mean that the person appointed commands respect – for their capability, integrity etc – across political party lines. By simply ignoring dissent – that his own reforms formally invited – Robertson made Orr’s reappointment a purely opportunistic partisan call. At the time – 11 months ago – I outlined a list of 22 reasons Orr should not have been reappointed (and at that I wasn’t convinced simply missing the inflation target was one)

I’ll come back – probably tomorrow – to a post on what I think the incoming government and its Minister of Finance (presumably Willis) should do about Orr and the Reserve Bank now.

But this rest of this post is to illustrate that not even the rituals Parliament forces them to go through – in this case the production of an Annual Report – amount to any sort of accountability at all. (One day. perhaps next year now, they will have to front up on it to the new FEC, but sadly select committee scrutiny – committees being seriously under-resourced – is hit and miss at best, the more so in this case if Grant Robertson is the key Opposition figure on the new FEC reviewing the performance of the man he appointed and reappointed.)

It is difficult to know where to start on the Annual Report that was released last week.

It might be quite useful if you care about the Bank’s emissions, as there is several pages of material, but you shouldn’t (since we have an ETS for that). It is almost utterly useless for anything much that the Bank is responsible for. There are administrative things like why the Bank has 22 senior managers earning more than $300000 a year, or why it has 36 people shown in the senior management group (in a total of 510 FTE), or why staff numbers have risen sharply yet again, or why – having signed up to a very generous five year funding agreement in 2020 – they were coming cap in hand for lots more funding (much of which they got) this year. Or why the part-time chair of the Board – who has a fulltime job running a university, and where many of the key powers are statutorily delegated to the MPC – is pulling in $170000 a year; this the same chair who has been shown to have actively misrepresented – and led Treasury to make false statements about – the past ban on expertise on the MPC (issues he has never addressed). Or why the Governor gets away with actively misleading FEC. Or how seriously (or not) conflicts of interest are taken (even how the Board sees itself relative to the recent lofty words in the RB/FMA review of financial institutions’ governance).

But on policy matters it is arguably even worse. In a year when core inflation has – again – been miles away from the Bank’s target, the Board chair’s statement is reduced to 1.5 emollient pages uttering no concerns at all (recall that the Board does not do monetary policy, but it is charged by statute with reviewing monetary policy and the MPC and making recommendations on appointments of MPC members and the Governor). We learn nothing at all from the highly-paid chair as to why he and his Board of unqualified non-entities considered, in the circumstances, that reappointments had been warranted (nothing in Board minutes has provided anything more).

We do however learn of the Board’s effort to indulge the political whims of the Governor and Board members, the Treaty of Waitangi (a) not being mentioned in the acts supposedly governing the Bank, and b) not itself mentioning anything even remotely connected to monetary policy or financial stability.

There is a couple of page section on monetary policy in the body of the report. But in itself this is a reminder that the MPC – which wields the power – publishes no Annual Report, and exposes itself to no serious scrutiny. In this central bank not only does the deputy chief executive responsible for economics and monetary policy never give a serious speech on the subject, she is never seriously exposed to either media or parliamentary scrutiny. External members are so sheltered we have on idea what any of them think, what contribution they make, and so on. They never front FEC or any serious media. Perhaps it isn’t surprising that the total remuneration of these three ornamental figures isn’t much more than what the chair of the Board himself is paid.

But then surely the Board would be doing a rigorous review (it is after all the Board’s job, by law)? That would be difficult when most of the Board has no relevant expertise (the Governor is the main exception, and he chairs the MPC….).

But what we actually get in no sign of any serious thought, challenge or questioning, no attempt to frame the MPC’s achievements and failings. Instead we get this process-heavy but substantively-empty little box

It might be interesting to OIA that “self-review” MPC members are said to have carried out, but you’d just have no idea from any of this that the biggest monetary policy failure in decades had happened on the MPC members’ watch – even as all expiring terms were renewed. It is Potemkin-like “accountability”, with barely even that level of pretence. (Note here that the weak internal review last year wasn’t even an MPC document but rather a management one.)

If that is all rather weak it gets worse when the LSAP comes into view. This, you will recall, was the bondbuying programme in which the MPC’s choices cost taxpayers now just over $12 billion, a simply staggering sum of money, swamping all those “fiscal holes” of the recent election campaign. There are lot of LSAP references – it is the Annual Accounts after all – but none from the Board chair, and here is the one substantive bit.

I’ve highlighted the utterly egregious bit. As they say, IMF staff did put out a little modelling exercise. but it has no credibility whatever, as the scenario described in the exercise bore no relationship to what actually happened in the New Zealand economy in 2020 and 2021. It was a scenario under which, even with the LSAP, the New Zealand economy languished underemployed for three years (but a bit less so because of LSAP) rather than an overheated economy with very high inflation and – in the Governor’s own words – employment running above maximum sustainable employment. I critiqued the piece in a post here, and I know of no economists who read the IMF piece and concluded “ah yes, of course, notwithstanding that the LSAP had a direct loss of $12bn, in fact the taxpayer was really made better off by that intervention after all”. I’m sure no serious economist at the Reserve Bank – there still are some – believes it either. But there seems to be a premium on keeping quiet, and keeping your head down, in the Orr central bank. It was dishonest when the Governor first ran this line in an interview with the Herald but perhaps then he’d seen no critiques (or asked for one); it is materially worse when the Board chair (and the Governor’s 35 senior colleagues) let him get away with it and repeat it, without any scrutiny or further attempt to make a case, in what is supposed to be a powerful public institution’s premier accountability document.

Any serious accountability for the Bank seemed to be dead, at least under the outgoing government. Whether it will be any less bad under the new government it is far too soon to tell. But if it isn’t, serious questions needed to be asked about whether the model is any longer fit for purpose in the sort of democracy New Zealanders typically aspire to have – we’ll delegate power, but if you take up that power and stuff things up then you should personally pay some price. In this document not only in there is serious scrutiny, no personal consequences, but not even a glimpse of contrition from any of them. Never mind the huge losses, never mind the arbitrary deeply disruptive inflation, never mind the lies……after all, the government hasn’t seemed to mind.

Almost any private sector CEO, committee or Board that had stuffed up as badly as the Reserve Bank – with corporate excess and loss of focus thrown in – would have been sent packing some time ago. The stock price would have been falling, investors demanding change, and the business press all over the situation. But not here, not our central bank………

It is the time of the cycle when plenty of groups are keen to have their policy ideas and prescriptions be heard. After all, parties may still be finalising policies and there seems to be a reasonable chance of a new government and different set of ministers before long.

Many are just self-interested (no doubt the authors mostly believe there might be wider benefits, but the fact remains that they are championing policies to help their firm/industry/sector). As an example I found a link in my email this morning to one called a “Blueprint for Growth”. It was this from the covering press release that made me rashly open the handful of slides:

“Today’s announcement is just the beginning, as we know that good, evidence-based, bipartisan policy leads to better outcomes for all New Zealanders. This is part of the key to unlocking the future prosperity and productivity in New Zealand.

Instead it was a bunch of suggestions from the Financial Services Council, some probably worthy, others purely self-interested, that were primarily going to be good for member firms of the Financial Services Council and which, whatever their merits, were going to do nothing at all for productivity,

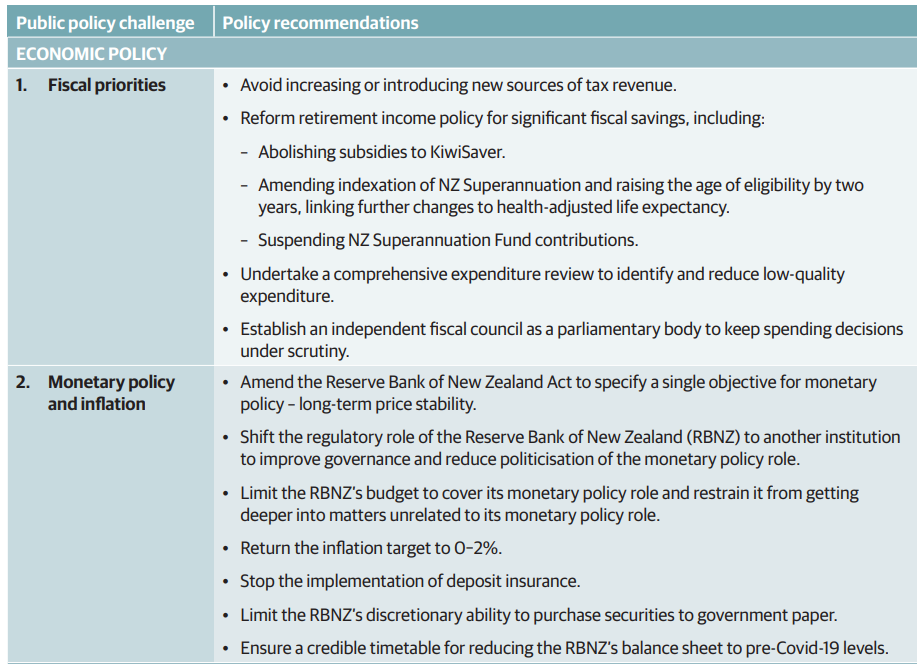

Yesterday the New Zealand Initiative released a rather more substantive effort, an 86 page collection of proposals and recommendations across a wide range of areas of government policy (nothing on foreign policy for example, and no references to China at all, except perhaps by allusion when discussing the proposed foreign investment regulatory regime, and no mention at all of company tax). (I wrote about their Manifesto 2017here.)

In some parts of the left, the New Zealand Initiative is looked on as some sort of lobby group for big business, and anything they say is, accordingly, to be dismissed without further examination. The Initiative would sometimes have you believe that it was the opposite: simply public-spirited disinterested people, focused only the well-being of all New Zealanders, who put up their money (in some cases, although mostly their shareholders’ money) only to produce research and analysis without fear, favour, or predisposition. The truth is probably in the middle, but it really shouldn’t matter because the Initiative is transparent about (a) who their members are, (b) their staff and the views of those staff, and (c) their analysis and research. Their stuff should be taken on its merits, and critically scrutinised in the same way as any other contributions to debates. Topics chosen will presumably reflect, to some extent, members’ interests (in both senses of that word) but that is a different matter than what is said on those topics.

I probably agreed with half the proposals in the latest Prescription. I often find myself agreeing with them on second order issues, while profoundly disagreeing with them on the diagnosis and prescription for New Zealand’s long-running productivity failure. But it is a fairly serious collection of ideas and I was a bit surprised not to have seen any media coverage.

In this post I wanted to comment only on their fiscal and monetary policy recommendations, summarised here (and discussed in a bit more depth on page 20-22 of the PDF.

Take fiscal first.

While I generally agree with the first recommendation (no new or higher taxes) – since there is plenty of room to close the (large) deficit by cutting out low-value spending over several years – some of the arguments adduced in support don’t stand much scrutiny. Take, for example, this paragraph

It is certainly true that Singapore and Taiwan have markedly lower rates of tax to GDP than New Zealand (or other advanced countries). On the other hand, OECD data for taxes and social security contributions as a share of GDP show that these days both Japan and Korea have about the same or higher tax shares than New Zealand does. Switzerland, Australia and the US are certainly lower than New Zealand, but then Canada is higher. And “Europe aside” does tend to rather overlook the fact that most of the world’s advanced economies are in Europe. (The Ireland line was fairly disreputable, it being well-understood that Ireland’s GDP numbers are seriously distorted by international tax factors. Using as a denominator the one the Irish authorities recommend (modified GNI), Ireland’s tax share is much the same as New Zealand’s).

I largely agree with their proposals around retirement income, and was surprised to realise that Kiwisaver subsidies now cost about $1 billion per annum. The text suggests that they envisage a pretty slow increase in the age of NZS eligibility, which does fit with what National is promising but should not be necessary in a first-best set of recommendations. Lift the age of eligibility by one quarter a year and it would be at 67 in eight years’ time.

There is quite a difference between suspending contributions to the New Zealand Superannuation Fund (the headline recommendation) and the alternative they moot in the fuller text of simply winding up the Fund. Do the former and Labour is likely to simply resume contributions again. There is no natural place for the government taking your money and mine (or, worse, borrowing it) to punt in international markets at our risk. The NZSF was initially designed for two things: to keep Michael Cullen’s colleagues’ spending sticky fingers off his early large surpluses, and to help buttress an NZS age of 65. We’ve not now had regular surpluses for a long time, and there is no good reason – with improvements in life expectancy – why the eligibility age for the universal state pension should be the same now as it was set at, for the then means-tested age pension, in 1898. NZSF should be wound up and the government’s gross debt substantially reduced.

The third bullet – comprehensive expenditure review – is fine, even admirable. But specifics, and willingness to actually cut, will matter. I like the idea of getting rid of interest-free student loans (my kids look at me reproachfully) but…..what hope?

I have long favoured a (small) Fiscal Council, or perhaps a slightly wider Macroeconomic Policy Council. This is a quite different thing than the policy costings office National, Labour and the Greens are all keen on (as a public subsidy to political parties). That said, if one were serious about austerity in the next term of government – and for my money the NZI doesn’t give sufficient weight to the scale of the fiscal challenge – I’m not sure I’d be treating new nice-to-have agencies (even very small ones) as any sort of priority. I’d rather focus on replacing the Secretary to the Treasury (whose term is up next year) and revitalising the analytical and advisory capabilities of The Treasury.

What of the monetary policy and Reserve Bank proposals. In several places, they overlap with ideas I’ve pushed here over the years.

I was in favour of something like the change to the statutory monetary policy mandate to the Reserve Bank, and am actually on record (in my submission to FEC in 2018) as having favoured going further. The change to the way the mandate was expressed was never envisaged as materially altering how monetary policy was run (from Robertson’s perspective it mostly seemed to be political product differentiation), and I don’t think there is any evidence it has actually done so. The Reserve Bank has made big mistakes in recent years but they have been analytical and forecasting mistakes, not things that can be sheeted home to the change in the way the mandate was expressed (here I imagine the Governor and I would be at one, although of course he’d be reluctant to get anywhere near the world “mistake”). All that said, since making the change made no substantive difference and was mostly about product differentiation, so would undoing it. We need real change at the Bank (and in how it is held to account) so I won’t argue strongly about symbolic change, a least if it markets/headlines real underlying change.

On the other hand, I have long favoured splitting up the Bank, and leaving a monetary policy and broader macro stability focused central bank, and then a New Zealand Prudential Regulatory Agency (probably comprising the regulatory functions of the Bank and much of the FMA’s responsibilities). That such a model would parallel the Australian system is not a conclusive argument on its own, but it is a real benefit when the biggest banking and insurance players in New Zealand are Australian-based. The Initiative argues that

Separating the functions into two organisations would improve governance and reduce the risk of political interference in the RBNZ’s core mission of price stability.

I agree (strongly) with the former. The current (reformed) Reserve Bank has a dogs’-breakfast of a governance model. I’m (much) less persuaded by the latter argument. I have seen no sign – in my time at the Bank or in recent years – of political interference in the operation of monetary policy. The mistakes have been Orr’s, and if there are valid criticisms of Robertson they are that he has showed little interest in doing anything about holding the Bank (and its key personnel) to account. Monetary policy and financial institution regulation are just two quite different functions, and need different skill-sets in CEOs. It isn’t impossible to make the current combined model work – though it would need big changes, including some legislative overhaul – but it simply isn’t the best model for New Zealand. (Such a reform would, done the right way, also render the Governor’s position redundant, with two new chief executive positions to fill.)

Should the Bank’s budget be cut? Yes, of course (and that comprehensive spending review shouldn’t overlook opportunities there), and since the NZI document was finalised we’ve seen an egregious increase in approved Bank spending without even the courtesy (or statutory obligation) to provide any documentation in support. But the budget is only one lever. As important will be finding expert people to lead the institution and monetary policy function who are really only interested, in their day job, in thinking about macroeconomics and doing and communicating monetary policy excellently, without fear, favour, or suspicion of either partisan allegiance or using a public role for private ideological purposes.

I have written here previously that I favour returning the inflation target to 0 to 2 per cent. That said, I don’t find the Initiative’s reasoning very persuasive

A lower target range would encourage the RBNZ to pursue more prudent monetary policies, minimising the risk of excessive inflation and promoting sustainable economic growth.

But there is no evidence for these claims. Adrian Orr and his minions would have made more or less exactly the same forecasting mistakes in recent years with a target centred on 1 per cent as with the actual target centred on 2 per cent.

Perhaps more importantly, I don’t think the New Zealand Initiative team has ever taken sufficiently seriously the current (regulatorily-induced) effective lower bound on nominal interest rates. That constraint can and should be fixed but unless it is fixed it would be irresponsible to recommend lowering the inflation target.

On deposit insurance, I have long favoured deposit insurance, as a second-best way of reducing the scale and risk of government bailouts of banks (if no one is protected a failing big bank will almost certainly be bailed out, whereas with (retail) deposit insurance it is more credible to think that wholesale funders might be allowed to lose their money in a failure. That said, my argument was primarily about the big banks, and the deposit insurance regime will not cover only them. I do worry about heightened moral hazard risks around the small institutions. One could, I suppose, argue that capital ratios are now high enough there is very little risk of a large bank failing, to a point where it is credible that depositors could face material losses, but that argument cuts both ways in that with high capital ratios moral hazard risks are much smaller even in the present of deposit insurance.

The second to last item on the monetary policy list is a curious one. The Reserve Bank has run up losses of about $11 billion dollars through an LSAP conducted almost entirely in government bonds. So while I agree with limiting what NZ assets the Bank can buy, I don’t think it gets near the heart of the issue. New Zealand legislation is generally for too lax in allowing huge risks to be assumed with no parliamentary approval (whether the Minister of Finance issuing guarantees, for which there is no limit, or the Reserve Bank – which cannot default on its debts – buying risky assets. While there is a need for some crisis flexibility, the scale of the intervention undertaken (over more than a year) should not again be possible without parliamentary approval. That, incidentally, does not impair monetary policy operational autonomy both because the LSAP is a very weak (just risky) instrument and because (see above) the effective lower bound on the nominal OCR itself can and should be fixed.

I have no particular problem with something like the final item on the list, but as regards the LSAP expansion it would seem to be already there. The Bank’s holdings of government bonds are being slowly but steadily sold back to The Treasury (and others are maturing in RB hands). One can argue that the mix of sales might have been different or that the pace should have been (much) faster, but the domestic monetary policy bit of the balance sheet will shrink a lot. There are debates to be had about how much of an “abundant reserves” approach is taken in future – I’d probably favour not – and there are issues that should have had more scrutiny around increases in foreign reserves that the Minister has approved this year, but they are probably second order in nature.

With only 86 pages and lots of policy areas to get through, the NZI document was never going to cover all the significant issues in any subject area. I have quite a list of others, both as regards fiscal policy and around monetary and financial regulatory policy, but this post was about engaging the debate on the ideas NZI has proposed, not tackling all the ones they didn’t or didn’t have space for. Overall, I’m mostly sympathetic to the direction they suggest, but any incoming government actually interested in change should subject the specifics to some serious critical scrutiny.

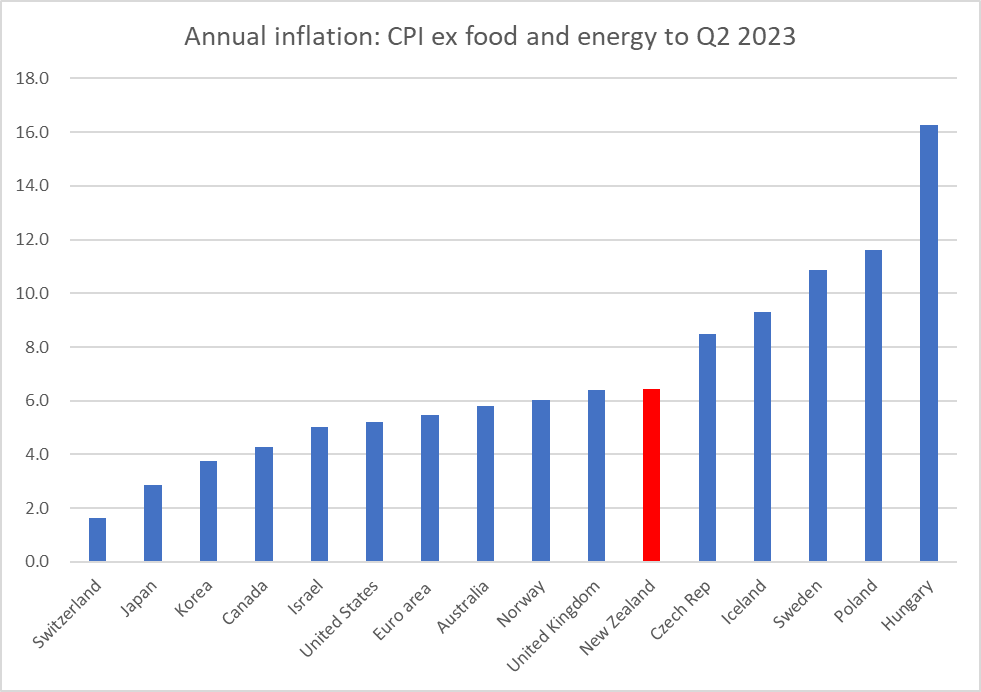

I’ve used this chart before to illustrate how diverse the (core) inflation experiences of advanced economies have been in this episode. It isn’t as if they’ve all ended up with similarly bad inflation rates, and the point of focusing on those countries with their own monetary policy and a floating exchange rate is that core inflation outcomes are a result of domestic (central bank) choices (passive or active) in each country.

Yesterday’s post focused on the rapid growth in domestic demand that the Reserve Bank had facilitated and overseen. But, it might have occurred to you to ask, what about foreign demand? It all adds up.

And if you look more broadly you might reasonably have thought New Zealand would be a good candidate for being towards the left-hand end of this chart.

The central banks in Australia, Canada, and Norway have faced big increases in the respective national terms of trade (export prices relative to import prices) over the last 3+ years. All else equal, a rising terms of trade – especially when, as in each of these cases, led by rising export prices – tends to increase domestic incomes and domestic consumption and investment spending and inflation. It isn’t mechanical or one for one (in Norway, for example, they have the oil fund into which state oil and gas revenues are sterilised) but the direction is clear: a rising terms of trade is a “good thing” and more spending, and pressure on real resources, will typically follow in its wake.

Here is the contrast between New Zealand and Australia over recent years.

In Australia a 25 per cent lift in the terms of trade is roughly equal to a 5 per cent lift in real purchasing power (over and above what is captured in real GDP). A 10 per cent fall here would be a roughly equivalent to a 2.5 per cent drop in real purchasing power. As it happens, over the last couple of years (since the tightening phases began) the terms of trade have been weaker than the Reserve Bank expected, all else equal a moderate deflationary surprise.

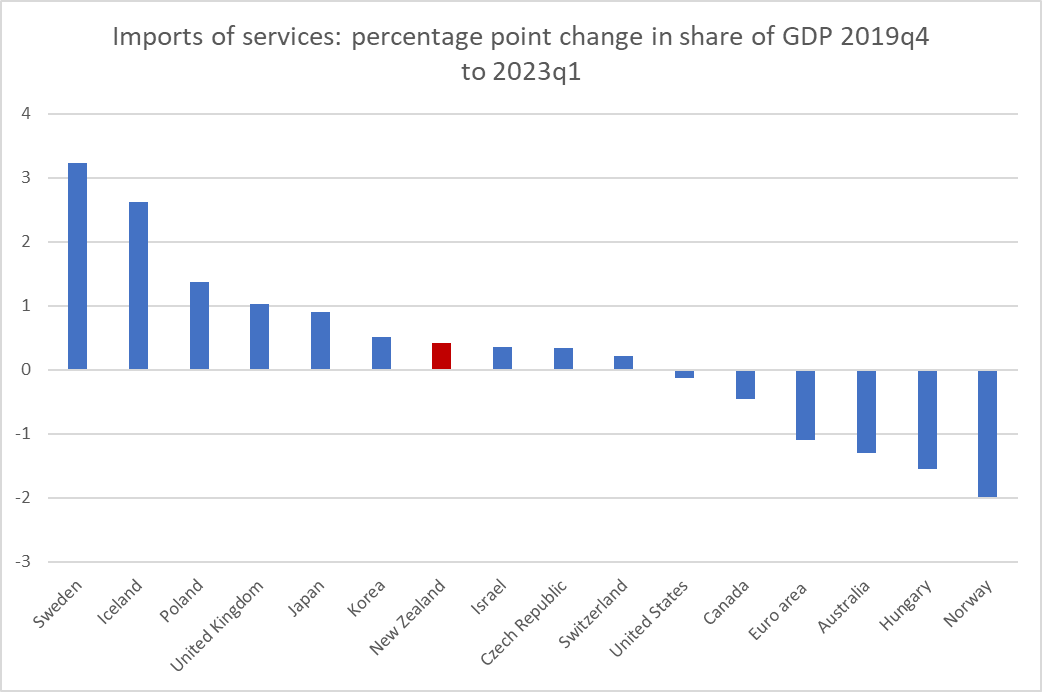

But the other big deflationary influence was the closed borders. I’m not here getting into debates about the merits of otherwise of such policies. Central banks simply have to take whatever else governments (and the private sector) do as given and adjust monetary policy accordingly to keep (core) inflation near target. The fact was that our borders were largely closed to human traffic for a long time, New Zealand has more exports of such services (tourism and export education) than imports, and exports of services are far from having fully recovered pre-Covid levels.

We don’t have easily comparable tourism and export education data across countries, but we can look at how exports of services changed as a share of GDP. From just prior to Covid to the trough, New Zealand exports of services fell by 5.7 percentage points of GDP, a shock exceeded only by Iceland (-12.7 percentage points) – the fall for Australia was just under half New Zealand’s, and for most advanced economies (of the sample in the chart above) the fall was 1-2 percentage points of GDP. In most countries, that trough was in mid 2020, while in New Zealand it was not until early 2022.

Some ground has been recovered (most starkly in Iceland) but New Zealand (and to a lesser extent Australia) are still living with a material deflationary shock from this side of the economy. Real services exports in 2023Q1 were 26 per cent (seasonally adjusted) lower than in 2019Q4, just prior to Covid.

Now, again you will note that this isn’t the entire story. After all, New Zealanders couldn’t travel abroad easily for much of the time either, and money they would have spent abroad seemed to be substantially diverted to spending at home (probably more so than was initially expected). That reduction of imports of services was large (3 percentage points of GDP, with Australia 4th largest of this advanced country grouping) but early – the trough for New Zealand as for most of these advanced countries was as early as 2020Q3.

But that was then. This chart shows the change in imports of services as a share of GDP from just pre-Covid to our most recent data (2023Q1). That share has fully recovered here, with an increase very similar to that of the median country.

So, relative to pre-Covid (and pre-inflation surge), imports of services as a share of GDP are about where they were, and exports of services were still materially lower as at the last official data.

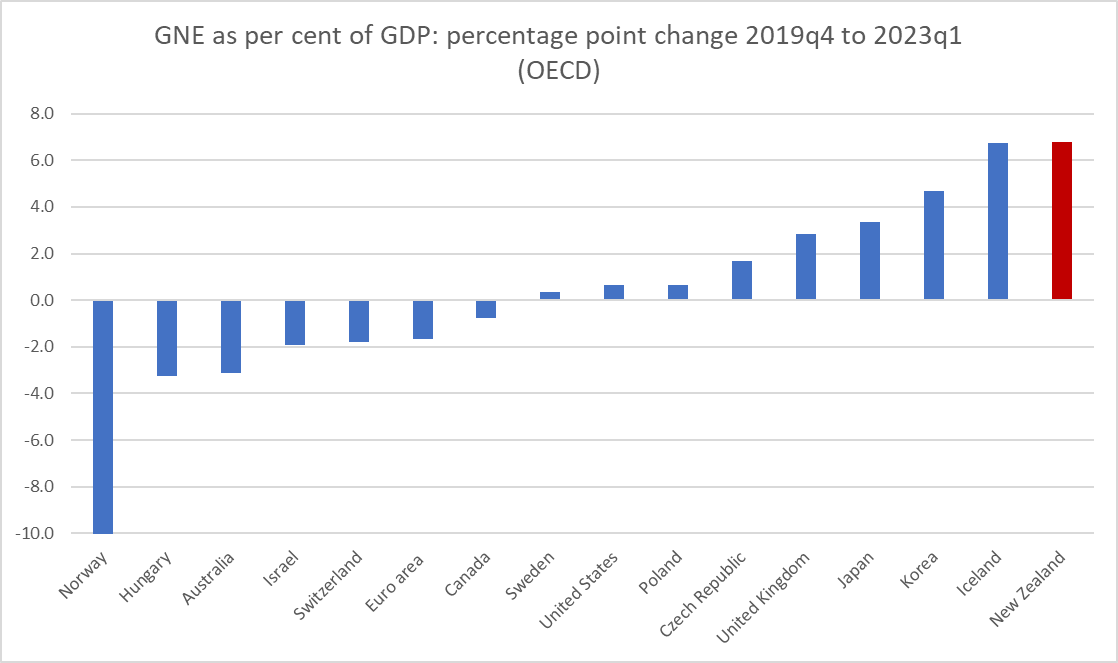

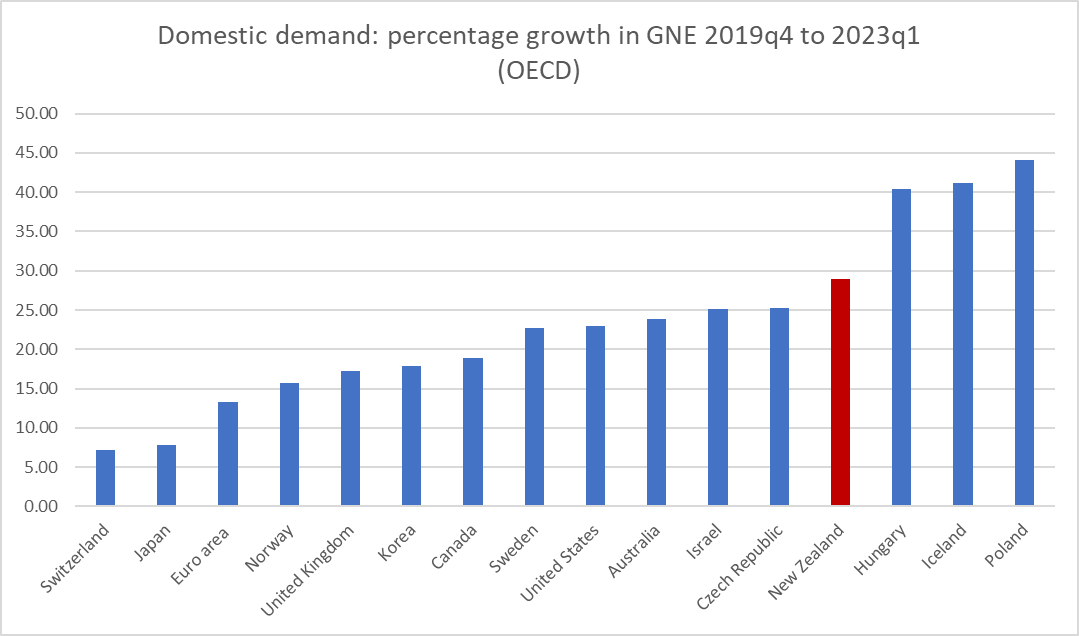

With a deflationary shock like this you might have reasonably thought that the Reserve Bank, if it was to keep inflation near target, would need to induce or ensure faster growth in domestic demand (than some other countries). Yesterday I showed this chart (remember, GNE is national accounts speak for domestic demand). New Zealand was at the far right side of the chart (strongest growth in domestic demand as a share of GDP).

But what if we treated the change in the services exports share of GDP as an exogenous shock that, all else equal, the central bank legitimately had to respond to? In this version of the chart I’ve subtracted the reduction in services exports as a share of GDP.

It makes a material difference to the New Zealand numbers, but even so we are still left with an increase in the share of GDP that is third highest on the chart, about the same as the UK which (as is well known) is really struggling with inflation. (In case you are wondering Korea has relatively modest core inflation now – so first chart – but still about 3.5 percentage points higher than it was just prior to Covid; for us the increase has been about 4 percentage points.)

There are lots of numbers and concepts in this post and it isn’t always easy to keep them straight. But the key points are probably:

echoing yesterday’s post, don’t be distracted by the Governor’s spin about Russia or the weather or whatever (they just don’t explain core inflation to any material extent) or spin (probably more from the Minister) that every advanced country is in the same boat (they aren’t, see first chart),

more than other advanced countries, we should have been predisposed to being able to have kept inflation in check a bit more easily, having had both a fall in the terms of trade (very much unlike Australia and Canada) and a sustained fall in exports of services that as a share of GDP is materially larger than any other advanced economy has seen. To be clear, those are bad things, making us poorer, but all else equal they were disinflationary forces,

and yet, core inflation here is in the upper half of the group of advanced economies and (as the MPS acknowledged) is not yet really showing signs of having fallen (unlike some other advanced countries, notably Australia, the US, and Canada),

the difference is about Reserve Bank choices and forecasting errors. The Reserve Bank can’t control the terms of trade or exports of services, but its tool – the OCR – is primarily about influencing domestic demand. They ended up producing some of the strongest growth in domestic demand (absolutely or relative to nominal GDP) anywhere in the advanced world. It wasn’t intentional, but it was their job, and their mistake resulted in high core inflation.

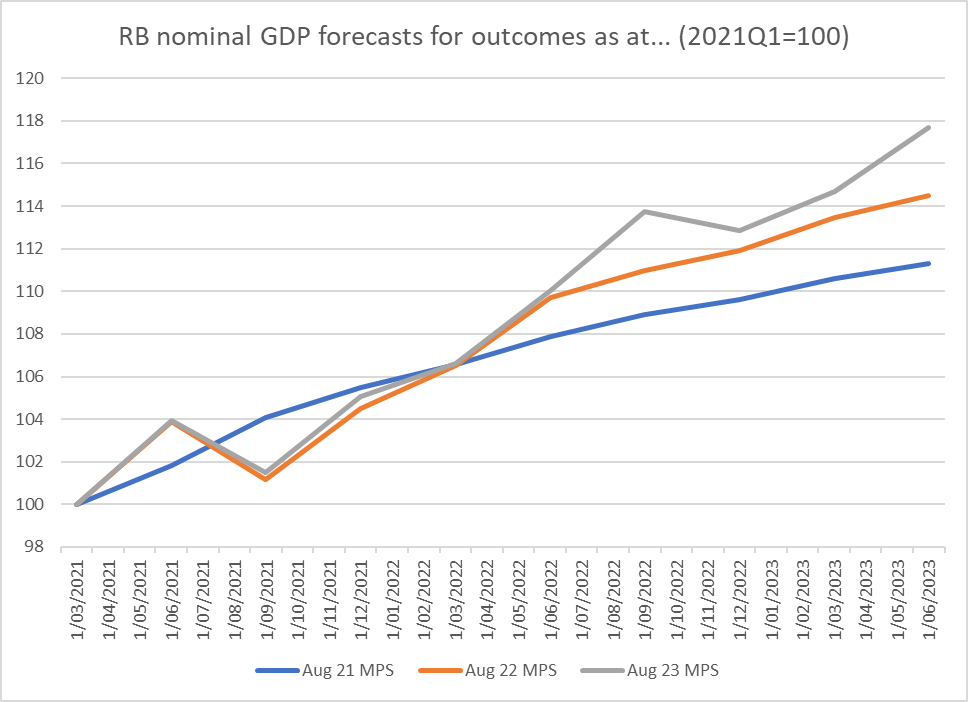

The Reserve Bank doesn’t publish forecasts of nominal GNE – and note that my charts have shown a big increase in GNE relative to GDP – but even their nominal GDP forecasts, even just starting from two years ago when they first thought it was time to start tightening, have materially understated domestic demand growth

and over this period they have actually over forecast real GDP growth.

Again, I’m going to end on a slightly emollient note. Macroeconomic forecasting is hard, and especially in times as unsettled as these. I heard an RB senior person the other day noting (fairly) that they couldn’t tell when the borders would fully reopen, or how quickly people flows would respond when they did. Personally, I’m less inclined to criticise them for getting their forecasts wrong (“let him who is without sin cast the first stone”) than for the sheer lack of honesty and straightforwardness, and the absence of either contrition (in respect of failures in a job they individually chose to accept – no one is compelled to be an MPC member) or hard critical comparative analysis. But…..relative to other countries they had advantages which should have given us a better chance of keeping inflation near target, and things ended up as bad or worse as in the median advanced country.

If forced to confront these arguments the Governor would no doubt burble on about “least regrets”. But the least regrets rhetoric a couple of years ago was really about – and they know this – the risk that inflation might, if things went a bit haywire, end up at 2.5 per cent or so for a year or two, rather than settling immediately around the target midpoint of 2 per cent. It wasn’t – was never even suggested as being – about the risk of two or three years of 6 per cent core inflation, and a wrenching adjustment to get it back under control.

They may still claim to have no regrets. They should have many. We certainly should. They took the job, did it poorly, and now won’t even openly accept (what they know internally) that it wasn’t the evil Russian or a cyclone or….or….or…it was them, Orr and the MPC. They made mistakes (they happen in life), with no apparent consequences for them, and not even the decency to front up, acknowledge the errors, and say sorry.

Particularly when he is let loose from the constraints of a published text, the Reserve Bank Governor (never openly countered by any of the other six MPC members, each of whom has personal responsibilities as a statutory appointee) likes to make up stuff suggesting that high inflation isn’t really the Reserve Bank’s fault, or responsibility, at all. It may be that Parliament’s Finance and Expenditure Committee is where he is particularly prone to this vice – deliberately misleading Parliament in the process, itself once regarded by MPs as a serious issue – or, more probably, it is just that those are the occasions we are given a glimpse of the Governor let loose.

I’ve written here about just a couple of the more egregious examples I happened to catch. Late last year there was the line he tried to run to FEC that for inflation to have been in the target range then (Nov 2022) the Bank would have to have been able to have forecast the Russian invasion of Ukraine in 2020. It took about five minutes to dig out the data (illustrated in the post at that link) to illustrate that core inflation was already at about 6 per cent BEFORE the invasion began on 24 February last year, or that the unemployment rate had already reached its decades-long low just prior to the invasion too. It was just made up, but of course there were no real consequences for the Governor.

And then there was last week’s effort in which Orr, apparently backed by his Chief Economist (who in addition to working for the Governor is a statutory officeholder with personal responsibilities), attempted to brush off the inflation as just one supply shock after the other, things the Bank couldn’t do much about, culminating in the outrageous attempt to mislead the Committee to believe that this year’s cyclone explained the big recent inflation forecasting error (only to have one of his staff pipe up and clarify that actually that effect was really rather small). See posts here and here. Consistent with this, in his interview late last week with the Herald‘s Madison Reidy, Orr again repeated his standard line that he has no regrets at all about the conduct of monetary policy in recent years. It is consistent I suppose: why regret what you could not control?

It is, of course, all nonsense.

But there is, you see, the good Orr and the bad Orr. The bad – really really bad, because so shamelessly dishonest – is on the display in the sorts of episodes I’ve mentioned in the previous two paragraphs.

The good Orr – some of you will doubt you are reading correctly, but you are – is a perfectly orthodox central banker informed by an entirely orthodox approach to inflation targeting. You see it, even at FEC, when for example he is asked about the role the “maximum sustainable employment” bit of the Remit plays. He has repeated, over and over again and quite correctly as far I can see, that there has not been any conflict between it and the inflation target in recent years. That is how demand shocks and pressures work. And whereas in 2020 the Bank thought inflation would undershoot target and unemployment be well above sustainable levels, in the last couple of years the picture has reversed. He told FEC again last week that when inflation was above target and the labour market was tighter than sustainable both pointed in the same direction for monetary policy: it needed to be restrictive. There was, for example, this very nice line in the MPS, which I put big ticks next to in my hard copy.

The Bank doesn’t do many speeches on monetary policy, and those few they do aren’t very insightful but this from the Chief Economist a few months ago captured the real story nicely

and this from the Governor, describing the Bank’s functions, was him at his entirely orthodox

We aim to slow (or accelerate) domestic spending and investment if it is outpacing (or falling behind) the supply capacity of the economy

Demand management, to keep (core) inflation at or near target is the heart of the Reserve Bank’s monetary policy job, assigned to it by Parliament and made specific in the Remit given to them by the Minister of Finance.

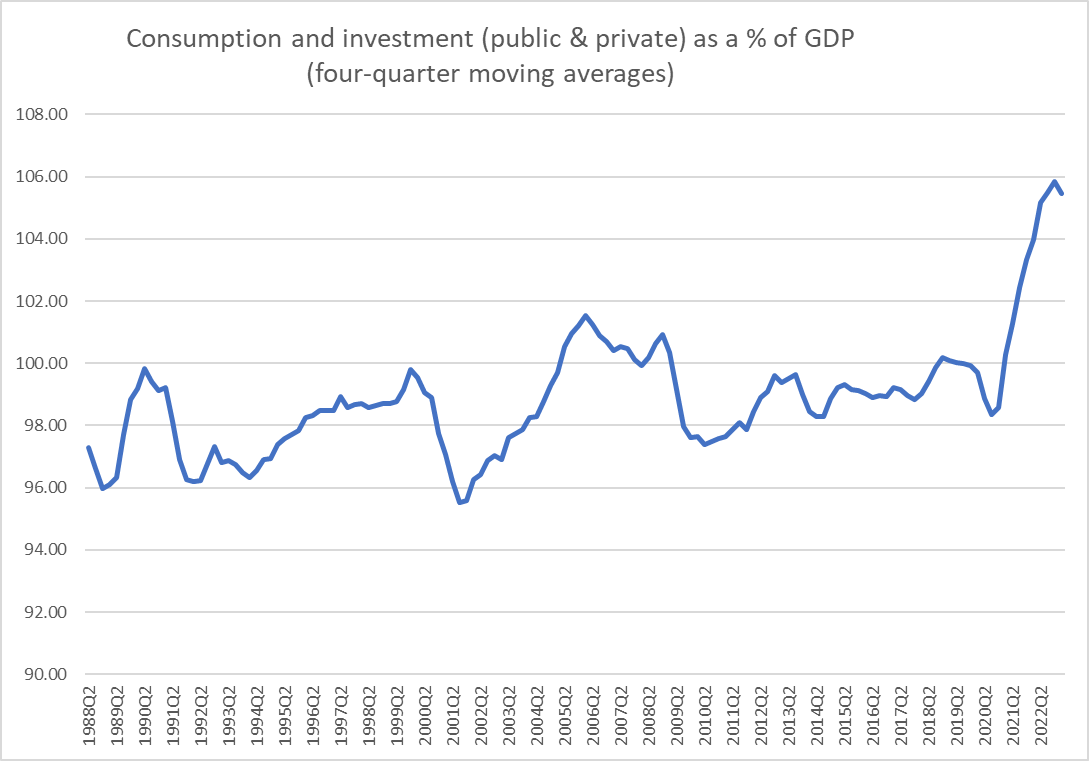

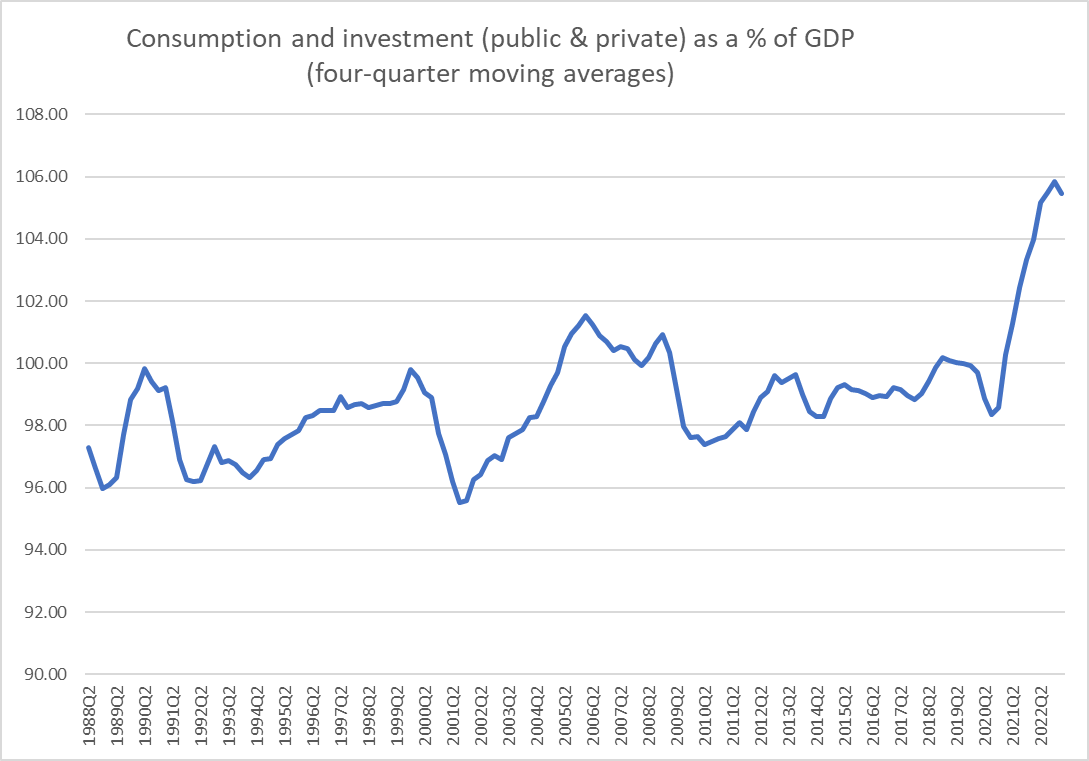

Domestic demand is known, in national accounts parlance, as Gross National Expenditure (or GNE). It is the total of consumption (public and private), investment (public and private) and changes in inventories.

I’ve been pottering around in that data over the last few days, and put this chart (nominal GNE as a percentage of nominal GDP) in my post last Thursday.

This ratio has tended to be low in significant recessions and high around the peaks of booms – investment is highly cyclical -but for 30+ years it had fluctuated in a fairly tight range. The move in the last couple of years has been quite unprecedented, in the speed and size. There was huge surge in domestic demand relative to (nominal) GDP.

One of the points I’ve made a few times recently is that country experiences with (core) inflation have been quite divergent over the last couple of years. The Minister of Finance in particular is prone to handwaving about “everyone faces the same issue” around inflation, and the Bank isn’t a lot better (doing little serious cross-country comparative analysis). But the differences are large.

And so I wondered about how those domestic demand pressures had compared across countries.

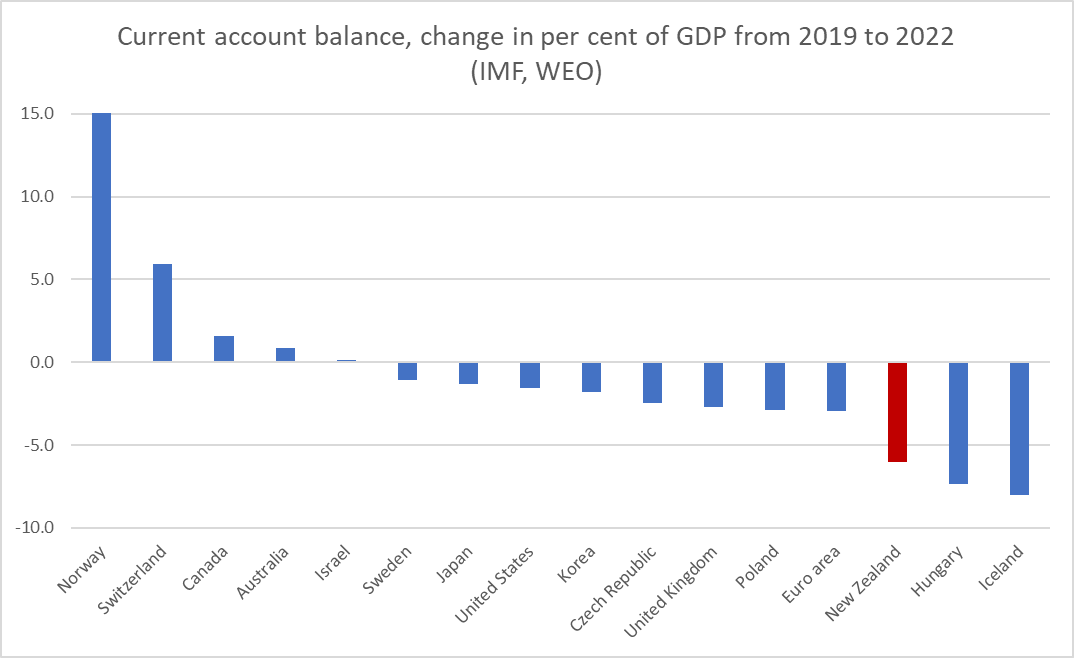

One place to look is to the change in current account deficits as a share of GDP. This chart, using annual data from the IMF WEO database, shows the change in countries’ current account balance from 2019 to 2022 (Norway is off this scale; what happens when you have oil and gas and another major supplier is being shunned)

There has been a fair amount of coverage of the absolute size of New Zealand’s current account deficit, and even a few mentions of the deficit being one of the largest in any advanced country. But for these purposes (thinking about monetary policy and demand management) it is the change in the deficit that matters more. Over this period, New Zealand’s experience has not just been normal or representative, instead we’ve had the third largest widening in the current account deficit of any of these advanced countries (those with their own monetary policy, and thus the euro-area is treated as one). Both Iceland and Hungary have slightly higher inflation targets than we do, but they have a lot higher core inflation (see chart one up).

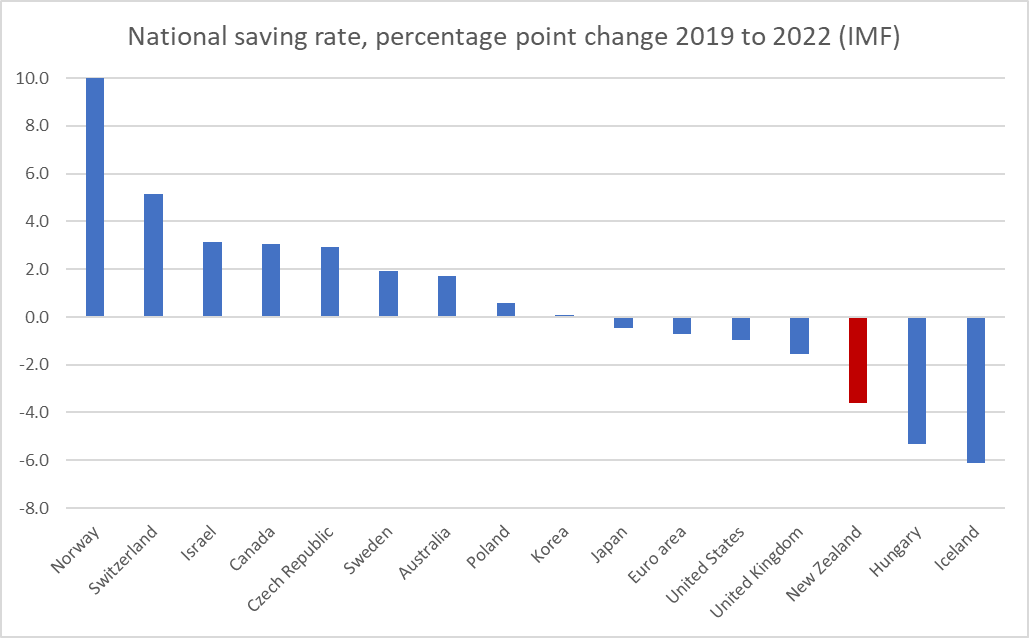

The current account deficit is analytically equal to the difference between savings and investment. Over that 2019 to 2022 period investment as a share of (nominal) GDP increased in all but two of the advanced countries shown. Of the four countries where it increased more than in New Zealand, three are those with core inflation higher than New Zealand.

National savings rates (encompassing private and government saving) paint a starker picture. Somewhat to my surprise, of these advanced countries the median country experienced a slight increase in national savings over the Covid/inflation period.

Norway is off the scale again, because I really want to illustrate the other end of the picture. That is New Zealand with the third largest fall in its national savings rate of any advanced country.

What about that chart of nominal GNE as a share of nominal GDP? How have other countries gone with that ratio? There is a diverse range of experiences, but that sharp rise in the New Zealand share really is quite unusual, equal largest of any of these advanced countries.

(If you are a bit puzzled about Hungary – I am – all the action seems to have been in the last (March 2023) quarter’s data).

But lets get simpler again. Here is a chart showing the percentage change in nominal GNE (growth in domestic demand, the thing monetary poliy influences) from just prior to the start of Covid to our most recent data, March 2023.

It looks a lot like that earlier chart comparing core inflation rates across countries. In this case, New Zealand had the fourth fastest growth in domestic demand of any of these countries over this period (and those with higher growth are not countries with outcomes we’d like to emulate). And in case you are wondering, no this wasn’t just a reflection of super-strong GDP growth: over this period New Zealand’s nominal GDP growth was actually a little below the growth in the median of these advanced economies. The economy simply didn’t have the capacity to meet the nominal demand growth the Reserve Bank accommodated and the imbalance spilled into a sharp widening of the current account deficit and high core inflation. It wasn’t Putin’s fault, or that of nature (the storms), it was just bad management by the agency charged with managing domestic demand to keep core inflation in check.

I’ve also done all these chart etc using real variables. The deviations are often less marked, but no less substantive for that. Real GNE (real domestic demand) growth from 2019Q4 to the present in New Zealand was third highest among this group of advanced economies, and only Iceland (see inflation and BOP blowouts above) had a larger gap between growth in real domestic demand and real GDP.

I don’t really want to divert this post into an argument about fiscal policy over recent years (monetary policy has to, as the Governor often notes, just take fiscal policy as it is, as just another demand/inflation pressure) but for those interested the government share of GDP has been high (which usually happens in recessions since government activity isn’t very cyclical) but private demand is what really stands out).

Bottom line: all those stories trying to distract people, including MPs, with tales of the evil Russian or the foul weather or whatever other supply shock he prefers to mention, really are just distractions (and intentionally misleading ones by the Bank). The Bank almost certainly knows they aren’t true, but they have served as convenient cover for the fact that the Bank simply failed to recognise the scale of the domestic demand (right here in New Zealand, firms, households, and government) and to act accordingly. We are now still living with the 6 per cent core inflation consequence. It is common – including in the rare Bank charts – in New Zealand to want to compare New Zealand with the other Anglo countries. But what the Bank has never acknowledged – and just possibly may not have recognised – is much larger the boost to domestic demand happened in New Zealand than in the US, UK, Canada or Australia. And domestic demand doesn’t just happen: it is facilitated by settings of monetary policy that were very badly wrong, perhaps more so here than in many of those countries.

Perhaps one could end on a slightly emollient note. Getting it right in the last few years has been very challenging, and it wouldn’t entirely surprise me if when all the post-mortems are done some of relative success and failure proves to have been down to luck (good or bad). But as in life, central banks help make their own luck, but digging deeper, posing and publishing analysis even when they don’t know all the answers, and by taking a coldly realistic view, not attempting to hide behind spin, misrepresentations, and what must come close to outright lies. Even by acknowledging errors, the basis for learning better, and being able to feel and display those most human of qualities, regret and contrition. We need a Governor and MPC members doing all this a lot more than has been on display here in the last year or two. Our lot show little sign of trying, or of even being interested in feigning seriousness.

I’m not a huge fan of central banks publishing medium-term economic forecasts (or projections as we were usually schooled to call them). As I understand it, decades ago the Reserve Bank of New Zealand only started publishing them because the Official Information Act was passed (and in those days the forecasts made little or no difference to policy so there wasn’t even an arguable ground for withholding). My scepticism only increased as the projections assumed an increasingly significant place in the policy communications, including the move to endogenous interest rate projections from 1997. It isn’t that a central bank’s forecasts are likely to be worse than anyone else’s, just that medium-term economic forecasting (cyclical stuff 2-3 years ahead) is really a mug’s game, and those medium-term forecasts rarely if ever have much impact on the accompanying OCR decision. OCR decisions are almost always, and necessarily (given the state of uncertainty, limited knowledge etc), driven by the latest data releases, which are at best real-time contemporaneous, and more often relating to periods a month or three back (the latest NZ GDP data are for the quarter that ended in March). And that is as it should be. And yet in my experience of the Reserve Bank forecasting and policy process, inordinate amounts of time (including time of the Governor) was spent on numbers for periods so far ahead they would, almost inevitably, be quickly invalidated; often more time (and more senior management smoothing, for messaging purposes) on where we thought things might be in 2 years than on where we think they are right now. I recall a speech some years ago now from a retiring senior European central banker who suggested that perhaps central banks shouldn’t bother publishing for horizons much more than six months, and that line still has some appeal to me. It isn’t about trying to withhold information, but about having nothing useful to say and no robust grounds on which to say it. None of that is a criticism of the Reserve Bank, or their peers abroad, it is just the state of (lack of) knowledge.

Of course, the international trend has been in the other direction, with more central banks publishing more forecast information, and for the time being we are where we are. The Reserve Bank of New Zealand was once considered a leader in forecast transparency, but there are some areas in which they really aren’t very transparent at all. Thus, despite the (quite appropriate) policy focus on core inflation, the Bank does not publish forecasts (even for the next few quarters) for any of the measures of core inflation, and despite the evident seasonality in the inflation data (sufficient for SNZ to publish seasonally adjusted series), the Bank’s inflation projections are not seasonally adjusted (in contrast to almost all quarterly quantity series). On core inflation, even the Reserve Bank of Australia, publishes projections (albeit at six-monthly rests rather than for each quarter) for annual trimmed mean inflation

But if I’m sceptical of the merits of published forecasts, that doesn’t mean those forecasts have no information about the central bank’s own thinking at the time of publication. In fact, the numbers can be – and often are – a significant part of the Bank’s storytelling and tactics, in support of a current policy stance. And how those numbers change over time can also be revealing.

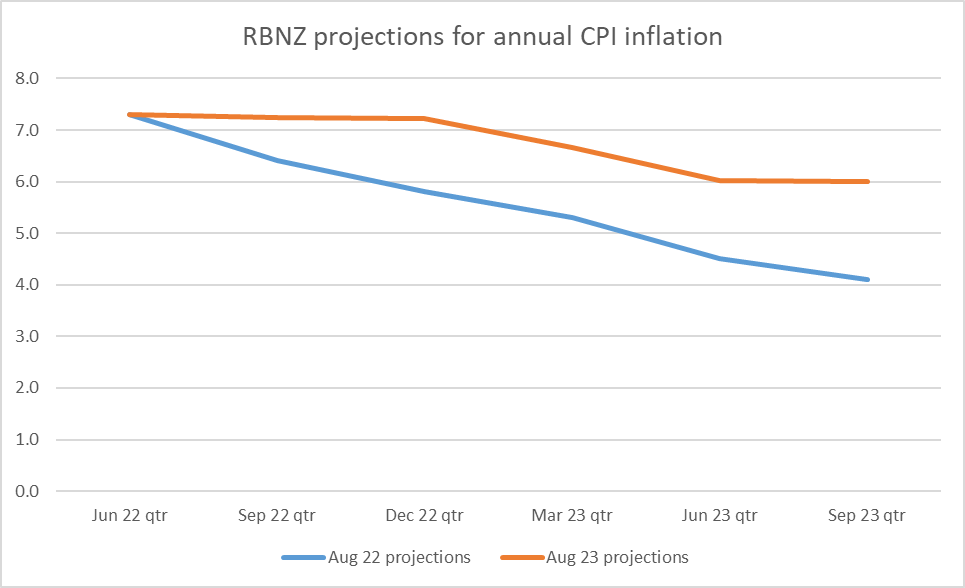

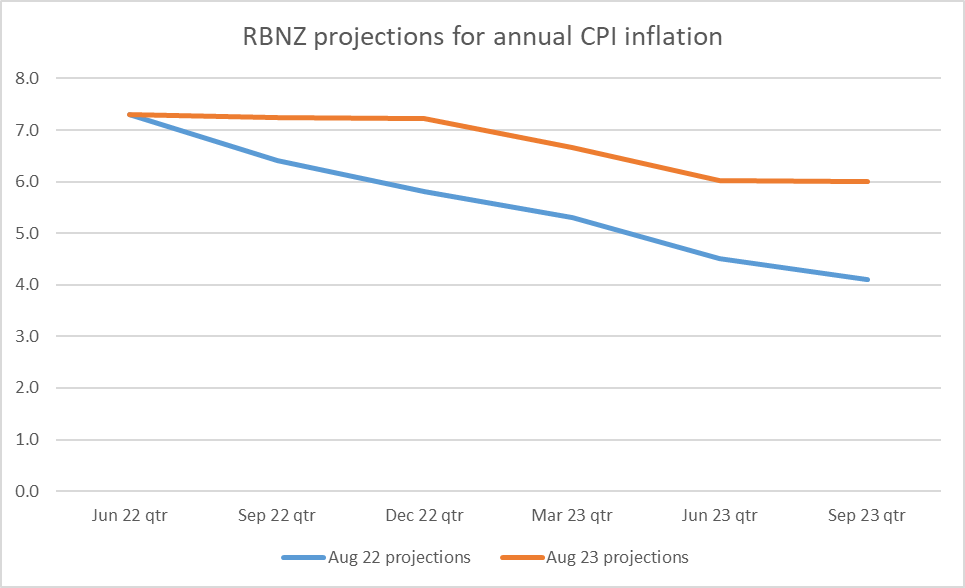

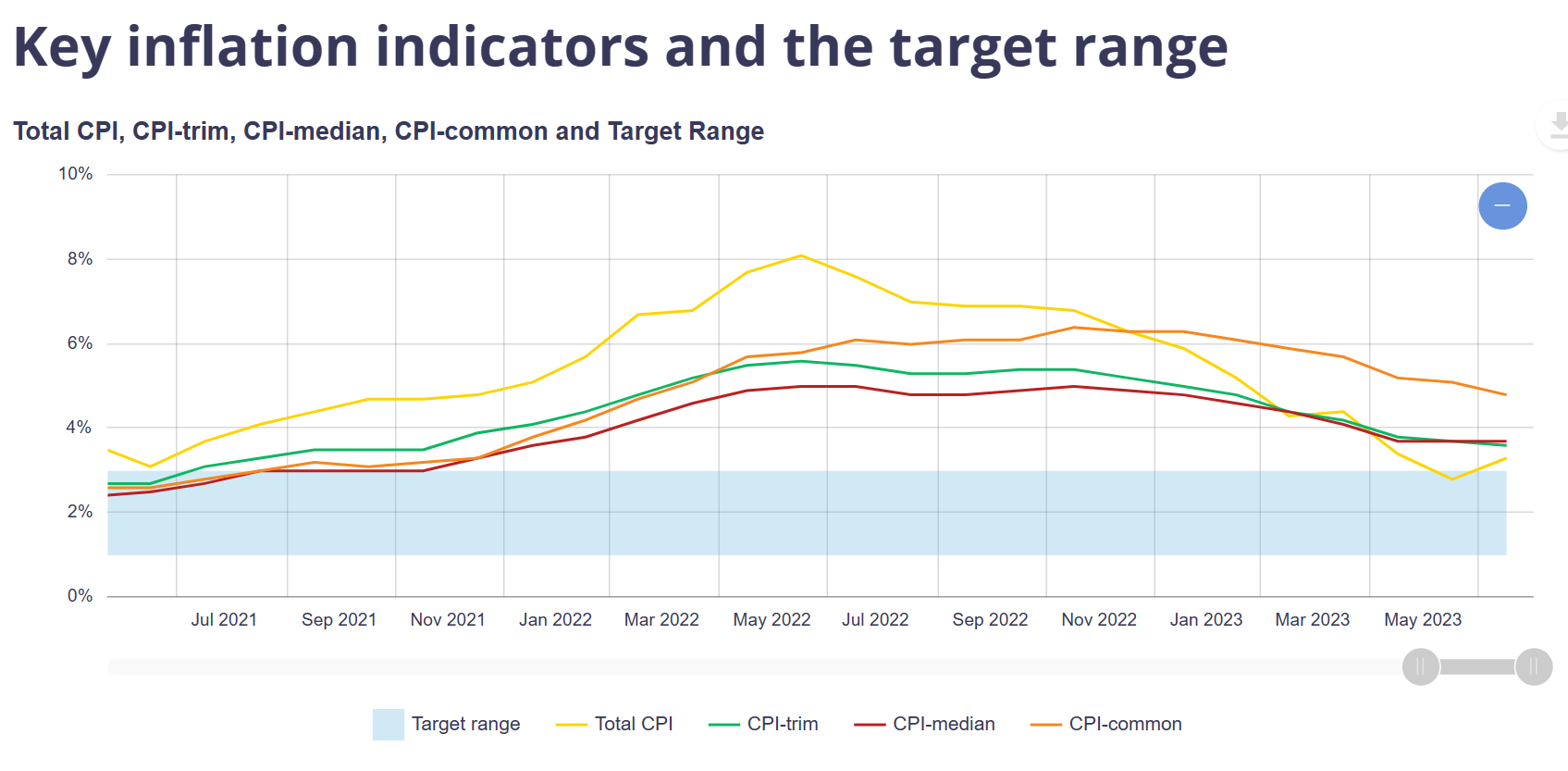

You’ll recall – I highlighted it in my post last Thursday – that one of the good features of last week’s MPS was the upfront acknowledgement that core inflation was hanging up, and that if anything domestic inflation had been a little higher in the most recent quarter than the Bank had been expecting. For example, the minutes record that “measures of core inflation remain near their recent highs”, a point reiterated a couple of times in chapter 2 (the policy assessment). In case there is any doubt, they have a chart showing the core inflation measures grouped around 6 per cent (annual rate). The target, you will recall, is 2 per cent – the midpoint (that MPC is required to focus on) of the 1 to 3 per cent target band.

The Bank doesn’t use one of my favourite graphs, of quarterly core inflation

…but they don’t really need to. They seem to be in no doubt that core inflation has been hanging up, in ways that are at least a little troublesome.

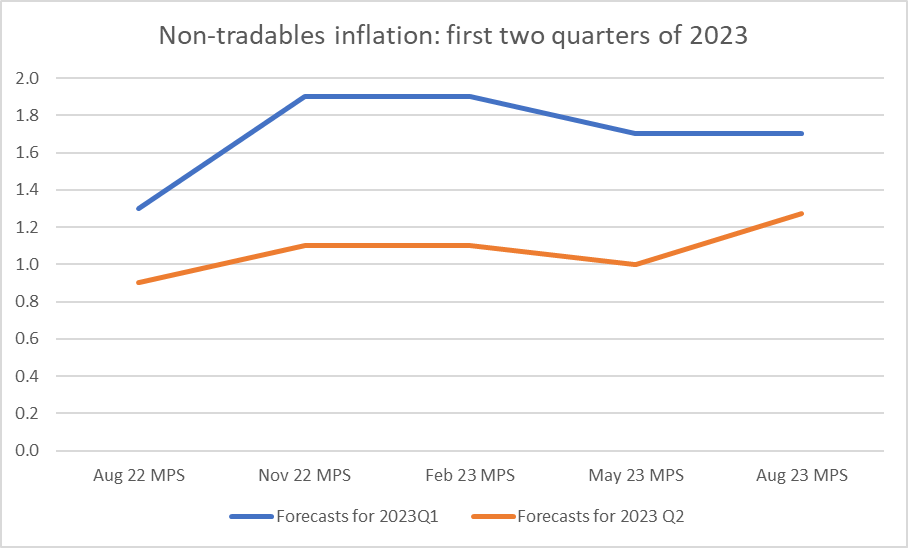

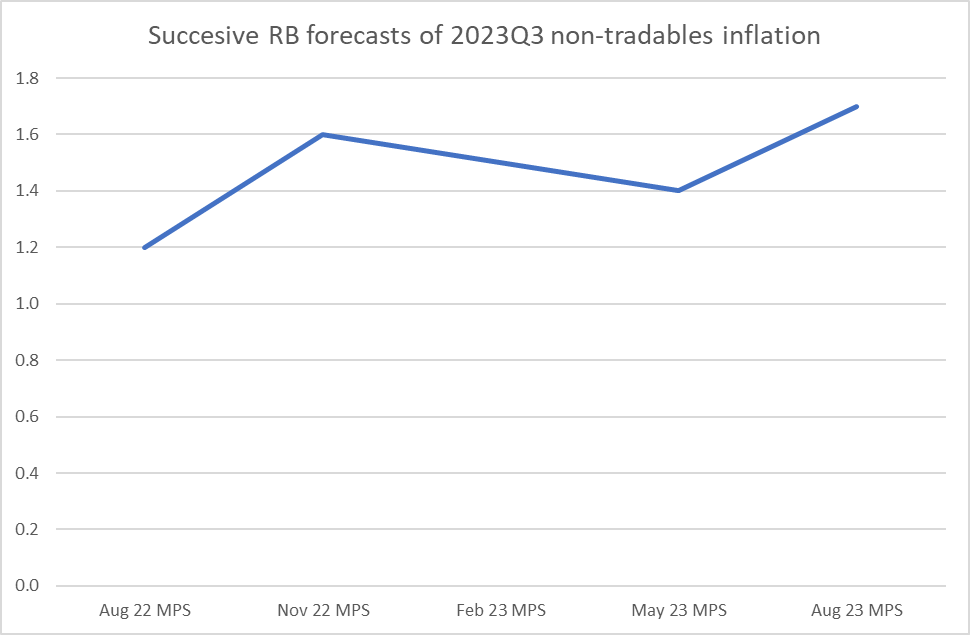

Of the published forecasts, the closest one to showing their hand on the outlook for core inflation is the forecasts for quarterly non-tradables inflation. Non-tradables inflation tends to run persistently higher than tradables inflation (for this century to date, annual non-tradables inflation has averaged 3.4 per cent while annual tradables inflation has averaged 1.4 per cent), and so even as tradables inflation has been abating, non-tradables inflation has been running at an annualised rate 6.6 per cent, a bit higher than core.

Looking out to the medium-term, the Bank seems to consider that non-tradables inflation of about 3.3 per cent will be consistent with inflation being at 2 per cent (for the final year of the projections, to September 2026, they show things being settled at those rates).

In the nearer-term they have generally been having to revise up their forecasts for non-tradables inflation. Here is how RB forecasts evolved over the last year towards the actuals for the two quarters in the first half of 2023.

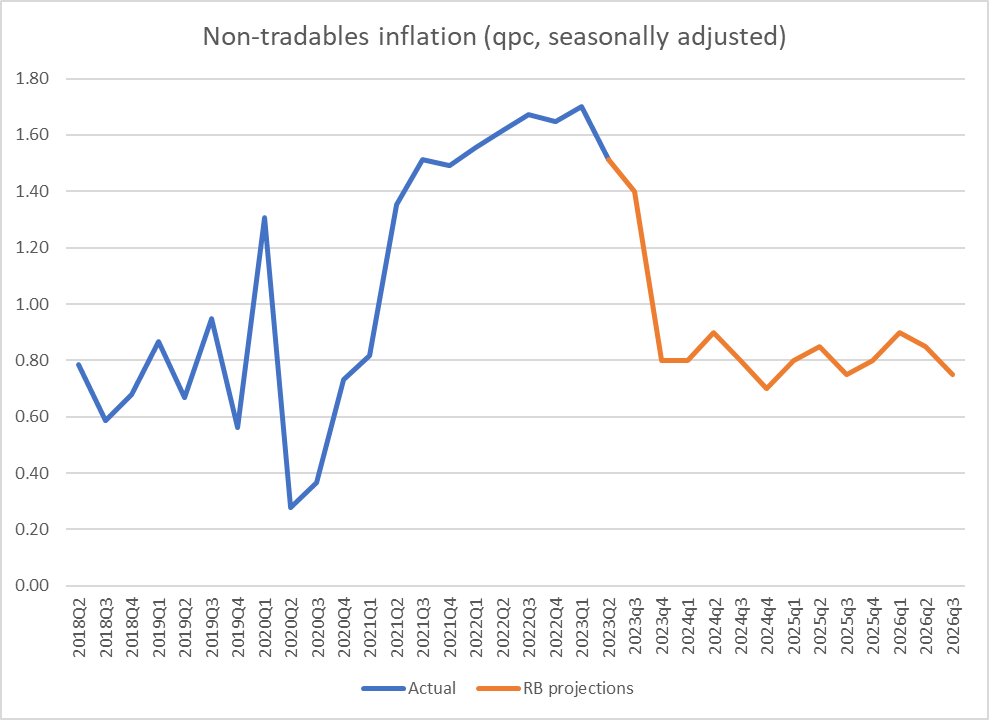

And here is the SNZ series for non-tradables quarterly inflation on a seasonally adjusted basis.

That last observation is modestly encouraging although (a) per the previous chart, it was quite a bit higher than the Bank was expecting, and (b) there is no sign of anything similar in the analytical core inflation measures themselves. Better than the alternative I guess, but nothing to hang your hat on (and as I noted earlier, when writing about inflation outcomes to date the Bank does not do so in the MPS – it is appropriately uneasy about core and domestic inflation holding up).

As it happens, the Bank has also been revising up its forecasts of Q3 non-tradables inflation – its latest view for the current quarter is (a touch higher) than any of its projections for the quarter over the last year.

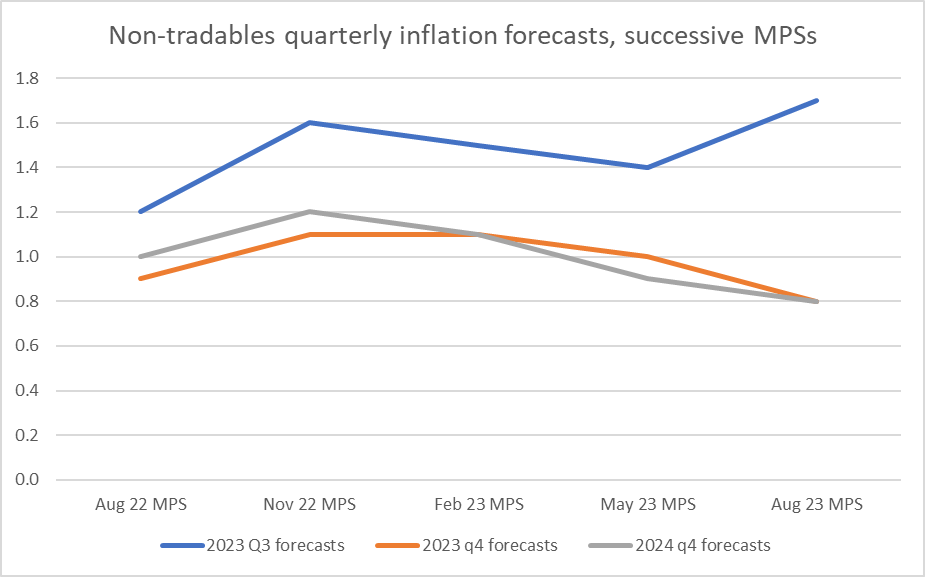

But….seasonality matters. The Bank doesn’t publish its inflation forecasts in seasonally adjusted terms. But if we compare the actual data, seasonally adjusted and not, we can back out some approximate seasonal factors, and convert the Bank’s projections into (approximately) seasonally adjusted terms (more technically oriented people could no doubt do it more formally).

This is the result

On these projections, non-tradables inflation (projections for which have been revised up to new highs) does fall a bit in in the September quarter, but then by the December quarter – measured centred on 15 November, now less than 3 months away, starting less than 6 weeks from now – suddenly the whole domestic inflation problem is solved. In (rough) seasonally adjusted terms, non-tradables inflation is back down to 0.8 per cent for the December quarter, a rate not seen since the start of 2021, and a rate consistent with all the inflation problems being solved. Annual rates take a while to come down to be sure, but any policy-setting agency would be firmly focused on quarterly tracks and…..within three months we are there (at least according to the Reserve Bank).

Quite the contrast: revising up the Q3 forecasts (a quarter we already know a bit about) and revising materially down the December 2023 and March 2024 forecasts, which we don’t yet know anything firm about.

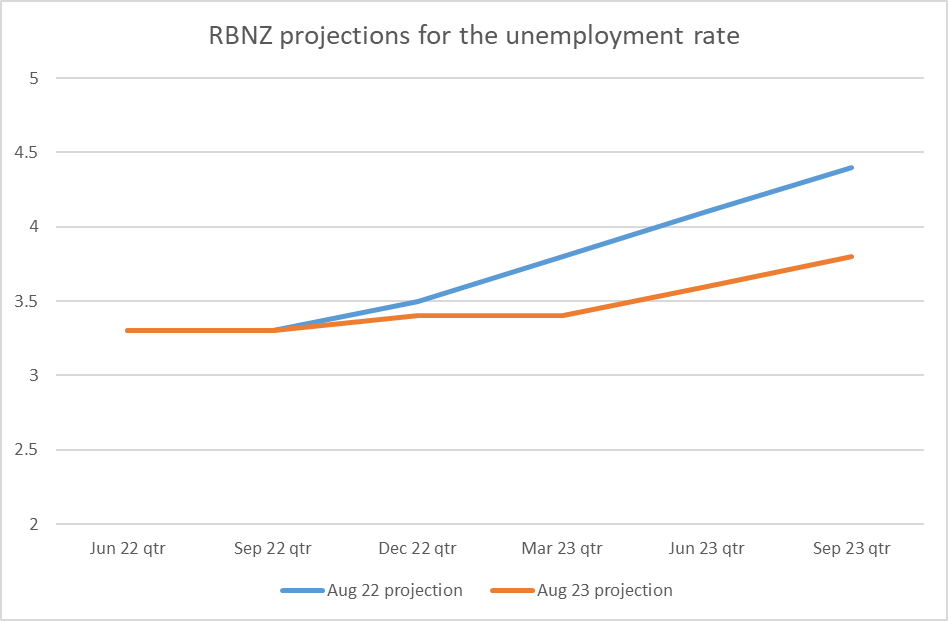

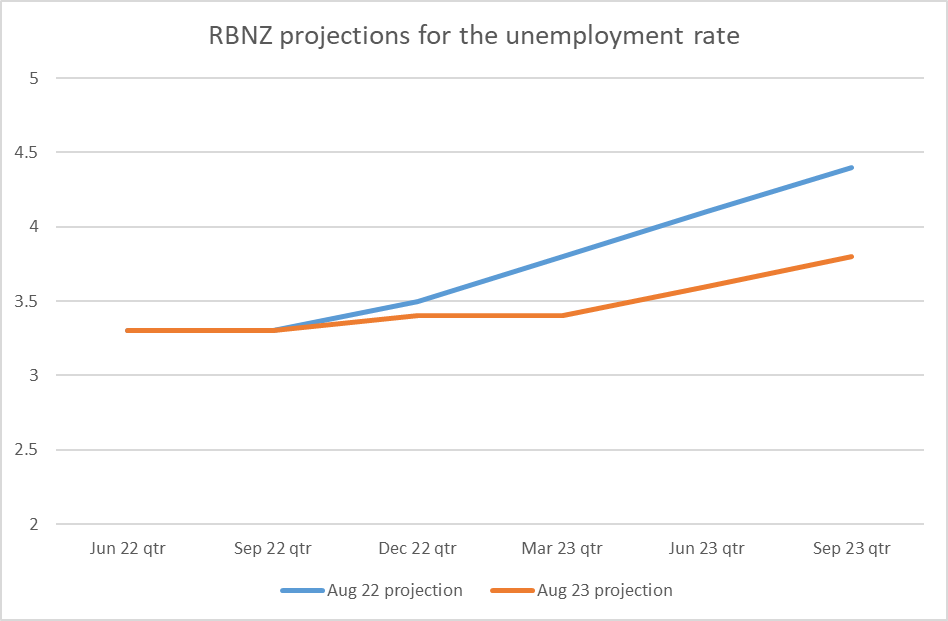

I won’t bore you with the charts but it is not as if they are suddenly expecting a much sharper rise in the unemployment rate. Actually, unemployment rate projections for the next 6 months have been revised down quite a bit.

It all seems like a rather miraculous good news story. and yet one that the Bank left buried in the website tables and made no mention of at all, not in the MPS itself or at FEC.

Suggesting they don’t really believe it themselves. How likely is that we’d go from an entrenched (core) inflation problem now (and in the most recent published quarter) back to something consistent with the target midpoint in a matter of weeks? Frankly, it doesn’t seem very likely.

One possibility – and who knows if it is the explanation – is that they really don’t want to raise the OCR again. That might be for political reasons, or because they like this idea of being (one of the first) central banks to reach a peak rate (or some, conscious or unconscious, mix of the two), but had those quarters from 2023Q4 into next year been a bit higher – domestic inflation abating more gradually, consistent with the fairly modest recession forecasts – they would have been under a great deal more pressure to raise the OCR now or in early October. Neither explanation would be to the Bank’s credit. Perhaps neither is the correct story, but then we don’t have any explanation at all from the Bank. If they really believed inflation was collapsing as we speak, surely they’d have told us?

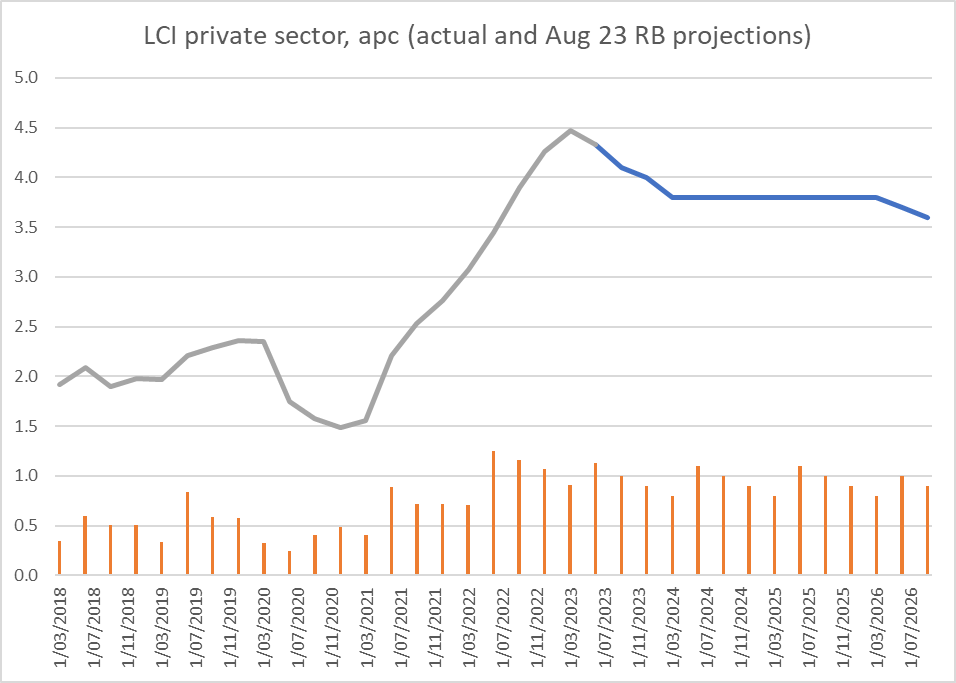

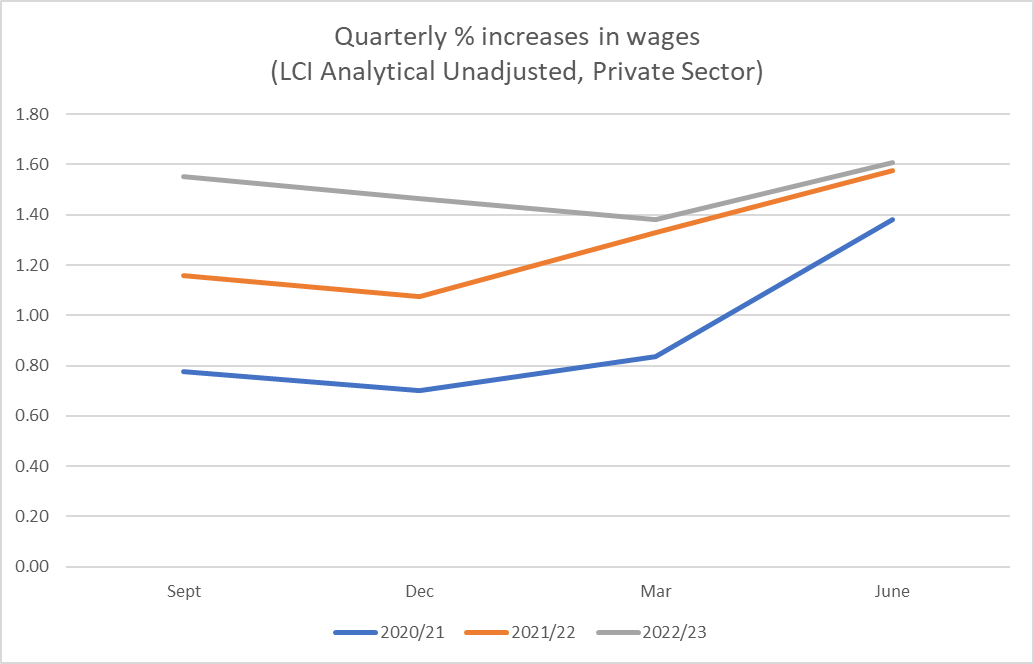

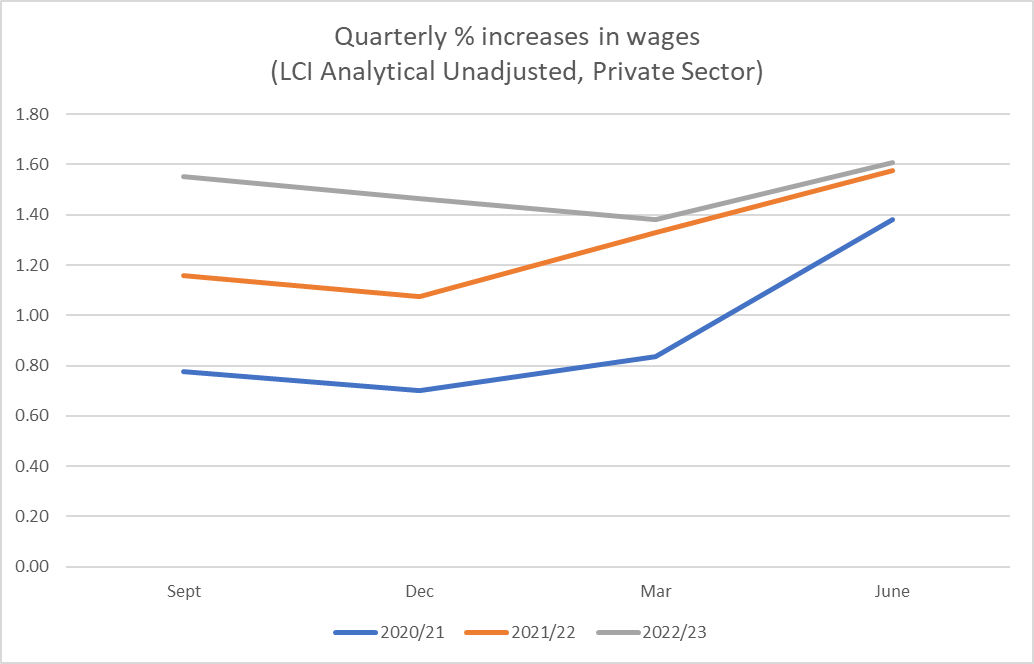

There are some other odd features in the numbers. Take the wage forecasts for example. The Bank doesn’t publish forecasts for the only data we have on wages rates themselves (that is the stratified LCI Analytical Unadjusted series). As I’ve shown previously, inflation in private sector wage rates seems to be levelling off (but not yet falling).

The Bank publishes forecasts for the LCI itself, for the private sector. The LCI is not a measure of wage rate but is designed to be a proxy for something like unit labour costs. Over the decades inflation in the headline private sector LCI has averaged somewhere not too far from the core rate of CPI inflation.

Eyeballing the chart might suggest that annual increases in this measure of the LCI of around 2 per cent might be roughly consistent with inflation at target.

Here are the Bank’s forecasts for LCI inflation

Note first that straight line. No model will have produced that, but rulers are a handy tool for forecast teams responding to gubernatorial whims. But more importantly, note that again they think the job is all but done – those quarterly rates of increases come down hardly any more (that apparently now being consistent with core inflation at the 2 per cent target, but again with no explanation). But then this measure of wage inflation holds up at a remarkably high levels even as the unemployment rate rises from the current 3.6 per cent to 5.3 per cent and only gets back to 5 per cent by the end of the projection period. It doesn’t make a lot of sense and simply isn’t very plausible.

None of it makes much sense. And these days, with a central bank whose Governor and Board chair just make up stuff when it suits, it is impossible to take anything they say or publish at face value. Which is a terrible place to be, when so much power is vested in the Bank, and so much havoc and loss wreaked, with no sign of any effective accountability at all.

In my post on Thursday I commented briefly on the appearance by the Governor and his Chief Economist at Parliament’s Finance and Expenditure Committee. They tried to suggest to the Committee that to the extent there had been inflation forecast errors over the last year – responding to a question from Nicola Willis – that much of it was down the summer storms including Cyclone Gabrielle. But then a helpful staffer in the back row – who may not have been so popular with management after that – piped up and explained to FEC that the impact of the cyclone was perhaps 0.1 or 0.2 per cent. The forecasting error Willis had asked the Governor about was 1.9 percentage points (the Bank had last August forecast that inflation would be 4.1 per cent in the year to September 2023, but now think that inflation rate will be 6.0 per cent).

It was pleasing to see yesterday that veteran journalist Jenny Ruth has emerged from her restraint of trade purdah after leaving Business Desk to begin a new Substack newsletter (free for the first few weeks) and that one of her first columns was about the very same Reserve Bank appearance. Her piece is worth reading. She and at least one other journalist have commented on the Governor having “toned down his hostility” towards Nicola Willis in this appearance. The tone may have been less bad, but the substance was just as contemptuous as ever – and not just of Willis but of Parliament itself. That was, once upon a time, treated as a serious matter. This is from Parliament’s own website

My Thursday post was written from listening to the appearance live and scrawling a few notes as I went. Jenny Ruth’s column prompted me to go back and listen to the recording (you can find it here), being able to stop as needed and take fuller notes. I pick up that segment of the appearance with Orr closing his opening remarks declaring that he was very proud of the Monetary Policy Statement document.

Nicola Willis then asked “what is going on? Inflation has been out of the target range for 27 months. Why is it taking so long to get inflation out of our economy?

The Governor responded along the lines of “Good question. It is a global question. The drivers of inflation have been changing through time, but all biased up, There were lockdowns, supply constraints, the Ukraine war and pressure on commodity prices, and now supply shortages in New Zealand, with severe storms. The drivers have changed but we are confident, subject to the next shock, that inflation pressures are easing”.

Nicola Willis asked if the Bank had stimulated the economy too much, and the response was yes.

The Bank’s Chief Economist (and MPC member) Paul Conway added that “it had been one supply shock after another, citing Covid, the Ukraine War, the pressure moving from goods prices to services prices, and all in all a very unusual period.

He added that the Reserve Bank had however been one of the first central banks to tighten and one of the first to signal that they thought they had reached a peak.

Nicola Willis then asked about the contrast with the US, where inflation had come down faster and appeared to be doing better.

Conway responded that he had “been amazed at the performance of the US, that it was a very different economy, a very flexible one”. He noted that unemployment had rocketed upwards when Covid began and then had fallen very sharply with resources being reabsorbed. The US was “leading the globe when it comes to inflation coming down”, but that “without thinking about it too much” New Zealand had been somewhere in the middle of the pack over the last year.

Willis observed “it strikes me how inaccurate the Reserve Bank’s forecasts have been”, citing the August 2022 forecast that CPI inflation for the year to September 2023 had been 4.1 per cent, and that the latest forecast was for 6 per cent. “Have you looked at the inaccuracies and what is going on there?”

Orr responded that “yes, we do so constantly”, stressing that the great thing about monetary policy was that it as a repeat game, reviewed afresh every six weeks, when they could reflect on surprises relative to forecasts. He indicated that the Bank was working across a whole range of different issues on how to improve. Recent forecasts erros had been “very well explained” by supply shocks, noting that a year ago they had not known about cyclone Gabrielle.

Willis then asked “how much of the difference of 1.9 percentage points is down to Gabrielle?”

The Governor responded “I don’t have that”.

Willis responded that “it seemed a stretch” that cyclone Gabrielle could account for that much of it.

Conway responded that they could back the numbers out to look at exactly that question, and then launched into a bit of a defence of the Bank’s inflation forecasting more generally, argued that they were “pretty good” relative to other forecasters but that it was challenging even in normal times, but that these had not been normal times and that the supply shocks had been “incredibly disruptive”. He said that the Bank had an active programme underway to better understand economic dynamics.

Anna Lorck (a Labour backbench MP) then asked “just for clarity, how much lower would inflation be without Gabrielle?”