The Reserve Bank Governor has given an interview to TVNZ’s Katie Bradford, apparently done under the aegis of the Q&A show but too late in the year to actually be broadcast on Q&A itself or to be done by Jack Tame, Q&A’s regular and most demanding interviewer.

There is a TVNZ article reporting the interview here, and you can find the full thing (only about 13 minutes) somewhere on TVNZ+ (my son found it for me). [UPDATE: Apparently that was only half the interview and the full 26 minutes is on the Q&A Youtube account.]

What is reported in the article is pretty breathtaking, with Orr reported as standing by his (or, presumably, the MPC’s) decisions during and since Covid with no apparent regrets, and then moving on to attack the public and the media for being focused on housing and house prices. We – and he – might regret the fact that we do not have a well-functioning land supply/use policy regime, but we don’t, and haven’t done so for decades, so it should hardly be a surprise (or a cause for attack/lament) that when interest rates are cut in what proves to be an overheating economy house prices go up.

But it got a whole lot worse when I listened to the full interview itself, where Orr seemed to just play on the fact that his interviewer wasn’t a specialist (with all the facts at her finger tips) to simply run claims that he knows not to be true. It was a reprise of his form earlier in this cycle when he repeatedly and deliberately misled Parliament’s FEC (but so supine are our democratic institutions that there were no consequences for what Parliament’s website solemnly assures us is a serious offence).

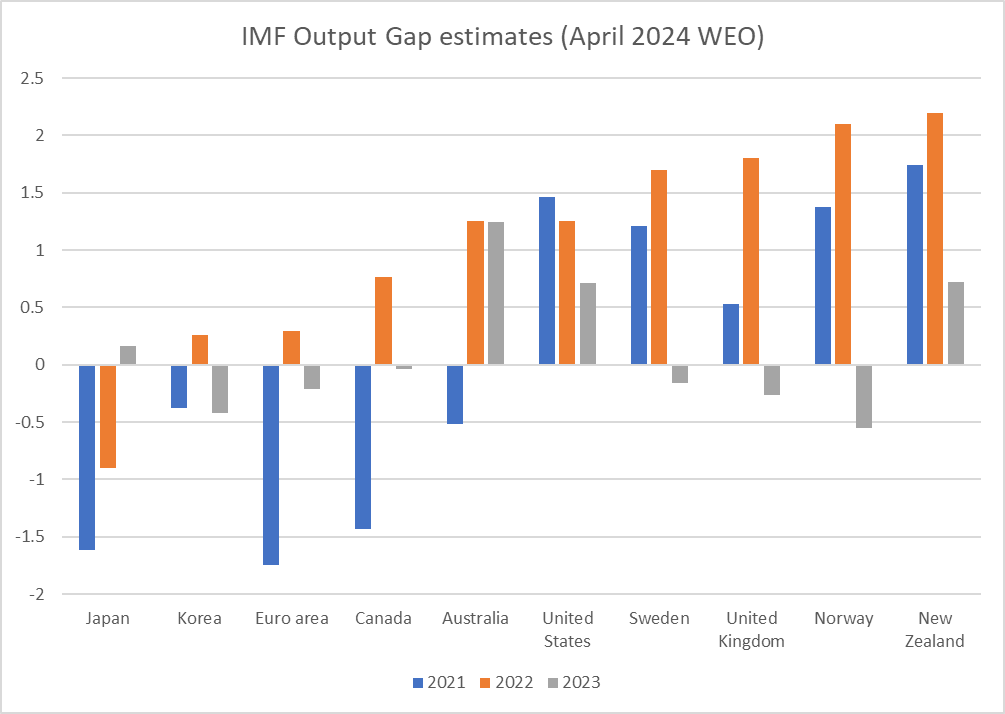

Orr was asked whether the Bank had been too slow to raise rates (of course it was, as the Bank has even grudgingly acknowledged in the past). His response was to claim that the Reserve Bank of New Zealand was the 2nd or 3rd central bank to raise rates in 2021. It simply wasn’t so. Even among OECD economies – and there are only about 20 separate monetary policy areas in it (much of the OECD having just the euro) – the Reserve Bank was the 8th (equal) to move (those moving ahead of us were Iceland, Norway, South Korea, Mexico, Chile, Czech Republic, Hungary). Perhaps as importantly, the issue should never be about who went first or second, but whether a particular national authority moved sufficiently early and aggressively for the circumstances their own economy faced. On IMF estimates, New Zealand had the most overheated economy of any of the advanced country monetary areas it does the numbers for (a group which doesn’t include all those in the list above, but does include the US, UK, Canada, Australia, Japan).

Orr then went to the claim that the Bank had been “lauded internationally – although not domestically” for being one of the most responsive central banks. It is certainly true that some market commentators have run such a line, but almost all of them seem to have had in mind the big countries and the Anglo countries, not the wider group of OECD economies. The Reserve Bank certainly wasn’t the slowest to move, but then it was dealing with a really badly overheated economy and should have moved a lot earlier. Their mistakes weren’t unique – misreading economies and pandemic macroeconomics was a common mistake, among central banks and private commentators – but they voluntarily took on the power and responsibility in New Zealand, and they actually made the bad policy calls, including increasing rates too late and initially far too sluggishly. Other people can hold their central banks to account.

(And, of course, the MPC also lost $11 billion or so or taxpayers’ money punting in the bond market. TVNZ didn’t ask about that particular bad call so we were spared a repeat of Orr’s blustering attempts to defend that. Puts the cost of running an RNZN vessel straight onto a reef not realising the autopilot was still on in some perspective….)

And then Orr claimed that the Reserve Bank was one of the few central banks confidently reducing policy rates. Which was a bit odd when most advanced country central banks have been reducing policy rates in recent months (obvious exceptions being Australia and Japan). But don’t let the facts get in the way of the Governor’s spin.

He had the gall to round off that section of the interview by suggesting, rather patronisingly, to Bradford that “your potted history is kind of incorrect”. Dear, oh dear. This from a very senior and powerful public official. Is this the sort of thing the Minister of Finance expects/tolerates? (Well, on the evidence so far anything goes.)

Bradford moved on. As was accepted, had it not been for the Covid outbreak in Auckland, the Bank would have started tightening at the August 2021 MPS (they actually started at the next review). So Bradford took a look at the projections in that Monetary Policy Statement. She pointed out (correctly) that in those projections, annual inflation was expected to be back down to 2.2 per cent by the year to September 2022 (with, as it happens, very little monetary policy help at all: as everyone agrees, there are long lags, and by the end of 2021 the OCR was expected to be only 0.75 per cent). I guess her point (obviously correct) is that the Bank was still badly misreading things by that point (and of course even now annual core inflation is still somewhere between 2.5 and 3 per cent, having required an OCR at 5.5 per cent to bring that about).

But Orr wasn’t going to be bothered engaging with facts. Instead, we got the same old outrageous claims he used to try to fob Parliament off with. “Do you know what happened after that [August 2021]”, he asked. “We had the Ukraine invasion, rising food prices”, going on to add in cyclone effects and so on. He even had the gall to suggest that we had among the lowest inflation rate peaks in the OECD and that European countries had been dealing with 20 per cent inflation. It is an outrageous attempt to mislead and distract, simply breathtakingly dishonest, and especially so when set against any discussion of core inflation or the economic overheating. Take the New Zealand labour market for example: the unemployment reached its lowest level (extremely overheated) in the December quarter of 2021 (ie before the invasion), oil price pressures from the invasion never lasted long, and…..as importantly….both food and energy prices are typically “looked through” by central bank policymakers focusing on core inflation. On CPI ex food and energy measures, New Zealand’s peak was about middle of the pack among OECD countries (and the extreme headline numbers in a few countries were largely the result of the gas price shock to which New Zealand – no pipeline or LNG trade – was not exposed).

Orr then moved on to an interesting claim (that I have not heard him make before, and which has not been documented in any published papers or material in MPSs) claiming a) that to have kept core inflation in the 1-3 per cent range the OCR would have to have been raised to 7 per cent on the first day of the pandemic, and b) that even if that had been done we’d still have had 6 per cent headline inflation. Neither result seems very likely, and given Orr’s record of just making stuff up should be heavily discounted unless/until they produce some robust formal estimates. On Orr’s telling it would have taken more monetary restraint to stop inflation getting away than it actually took to bring it down again once it had gotten away. That doesn’t seem very likely, and perhaps a useful counterpoint is the experience of Japan and Switzerland which didn’t cut policy rates into the pandemic, and didn’t see a particularly severe later inflation experience. As for the 6 per cent claim, that seems simply preposterous, since there has been no time in the last few years when the gap between headline and core inflation has been anything like as large as 3 percentage points.

Later in the interview, questioning moved on to fiscal policy. Here I will give Orr credit on one point: he explicitly corrected the journalist to note that the current goverment had certainly cut spending, but that it had also cut taxes, and that the two effects were roughly even. This is exactly consistent with the estimates in Treasury’s cyclically-adjusted balance series (chart in Monday’s post), in which this year’s deficit is just a touch larger than last year’s. Of course, it would have been nice had the Bank made this point in its MPSs, instead of spending the last 18 months – both governments – avoiding the issue and focusing on largely irrelevant series of government consumption and investment spending (rather than the cylically-relevant) fiscal balance and fiscal impulse measures.

For the rest of it, Orr was back in his preferred space, playing politician and advancing personal political and ideological agendas that are simply out his bailiwick. It was, we were told, critical for governments around the world to close infrastructure deficits and New Zealand’s was “one of the worst”. He appeared to attack a focus on reducing deficits and keep government debt in check, suggesting that the government needed to spend “a lot more” on infrastructure, suggesting that New Zealand had been failing in this area since World War Two (a claim that of course went unexamined – in fairness no time – but presumably includes overbuilt hydro power capacity, sealed roads in the middle of nowhere etc). Now, in fairness, he did also talk about enabling private capital – this the same Governor who only a few months ago was bagging foreign investment – but the overwhelming tone was to welcome more public debt. Waxing eloquent he launched into Labour Party and left wing themes about how great it would be if governments were investing and delivering more “social cohesion” (around whose values Governor?), an “inclusive economy” and so on.

In any sane environment it would have been to have significantly overstepped the mark, but Orr has done that so often – and worse, with all the misrepresentations and denials – with no consequences (no rebuke from the Board or minister(s), reappointment for a final term comfortably secured, tame board chair reappointed etc) that no doubt it will again pass with little notice.

It really was a pretty disgraceful, if again revealing, performance. But then the fact that Orr still holds office, and the incoming government – that used to rail against him and his style and the corporate bloat – has been content to see things just run on as usual, is just another sad reflection of the debased state of New Zealand public life and standards. One of many to be sure, but no less acceptable for that.

I had in mind another post for today, but this morning we had something rare: a speech about monetary policy from the Governor of the Reserve Bank, delivered in Washington at a think-tank which appears to have been hosting many speakers this week (in town for the IMF World Bank Annual Meetings). On their schedule, the Deputy Governor of the Banque de France was speaking earlier in the afternoon (some very interesting material in her presentation) and the Prime Minister of Liechtenstein a bit later.

The Governor’s wife writes fiction (several books published) and teaches creative writing. Entirely laudable and there are often powerful insights in great works of fiction. But when – as her husband does – fiction and sheer spin are dressed up as serious accounts of policy stewardship etc, the only possible insight is into the character of the chancer who tries it on. And perhaps those who enable him (one could think of Neil Quigley and Grant Robertson, but also now (sadly) of Nicola Willis).

But first a point to his credit. Climate change, for example, didn’t get mentioned even once in the speech. Or the treaty of Waitangi. It had the appearance of a straight up and down speech about monetary policy stewardship, as advertised (“Navigating monetary policy through the unknown”). And, if you recall how he used to tell people (well, Parliament actually) that the Russian invasion of Ukraine was to blame for the worst New Zealand inflation in decades that line has now been quietly minimised too.

Consistent with his revealed preference for fictional embellishments, Orr builds his speech around the navigational challenges faced by ancient mariners, in his case primarily Kupe. Orr claims to know that Kupe had a clear goal in mind, and whether he did or not, (I guess he could have used Captain Cook too) but – technology having moved on – he wasn’t reliant on the sea birds etc. It still seemed a rather strange analogy to use, in 2024, in an age of GPS. Then again, I guess it is only a couple of weeks since the HMNZS Manawanui ran onto the reef, so perhaps it isn’t such a bad analogy for New Zealand monetary policy after all. Perhaps the salvage will be done well, at considerable costs (perhaps lingering costs for the people of Samoa) but the ship never should have ended up on the reef in the first place. Those responsible for the loss of a ship face courts of inquiry, perhaps even a Court Martial.

But in Orr’s fictional world central bankers – New Zealand central bankers, since his speech does actually concentrate on New Zealand – are heroes, having delivered us to the least-bad possible outcomes through the storms, vicissitudes and other uncertainties of the last few years, where anything bad was no one’s responsibility, and anything good was to the credit of the wise and respected navigators, led by Orr himself. It was pretty breathtaking stuff really – although questionably persuasive even as fiction – as there is no longer even a hint that anything could have been done better, by our courageous central bank navigator, than it was. When the Bank reviewed its own performance a couple of years ago, they then thought it prudent to acknowledge the odd small error, even while claiming that none of it mattered much. But no longer apparently.

In his celebratory self-congratulatory mood – he claims to have saved us from two deep recessions – his overseas listeners would have had absolutely no idea that on the IMF forecasts that came out yesterday, New Zealand’s real per capita GDP growth in both 2024 and 2025 is estimated to be among the worst in the world, down there with places like Yemen and Haiti. Or that on those same IMF estimates, New Zealand will have been one of the very worst performers over the entire 2019 to 2025 period.

Now, to be fair to the Governor, one can’t blame underlying long-term productivity problems on the Reserve Bank, but equally no one really doubts that those 2024 and 2025 outcomes are mostly on monetary policy: the consequences of the Bank belatedly waking up to its past mistakes, and doing what it took to get inflation back down again. And, frankly (although the Governor won’t tell you this) anyone can get inflation back down: the trick (the reason we delegated the job to supposed experts) was never letting it get away on you (well, on us, the public) in the first place.

The spin, and utter avoidance of any responsibility, begins earlier, in fact with the Bank’s covering press release, which presumably captures the key lines Orr would like to see reported here.

First, there is this framing

Followed up in the speech with this extraordinary admission from someone charged with keeping inflation near 2 per cent.

Now, I don’t doubt that briefly in early 2020 perhaps the MPC really believed that the alternative to them acting as they did was economic disaster, but it was very quickly evident that that simply wasn’t the case. Economic indicators here rebounded quickly and early. And the MPC did nothing to start to pull back on the excessively loose monetary policy until late 2021 (it wasn’t until into 2022 that the nominal OCR was even lifted back to the immediate pre-Covid level by when inflation and inflation pressures were already running away on them): they now estimate the positive output gap was in excess of 3 per cent by late 2021. If we want to play with nautical analogies, Ulysses steered his way between Scylla and Charybdis. Orr and his team ran us onto the rocks (full blown inflation, fixed only at great cost). And he claims to have been now quite relaxed about those hugely and disruptive inflationary consequences, with all the attendant arbitrary redistributions.

And then, still with the press release, there is this

Inflation simply was not “caused by COVID-19”. With all their comms staff, this is very unlikely to be a slip of the pen, rather it is yet another in the endless series of attempts to avoid actual responsibility for doing the highly-paid job they took on so badly. No one doubts that Covid provided a context where many policymakers had to make difficult calls in conditions of great uncertainty. But it was the Reserve Bank MPC’s calls, faced with all that uncertainty and the decisions of others (since monetary policy moves last, by construction), that delivered the worst inflation in decades and the attendant cost and disruption to getting it down again. But Orr can’t or won’t admit that.

As the work fiction continues, there is no mention of the LSAP – just a couple of passing lines about how quantitative easing tools hadn’t been used in New Zealand before – or the $11 billion of losses the MPC’s choices imposed on the New Zealand taxpayer (as someone pointed out a couple of weeks ago, one could build three Dunedin hospitals for that price), and of course none of the way in which the Bank went on provided concessional lending to banks to the very end of 2022. No doubt, if challenged, Orr would bluster and repeat his utterly unsubstantiated claims that the LSAP made a big positive difference to New Zealanders, but on this occasion his fictional treatment just airbrushes it away.

I spluttered when I came to this paragraph

He chooses not to mention to his overseas audience (or to remind local readers) that his own reappointment was formally opposed by the two Opposition parties in Parliament at the time or that – as in many other countries – public discontent and inflation and the cost of living registered extremely high in opinion polls throughout, arguably playing a role in defeating the government here last year. It is hard to find anyone with any subject expertise who has any confidence in Orr (I’d mention Orr’s board, who seem to, but hardly any of them have any subject expertise).

(In case you are wondering quite what he meant, Orr’s idea of “mutiny” appears only to involve troublesome inflation expectations).

The creative writing continues as we move towards the end of the speech.

Has anyone ever associated Orr and his public communications with the word “humility”? Perhaps we might all take this as less like make-believe if it weren’t so well-documented just how many times Orr has actively misled Parliament’s Finance and Expenditure Committee (charged in part with holding him to account), or if he didn’t send out his chief economist to say “oh no, we didn’t really mean what the numbers say, and anyway it isn’t our fault but that of the tools”. Nothing, you see, is ever the fault of Orr and the MPC…..at least in this fairy tale.

It goes on.

I’m wondering how Martien Lubberink, Roger Partridge, Jenny Ruth or Nicola Willis (in her Opposition days) feel about their experiences of Orr as empathetic communicator? Disdainful bullying is probably a fairer characterisation of his style. And as for the rest of the MPC, all these supposedly-expert external members sat on the MPC right through this extreme period, and none of them ever said a word….no speeches, no serious interviews, no scrutiny by Parliament. Nothing.

Orr has the gall to then claim that it is really all in the minutes (the “Record of Meeting”) and that is only a shame that so few people, even “economic experts refer to or query” it. Which is, of course, nonsense on stilts, and just more active make believe. People read the Record of Meeting but they just don’t find much there. Despite all the uncertainties that Orr makes much of, there is never a serious sense of that in the Record of Meeting. Oh, they talk a good game, but when there is real uncertainty about important things, really able smart and engaged people will – with all goodwill – reach quite differing conclusions about where to next, and what the latest data probably mean. There is just none of that. The grapevine reports claim that there is in fact vigorous debate in the MPC, but there is not the slightest evidence of it shown to those us press-ganged into enduring the consequences of their bad calls. If the MPC really was unanimous on all but one call in the last five years, that is a very poor reflection indeed on the MPC members (some of whom are simply unfit for office, but from a couple one might have hoped for a bit more) and their chair. If not, the Record of Meeting is just comms spin.

I could go on, but will draw this to a close here. Somewhat remarkably – well, perhaps not in the fictional world Orr would prefer to draw for us – there is no mention of accountability. It was always supposed to be the price, the quid pro quo, for delegating a great deal of constrained power to central banks. Accountability was supposed to involve real consequences. And yet, through the biggest and most costly monetary policy misjudgements in decades, Orr would just prefer no one mentioned anything about accountability (or in fact about mistakes at all). I guess it is the New Zealand public sector way (as we seeing again now in the wake of revelations of obstruction and cover-ups in the context of decades of abuse of people in state care).

When captains of naval vessels made mistakes and ran their ship onto the rocks it was often considered fitting, and not inappropriate, for the captain to go down with his ship. But barefaced creative fiction, with not even a hint of contrition or regret to add nuance to the manuscript, seems to be Orr way.

Over the last few years, The Treasury seems to have been toying with bidding for a more significant role for fiscal policy as a countercyclical stabilisation tool It seemed to start when Covid hubris still held sway – didn’t we do well? – and the first we saw of it in public was at a Treasury/Reserve Bank conference in mid 2021, at which both the Secretary and some of her staff were advancing thoughts of that sort (I wrote about it here). More recently, this mentality has shown up in the commissioned report from US economist Claudia Sahm (post here) and in the consultation for The Treasury’s forthcoming long-term insights briefing (post here).

Last week they issued three papers in this vein (all carrying standard disclaimers that the views presented are not necessarily those of The Treasury itself, let alone the government).

The first one (long, and I haven’t read it yet) appears to be a fuller and final version of something presented at the 2021 conference. The second, quite short, is Sahm’s report (how much did the taxpayer pay for it?). The focus of this post is the third paper.

In the interests of full disclosure, the author is a former colleague and was my first substantive boss decades ago at the Reserve Bank. We have ongoing connections through the troubled Reserve Bank superannuation scheme, where Bruce has been a dogged campaigner for the trustees (appointments of most controlled by Orr/Quigley) to do the right thing, fixing some pretty egregious historical errors, and he was for a time a trustee himself. We have spent many many hours over the decades debating issues around macro stabilisation, in the 20+ years our Reserve Bank careers overlapped and since.

It is a 40 page paper covering multiple decades and so I’m not going to try to review the entire document, but rather to pick out a few themes that struck me, including revisiting my ongoing scepticism about Treasury (or Treasury staff/consultants) bids for a new and bigger role. Doing core fiscal policy, and associated analysis, seems quite challenging enough – and if ever that was in doubt the last couple of years should have brought it back into focus. Sticking to your knitting (and doing your own core job excellently) is typically good advice for government agencies.

Particularly if you are young, or haven’t followed New Zealand macro policy developments closely, there is useful background material in Bruce’s paper. It is easy for detail and institutional context to be lost as time passes, memories fade, (and embarrassing episodes – think the Monetary Conditions Index – are quietly swept under the carpet, the place the Reserve Bank would probably now like the LSAP losses to disappear to).

But I’m inclined to think that the paper is mis-titled. On my reading of things – and I was reasonably close to macro policy from the inside for much of the period – there was very little of what could properly be described as “fiscal – monetary coordination” over the last 35 years. That was mostly by design, and in my view was (and is) mostly a good thing. There have at times been tensions, but that isn’t necessarily a bad thing, but not usually much coordination. It generally hasn’t been needed. The approach was, and is, pretty standard among countries of our sort. So the paper is more of a retrospective on the parallel developments in each of fiscal and monetary policy, with some added thoughts on whether, and if so how, there might be room for more in future.

Contrary to one claim in White’s paper, active monetary policy isn’t new. But for a long time, in those countries that had central banks (we didn’t until 1934), interest rate (and related instrument) policy adjustments were mostly about defending exchange rate pegs (Gold Standard or simply fixed exchange rate choices). In the post-war decades fiscal policy sometimes played a part in that (think of prominent episodes like the 1958 “Black Budget” or adjustments following the wool price collapse in 1966), and through those decades in New Zealand both fiscal and monetary instruments were directly in the hands of the Minister of Finance.

Floating the exchange rate (in 1985) and making the Reserve Bank operationally independent in conducting monetary policy (formalised in law from 1 February 1990) opened the way for what we call the “consensus assignment” of tasks. The Reserve Bank would focus on delivering inflation at or around target, and in the process – and particularly in the presence of demand shocks – would do something towards leaning against big swings in real economic activity. And the Bank would be accountable for its stewardship. Fiscal policy would be made as transparent as reasonably possible (so that the Reserve Bank could properly take fiscal developments into account), but that fiscal policymakers (ministers) could concentrate on doing stuff voters expect with the public purse (schools, hospitals, Police, Defence, roads or whatever) while keeping debt to tolerable and sensible levels. There were, of course, the “automatic stabilisers” (mostly, the fact that taxes are proportional or progressive, and so government revenue shares some of the gains/losses when times are particularly buoyant or subdued) but they operated in the background, not overly strongly. Any macro stabilisation dimension was an incidental nice-to-have (eg we don’t pay unemployment benefits to try to keep GDP up, but because we don’t think people should simply be left to their own devices and whatever private charity can offer when times get (perhaps very) tough).

The separation was pragmatic and practical in the world New Zealand has chosen. People will rightly point out that fiscal choices can, in the extreme, end up dominating monetary policy (hyperinflations are always political – and fiscal – phenomena), but not when government debt as a share of GDP is in the sort of ranges it has been for (say) the last 80 years in New Zealand.

And so it has largely proceeded, really since the late 1980s (ie before the changes to the Reserve Bank Act or to the Public Finance Act (or what was initially a standalone Fiscal Responsibility Act). Sometimes the stance of fiscal policy has been working in the same direction (affecting demand) as monetary policy, and sometimes in opposite directions. Sometimes those similarities or differences have been helpful, sometimes not. But there really hasn’t been much co-ordination, in the sense of the Governor and the Minister of Finance getting together and agreeing which party (which policy) would do what when.

In his paper, White often conflates “working in the same direction” and “co-ordination”. He recognises that it is his definition, but I genuinely don’t find it helpful and, if anything, I think that usage muddies the water.

For example, if there is a really big earthquake at a time when the economy is badly overheated, you’d expect the aggregate effect of the resulting fiscal choices and pressures to be adding more to demand/activity but at the same time would expect that monetary policy would be acting to dampen overall demand (in practice, squeezing out some private sector spending/activity to make room for the post-earthquake repair and rebuild spending). That is a good example of both sets of policies doing what they do best, within a policy framework recognised by both the Minister (and her Treasury advisers) and the Governor (and his MPC colleagues). There is no particular for any further coordination because both parties know how things work. You might – as always – expect that Reserve Bank and Treasury officials would be exchanging notes (understanding respective models and analytical frameworks, and ensuring the RB is well aware of the fiscal plans, including timing) but the ground rules are clear.

And if the huge earthquake happened to come when there was a great deal of slack in the economy then we might have a very stimulatory fiscal policy (all that rebuild spend) but monetary policy might still need to be expansionary (just less so than otherwise). Policies now look like they are both working in the same direction, but in fact it is exactly the same framework – no more or less coordination – with the only difference being the (macro) starting point. I was bit surprised that in his account of how fiscal and monetary policy have operated over recent decades, including following shocks, there was little no reference to output gaps (or, less technically, to the starting point, whether of excess demand or excess capacity). It really matters: in 2007/08 for example the Bank’s best estimate was that economy had been badly overheated and thus contractionary monetary was required, whatever fiscal policy was doing, while by 2010/11 (earthquakes) economywide excess capacity was again a thing. But neither earthquakes nor pandemics (or foreign financial crises/downturns for that matter) can be counted on to conveniently time themselves to the state of the NZ business cycle.

White covers what is probably the closest example of fiscal-monetary coordination over the 30+ years he looks at.

It is good for governments to be conscious of where their fiscal choices might put pressure on monetary conditions but…..as both Brash and White note…..it often isn’t a particularly robust basis for making fiscal choices. Macro forecasting is notoriously challenging.

I don’t think the exercise has been repeated in quite that way. And perhaps, for various reasons, it is better not to. One could think of this year’s tax cuts for example. The government knew that, all else equal, tax cuts would put a bit pressure on demand and inflation but actually neither they, nor their Treasury advisers, nor the Reserve Bank knew whether by the time any cuts came that would be particularly problematic or not. And to, in effect, invite the Reserve Bank to exercise a yea/nay call on whether the political promise of tax cut proceeds seems to risk undesirably politicising the Bank.

White structures his discussion of history around four sets of shocks: the Asian crisis in 1997/98, the “global financial crisis” of 2008/09, the Christchurch earthquake(s), and the Covid pandemic.

I wasn’t fully sure how helpful this was. Discretionary countercyclical fiscal policy really didn’t play a material role in either of the first two episodes. In the late 00s, fiscal policy had moved into a quite expansionary mode but that had more to do with politics (Labour’s position was slipping, and large surpluses over many years had become an appetising opportunity for the Minister of Finance’s colleagues) and a rather belated – and, it turned out, erroneous change of heart by Treasury, which advised governments that revenue had moved sustainably high – than anything designed to be deliberately countercyclical. As it happened, fiscal policy was expansionary into the recession, but that was more by chance and poor forecasting than by design. Beyond the 2008 Budget, the Crown offered guarantees (for retail deposits and new wholesale bank funding), and that was an area in which the RB and Treasury worked closely together, but the overwhelming bulk of the macro policy discretionary adjustment was monetary policy. We ended up with one of the very largest cuts in our Tpolicy rate of any advanced economy (partly because our economy had been more overheated, and inflation more troublesome, than many other advanced economies).

Treasury officials (and advisers/consultants) seem more enamoured with the earthquake and pandemic stories. I don’t think either has much to offer in favour of more coordination. The series of earthquakes from September 2010 created fiscal obligations (legal and political), for spending that needed to happen over a succession of years. At the Reserve Bank, we knew that the earthquakes (especially from February 2011 on) represented a substantial positive shock (positive in a “pressure on resources” sense; serious earthquakes are themselves not positive events) over several years. It wouldn’t have made sense for the government to have tried to hold back the repair and reconstruction effort because there was going to be pressure on whole-economy resources; rather they got on and got things done, and the Reserve Bank was left to manage economywide pressures (and all the uncertainty around them) to keep overall inflation more or less in check. As per the earlier discussion, as it happened, the output gap was negative and the unemployment rate was high at the time, so the OCR stayed pretty low. But bad earthquakes can happen in badly overheated economies too.

What of the pandemic? Officials are – probably rightly – proud of the fact that they could roll out the wage subsidy scheme so quickly. They needed to. Their political masters had decreed that we all had to stay home for weeks on end – likely time initially unknown – and thus that many people would have no way of earning an income. The wage subsidy scheme was (largely) an income replacement scheme, with a leavening of “keep existing firms together as far as possible”. The point was not to maintain GDP, or to avoid people being (in economic substance) temporarily under or unemployed (not actually working) – the sort of traditional countercyclical stabilisation goals. If anything, the goal was to shut down a lot of the economy for a while, but to ensure not too much damage (including to individual ability to feed their kids and pay their mortgage) was done in the meantime. It was probably a worthy goal (certainly a politically necessary one) but it really does not have implications for countercyclical stabilisation policy. After all, if the pandemic had struck when the economy was grossly overheated (eg the 4.5% positive output gap the Bank now estimates for late 2022) no serious person would have said “oh never mind about a wage subsidy, it is a good chance to get inflation down”. Any more than we cut off unemployment benefits at the peaks of booms. They are instruments and tools for particular purposes (eg some sense of fairness), but those purposes just aren’t primarily countercyclical macro stabilisation. We have monetary policy to do that.

The pandemic is also a good example where the “both pulling in the same direction” approach to coordination is flawed. With hindsight it is pretty clear that the best policy mix in March/April 2020 would have been a stimulatory fiscal policy (the macro effects of the measures governments needed to take to assist the populace – notably the wage subsidy) and a contractionary monetary policy (a higher OCR). Again, that wouldn’t have been a case of policy being at odds, but of the framework working – governments being free to do what the circumstances demanded (and having the balance sheet capacity to do it), while not having to worry about what if anything it might mean for inflation because the Reserve Bank had that covered. (As it is, both the Reserve Bank and The Treasury misread the macro situation and what was really warranted from monetary policy, but that doesn’t change the conclusion. But just think if the Reserve Bank had done its job better – and been raising the OCR in mid 2020 – how much pressure they might have come under from the fiscal – political – authorities, had their been a more-formally coordinated model.)

You could imagine a half-respectable case being made back in 2019. Back then, the public finances were in reasonable shape and (after far too long) inflation was also back to around target. If someone had been doing a scenario exercise around a pandemic it would have been easy to talk about fiscal policy: yes, we can do something quickly (timely), temporary and targeted. And, as noted earlier, on the narrow issue of the wage subsidy they did. But what happened to fiscal policy subsequently? It was thrown badly of course, and we now sit here in 2024 – having come thru post-Covid booms and busts still with not the slightest idea as to when the operating balance might be returned to surplus. There was a decent case for some big fiscal outlays in 2020 and 2021, but…..we are years on now, and nothing of the fiscal predicament is directly caused by Covid. But the legacy is still problematic, and the record suggests that Treasury advice was (to put it mildly) not always helpful in that regard. Officials don’t seem to have been focused on the basics – getting back to balance. As a matter of realpolitik it is simply much more difficult to change track on fiscal policy than it is on monetary policy. The Reserve Bank did badly over recent years, but by late 2022 monetary policy was on a contractionary footing and inflation has now largely been beaten. As for fiscal policy, this year’s Budget was still expansionary and no one knows when we might next see a surplus. How much riskier if we were to empower ministers and officials to use fiscal policy more routinely for countercyclical purposes (in reality, almost inevitably, much more enthusiastically to boost demand than to restrain it)? The temptation should be resisted by officials, not encouraged.

If there hasn’t been much fiscal and monetary policy coordination over the years, that doesn’t mean there haven’t been tensions between them, and between ministers and the Bank. It also doesn’t mean there haven’t been times when reasonable people have argued that a different fiscal policy might help ease some of the burden on monetary policy and monetary conditions. Decades ago, before the RB become legally operationallly independent, I ran a small policy team that wrote a monthly memo to the Minister of Finance on monetary policy and conditions: every single one of them ended with what became almost a ritual incantation that faster progress in reducing the fiscal deficit would ease pressure on monetary policy. I doubt our view ever made much difference – it was hard enough to get the deficit down just focused on fiscal issues and associated political constraints.

White notes that one of the big presenting issues over the years was the exchange rate. Intense upward pressure on the exchange rate would reawaken these issues: all else equal, a tighter fiscal stance would mean slightly lower interest rates and less pressure on the real exchange rate. It was an issue for decades, until it wasn’t. One of the little appreciated aspects of the last decade or more is how much less volatile our real exchange rate has been than it was in the period from 1985 to about 2010 (for reasons that I don’t think are that well understood by anyone).

The last such period of angst was in about 2010. After the recession the exchange rate rebounded very strongly, and there was quite a sense of “oh no, here we go again”, including among senior ministers. At about that time, then private citizen Graeme Wheeler encouraged the government to move faster on fiscal consolidation, to take pressure off the exchange rate, citing experiences from 1990/91. It came to nothing much, but did prompt me to write a paper for my colleagues on that earlier experience. After I left the Bank I OIAed that document and wrote about it here.

Over the years, there was angst on both sides of the street. Don Brash was well known (to his colleagues and others) for his hankering for “tweaky tools” – things that might ease the exchange rate pressures. After his departure, Michael Cullen became increasingly exercised about the exchange rate implication of our tightenings in the mid 00s, to the point where we and Treasury were commissioned to provide a joint report on Supplementary Stabilisation Instruments, and then a follow-up report on a scheme for a Mortgage Interest Levy (taxing mortgages to keep down the extent of OCR adjustment). I wrote about that episode in a post on Cullen’s autobiography. Very late in his term, Cullen became quite vocal – even talking of overriding the RB – and in particular was exercised by our public view that expansionary fiscal policy was exacerbating pressures on interest and exchange rates (his claim was that this could not be so since the budget was still in surplus, but it is changes in balances not the levels of them that matter for these purposes). An open clash of view culminated in a two page box in the December 2007 MPS, articulating our approach to these issues.

The established framework does rest partly on the willingness of the Reserve Bank to identify honestly fiscal pressures as they arise. A couple of decades ago The Treasury developed the fiscal impulse measure specifically for the Reserve Bank, to help provide a common framework. Over the last 18 months there have been signs of considerable slippage. I wrote last year about how the Bank had suddenly stopped referring to overall fiscal balance measures and fiscal impulse type indicators, and had switched to focusing on just one part of the overall fiscal mix, the level of real government consumption and investment spending. OIAs revealed, unsurprisingly, no serious analytical basis for such a switch, and the most likely story seemed routed in opportunism: government spending was projected to fall as a share of GDP (including from Covid peaks), which distracted attention from the fact that last year’s Budget was really quite expansionary (as the IMF pointed out in public even as the Reserve Bank refused to) and this year’s was also modestly expansionary. Those are political choices open to the politicians, and we shouldn’t expect the Reserve Bank to make a song and dance about them (whether the budget is in surplus or deficit) but we should expect some honest, balanced, and calm analysis of fiscal pressures on demand (as for any source of pressure). We aren’t getting it at present.

This has ended up being a long post and only partly focused on the White paper. My view remains pretty strongly that both the Reserve Bank and the Minister/Treasury should continue to specialise; that countercyclical macro stabilisation is best assigned to the Reserve Bank (for various reasons, notably around reversibility, but illuminated by the dubious record of the last 2-3 years), and with the Reserve Bank held to account for its performance in that role. One of the developments of the last half dozen years was the addition of a Treasury observer (formally the Secretary but usually a deputy) on the MPC, as a non- voting member. I championed such a move and welcomed the change that Grant Robertson introduced. That said, I have been struck over the years by the lack of any evidence in the record of MPC meetings that the Treasury observer or the Treasury presence has made any difference (positive or negative) whatever. Perhaps that is just about how the record is written, but perhaps not either. And yet the presence of senior Treasury officials in the MPC meetings must, at the margin, fix them with some sense of ownership for the resulting policy, and in turn impede their willingness and ability to ask hard questions of the Bank – when things turn out poorly, as they have in recent years – and to be part of supporting the Minister of Finance in holding the Bank to account.

Tantalising as it might be to Treasury officials to be more active in the countercyclical space, it isn’t a good idea. They have quite enough to do in just sticking to their knitting and doing that excellently.

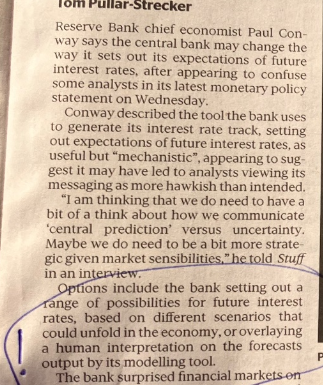

There is a lot one could write about the Reserve Bank’s Monetary Policy Statement and the Governor’s (sadly all-too-typical) thin-skinned and defensive responses to questions since, whether from journalists or a lone MP at the Finance and Expenditure Committee this morning. He never ever acknowledges a mistake and seems utterly unable to cope with criticism or disagreement whether (as reports suggests) inside the Bank or (as we can all see) outside it. In a field where there is inevitably huge uncertainty, it renders him simply unfit for office. It remains appalling that Grant Robertson reappointed the Governor and that Nicola Willis just reappointed the chair of the board responsible for holding Orr to account and for having recommended – presumably captive to management – his reappointment. How much more honest – and frankly reassuring – had Orr simply stood up yesterday and noted ruefully that “perhaps our May MPS wasn’t one of our better efforts”. At least in my book, a bit of contrition and humility goes a long way.

While I want to focus on yesterday’s statement, the contrast with May, and the outlook from here, it is worth remembering that simply unacceptable as the huge flip-flop from May to July/August should be – the sort of episode that further undermines whatever respect the Reserve Bank, the MPC, and Orr himself, might command – in macroeconomic terms it matters much less than the really big mistakes from a few years back that still get far too little scrutiny, and for which there has been no accountability. Losing $11 billion of taxpayers’ money on an ill-considered huge punt in the bond market remains simply staggering. How much difference would $11bn make in, eg, our hard-pressed health sector? And then there was the small matter of the worst outbreak of core inflation in many decades, the most overheated economy in the advanced world, and the massive dislocations and redistributions that that glaring policy failure brought about. And if many other central banks made mistakes in similar directions (a) we can only hold our central bank to account (other central banks are the problem for their citizens/governments) and b) our central bank did a worse job than most (see “most overheated economy in the advanced world”). If you take the pay, prestige, and the power, there should be some serious accountability. There has been none. But to get back to the MPS.

Sometimes small things make you proud of your kids. My son is an honours student in economics, with a keen interest in monetary policy and macro. Within minutes of the release yesterday he’d spotted this and pointed it out to me

Does it matter? Not in substance of course (and if you check now, they have fixed it), but it seemed revealing of an institution that struggles to even get the basics consistently right. Excellent it is not.

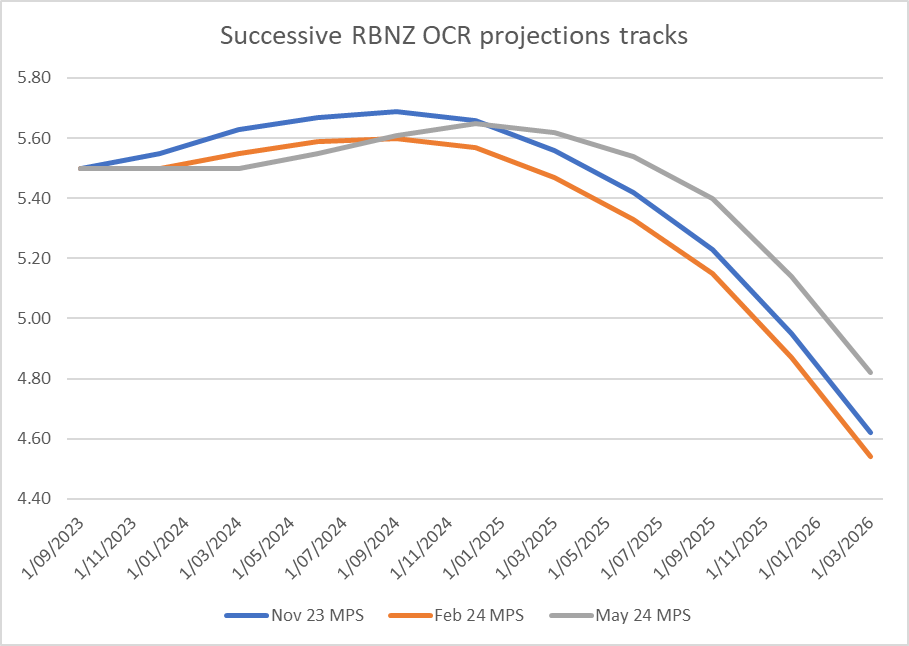

That there was a huge shift from May to August isn’t really in doubt. Here are the two OCR tracks

There has been no nasty external shock in that time (global financial crisis, pandemic, collapse in commodity prices etc) but we’ve gone from a “hawkish hold” (best guess, no easing until this time next year, and possibly some tightening late this year) to not only an OCR cut now, but a really large (at peak 130 basis points) change in the projected forward track for the OCR. I can’t recall another change that large that quickly, in the absence of a major external shock, in the 27 years since the Bank started publishing these forward tracks. It was simply because Orr and the MPC badly misread how the economy was unfolding now (Orr himself made this point yesterday, when he noted that the change of stance wasn’t about the medium-term outlook, but about partial data etc about where the economy is right now.) Other commentators have used the label “U-turn”. I prefer flip-flop myself (and in reality that change wasn’t even from May to August, but was largely between May and the July OCR review just six weeks later). Getting the medium-term right is a challenge for everyone, but an MPC – delegated so much power, allegedly as technical experts – simply should not get the near-term so wrong. And its communications should be a lot of more assured and authoritative than they are (eg recall the chief economist in May attempting to blame his tools). Instead we have a central bank and MPC that no one has any confidence in or respect for – be it local observers or international markets. They wield the power of course (they still set the rates) but no one serious looks to them as an authoritative guide or interpreter, despite all the budget and analytical resource at their disposal.

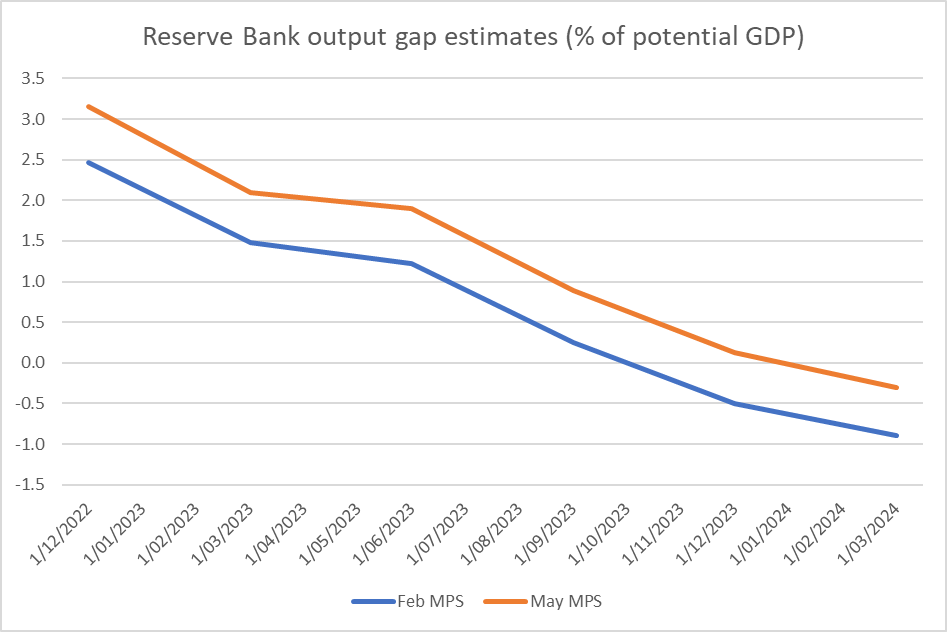

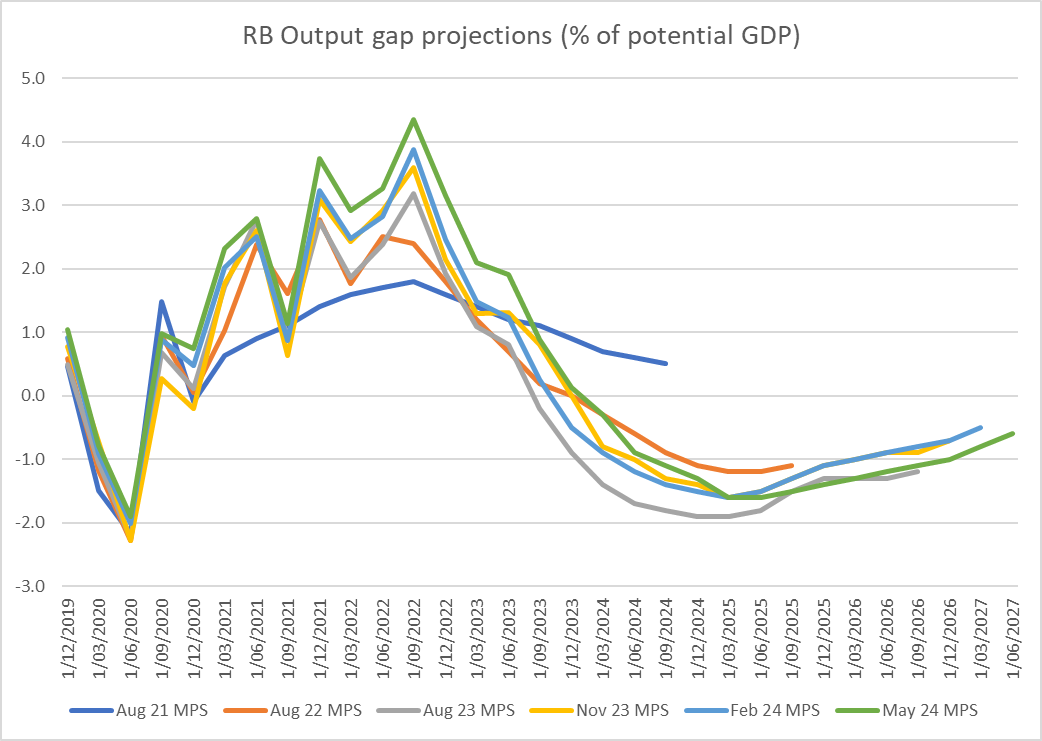

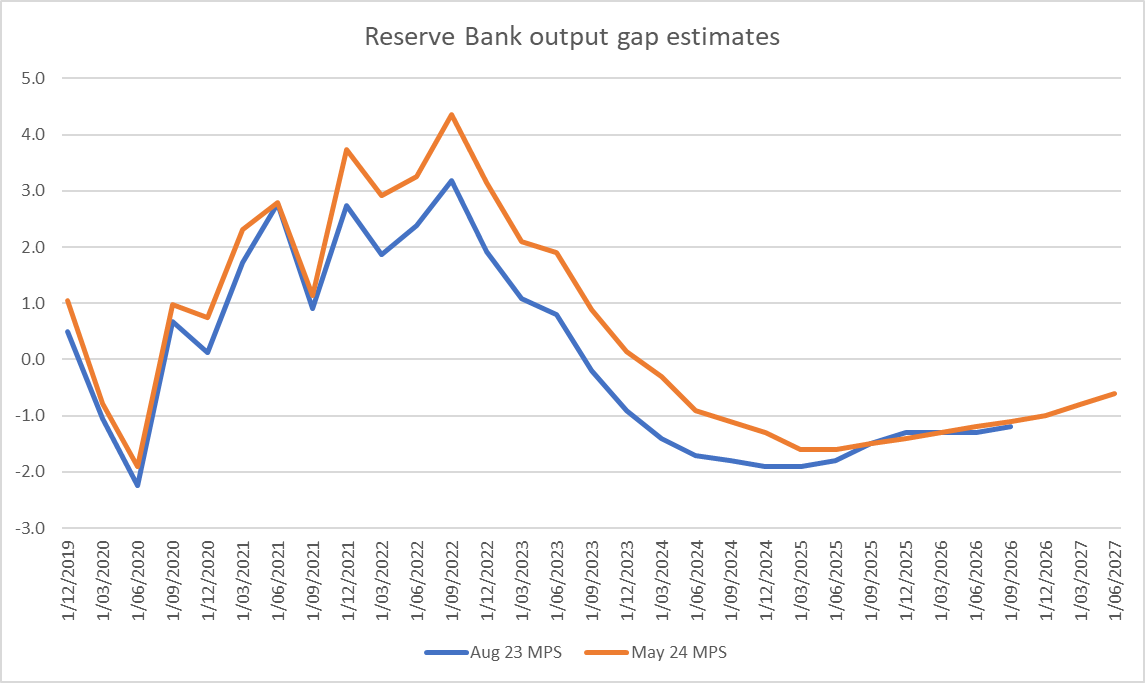

What about some of the numbers? I’ve been banging on for a while about how IMF estimates suggested that New Zealand’s economy was the most overheated of any of the advanced economies in 2022. The Reserve Bank has largely avoided until now any such comparisons, so it was interesting to see this chart

accompanied by the explicit comment that “New Zealand’s output gap reached a higher level than other countries in our sample [wider than those shown in the chart] during the COIVD-19 pandemic, indicating higher capacity pressures relative to our sample countries.” As it happens, in this set of forecasts they revised further upwards the extent of that peak excess demand (“output gap”) – a really damning commentary on MPC’s stewardship a few years back.

Right now (September quarter) the Reserve Bank estimates that the output gap is about -1.8 per cent of GDP. That number will inevitably be revised, but it represents the MPC’s best guess of where we are now. There is a lot of slack in the economy (or so they think). And it is unusual for the easing phase to start when the MPC believe that so much excess capacity has already built up. The Bank hasn’t always published real-time quarterly output gap estimates, but I cannot think of a time when the first easing would have come so late (eg the first easing in 2008, in July, appears to have been when we thought the output gap was about zero, the easings in 2015 were against the backdrop of a zero output gap, and there was no negative output gap when the easing came in 2019).

The fact that the first easing is late, relative to real-time output gap estimates, is not itself a criticism. There had been a huge inflation shock, that wasn’t overly well understood, and anyone in the Reserve Bank’s shoes might understandably have been a little cautious. My concern is less on how we got here (there isn’t much point quibbling now as to whether – as I thought – the OCR should have been cut in July rather than August) but on where to from here.

In my commentary after the May MPS I included this chart and comment

Quite how was growth expected to rebound was a complete mystery then.

And although the Bank has pulled down its estimates of growth for the rest of this year, in their dramatic change in OCR track, the same puzzle remains.

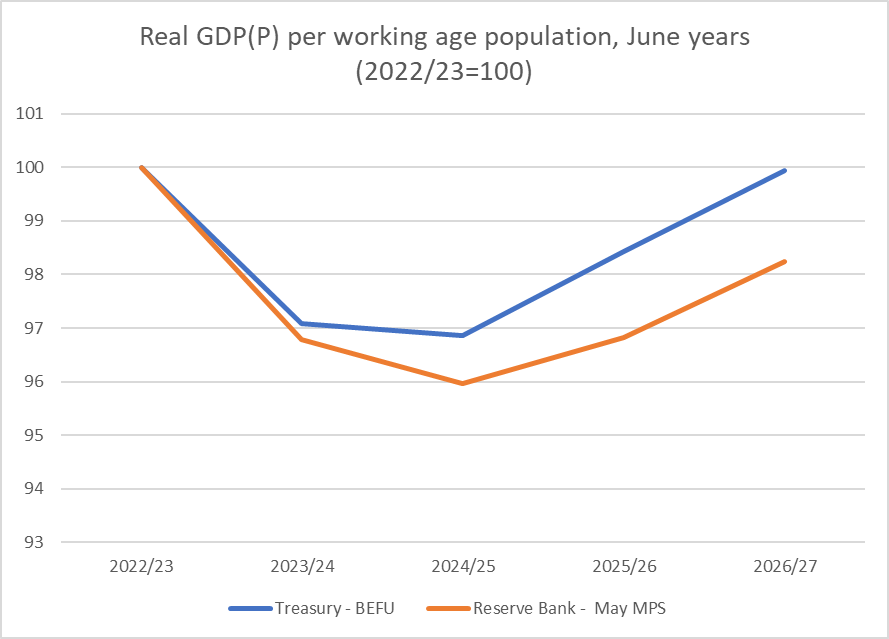

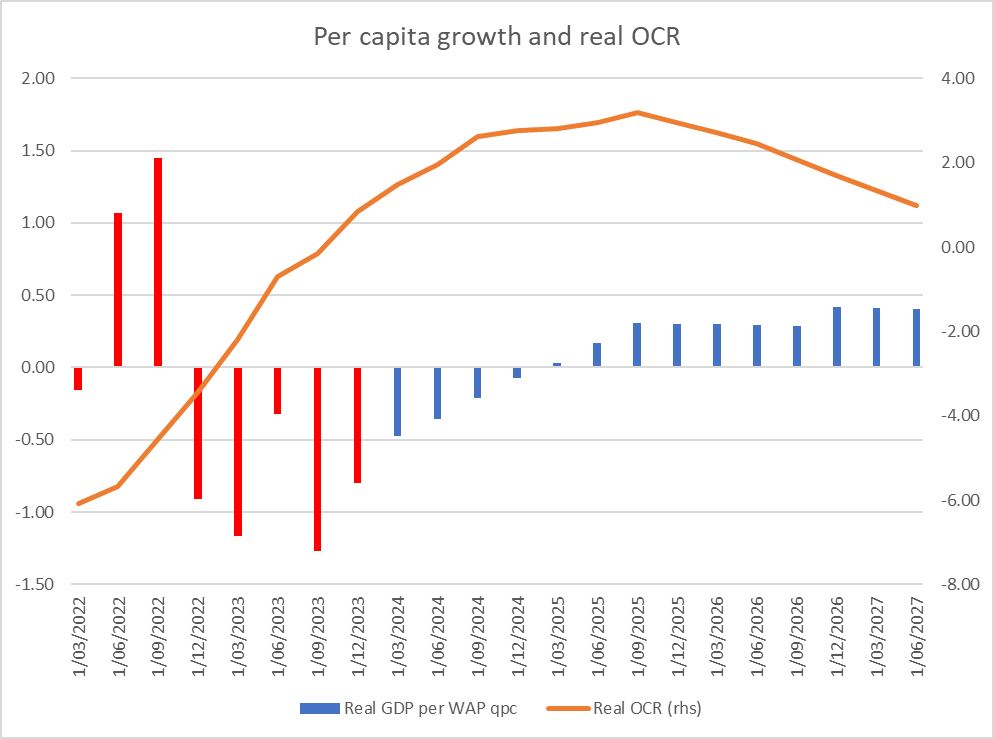

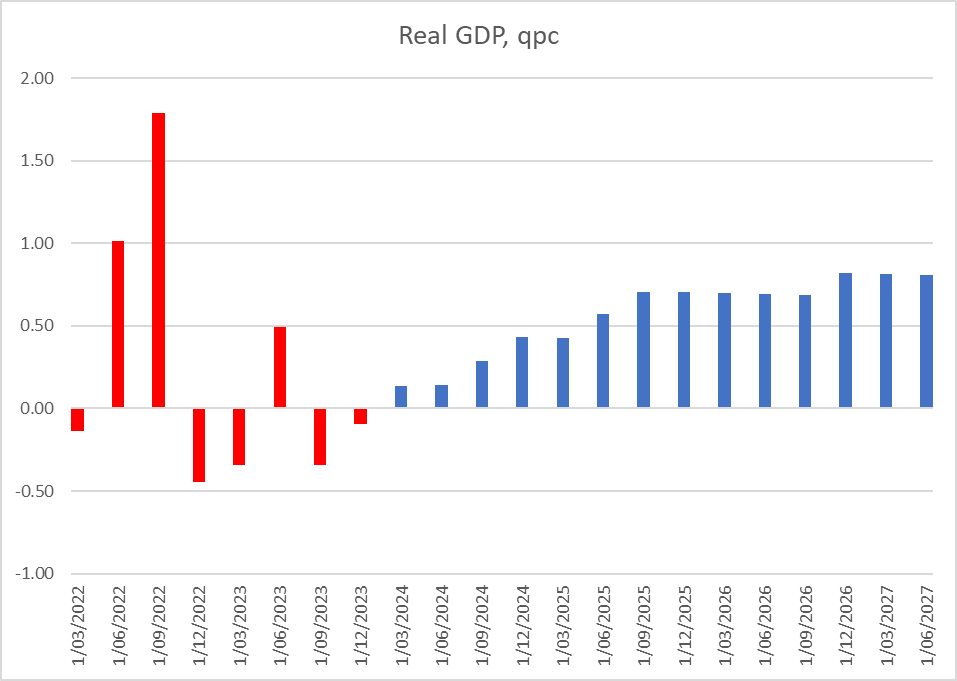

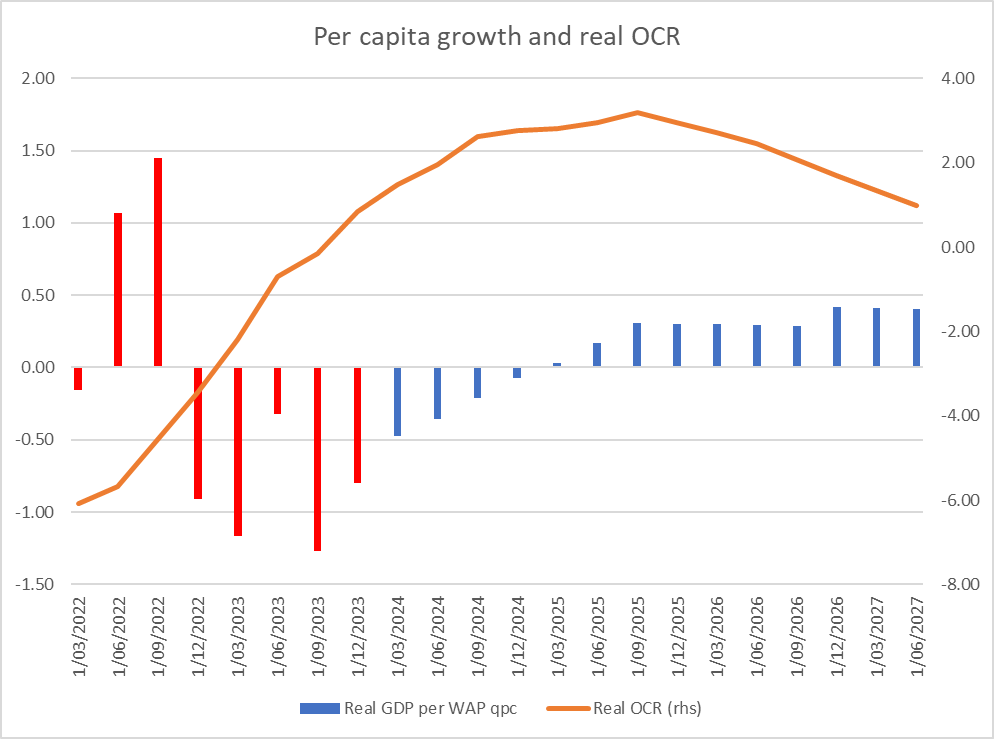

Here is growth in real GDP per working age population from yesterday’s MPS (red, SNZ data, green remaining 2024 quarters, and blue beyond that)

After two years of really lousy GDP growth (sadly, needed to get inflation securely down), the Reserve Bank expects that everything on the growth front will be back to normal from the March quarter of next year. Those projected growth rates are above the Bank’s own estimates of potential GDP growth, and so the output gap is projected to close gradually.

But how? On their assumptions, the world economy remains pretty subdued, net immigration settles to a fairly low level not doing anything much to growth, reflecting the government’s numbers fiscal policy (after being slightly expansionary this year) is expected to be quite contractionary for the couple of years beyond that. Whatever useful micro reforms the government is doing don’t look large enough to make a material difference, and aren’t something cited by the Bank.

Ah, but perhaps you are thinking, monetary policy must be the answer. After all, the OCR has been cut and is projected to be cut quite a bit more over the next couple of years.

But that can’t be the answer either, because the Governor was quite explicit in his press conference yesterday that the OCR remains at or above their estimate of neutral throughout the entire forecast period (several years ahead). Easing the OCR might reduce the extent of downward pressure – and recall that the lags mean that economic activity well into next year will already be being dragged down by policy as it stood until yesterday – but it isn’t going to generate anything like above-potential growth rates. Absent other shocks (which the Bank doesn’t forecast) and by construction (the Bank’s own articulated model) you get that sort of stimulus only when the OCR is taken somewhat below neutral. (Note that as inflation expectations are likely to carry on falling as headline inflation gets back to near 2 per cent, real interest rates may still be flat or rising even when the nominal OCR is being cut).

Look back at the output gap estimates since 2000 (the period the Bank publishes for) – or even back to the 1990s – and you simply do not find a time when a negative output had emerged when it has been closed again without the OCR being taken below best estimates of neutral. It was so in the early 1990s, it was so around 2001, it was so (for far too long) after 2008, a period which encompassed the 2015/16 easings. There is simply no reason to think the economy is operating any differently now (and again the Bank has often recent years repeatedly reaffirmed that it thinks transmission mechanisms are operating normally). The economy has been taken into a hole – to get inflation down again – and to get out of the hole anything other than very very slowly needs some external intervention. That is what active discretionary monetary policy does.

And that is why, as I’ve said a few times over the last 24 hours, I wouldn’t be surprised if a year from now the OCR was 2.5 per cent, or perhaps even lower. In fact, I will be a bit bolder and say that I will surprised if it is not that low. People have looked/sounded puzzled when I’ve said it, but the logic – of the Bank’s own frameworks and projections – seems pretty clear. I don’t think it is a big call at all. On the Reserve Bank’s own numbers, the best guess of the longer-term term neutral OCR is 2.8 per cent. No one knows what the neutral OCR is with any precision whatever – it really only be revealed over time, after the event – but I don’t see any reason why, give or take say 0.5 percentage points, the Bank’s estimate should be so very wrong. My own guess is probably a bit lower, but stick with theirs for now: if neutral is 2.8 per cent then even an OCR of 2.5 per cent by this time next year is (a) barely stimulatory, and b) will have to be dealing with more disinflationary pressure that will have built up between now and then as in the meantime the OCR has been above neutral.

Frankly, it shouldn’t be a terribly controversial view (and market pricing is already well below the Bank’s projected path). Of course, there are risks to both sides, and almost inevitably some shocks (positive or negative) will change the outlook between now and then, but the simple point remains that if you run monetary policy in a highly contractionary way to get a nasty bout of inflation back down again, and in the process generate a big negative output gap, a period of stimulatory policy is likely to be required to settle back on a more normal path. On RB numbers that would mean 2.5 per cent or below, and before too long.

I’m not a big fan of central banks publishing medium-term macro forecasts – about the largely unknowable future – but when they choose to, they really should follow through on the logic of their own mental models. A significant rebound in economic growth from the start of next year simply doesn’t seem consistent – with all their other assumptions – with continued materially contractionary monetary policy settings. Stick with those settings and the recession is only even more likely to deepen.

(And finally, but fairly briefly as this post has gone long enough, could the Reserve Bank please stop playing games around fiscal policy. As I highlighted last year, they had then shifted to focusing on government consumption and investment spending, rather than deficit measures, seemingly to avoid putting any heat on the then government. They aren’t much better now. Most macroeconomic analysis around fiscal policy, here and abroad, uses measures like the cyclically-adjusted or structural balance estimates that The Treasury and the IMF/OECD produce. Those measures exist precisely to aid assessments of the impact of discretionary fiscal choices on demand, activity, and inflation pressures. On the Treasury Budget estimates, this year’s Budget means the cyclically-adjusted deficit in 24/25 is slightly larger than the estimated deficit for 23/24. It isn’t the Reserve Bank’s place normally to weigh in on what should or shouldn’t be done with fiscal policy, but they should be consistently straightforward and honest about the impact of the fiscal choices any government makes. That simply hasn’t been happening last year or this. It may be convenient for MPC members, but serving their convenience is not either our concern or their job.)

UPDATE: Finally, finally…..monetary policy (OCR) cycles, whether in New Zealand or the US, have tended to involve swings in policy rates of 500 basis points (on average, albeit with variance). We had a 525 basis point rise to deal with the inflation outbreak. We shouldn’t be at all surprised if most of that proves not something that needs to be sustained. Big lifts in policy rates are almost always followed by big cuts, and when those cuts come they usually come much more quickly than forecasters – public or private – had allowed for.

Since taking office, the new government has replaced quite a number of chairs of government entities. I’m sure there are many others but NZTA, Health NZ, Pharmac, and the FMA are just the examples that spring to mind. It isn’t uncommon for such changes to be made, and in many government entities board members can be replaced at will by the government of the day.

It isn’t so for the Reserve Bank. Mostly, board members (including the chair) can only be replaced at the end of their terms. This is consistent with notions of the operational independence of the Reserve Bank, and much the same provisions apply to MPC members.

Two years ago the overhauled Reserve Bank Act came fully into effect and with it came a new Board. If the previous government appointed people who mostly simply weren’t fit for the responsibilities they were taking on (I compared them in an earlier post to a slightly overqualified board of trustees for a high decile high school), and in several cases had question marks around them, at least the terms of the appointees were staggered so that if there was a change of government there would in reasonable time be an opportunity for change. In fact, they left one possible position unfilled (the Board can have between 5 and 9 members). Perhaps most importantly, the previous chair Neil Quigley was given only a two year term (ending on 30 June 2024), much shorter than would normally be desirable but in what was clearly intended as a transitional appointment, smoothing the way with (a) a new Act, and (b) a large and simultaneous crop of new Board members.

As a reminder, the Reserve Bank’s Board is a very powerful body. They hold all the powers of the Reserve Bank other than those statutorily assigned to the Monetary Policy Committee. That means not just the corporate aspects (that the published Board minutes suggest they relish most), but all the prudential regulatory policy and supervisory powers, and most of the issues around the Reserve Bank’s large balance sheet. It also means that the Board has the primary responsibility for recommending the appointment of the Governor and of the external MPC members, and the responsibility for holding to account and overseeing the Monetary Policy Committee. These are very substantial powers, and in some cases at least seem to be taken very seriously (for example I noticed in a recent set of published Board minutes that a Board member had actually been presenting to the Board the paper on a set of proposed regulatory policy changes – which seems, frankly, quite unusual, but their choice I guess).

It is no secret that things have not gone well at the Reserve Bank in recent years.

And yet late last week this announcement appeared from the Minister of Finance

Even among those with low expectations of the current Minister of Finance, it was pretty astonishing news. It isn’t really possible to get rid of the Governor – unless he had been inclined to do the honourable thing, including accepting responsibility for the macro mess, and resign – but the Board chair’s term expired just six months after the new government took office. Of the three parties in the government, the two who had been in Parliament last term – ACT and National – had both objected to Orr’s reappointment when, as his new law required, Grant Robertson had consulted them. And it was the Board, led by Quigley, that was responsible for choosing to recommend Orr. The Finance spokesman for one of the parties (ACT) had been out in public, on ACT’s official accounts, just a few weeks ago attacking Orr

And who is responsible for the Governor’s performance monitoring and accountability? Why, that would be the board, with typically a leading role played by the Board chair.

But never mind says Nicola Willis (presumably with the endorsement of the entire Cabinet), let’s give Neil yet another two years. Either the government thinks things at the Reserve Bank are going swimmingly or (much more likely) they just don’t care. That would be consistent with there being no sign of any change to how the MPC is supposed to work (eg requiring more openness and accountability), no sign yet of any Letter of Expectation from the new minister to the Bank signalling any sort of difference of direction/emphasis, and no sign at all of pressure on the Bank to voluntarily join in cutting its (bloated) expenditure authorised by the previous government, in an agreement that has another year to run.

It isn’t obvious that there would have been any political price at all if they had chosen to replace Quigley. It was widely expected. It was the end of his term. And so on.

And there are numerous reasons why this reappointment is bad.

One of them is that, no matter how good a person is, sixteen years on a single board is just too long (Quigley was first appointed in 2010). He has already been chair for eight years (the typical limit, for example, on government department chief executives in a single role). Even the Reserve Bank Act recognises this sort of issue: the Governor, for example, simply can’t be reappointed when his current term expires in 2028, and the same went for the external Monetary Policy Committee members who are turning over this year and next. And what of Board members?

Presumably Quigley’s time on the Board prior to 2022 doesn’t count formally against this constraint, but…..sixteen years (even as the Board’s role has changed over time) is simply too long (as is 10 years as chair, again almost no matter how good you are).

Then there is the Reserve Bank that he has presided over for the past eight years, as the power and responsibility of the Board was substantially increased. That is the Bank that has delivered as follows:

the worst outbreak in inflation in modern times, including first the most overheated economy among OECD central banks, and now a wrenching dislocation – including deep falls in per capita GDP – to get inflation back under control,

losses of around $11.5 billion dollars on the utterly unnecessary Large Scale Asset Purchase (LSAP) programme, with no material offsets or benefits to show for this rather reckless gamble,

the sharp decline in the volume and quality of published Reserve Bank research and analysis (Treasury is hardly a research powerhouse but is now clearly better than the RB),

the near-complete absence of any sort of serious speech programme from powerful senior decisionmakers,

the blackball placed by the Board/Bank on the appointment to the MPC in its first five years of anyone with actual or future research expertise/activity in macroeconomics or monetary policy (a policy so beyond comprehension that the documents show that not even Treasury officials in the macro area understood it)

the absence of robust cost-benefit analysis for the increasingly intrusive range of prudential controls the Bank has put in place,

the evident loss of focus on core functions, in favour of the personal ideological preferences of management (and perhaps the Board),

the appointment of a deputy chief executive with specific responsibility for monetary policy and macroeconomics with no background in the subjects and no evident expertise (pretty much unprecedented these days),

a Governor who has repeatedly lied to or actively misled Parliament (eg here, here, here, and here),

and so on.

Many of these things were the direct responsibility of the Governor and/or the Monetary Policy Committee, and it is pretty appalling that Orr himself was reappointed but (a) the Board is responsible for overseeing and holding to account the holders of these offices, and b) the Board recommended the appointment or reappointment of each of these people (the Governor himself, external MPC members to the limits the law allowed, and the utterly ill-qualified DCE who could not have been appointed to an MPC role without the Board’s imprimatur). There is also no sign that the Governor is any more willing or able to engage in a constructive manner or tolerate dissent, disagreement, or criticism than ever. He plays distraction, he plays the man. He simply isn’t a figure of gravitas commanding general respect. And he is Quigley’s responsibility.

“Public sector accountability” has increasingly become a sick joke, but Orr and Quigley are perhaps the New Zealand epitome of that. Accountability – serious practical accountability, with consequences – was supposed to be price of power and independence. Mess up really really badly and under this government (and the last) you don’t even get politely sent on your way when your term is up. This government couldn’t do much about Orr now, but they could have replaced Quigley and simply chose not to do so.

As to why, who knows? Well, the Minister presumably does but she isn’t saying (and apparently no journalists are asking). Her statement talks of two things. The first is “retaining his leadership and experience in central banking and monetary policy”, which can’t really be said with a straight face when one looks at the Reserve Bank’s recent record as a central bank (and Quigley has no direct involvement in monetary policy). The second is that his reappointment ensures the Board “is well positioned to take om new members”. Which might have been a half-plausible line in 2022, with five new members in a single day (and a new Act and responsibilities) but is a rather desperate claim now…..especially when the Minister – in office for six months already – has made no effort to fill the two possible vacancies that are there (one of long standing, the other arising 2-3 months ago when an existing director left for another government appointment), and there is an established cohort of existing directors carrying on.

The best explanation is that she simply didn’t care.

(The more hardbitten cynics might recall Quigley’s cosy relationship with the National Party over his university’s bid for a medical school (“a present for the start of your second term”), but Quigley is more of an opportunist, working whatever angles or sides benefit him, rather than some National hack – he was, after all, confirmed as chair previously by the Labour government.)

I have wondered if one possibility is that the government has someone in mind who might be suitable as chair but is either not yet ready or not yet available. Looking at the Board page I spotted this

“Future directors” are quite the thing in the public sector these days, and as this text says Grant Robertson encouraged the Board to appoint one. But they only got round to doing so on 1 June. Vermeulen, who seems to be Belgian, was a researcher at the ECB for a long time, switching to academe and relocating to New Zealand just a few years ago. He looks as though he could be a credible contender for some role in or around the Bank (possibly an MPC position, when another vacancy arises next year), perhaps even an effective Board member or even, one day, chair. It seems like a fairly unambiguously good appointment on the face of it. But then with actual Board vacancies outstanding, if this was anything like the backstory why wasn’t he just appointed straight onto the Board? If he doesn’t seem to have any much governance background, he looks no worse qualified overall than several existing Board members, and at least (unlike most of them) has some subject knowledge and expertise. So the more I think about it, the less likely my charitable explanation seems.

It is true, as the minister said, that a couple of other (underqualified) board members’ terms expire next June, but that shouldn’t have impeded replacing Quigley now – if anything it should have helped impel change at the top starting now. If Willis and her colleagues cared.

Finally, a reminder that Quigley hardly exemplifies the qualities one should be looking for in a chair of a powerful and prominent government agency, that needs to command widespread respect – not just as non-partisan, but as highly capable, honourable, and marked by the utmost standards of integrity – in return for the huge degree of influence (for good, but often for ill) that the public and Parliament grants to the Bank. The Board’s role in such an entity is to act as agent for the public, upholding all the standards citizens might reasonably expect, not to simply have the back of management and the bureaucratic institution.

Quigley can on occasion talk a good talk. But there is little evidence that he walks the talk or insists on it from the Governor or management.

On institutional capability for example, he was clearly primarily responsible for the extraordinary blackball put in place, preventing active experts from being appointed as external MPC members (a call all the more extraordinary when none of the internals were really expert either). Astonishingly, OIAed documents (finally obtained recently, when they should have been released in response to a 2019 request – now subject to an appeal to the Ombudsman) show that Quigley himself had been keen on stocking the MPC with, all things, lawyers – for a function that had almost no regulatory dimensions.

As to integrity, a series of OIAed documents last year (eg here ) show that Quigley actively asserted to The Treasury that there had never been such a blackball – this the person who himself in 2018 told an academic of my acquaintance that that person would not be considered for exactly that reason (research active in the broad subject area). And then last year – when MPC positions were being advertised again and question about the blackball were being asked – together with The Treasury he tried to suggest it was all a misunderstanding, the responsibility of some midlevel Treasury manager who had somehow misunderstood everything (and by 2023 was no longer at Treasury so was no longer in a position to push back), prompting Treasury and the then Minister to repeat his simple falsehood in public statements to the media. It was pretty despicable behaviour – against a backdrop of public comment from the then Minister, the Minister’s then economic adviser, and the Bank itself (in 2019 and 2022) defending exactly the blackball Quigley now denies ever existing. Just possibly by last year, Quigley – a busy man – had ended up confusing a couple of different things (real conflicts of interest were a genuine concern for the Board in selecting MPC members), but he made no effort to clarify the situation or acknowledge any mistake. Note that one of the other Board members from 2018/19, actively involved in the selection proceess, went on record to the Herald to (a) disagree with Quigley, b) wonder why Quigley didn’t just act to clarify things, and also, as I understand, to indicate to the Herald that they had accurately reported him.

These simply aren’t the actions of an honourable man, with any sort of commitment to the openness and transparency the Bank prefers to prattle on about rather than to practice.

On integrity, I found this line from Quigley himself in an email from 2018 (around the MPC selection process): “the Reserve Bank can never be in the situation that the integrity of its senior decision-makers could be called into question by other roles”.

Again, fine words and no one is going to disagree. But Quigley simply doesn’t walk the talk. He was active in the selection of Rodger Finlay for, first, the “transitional Board” and then the full new Board of the Reserve Bank in 2021/22 at a time when Finlay was the chair of the board of the majority shareholder in the fifth largest bank in the country. It was simply extraordinary that it happened, but nothing in the documentary record suggests that Quigley – the Board chair – ever raised much concern. It all finally got sorted out about the time the new Board finally took office, but (a) Finlay had been receiving Board papers and attending Board meetings for months while still having his Kiwibank ownership role, and b) now serves as the Board’s deputy chair, with perhaps no current conflict but still tainting the Board’s standing (and any sort of commitment to strong and honest governance in the financial system) by his prominent presence.

Then there was the case of the current Board member Byron Pepper, who was appointed to the Reserve Bank Board – with no sign of any objection by Quigley as chair – despite being then a director of an insurance company part-owned by another insurance company that was regulated by the Reserve Bank (Board) itself. It wasn’t illegal, but it was simply a poor appointment (particularly in the first up round of appointments to a new institution) and dreadful look. But not to Quigley apparently, who simply seems to have no moral sense of what is right and wrong, what is an appropriately high standard of governance, just of what can be gotten away with. Eventually, several months later, Pepper resigned from that insurance role under pressure. OIAed documents show that Quigley still didn’t think there was anything wrong but that awkward public questions might be asked and they had to worry about the pesky OIA, which (apparently inconveniently) they had to provide “good faith responses to”.

And what of Quigley own other roles? Specifically, (what always seemed like it should be a fulltime job) as Vice-Chancellor of Waikato University. Well, there Quigley and his university were recently openly reprimanded by the Auditor General for inappropriately weak procurement practices in respect of the expenditure of large amounts of public money hiring a former Cabinet minister as a lobbyist. And this was the same Quigley, the same institution, that hit the headlines a few months ago with the oh-so-cosy, but spectacularly badly phrased (particularly from someone who was at the same chair of the Board of the Reserve Bank) fawning email to National’s then health spokesperson Shane Reti, as Quigley lobbied for a new medical school.

All the evidence is that, under pressure, he lacks integrity and judgement, including any fundamental sense of what is right and wrong, and what is fit and proper in the chair of a prominent and powerful public institution. He is unfit for office (an office he seems not to have exercised for any good – and if the Orr we’ve seen, blustering, repeatedly actively misleading Parliament, unwilling and unable to engage constructively, pursuing personal political agendas in public office (most recently his weird FDI remarks) is the one that has benefited from any guidance, counsel, or restraint from Quigley as Board chair heaven help us). And yet…. Nicola Willis and the Cabinet just went ahead and appointed him again.

They seem not to care at all about the decline of New Zealand public institutions (as, for example, their extraordiinary failure to appoint a Public Service Commissioner). Cynics suggested their only real interest was in holding office themselves. Sadly, evidence is mounting in support of that claim.

(But I have this morning lodged an OIA request with Willis’s office for all material relating to the Board appointments and vacancies. Perhaps some more favourable material will emerge. Time will tell, but I won’t be holding my breath.)

Note that under the amended law passed by the previous government, Willis will have been required to consult with other parties in Parliament on Quigley’s fresh appointment. Here, of course, only opposition parties matter. It will be interesting to see if any of them had comments to make – but between two mired in severe reputational (and worse) issues around their own members, and one that reappointed Orr (and the rest) in the first place, it is perhaps too much to hope for anything to have been said.

ADDENDUM