Monday afternoon’s post was prompted by news of the New Zealand Initiative’s business leaders’ study tour to Switzerland. Switzerland is materially better off than New Zealand, but as I illustrated over the last 45 years it is the only advanced country to have managed lower productivity growth than New Zealand.

The news of the Swiss trip reminded me of a story I’d seen a while ago, and had meant to write about, about another business study tour (involving at least some of the same people), to another laggard OECD economy, Israel. Even the Prime Minister’s chief science adviser went along. That trip was promoted by the Trans-Tasman Business Circle. You can read about it here in a story written by a journalist who was invited along on the trip (or there is an Israeli perspective here).

Most people have heard of Israel’s high-tech sector, which was the focus of this New Zealand mission. Somehow, there is an impression around in many circles – I recall first encountering it at The Treasury – that Israel is an economic success story. Here are a couple of snippets from the Herald story

The mission will visit leading Israeli companies and institutions.

This includes Start-Up Nation Central, which connects companies and countries to the people and technologies in Israel that can solve their most pressing challenges.

Start-Up Nation Central was inspired by the 2009 best-selling book Start-Up Nation: The Story of Israel’s Economic Miracle, which explores the roots of Israeli innovation. The book continues to generate enormous demand from around the world for access to the people and technologies of Israel’s innovation ecosystem.

and

Why Israel? Moutter reckons while there are obvious differences, New Zealand shares many things with Israel. “We are both relatively young countries, with a culture and heritage of innovation, as well as some similarities in terms of market scale – from our perspective Israel is a more comparable point of reference for New Zealand than larger innovation ecosystems such as Silicon Valley or Shanghai. How has this small nation, less than 70 years old, with less natural resources than New Zealand, in one of the most volatile regions in the world, become widely known as the Start-Up Nation? I believe it will be invaluable for New Zealand to have greater insight into this journey.”

Sounds good. It is a shame about the hard data.

In the modern sense, both Israel and New Zealand are young countries. And they are both somewhat improbable outposts. New Zealand was the last major land mass settled by humans, and was so remote that until the 19th century all economic activity had to occur within these islands. Foreign trade wasn’t possible, or economic. Technology changed that and for a time – after the land was taken more or less by force and the indigenous culture displaced – an economy grew here that supported some of the highest material living standards in the world, for a pretty small number of people. We remain physically remote, and that still seems to matter rather a lot.

As for Israel, the land itself has been close to where major civilisations grew and prospered long ago. Ancient Israel itself was, for a time, a rich kingdom. But in the 19th century there wasn’t much high value economic activity there. Through some mix of ideology, religious convictions, the horrors of Nazi Germany, and other later push and pull factors, a mass relocation of Jewish people has occurred. In a land taken more or less by force, in the process something fairly remarkable has been built – a relatively rich democratic society, in a region with little or no tradition of democracy and where modern prosperity has otherwise been achieved only in some of the countries with oil windfalls. Physical distance isn’t such an issue for Israel. It is surrounded by countries with hundreds of millions of people. Unfortunately for Israel, many of the regimes of those countries (or popular movements those regimes suppress) would like nothing more than the destruction of the state of Israel. Sixteen countries, apparently, ban altogether people on Israeli passports, and most of those countries are quite physically close. So, mostly, economic and social ties aren’t close. In an age when distance seems to matter rather a lot.

As I did with my Swiss post the other day, I’m going to start my comparisons from around 1970 where possible. For us, it was just before Britain entered the EU and before the dislocations of the collapse in the terms of trade in the 1970s. For Israel, it was 20 years after independence, when the country had achieved reasonable size (the population then was very similar to New Zealand’s, at just under three million), and it was few years after Israel’s greatest military success.

Unfortunately, not all of the Israeli data goes back that far (especially in the OECD databases). As I showed the other day, in 1970 New Zealand’s labour productivity (real GDP per hour worked) was just a touch below that of the median OECD country (in company with the larger European countries). I couldn’t find good comparable data for Israel for 1970 (whether for GDP per hour worked or real GDP per capita) but it looks as though Israel had outcomes pretty similar to New Zealand, perhaps just a little below. On the earliest OECD data I could find, Israel’s real GDP per capita was around 5 per cent less than New Zealand’s in 1977, and the few years leading up to 1977 were bad ones for New Zealand.

The OECD has real GDP per hour worked data for Israel from 1981. This chart shows how New Zealand and Israel have done relative to the median of the OECD countries for which there was 1970 data (ie mostly those who were really prosperous and democratic back then).

Israel’s outcomes, at least on this score, look a lot like New Zealand’s. New Zealand’s have been pretty poor. The median real GDP per hour worked for that group of country (mostly the rich countries in 1970) is 42 per cent above New Zealand’s 2015 number.

From 1981 to 2015. the median OECD country achieved growth in real GDP per hour worked of 72.7 per cent. That was around the sort of increase the US and the UK experienced. But here are bottom five growth rate countries over that period

|

Growth (%) in real GDP phw 1981-2015 |

Level in 2015 (USD, converted at 2010 PPPs) |

| New Zealand |

56.5 |

37.5 |

| Netherlands |

54.0 |

61.5 |

| Israel |

52.3 |

35.1 |

| Italy |

39.9 |

47.7 |

| Switzerland |

37.5 |

56.5 |

New Zealand wasn’t the worst, and neither was Israel. But both New Zealand and Israel started out materially less productive than the Netherlands, Italy and Switzerland, and we still languish well down the field. For all its problems, even Italy manages much higher average labour productivity than either Israel or New Zealand.

The picture doesn’t change much if, say, one starts the comparison from 1990 (after many of our reforms had been done). We and Israel still managed labour productivity growth in the bottom quartile of OECD countries.

What about foreign trade? It is now better realised that New Zealand’s export (and import) share of GDP has been going nowhere for quite some time. By contrast, world trade as a share of GDP has been trending strongly upwards over the decades. And while exports aren’t some panacea – governments can always subsidise them and get more of them – in successful highly productive economies, an increasing share of foreign trade (again imports as well as exports) is usually part of the mix. In fact, I’m not aware of any country that has successfully closed the economic gaps to the leading economies, without export success playing a material part.

So here is a chart of exports as a share of GDP, for Israel, New Zealand and for the OECD as a whole, since 1971.

Being small countries, you would expect both Israel and New Zealand to do more foreign trade than larger countries. As the chart shows, both countries used to export a lot more (share of GDP) than did the OECD countries as a whole (in which, of course, the US is a large share). That is no longer so, despite (in Israel’s case) that vaunted high-tech sector. Firms in both countries – remote in their own ways – find it more difficult to be a part of global value chains than, say, contiguous European countries (in something approaching a single market) do. But whatever the full set of reasons, it isn’t an encouraging picture.

One factor, so I hypothesise, might be relatively rapid population growth. As I noted, in 1970 Israel and New Zealand had similar populations. Now Israel is getting on for double New Zealand’s population.

Using the United Nations population data, here is a chart of population growth since 1990.

High-income countries in total have had population growth or around 16.5 per cent over that period. New Zealand’s population has increased much faster than that (at around 35 per cent), and Israel’s population has increased much more rapidly still, up by around 79 per cent.

If there are lots of great new opportunities in a country, population growth needn’t impede productivity growth. In some cases, it might even help it. Australia, for example, has also had rapid population growth, but seems to have had enough new opportunities (all those minerals) that its overall productivity and per capita income performance hasn’t been bad (although far from top tier).

What of New Zealand and Israel? There don’t seem to have been many new high value opportunities in New Zealand – in fact, in the article on the mission to Israel one thing that struck me was how many of the listed participants were from domestic-focused firms. For Israel, one might have supposed it was different (all those high tech firms).

I’ve argued for some years, that rapid population growth can crowd out other business activities. The basic logic is pretty simple. New people – whether born or migrant – need new capital stock. A modern economy requires rather a lot of (physical) capital per person (houses, roads, offices, schools, shops, machines etc) and real resources that have to be devoted to meeting the needs and demand of the new people, can’t be used for other purposes. It is often those “other purposes” that seem to get squeezed out – in particular, investment in the tradables sector. People have to live somewhere, so that demand is often more inelastic (insensitive to changes in price) than is potential investment in support of new business opportunities

It needn’t happen. A country with a fast-growing population could also have a higher than usual savings rate. That would free up resources to meet both potential needs. Over time, one might expect that. And a country with a fast-growing population might also meet some of its needs by running a current account deficit (drawing on resources from the rest of the world). But while you import a car, you can’t import non-tradables. So current account deficits can help, but they don’t relieve all the pressure.

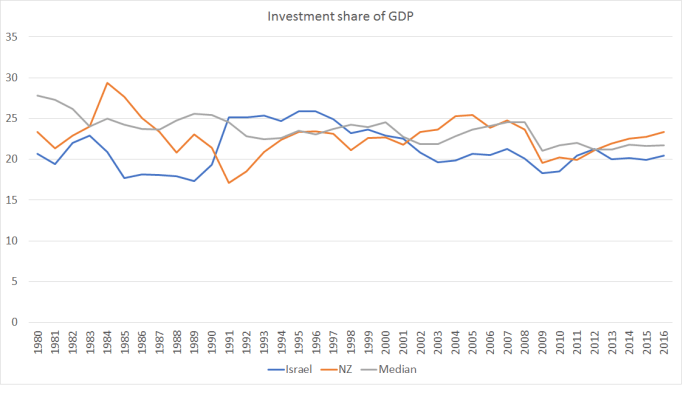

What do the summary data suggest? The IMF publishes data on the savings and investment rates for each advanced country back to 1980. Over that period, both Israel (in particular) and New Zealand have had materially faster population growth than the median advanced country. All else equal, that should have been reflected in a higher share of GDP having to be devoted to investment in both New Zealand and Israel than in the typical advanced economy.

But here are the data

There is plenty of cyclical variation, but in both countries on average over this period, the share of investment spending in GDP has been a bit lower than advanced country median. Given all the resources that needed to go to meeting the needs of the fast-growing populations (simply maintaining capital per person), there will have been materially less “left over” for capital deepening, or for new businesses and ideas. It isn’t a mechanical rationing process, but just a response to the opportunities and the relative prices.

There is plenty of cyclical variation, but in both countries on average over this period, the share of investment spending in GDP has been a bit lower than advanced country median. Given all the resources that needed to go to meeting the needs of the fast-growing populations (simply maintaining capital per person), there will have been materially less “left over” for capital deepening, or for new businesses and ideas. It isn’t a mechanical rationing process, but just a response to the opportunities and the relative prices.

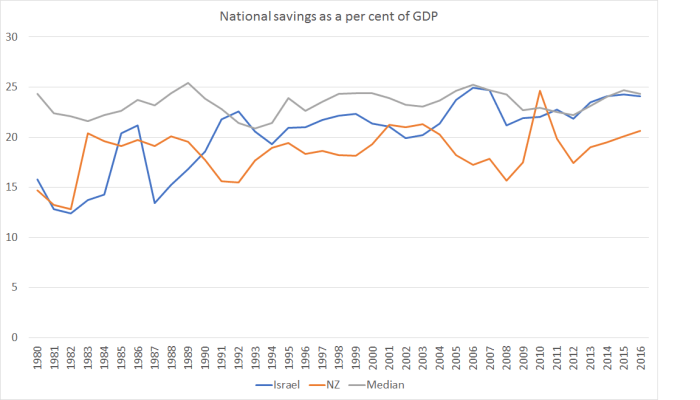

And here is the same comparison for national savings rates.

Again, despite the much more rapid population growth rates, both countries have had lower national savings rates than the median advanced country over this period.

I don’t know enough detail about Israel to be highly confident about quite what mix of factors is important in explaining its sustained underperformance (relative to other advanced, and key emerging, economies). But the underperformance is pretty clear. Israel’s productivity, like New Zealand’s, languishes towards the lower end of the OECD (and certainly of those OECD countries that were market economies a few decades ago). Perhaps there are some specifics in the Israeli high-tech sector from which visitors can learn. But if, to some extent, Israel’s sheer survival (so far) might be loosely termed a “miracle”, it isn’t clear that its economic performance is anything of the sort. Very rapid population growth looks like it might have been part of the story (whatever it has done in terms of boosting the number of future IDF soldiers).