The second XI at the Reserve Bank fronted up to present today’s Monetary Policy Statement. There was the unlawfully appointed “acting Governor” Grant Spencer – who is now signing himself as “Governor”, not even as acting Governor – the chief economist, John McDermott, and the new head of financial stability (and openly acknowledged applicant for Governor) Geoff Bascand. At best, they are holding the fort until the new Governor is appointed, and a new Policy Targets Agreement put in place, but despite that Spencer still felt confident enough to assert that “monetary policy will remain accommodative for a considerable period”. How would he know? He won’t be there.

One could feel a little sorry for the Bank. After all, not only is the second XI holding the fort, but a new government took office only a week or so ago. Between Labour’s manifesto commitments and the agreements with New Zealand First and the Greens, there are a lot of new policy measures coming. But there is not a lot of detail on most of them. The Bank’s typical approach in the past has been not to incorporate things into the economic projections until they become law (at, in the case of fiscal policy, in a Budget). They’ve departed from that approach on this occasion, and have incorporated estimates of the macro effects of four new policies:

- fiscal policy,

- minimum wage policy,

- Kiwibuild, and

- changes to visa requirements affecting students and work visas.

I suspect they’d have been better to have waited. On fiscal policy, for example, there are no publically available numbers yet – just last week the Prime Minister told us to wait for the HYEFU. On immigration, there has been nothing from the new government on the timing of any changes. And on Kiwibuild, there is no sign of any analysis behind the assumption the Bank has made that around half of Kiwibuild activity will displace private sector building that would otherwise have taken place. And so on.

And then there are the numerous other policy promises the Bank hasn’t accounted for. In the Speech from the Throne yesterday there was a clear commitment to “remove the Auckland urban growth boundary and free up density controls” in this term of government. If so, surely that would be expected to affect house prices and perhaps building activity? Binding carbon budgets are also likely to have macro effects.

I’m not suggesting the Bank can produce good estimates for any of these effects. Rather, they’d have been better to have stayed on the sidelines for a bit longer, since they were under no pressure at all to change the OCR today, rather than incorporate rough and ready estimates of a handful of forthcoming changes, with little sign that they have really stood back and thought about how the economy is unfolding.

And the conclusions they’ve come to do seem rather questionable. The “acting Governor” kicked off his press conference talking of the “very positive” economic outlook. I’m not sure how many other people will agree with him. As the Bank themselves note, they’ve been surprised on the downside by recent GDP outcomes, and housing market activity has been fading. Even dairy prices have been edging back down, and oil prices have been rising. (And, of course, there has been no productivity growth for years.)

The Bank forecasts an acceleration of economic growth – even as population growth slows – on the back of additional fiscal stimulus and additional building activity under the Kiwibuild programme. Like other commentators, I’m rather sceptical that we will see anything quite that strong. But even on their own numbers, productivity growth over the next few years is now projected to be weaker than the Bank was projecting in August. And if Kiwibuild really is going to add so much to housing supply, in conjunction with slower population growth than the Bank was expecting, how plausible is it real house prices will simply be flat as far the eye can see (or the forecasts go)? Not very, I’d have thought.

In the end, the numbers don’t matter very much. Spencer will be gone at the end of March, and we’ll have a new Governor and a new PTA. A new Governor will make his or her own assessment, and own OCR decisions. But part of what that person will need to do is take a look at lifting the quality of the Bank’s economic analysis.

For all the talk of initiatives promised by the new government, the Monetary Policy Statement itself was striking for containing not a word – not one – mentioning that the monetary policy regime itself is under review. Of course the “acting Governor” can’t pre-empt changes the detail of which aren’t known, but the Act does require the Bank to discuss in MPSs how monetary policy might be conducted over the following five years: a horizon over which we’ll have a different PTA, a different Governor, an amended statutory mandate, and a statutory committee to make decisions.

My main interest was in the contents of the press conference, where journalists raised both the issue of the proposed new mandate and the proposed changes to the statutory decisionmaking model. In both cases, I suspect the second XI said too much.

Asked about the proposed mandate changes, Spencer began noting that he couldn’t say too much as the review was just getting started. He then went on to assert that “moving to a dual mandate was unlikely to have a major impact on how policy is run”, explaining that in many ways flexible inflation targeting is akin to a “dual mandate” (something that, in principle, I agree with). But then, somewhat surprisingly, he claimed that the proposed change could lead the Bank to become more flexible, potentially allowing greater volatility in inflation to promote greater stability in employment. I guess it depends on the details of the changes, which none of us yet knows, but it was the first I’d heard of anyone calling for more volatility in inflation. Over the last decade, those who think the Bank hasn’t put sufficient weight on the labour market indicators (like me) would have been quite happy to have seen core inflation at the target midpoint on average. The previous Governor committed to that, but didn’t deliver.

On which note, it was a little surprising to hear the Chief Economist talk about how the Bank had improved its forecasts, and got its inflation forecasts right over the last couple of years. That would then explain why core inflation has remained persistently below the target midpoint??? And has not got even a jot closer in the last couple of years?

Spencer noted that at present the Bank regarded the labour market as ‘pretty balanced’, such that a dual mandate wouldn’t make much difference right now. But it turns out that they really don’t know.

They were asked a question about the government’s goal of getting the unemployment rate below 4 per cent, and – fairly enough – drew a distinction between structural policies that might lower the NAIRU and anything monetary policy could do. When pushed, they argued that on current structural policies, an unemployment rate lower than 4 per cent would be inflationary, and suggested that estimates of the NAIRU range from 4 to 5 per cent at present.

But then all three of the second XI went on. Spencer noted that the estimates are ‘very uncertain” and that in anticipation of a “dual mandate” the Bank was now doing some work to come up with some estimates of the NAIRU, suggesting that they haven’t had a precise estimate until now [although there were always assumptions embedded in the model]. Then the chief economist – who at almost every press conference tries to discourage the use of a NAIRU concept – chipped in claiming that any NAIRU was “very very variable” and “changes all the time”, without offering a shred of evidence for that proposition.

And then the head of financial stability chipped in, opining that estimates of NAIRUs around the world have been declining (not apparently seeing any connection between this thought and (a) the NZ experience, and (b) his colleague’s observation a few moments earlier that the numbers were pretty meaningless anyway.

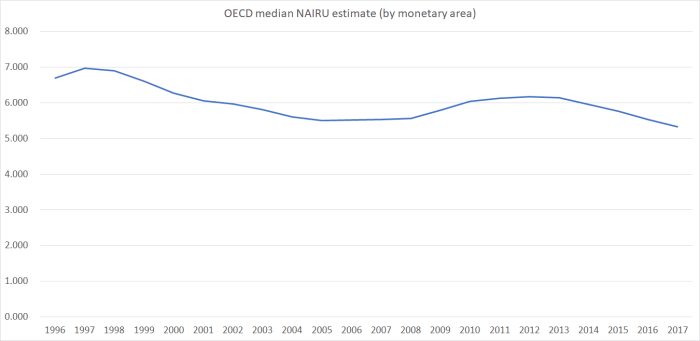

Out of curiousity I had a look at the OECD’s published NAIRU estimates. This is the NAIRU for the median OECD monetary areas (ie countries with their own monetary policy plus the euro-area as a whole).

The estimate for 2017 is 5.3 per cent. That for 2007 was 5.5 per cent. There just isn’t much short-run variability in the structural estimates of the long-run sustainable unemployment rate. That is true for other advanced countries. It is almost certainly true for New Zealand. It reflects poorly on the Reserve Bank how little they’ve done in this area, and it one reason why a change in the wording of the statutory mandate is appropriate. The unemployment rate is a major measure of excess capacity, pretty closely studied by most central banks but not, until now it appears, by our own.

(Of course, had they wanted to be a little controversial, they could have noted that proposed structural policy changes – notably the increased minimum wages they explicitly allowed for – will tend to raise (not lower) the NAIRU to some extent.)

If they were at sea on the unemployment rate issue, what really staggered me was the way Spencer (and Bascand) used the press conference to campaign for minimal changes to the statutory governance and decisionmaking model for monetary policy. They didn’t need to say more than “decisionmaking structures are ultimately a matter for Parliament, and we will be providing some technical input and advice to the Treasury-led process the Minister of FInance announced earlier in the week”.

But instead, they took the opportunity to campaign for as little change as possible. Spencer noted that they agreed the Act should be changed to provide for a committee, but noted that they already had a committee, they thought it worked well, and they would like to reflect that in the Act. Others might challenge whether the advisory committee, or the Governor, has done such a good job in the last five years (or today) but set that to one side for the moment.

They loftily conceded that there were possible advantages to having externals on a committee – the potential for greater diversity of view. But they were concerned that in a small country it could be very difficult to find outsiders with unconflicted expertise to make the system work. There was nothing to back this – no explanation, for example, as to how places like Norway and Sweden manage, or how we manage to fill the numerous other government boards in New Zealand.

But what they really hate – and I knew this, but was still surprised to hear them proclaim it so openly, just as a proper review is getting underway – is the idea that any differences of view might be known to the public. They could, we were told, tolerate a system of ‘collective responsibility’ – in which all debates are in-house and then everyone presents a monolithic front externally – but were strongly opposed to any sort “individualistic committee” in which individual views might become known. These systems – of the sort prevailing in the UK, the United States, Sweden, and the euro-area – have, they claimed, the potential to become a “circus” with too much media focus on monetary policy, and a concern about “heightened volaility” in financial markets. Spencer went so far as to suggest that an individualistic approach could undermine the reputation and credibility of the institution.

A slightly flippant observer might suggest that the second XI and their former boss have done that all by themselves – between the actual conduct of policy, and attempts (in which they all participated) to silence one of their chief critics. A more serious observer might ask for some evidence from the international experience, to suggest that the more individualistic approach has damaged the standing of the Fed, the BOE, or the Riksbank. Are these less well-regarded organisations than the Reserve Bank of New Zealand? I’d have thought it would be hard to find such evidence.

Bascand – one of the declared candidates for Governor – then chipped in to note that what management was concerned about was to ensure that the focus of discussion was on the issues “the Bank” had identified, not on individuals or their particular views. Loftily – earnestly no doubt – he declared that they wanted the focus to be on substance. No doubt, as defined by management. It reinforces the point I’ve made often that Bascand is the candidate for the status quo. Bureaucrats setting out to protect their bureau. Predictable behaviour – even if usually more subtle than this – and what the public need protecting from.

There are successful central banks that adopt the collegial approach – the RBA is one, albeit one with a rather old-fashioned committee decisionmaking model – but there is nothing to suggest, in the international experience, that that model produces better outcomes, or a more credible central bank, than the individualistic approach. Indeed, many observers would regard Lars Svensson’s open disagreement with his colleagues on the Riksbank decisionmaking committee as a useful part of the process that finally led the rest of the committee, including the Governor, to abandon their previous excessively hawkish approach a few years ago.

The second XI’s approach is that of “the priesthood of the temple” – we will tell you, the great unwashed, only what it suits us to tell you, in the form we want to present it. It is simply out of step with notions of open government, or with a serious recognition that monetary policy is an area of great uncertainty and understanding is most likely to be advanced by the open challenge and contest of ideas.

Fortunately, the new government shows signs of seeing things differently. There is a minister for open government (admittedly, lowly ranked), a commitment to improving transparency under the Official Information Act. And in the Speech from the Throne yesterday there was an explicit commitment – not referenced by the Second XI, still trying to relitigate – that

“The Bank’s decision-making processes will be changed so that a committee, including external appointees, will be responsible for setting the Official Cash Rate, improving transparency.”

Note the use of “will”. The Bank management’s preference for a “collective model” would do nothing at all to improve transparency.

It is all a reminder of how uncertain things still are, and how important the membership of the Independent Expert Advisory Panel the Minister of Finance has pledged to appoint as part of review of the Act might be (including whether the panel is really “expert” or – as rumour suggests – a politician might chair it). And also how important it is that Bank management do not have a leading say in the advice that goes to the Minister. Management is paid to implement Parliament’s choices, not to devise models that cement in the dominance (and secrecy) of management.

It is also a reminder of just how important the appointment of the new Governor is, and why it remains hard to be confident about just how committed the government is to serious change when they’ve left that appointment in the hands of the Reserve Bank Board – all appointed by the previous government, all on record endorsing the way things have gone for the last five years, and with a strong track record of serving the interests of management rather than those of (a) the public and (b) good public policy.