Two of the government’s top four ministers appeared on the weekend TV current affairs shows. It wasn’t encouraging.

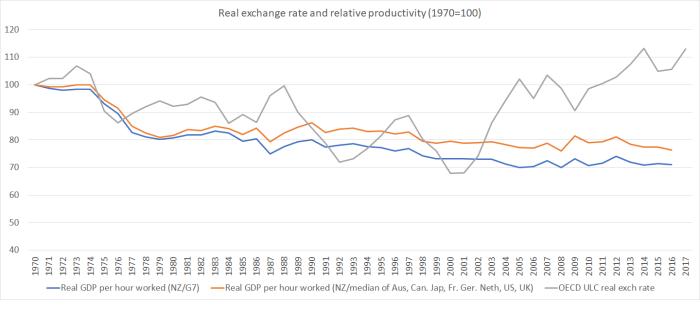

The Minister of Finance appeared on TVNZ’s Q&A. There was a great deal of talk about boosting wages – after several years in which real wage growth has outstripped (almost non-existent) productivity growth. But nothing about credible steps that might lift productivity growth itself. It is easy to spend money, but much harder to generate the foundations for higher incomes in the first place. And there seemed to be no recognition whatever that the real exchange rate has been increasingly out of line with the dismal productivity performance

or, not unrelatedly, that the export share of New Zealand GDP has been shrinking, not rising. And, of course, no plans, no suggestions even, as to what might be done to reverse this decline.

There was talk of the tax system having, it was claimed, underpinned a “speculative economy”, but no sense of how the Minister of Finance saw possible tax system changes producing materially different outcomes – notably around house prices – than they have in Australia, the UK, Canada, or much of the coastal US. Nothing, of course, about fixing the fundamental problem: land-use restrictions, the effects of which appear to have become increasingly binding (some nice new evidence on just that point from Australia was published last week).

There was blather about the forthcoming ‘wellbeing budgets”, built on The Treasury’s living standards framework, but no sense of how decisionmaking was going to be improved or economic (or other) outcomes improved.

There was a lot of talk about the “future of work” – one of the Minister’s favourite themes – and the potential to support workers facing displacement by the advance of technology etc, at a time when the employment rate and the participation rate are both higher than they’ve been at any time in the 30+ years history of the HLFS data.

There was enthusiastic talk about the economic benefits of immigration, but no evidence or argumentation. And for all the talk about “skills gaps” no recognition of the OECD data suggesting New Zealand workers are among the most skilled of any in the advanced world. And for all the allusions to the role of immigrants in building houses, no apparent recognition of just how few construction workers are among the immigrants, or of the new research published by the Reserve Bank of which the authors note (and which in many ways just repeats what New Zealand economists knew decades ago)

The estimates further suggest population change may be ‘hyperexpansionary’ as the residential construction demand associated with an additional person is higher than the output they produce. In these circumstances, population increases raise the demand for labour and create pressure for additional inward migration, potentially explaining why migration-fueled boom-bust cycles may occur.

And that was just the Minister of Finance.

On Saturday, the Deputy Prime Minister and Minister of Foreign Affairs had been interviewed on The Nation. When I read the news story about the interview I couldn’t quite believe what I was reading, and went back to watch the interview to see if Winston Peters was being fairly reported. He was.

It was bad enough to find New Zealand’s Minister of Foreign Affairs appearing to defend Donald Trump’s tariff policy. I can understand that it might not have been diplomatic to have openly attacked them as rushed, ill-considered, dangerous and not grounded in any decent economic analysis. In other words, stepping around the issue delicately would have been one thing. But the defence of Trump was pretty shameful – the more so in a week when the government of which he is Deputy Prime Minister was signing up to what it would have us believe was a new “free trade agreement”.

But rather than oppose the move as detrimental to free trade, Mr Peters said Mr Trump was reacting to unfair deals.

“What’s Donald Trump’s biggest complaint? It’s that countries shouting out ‘free trade for America’ don’t practise free trade themselves. In fact it’s New Zealand First’s and my complaint that the countries we deal with apply tariffs against us whilst we’re giving them total and unfettered access to our country. It’s simply not fair.”

He said Mr Trump’s move was “not Luddite, it’s not old-fashioned”.

“It happens to be an economic fact which some propagandists of the free market tenet should face up to, and describe why it’s not fair for Donald Trump to do what he’s doing.

Do the Minister of Finance, the Minister for Trade and Export Growth, and the Prime Minister agree with this sort of “trade as zero-sum” analysis and approach, that threatens to further undermine the WTO arrangements governing world trade, which have been of considerable value to New Zealand?

But our Minister of Foreign Affairs hadn’t finished. He also went on record as one of the few people left, outside the Russian government, asserting that Russia had not been attempting to meddle in the US 2016 election. Reasonable people might differ on whether there is any real evidence that such meddling made any material difference – as staunch an anti-Putin anti-Trump observer as Masha Gessen remains very sceptical. One might even take the view that it is not really any of New Zealand’s business. But for our Foreign Minister to actually be weighing in in defence of Putin should be inconceivable, inexplicable, and indefensible. Sadly, it is now only the latter two.

But even that was just the entree. The crowning outrage was the attempt by our Deputy Prime Minister and Minister of Foreign Affairs to suggest that the Russian authorities had no part in any responsibility for the downing of the Malaysian airliner over Ukraine and the deaths of 298 people. Sure, Vladimir Putin himself didn’t the fire the missile (leaders rarely do) but as David Farrar summarises it

the Dutch investigation found the Buk missile system was transported from Russia on the day of the crash, fired from a rebel controlled area and returned to Russia after it was used to shoot down MH17.

If the Minister just wanted to mount an argument that our firms can still trade with evil regimes – a point he went on to make – that would be one thing. After all, our governments have been pursuing deals with Saudi Arabia, even as it is primarily responsible for the ongoing disaster in Yemen. If he wanted to make an argument that there are bigger threats to the world than Russia – China say? – reasonable people could also debate that proposition.

But to minimise the Russian regime’s responsibility for what was an act of mass murder of innocent, otherwise uninvolved, civilians is just shameful, indeed disgraceful. It shouldn’t be allowed to pass quietly by by the Prime Minister, the rest of her Cabinet, or (say) the leaders of the Green Party on whom the government also depends. What sort of country would we be becoming if a senior minister can get away with lines like this?

It seemed to be a weekend for trivialising the really dangerous stuff by use of spurious – and insulting – comparisons. In the same interview, Peters seemed to compare Russsa’s actions in Ukraine (or the US) with Australia’s in legally deporting from Australia non-citizens convicted of committing crimes in Australia. And in another interview a few days ago Peters seemed to be attempting to draw parallels between the activities of the government of the People’s Republic of China in the Pacific (and presumably New Zealand) and those of private citizens among the Samoan and Tongan diaspora in New Zealand.

Amidst fears about outside influence from the Chinese in the Pacific, Peters is quick to note that New Zealand possesses some influencers of its own.

“One of great forces in Tongan society is the Tongan society in New Zealand, that’s where an enormous amount of remittance money is coming from, and that’s the same for Samoa.

“So when you talk about outside influences, bear in mind that we have massive outside influences on Samoa.”

If you refuse to actually confront real threats, that is one thing, but don’t insult us – or our friends, allies, and even our citizens – with such efforts at trivialising those threats, those behaviours.

That seemed quite startlingly incompetent.

I had a further note from Mr Horne this noting that “unfortunately MBIE are still receiving enquiries around this. As mentioned the roles are around the teams involved in the labour market issues and are to fill existing vacancies not focused on a new initiative”. At his request I have elevated his earlier comment into the body of this post.

And, as far we can now tell, there is no new thinking going on about immigration and economic performance, and MBIE has still not published the (well overdue) annual data on approvals etc under current policy (when I asked the other day, I was told it should be out by the end of April, six months late on the normal schedule.