It wasn’t me that introduced that wonderful 1957 movie to discussions about Reserve Bank governance, but them. I’ll get back to that.

Yesterday the Bank released its first on-the-record speech of the Orr era, although it must surely have been largely written before the new Governor came on board. Chief economist John McDermott and one of his staff had prepared a paper for a Reserve Bank of Australia conference. The title of the paper was Inflation targeting in New Zealand: an experience in evolution.

I’ve not typically been a fan of McDermott’s speeches (eg here) but this one reads quite well. It is mostly a background account of how inflation targeting developed and evolved in New Zealand, culminating in some brief, and fairly innocuous, comments on the pending changes to the Reserve Bank Act that the government has recently announced. For anyone looking for background or longer-term context on New Zealand monetary policy in recent decades, I’d happily suggest it as a reference (in fact, I just did for one reader).

I don’t have much problem with the description of the history – and they draw on an old article of mine on the origins of inflation targeting – and although I’d describe a few things differently I think it is mostly a fair account. As ever, I think the Bank tends to caricature the early days of inflation targeting to some extent, suggesting that things were done fairly rigidly or mechanically when the truth is – whatever some of the rhetoric at the time – quite the opposite. Then again, as I reflected on the speech I realised that there is – as far as I can work out – no one now at the Reserve Bank who was involved at all in monetary policy for the first seven or eight years of inflation targeting. I guess it is a quarter of a century ago now, but even so that took me a little by surprise. The Governor, for example, first joined the Bank in mid-1997 just in time to share responsibility for one of the more embarrassing episodes of the last 30 years, the Monetary Conditions Index. (I’ve been meaning to write up that episode, which seems to me not well-documented, and now that Orr is back at the Bank perhaps it is time to do so.)

As it happens, the Monetary Conditions Index – when for a year or more we set things up in a way that foreseeably introduced extreme short-term volatility to interest rates – remains the only mistake the Bank seems willing to concede over almost 30 years (“the MCI was a branch that we lopped off fairly quickly”). Certainly nothing about the persistent failure, over seven years now, to have core inflation near the 2 per cent focal point of the inflation target – or the attempt to aggressively tighten policy in the midst of that – all while, on their own numbers, unemployment was above estimates of a NAIRU.

But the prompt for this post was mostly some comments McDermott made about the planned introduction of a statutory Monetary Policy Committee, finally moving away from the single decisionmaker model that has few/no parallels among other central banks and financial regulators, and none among other New Zealand public sector agencies.

This was the paragraph that caught my eye

Of course, the creation of a formal (or indeed informal) committee does not guarantee superior outcomes. How the MPC will operate in practice is also extremely important. Committees are more successful when they have processes in place that aim to minimise various human biases, such as the pressure to conform, confirmation bias, and a tendency to rely on the most recent events to a greater extent than is sometimes warranted.[24] The Bank will continue to ensure our internal processes aim to maximise the benefits that committees can provide.

The footnote 24 reads as follows

24 The movie 12 Angry Men (1957, MGM) provides an excellent demonstration of how ‘committees’ (a jury in this case) should not behave, for example publicly revealing individual priors at the start of the meeting.

Of course, I agree that simply creating a legislated committee does not guarantee superior outcomes. Much of the time it shouldn’t make much difference at all to the setting of the OCR – whether for good or ill (thus the former Governor wanted his internal committee enshrined in law, and since it was gung-ho for tightening in 2013/14 as advisers, it is hard to believe they’d have taken a different collective view as decisionmakers). Committees are, in large part, about institutionalising resilience, to protect us to some extent against idiosyncratic or bad actors (in this case, a bad Governor – but it generalises in that Prime Ministers govern in Cabinets, higher courts operate as benches of judges, and so on). Layers of review – eg appeal courts – can perform much the same sort of function. Committees can help instill confidence, perhaps especially when – as with the higher courts – all judges are free to record, and have published, their considered opinions. In many of these areas – probably including the setting of the OCR – there is no objectively right or wrong answer, only a final one (for now).

McDermott rightly notes that there can be problems that undermine the effective contribution of legislated committees. He notes “the pressure to conform, confirmation bias, and a tendency to rely on the most recent events to a greater extent than is sometimes warranted”, but there are others, including the possibility of individual committee members free-riding. But he makes no attempt to relate the structure of committee that the government has chosen – which seem to largely mirror the Bank’s preferences – to the sort of biases and risks he is concerned with. How does the chosen structure allay those risks?

Thus, the government has chosen to adopt a model in which:

- outsiders will always be numerically dominated by insiders,

- the Governor – an insider in these terms – chairs the committee and controls all the resourcing of, and paper flow to, the committee, and where

- the Governor will have a big influence on all the appointments to the committee (several will be his own staff, appointed on his recommendation, and the others will be appointed by the Minister on the recommendation of the Bank’s Board – but with the Bank’s Board historically having served mostly to assist the Governor).

- and outsiders (and insiders for that matter) will be unable to articulate their individual views in public, and won’t be held individually accountable for those views (or for their contribution to the committee).

In the hands of an exceptional Governor – one genuinely open to debate and challenge, through the worst of times – none of that might matter. But we don’t legislate on the presumption that men are angels. For a typical Governor – moderately competent, moderately defensive, moderately arrogant – it is a recipe for something as close as possible to the status quo. And, frankly, for typical other members: insiders won’t see much payoff in resisting a Governor with a strong view, collegiality among management will encourage caucusing and a fairly common insider view, and anyone willing to take appointment as an outside member might be readily content to settle for the prestige, and the inside view of the process, rather than supposing that they have much chance of making much difference. There will be no cost to just going along, and in the papers the Minister raised the threat of being dismissed if an outside member does make life awkward for the Governor.

I don’t want to overstate things. But the chances of getting the real benefits of a committee on this particular topic (monetary policy) have been undermined by the choices the government has made and the Bank appears to have supported. Bureaucratic interest appears to have trumped the public interest.

And that footnote concerned me on a number of counts. It obviously wasn’t just a throwaway line – having been deliberately included as a footnote in a published text, which will have gone through numerous drafts. It is an odd example to use in many ways. For example, a jury is a one-shot game (jurors typically don’t know each other previously, they decide one case, and then may never see each other – let alone meet for another deliberation – again). Monetary policy decisions, by contrast, are a repeat game: the OCR is reviewed every six weeks or so, and the same individual or group of people make the decision for years at a time. They bring their priors, their experiences, their past mistakes to the table, and are encouraged to do so. It is also deliberating on issues where everyone – inside the committee and outside – has access to the same information, and no information is inadmissible. (And where the financial markets are trading that information continuously.)

McDermott seems to take as the lesson of 12 Angry Men that members of a committee should not outline their individual initial views at the beginning of the meeting. Perhaps that is arguable (in principle), but in the case of the jury in question the “meeting” began only after all twelve jurors had been exposed to all the evidence in court – defence and prosecution. In that sense, the start of the jury deliberations in the movie reminded me quite a bit of OCR Advisory Group meetings I sat on for years: we’d have spent several days listening to presentations, asking questions, listening to the questions of others, and then the small group would retire. And often the Governor would go round the table and invite each member in turn to outline their view. When we wrote our formal advice to the Governor, we were all supposed to do so independently – and not read anyone else’s until we’d sent off our own. And when the group reconvened there was never an opportunity to seriously debate the issues, or challenge the arguments that (say) an 11:1 majority of the Governor’s advisers were using. In some ways, it felt a lot like 12 Angry Men, except without the heroic denouement in which truth was outed, and the majority converted.

The parallels are weaker than they might look. For a start, no one’s life is on the line (as in the movie). Perhaps more importantly, an OCR decision made today can be, and is, revisited 6-8 weeks hence. And if all the members aren’t necessarily expert they at least have some ongoing familiarity with the subject matter, and exposure to the views of equally capable people outside the institution, in real-time.

But the challenge remains for the Bank (and the government). How does it propose that the new committee will overcome the tendency for the Governor’s preference – backed by resourcing, control of pay etc for internal members, an inbuilt majority, and an appointment procedure that will encourage the appointment only of house-trained outsiders – to go on dominating, whether the Governor’s view (or the collective inside view) is right or not. Sometimes it will be right, but those arguments should prevail on their merits, not on institutional biases that strengthen the hand of one dominant individual and his clique, and make unlikely the prospect that a single outsider will ever be able to make the sort of difference the (heroic) 12th juror in the movie made. Of course, it is only a movie…..then again, it was the Bank that introduced the reference, not me.

Far better to institutionalise a system more explicitly designed to air, test, and challenge the full range of views:

- all members appointed directly by the Minister of Finance,

- a majority of the members being non-executive outsiders,

- those outsiders having access to (a limited amount of) resources to do/commission their own analysis research,

- individual OCR votes being recorded, and published, by name,

- full minutes – with views attributed on a named basis – be kept and published (paralleling the Swedish system, and – in a slight different way – the way the higher courts work),

- individual members being free to engage externally (including making speeches) articulating openly their views and questions.

In the nature of the monetary policy issues – repeat game, same information base open to everyone, huge uncertainty – it seems like a model better designed to get the most from a committee system, and to be consistent with commitments – from the government – to more open government. Of course, the Bank – at least under the previous management – never really wanted more than an fig-leaf committte. Any analysis of bureaucratic incentives means that shouldn’t be a surprise. From McDermott’s comments yesterday, it isn’t clear that anything has yet changed. But the bureaucrats – with interests to protect – shouldn’t be the ones driving the reforms.

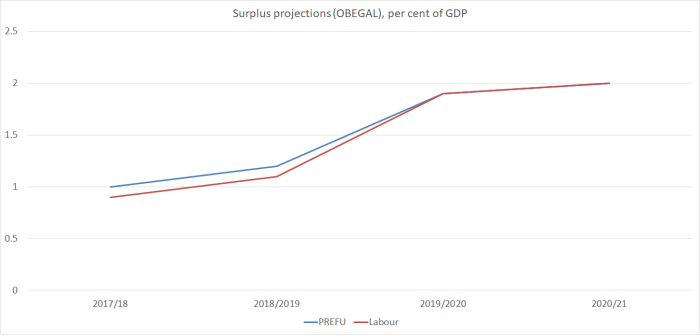

When net core Crown debt is already as low as 9.2 per cent of GDP – not on the measure Treasury, the government and Labour all prefer, but the simple straightforward metric – what is the economic case for material operating surpluses at all? With the output gap around zero and unemployment above the NAIRU, it is not as if the economy is overheating (the other usual case for running surpluses). Even just a balanced budget would slowly further lower the debt to GDP ratios. One could mount quite a reasonable argument for somewhat lower taxes (if you were a party of the right) or somewhat higher targeted spending (if you were a party of the left, campaigning on structural underfunding of various key government spending areas).

When net core Crown debt is already as low as 9.2 per cent of GDP – not on the measure Treasury, the government and Labour all prefer, but the simple straightforward metric – what is the economic case for material operating surpluses at all? With the output gap around zero and unemployment above the NAIRU, it is not as if the economy is overheating (the other usual case for running surpluses). Even just a balanced budget would slowly further lower the debt to GDP ratios. One could mount quite a reasonable argument for somewhat lower taxes (if you were a party of the right) or somewhat higher targeted spending (if you were a party of the left, campaigning on structural underfunding of various key government spending areas).

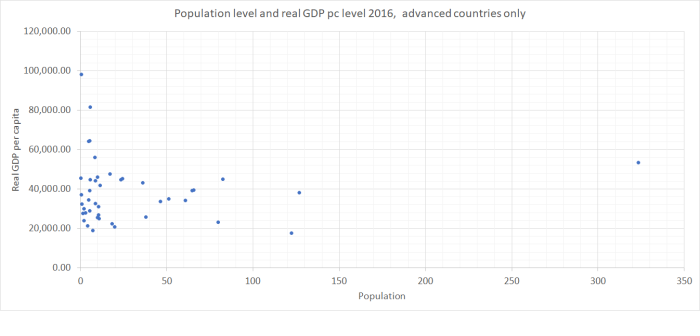

For those with sharp eyesight, New Zealand is a dot coloured orange.

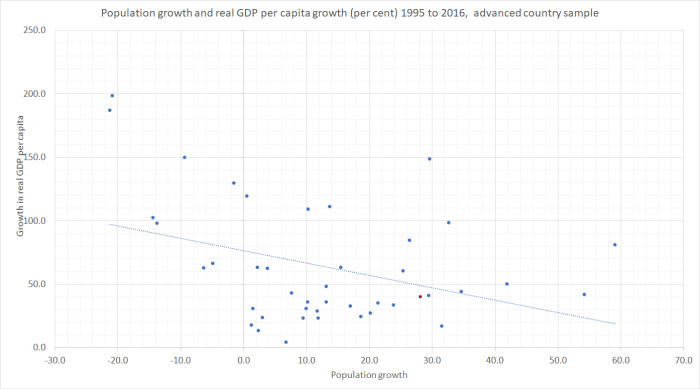

For those with sharp eyesight, New Zealand is a dot coloured orange.