The Australian Productivity Commission that is.

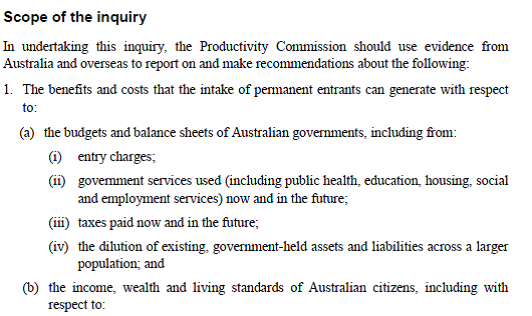

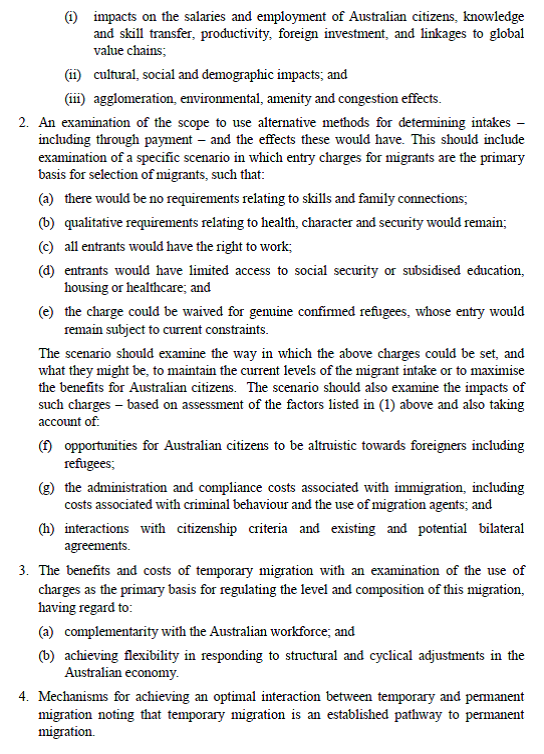

The Australian Productivity Commission has underway an interesting inquiry, initiated by the Federal Treasurer, into immigration to Australia. Here is the scope of the inquiry, taken from the Treasurer’s Terms of Reference.

It is interesting that the Australian government has chosen to initiate another Productivity Commission inquiry only 9 years after the previous large report into the economic impact of immigration. That bulky report concluded that in Australia, the gains from immigration mostly accrued to the immigrants, with little evidence of any material gains to native Australians. Despite the size of that earlier report, there was some aspects of the economic issues (possible benefits, as well as possible costs) that were not covered at all, and the modelling work that was done looked at the medium-term rather than the long term.

The new inquiry has two areas of focus. The first is helping to answer the questions about the costs and benefits of immigration, both to Australian citizens more generally and to the fiscal position of Australian governments more specifically. The second is around the intriguing idea of charging for entry. The idea of rationing entry by price turns up in immigration debates from time to time. “Intriguing” here is my code word for something like “this idea appeals to the economist in me, but yet there is something about it – which I can’t quite put my finger on – that is distasteful, and it seems unlikely to fly”. I can’t see it happening, and yet I’m not entirely sure why it shouldn’t. If we set aside the refugee quota, countries like New Zealand and Australia allow and promote immigration largely for economic reasons, and a price should tell something useful about who could get most value out of permission to live in our country. Perhaps willingness to pay is not overly well aligned to ability to help generate domestic productivity benefits? But is there good reason not to use price to ration demand for places among those who meet certain basic criteria (age, English language, lack of criminal history etc)? It will be interesting to see what the Commission comes up with in this area.

To their credit, the team working on this immigration inquiry sent a couple of senior people to Wellington this week. New Zealand has quite similar immigration policies to Australia, and for Australia in particular, the largely-free trans-Tasman immigration area also complicates things (as it does for us, in the possibility of people returning home late in life to claim New Zealand welfare benefits). I was among the various groups of public and private sector people they met while they were here, and we had a good wide-ranging discussion.

I noted that I had increasingly come to think that good immigration policy – in countries like ours, with no treaty obligations to allow open access, and (unlike Israel) no national identity/security reasons to promote immigration – is best thought of as an optional complement to economic success. The alternative, which seems to be at the heart of the arguments of immigration advocates in New Zealand, is to see immigration policy as an engine (perhaps large, perhaps small) helping generate economic success. I can’t think of a country – going back centuries – where immigration has materially improved the economic fortunes of the recipient country. In the last great age of immigration – the decades prior to World War One – migrants flowed to countries that were already economically successful (be it New Zealand, Australia, Canada, Argentina, the United States or even within Europe itself). Economic success allows a country, if it chooses, to support more people at high incomes. And emigration eases the pressures in the source country, lifting living standards among those who remain.

There is, of course, an exception to my story. Immigration has transformed the economic prospects of some physical territories, but only by totally taking over and largely replacing the indigenous population, and the economic institutions of that culture. New Zealand – like each of the colonies of settlement – is an example of that. And it is an uncomfortable example. My assessment (backed, for example, by the work of people like Easterly, looking at long-term global economic performance) is that Maori average incomes are higher now than they would have been without extensive European settlement, but was the trade worthwhile – across all its dimensions – for the indigenous population? There are huge discontinuities between 21st century New Zealand and 18th century “New Zealand” that don’t exist for, say, the United Kingdom or France.

By advanced economy standards, New Zealand is a classic example of an underperforming country that people should be leaving. And, of course, for decades New Zealanders have been doing so, mostly to more successful Australia. Of course, we can always attract plenty of people from other (even poorer) countries if we want to. But why would we? There is no obvious area of the world where the culture and economic institutions are so obviously superior to our own Northern European-sourced ones that we can get the sort of transformative gains (at whatever costs) that Maori may have achieved by allowing extensive European settlement in the 19th century. There is no sign in the data that slightly larger countries grow faster (per capita) than slightly smaller ones. And there is no reason to think we can somehow attract the very best of possible migrants to a small, remote, underperforming, but pleasant, country. And if current migration patterns were repeated at scale, or for long enough, we would face the risk of factor price equalisation occurring, but not in the way we want – the typical migrant to New Zealand comes from countries, and economic cultures, that generate materially lower living standards and levels of productivity than New Zealand (or Australia) does.

The draft report of the Australian inquiry is due out in mid-November. I’ll be keeping an eye out for it. Perhaps it might be time for a similar inquiry in New Zealand. I think I’ve mentioned that when I first started raising my arguments about the possible link between immigration policy and New Zealand economic underperformance, there was a lot of discomfort at Treasury. Senior people then talked of the new Productivity Commission as a good place for such issues to be explored. That remains true today, and Treasury has a key role in advising ministers which inquiries to request from our Productivity Commission.

I have had Official Information Act requests in for some time with Treasury and MBIE for copies of advice to ministers on the economic impacts of immigration, and on the target level of permanent residence approvals. As is customary with government agencies, the responses to the requests have both been extended/delayed. These aren’t particularly time-sensitive requests, but I will be interested to see what the departments have had to say. MBIE is well-known to be strongly pro-immigration, and I have heard reported that current Secretary to the Treasury (himself a temporary migrant) recently reiterated in private a view that “immigration is good; it is as simple as that” (repeating the tenor of comments in a speech earlier this year). Perhaps, but let’s see the argumentation, in the specific context of New Zealand, and in the light of cross-country economic history and experience.