On the day of the US mid-term elections it seems appropriate to have a US topic.

I read a lot of books each year. Many of them provide a fresh angle on some or other issue I’m interested in, but few lead me directly to change my mind. Professor Laurence Ball’s The Fed and Lehman Brothers is one of the exceptions. I wasn’t pre-disposed to expect much from Ball (a professor of economics at Johns Hopkins university): my impressions of him were formed by his visit to New Zealand 20 years ago when, as Reserve Bank professorial fellow at Victoria University, he somewhat embarrassed his hosts by suggesting that the conduct of key elements of fiscal policy should be handed over to independent technocrats. Interesting idea I suppose, but given that the point of spending public money on the fellowship had been to buttress public support for an independent Reserve Bank, it didn’t really help, especially in an election year with Winston Peters in the ascendant.

But the new book looked intriguing. As it turned out, it was much more than that, and I’d go as far as to call it a “must-read” for any serious student of the 2008/09 financial crisis.

It is a very careful and detailed study focused largely on one question: could the US authorities have lawfully prevented the failure of Lehmans that fateful weekend in September 2008 if they had wanted to? Key decisionmakers have claimed, at the time and subsequently, that there were no lawful options open to the Fed (Bernanke, for example, is quite explicit in his claim that the authorities could only have intervened in breach of the law). Ball shows, pretty conclusively, that such claims are simply wrong. The decision not to provide liquidity support to the Lehmans group was just that, a choice. And he goes on to illustrate that although in law any decision to have provided liquidity support (or not) rested solely with the Board of Governors of the Federal Reserve, in fact the key player was the US Secretary to the Treasury, Hank Paulson, with the Fed apparently deferring to his preferences.

Under the Federal Reserve Act as it stood in 2008, the Fed could lend to non-banks (as Lehmans then was, and as Bear Stearns had been) only in “unusual and exigent circumstances”. Most commentators will agree that in September 2008 – a year into an unfolding financial crisis, shortly after the US government had intervened to support the mortgage agencies – that particular strand of the legal test could readily have been passed, in respect of a major investment bank closely intertwined with the rest of the wholesale financial system in the US and abroad (Lehmans had major operations in London). The other strand of the legal test was that any loans had to be “secured to the satisfaction of the Reserve Bank” making the loan. There apparently wasn’t much (or any) case law on this provision, but it was generally accepted within the Fed that the Federal Reserve shouldn’t be lending if they weren’t pretty sure of getting their money back.

But what wasn’t in the statute was a requirement that the borrower itself still be solvent (positive net equity). A financial institution’s directors would presumably have quite severe limits on their ability (or willingness to risk doing so) to trade while insolvent, but from the point of view of the Federal Reserve, considering providing lender of last resort liquidity support, the relevant issue wasn’t the solvency of the institution, but the adequacy of the specific collateral the Fed would receive to cover any loan. Nonetheless, senior policymakers have since claimed that Lehmans was insolvent and that, in any case, there was insufficient good collateral to support a loan of the size that might have been required. Ball challenges both claims.

He does so using an array of published material, including regulatory filings, bankruptcy examiners’ reports, and the report (and supporting documents) of the Financial Crisis Inquiry Commission.

On the solvency front, one issue Ball has to grapple with is that when Lehmans was placed in bankruptcy there proved to be a considerable shortfall in net assets: not just shareholders (who lost everything) but creditors lost significant sums (and some court cases are still unresolved). But that is a quite different issue from whether there was positive net value in the business at the point where the decision not to provide liquidity support was being made. Economists have long recognised the concept of “bankruptcy costs”, and Ball makes a pretty compelling case that the bankruptcy process itself resulted in significant transfers of value to other parties that would be unlikely to have occurred in a more orderly process (the three areas he singles out relate to the termination of derivatives contracts, the fire sale of subsidiaries, and the disruption of various investment projects (mainly in real estate) that Lehmans was party to. But on a going concern basis Ball concludes his detailed analysis this way

…the best available evidence suggests that Lehman was on the border between solvency and insolvency based on realistic mark-to-market accounting, and it was probably solvent based on its assets’ fundamental values.

As noted earlier, the critical (legal) criterion wasn’t about institutional solvency, but about the specific collateral the Fed could have obtained.

You might have assumed – in a hazy way I think I did – that by the end Lehmans wouldn’t have had much decent collateral left. Perhaps you assumed that if the Fed had lent, it would all have been “secured” on dodgy commercial real estate loans. But, as Ball demonstrates, that view is quite wrong. Lehmans had been funding a large proportion of its balance sheet (as was the norm then for investment banks) through repos using fairly high-quality securities (ones that Fed was happy to accept), and the run on Lehmans primarily took the form of counterparties not being willing to roll over this repo finance (itself an interesting phenomenon, given that repo contracts should have left any counterparty with a clean ownership of the collateral security in the event of bankruptcy). But to the extent the repos didn’t roll over – and it was clear they wouldn’t have on the Monday morning without Fed support – Lehman would still have been left with the (good quality) securities. It also had long-term funding on its balance sheet, which couldn’t go anywhere in the short-term. Ball demonstrates that Lehman had sufficient volumes of good quality acceptable collateral that it could have secured a large enough Fed loan to have replaced all its short-term funding if necessary. The numbers would have been large, but as Ball points out no larger than the amounts injected into AIG a few days later (for a risky equity stake), or lent to Morgan Stanley a short time later.

There is an important distinction to be made here. The issue Ball is dealing with is not whether the US authorities should have taken over, and recapitalised, Lehmans. His argument – nested in the liquidity provisions of the Federal Reserve Act – is that liquidity support could (lawfully) have been provided, and that had it been provided it would have opened the way to a less costly, less disruptive, resolution over the following months. Perhaps it would have been possible to inject more private equity to the holding company and enable it to continue as a going concern. But if not, the prospects for a takeover of the business would have been greater – for example, a key obstacle to Barclays taking over Lehmans was the need for a shareholder vote which would have taken at least a month – or it would have been possible to have sold subsidiaries – including the valuable asset management subsidiary – in a more orderly and competitive process. At worst, a more orderly wind-down would have been facilitated.

One of the other things Ball documents is the work that had gone on inside the Fed over several months, right up to the fateful weekend, on possible liquidity support mechanisms for Lehmans. It seems pretty clear that there was never a presumption inside the Fed that if a private buyer was not be found that Lehmans would simply be left to the tender mercies of the bankruptcy administrator. (In fact, as he notes even when Lehmans was forced to file for bankruptcy, the Fed provided substantial liquidity support to keep the New York broker-dealer subsidiary open for several days until Barclays committed to purchase it.)

So why didn’t the Fed prove willing to provide liquidity support for the whole group? Ball argues, pretty conclusively, that the key player here was Secretary to the Treasury, Hank Paulson. In law, the Secretary to the Treasury (or anyone else in the Administration) had no role in such decisions. And it is not as if, in the specifics of the time and system, Paulson had any greater political legitimacy than, say, Bernanke. Both were appointed by (outgoing) President Bush, and both had been confirmed by the Senate. Presumptively, Paulson was likely to be out of office in January 2009 no matter who won the election, while Bernanke had more of his term to run. But, of course, the politics around Wall St “bailouts” had been turning increasingly nasty since the Bear Stearns intervention (where the Treasury had got involved, implicitly underwriting the Fed’s credit risk) and Paulson – a strong personality – was quite open that he didn’t want to be remembered by history as Mr Bailout. Perhaps the distinction between well-collateralised liquidity support and (actual or implicit) equity support got bypassed in the heat of the moment.

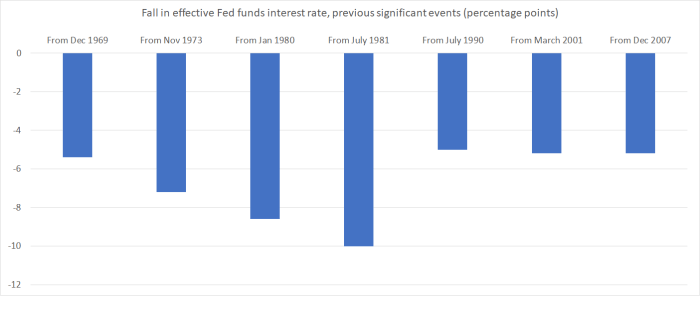

But the other relevant aspect, given the political aversion to more “bailouts”, seems to have been a sense within the Fed that the pressures on Lehmans had been so well-foreshadowed, over months, that its failure wouldn’t prove that disruptive. Key players now claim that that wasn’t their view – Bernanke is on record claiming that he always knew it would be a “catastrophe” – but Ball demonstrates that such claims are simply inconsistent with what the Fed was saying or doing at the time. For example, the FOMC met two days after the Lehmans failure. Had the Fed thought the Lehmans failure would prove “catastrophic”, or even just aggravating the severity of the recession, a cut to the Fed funds rate would surely have been in order. There wasn’t one. And the published records of the meeting show no sign of any heightened concern or anxiety about the financial system or spillover effects to the economy. If that was the prevailing view at the top levels of the Fed, it makes more sense as to why central bankers would defer to political pressure not to have provided (liquidity) support for Lehmans.

Central bankers don’t emerge with much credit from Ball’s book. Anyone can make mistakes in the heat of the moment – even a large institution with a deep bench like the Federal Reserve – but what is perhaps more troubling is the suggestion (which seems pretty convincing to me) that key players (Bernanke, Geithner and Paulson) had been spinning the situation in their memoirs, rather than confronting the specifics of the data and the law. Perhaps I become a bit more sympathetic than I was to (former BOE Governor) Mervyn King’s choice to avoid memoirs, and a defence of his involvement, in his own post-crisis book. Thank goodness then for the efforts of a careful, apparently dispassionate, academic like Ball.

Of course, to agree with Ball’s conclusion that the Fed could have provided liquidity support to Lehmans if it had wished to do so is not to immediately jump to the conclusion that they should have done so. Although it isn’t the focus of his book, it is pretty clear that Ball thinks such support should have been given.

A counter-argument could have a number of strands:

- first, Lehmans had been under pressure for months to raise additional outside equity, and had failed to do so. Had they done so, even at deeply discounted prices, it is unlikely that the wholesale run would have developed as it did (and even had it done so, the politics of liquidity support might have been different),

- second, had Lehmans been a bank supervised by the Fed it would probably not have been allowed to stay open even as long as it did without new capital. In bankruptcy courts, the relevant test might be whether there are still positive net assets, but bank supervisors who are doing their job should have been intervening pretty strongly – including using directive powers – before any question arose as to whether net assets were still (perhaps barely) positive, and

- third, there is still the unanswered question (which may never be satisfactorily resolved) as to just how much the Lehmans failure exacerbated the recession. Counterfactual history is hard. The consensus view at present is that the adverse effects were large, but if much of the disruption would have happened anyway – even if Lehmans had been left limping for a couple of months on liquidity life-support – the case for intervention is weaker than many would allow (and, for example, AIG’s plight was largely unrelated to the Lehmans failure). After all, there is a salutary place for market discipline, including around the urgency of injecting new capital when dark clouds loom.

I was one of those who tended to welcome the decision not to “bail out” Lehmans (better still not to have intervened around Bear Stearns months earlier) but I probably haven’t distinguished clearly enough between liquidity and solvency support. The latter option – which wasn’t something the Fed could have done anyway – isn’t the focus of this book, but Ball does make a pretty persuasive case around liquidity support, including based just on facts that were available at the time (on the aftermath, no one could be certain).

I could still mount a counter-argument based on the first couple of bullet points above. Providing liquidity support in such circumstances would have sent a signal to boards and managers of other institutions that any urgency to raise new capital, at deep discounted prices, was less than it might have seemed. On the information availabe at the time, that would have been unfortunate. Then again, within days that whole argument was tossed out the window as the authorities rushed to respond to a deepening crisis.

But perhaps what finally gets me over the line in thinking the Fed made a mistake, in not lending and in deferring to Paulson (in a politicised time six weeks out from an election), is an assessment of the probabilities. Perhaps the Lehmans failure really wasn’t that big a deal. Perhaps the Fed at the time was justified in its view that a failure could be managed without too much spillover downside. But operating in a world of heightened uncertainty, no one could really know. There had to be a chance that simply allowing Lehmans to go into bankruptcy – the largest bankruptcy in US history, all done in rush – would prove very very disruptive and economically costly. But if providing strongly-collateralised liquidity support, quite possibly at a high interest rate and with ample haircuts, could have alleviated that risk – even if it was only a 10 per cent risk – it is hard not to conclude (even without the benefit of hindsight) that the central bank should have acted. After all, lender of last resort provisions are put in statutes for a purpose – and not just a decorative one.