On a quick read through the Executive Summary of the latest consultation document from the review of the Reserve Bank Act, there look to have been a range of not-entirely-unreasonable in-principle decisions made by the Minister of Finance. Some even look thoroughly welcome, if long overdue, including the in-principle decision to end the charade that the Board of the Reserve Bank could or would adequately do the job of holding the Governor to account. In turn, the decision to stop the Governor being the sole decisionmaker on banking regulatory policy can’t be implemented soon enough.

The other major change that I welcome, and have championed for some years inside and outside the Reserve Bank, is the decision to introduce a deposit insurance system. Among advanced countries, New Zealand has been increasingly unusual in not having such a system. The discussion of deposit insurance issues is from page 85 onwards in this document.

There are lots of details still to be sorted out, but the headline-grabber in the announcement yesterday was the aspect of what is proposed that I have most problem with.

The Minister has also made an in-principle decision that the scheme will protect eligible depositors’ savings up to an insured limit, proposed to be in the range of $30,000-$50,000 per depositor.

This has the feel of a bureaucratic compromise, including with the staff at the Reserve Bank who have consistently opposed deposit insurance. More importantly, it is a ridiculously low limit which would almost certainly prove untenable, unsustainable, in an actual crisis. David Tripe, at Massey University, calls it “a joke”, but it is (of course) more serious than that.

I favour deposit insurance mostly for second-best reasons. You can advance various arguments for why deposits should, in principle, be specially favoured and protected. I’m not really convinced by any of them. If people really wanted rock-solid assets, and were willing to pay for them, the market could and would provide. The evidence is, quite strongly, that people don’t (look, for example, at the tiny number of people holding government retail Kiwi Bonds, in contrast to the amount in bank term deposits etc). And that isn’t surprising. Not only are banking crises rare, in countries where markets are allowed to work – how much different the literature and mindset in this area might be if for 150 years Canada had had US banking etc laws, and the US had had Canadian ones – but in the course of our lives many of us are much more likely to have serious – larger – unexpected losses (financial or otherwise) from other sources. A leaky home, a lost job, a serious relationship break-up, health problems, a business plan that just didn’t work out, an unexpected change in government policy, living in a town that economic activity moved away from, and so on.

I’m not even persuaded by arguments about bank runs, that seem to have appealed to the authors of the consultation document (and the IMF and OECD). There is little evidence of irrational runs and – as we saw globally in 2008/09 – wholesale creditors are at least as capable of running for their money, rationally or otherwise, as small depositors.

No, I support a credible deposit insurance system because governments – abroad, and here – have a demonstrated track record of bailing out depositors, and whole banks, when faced with a crisis, and political incentives that mean it would be difficult to change that track record – perhaps especially in a political system such as our own, where so much power is bested in the executive, and the executive governs by commanding a majority (at least on supply issues) of Parliament. If we believe in the importance of market discipline (beyond simply shareholders) – and I do – then we need to do what we can to identify and recognise the pressure points and to internalise the costs of the protection they result in. In this case, it is a concentration of (likely) voters, facing (potentially) large and visible immediate losses.

I’ve run through the likely political calculus in earlier posts (eg here), but suffice to say that I just do not believe that a plausible New Zealand government, faced with a plausible failure scenario for a major New Zealand bank, would let a bank fail, and use the OBR tool on all creditors, with protection only (via a deposit insurance scheme) for $30000 to $50000 per depositor.

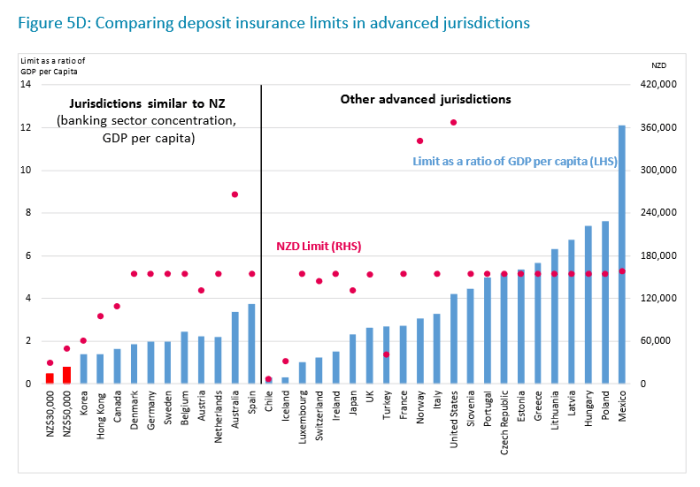

The government has sought to argue that the proposed cap on coverage is somehow internationally mainstream, but I don’t know who they are trying to fool (themselves apart?). This chart is from the official document.

You can ignore the strained attempt to split OECD countries into two separate classes and just focus on the data. Whether you look at the limit in simple dollar terms, or as a ratio to GDP per capita, the range of coverage the government proposes here would be lower than in all but two OECD countries. And perhaps the thing that stands out to me most starkly from the chart is how many of those red dots (the other country limits in NZD terms) are at or near $150000.

Not unimportantly, the limit in Australia is A$250000 (just a bit more than that in NZD terms). The government has probably noticed that the big banks in New Zealand are all subsidiaries of Australian banks. It is probably aware that if a big New Zealand bank ever gets to the point of failure, it is highly likely to be a situation in which the parent is also on the brink of failure. And anyone who has ever thought about the issue recognises the high likelihood that the resolution of a failed Australian banking group, with major operations in New Zealand, is likely to be handled at a trans-Tasman political level (including because of pressure from the Australian government to keep the banking groups together, which might well be the best way to realise value for creditors). Most likely, the big banks would simply be bailed out completely. But if they weren’t, how credible do you suppose it is that a New Zealand government will simply walk away from depositors with amounts in excess of, say, $50000 – left to the tender mercies of OBR – while their Australian siblings (in a bank with the same brand) are protected to A$250000? Not very, would be my answer. (And bear in mind the complication that it is generally recognised that if OBR is ever used, the non haircut deposits in any failed bank will need to be government guaranteed, and that such a guarantee may even need to be extended to other banks, to avoid a big loss of funds to the failed bank.)

I’m not arguing that we need the same limit as Australia – apart from anything else, New Zealanders are poorer on average (but would it have hurt to have looked at common model?) – but a $30000 to $50000 limit will simply strike people as so low that it won’t be persisted with if and when a crisis hits. Deposit insurance limits get changed on the fly – it happened all over the advanced world in 2008/09 – and when they are, those who get the protection won’t have paid for it. Failing to get this right, ex ante, simply increases the risk that when the crisis comes we’ll end up bailing out wholesale creditors (including foreign ones) too.

Much better to put in place a credible limit (indexed to inflation or nominal per capita, to remain sensible) – perhaps $150000 per depositor – and charge depositors directly for the protection the Crown is proposing to offer. Don’t – as the discussion document talks of – build up a modest fund and then stop charging the levy. Remember that major bank failures are (and are supposed to be) very rare events: a levy of 15 basis points per annum on insured deposits for 150 years, would cover losses of (say) 20 per cent of all insured deposits (an extraordinarily large loss). But just like your house insurance, the best outcome is if you pay your premium all your life and never need to make a claim.

The consultation document discussion on deposit insurance is itself something of a mixed bag. At a technical level, some of its seems solid enough, but then they attempt to buttress it with overwrought claims. There was this, for example

The GFC showed that a loss of confidence in one bank can rapidly spread throughout the financial system through ‘contagion’ that causes instability and destroys financial and social capital.

“One bank”???? And, even more far-fetched

The OECD (2013) and IMF (2017) have both warned that, without depositor protection, New Zealand is particularly vulnerable to contagious bank runs that can escalate into banking crises that destroy social and financial capital. The financial costs alone could be profound and long-lasting: experience overseas suggests that in a bank crisis GDP might fall 20 percent below trend, and the Government debt-to-GDP ratio might increase by 30 percentage points for a decade.

As we have seen, in analysing the Reserve Bank’s claims around bank capital, most of those “cost of crises” analyses simply don’t withstand serious scrutiny. But, even if they did, no serious observer would claim that the presence or absence of deposit insurance in the difference sparing us staggering GDP losses. Here, officials and the governments are attempted to sell us a model in which financial crises arise out of nowhere, and they know – even the Minister really should – that that is simply not so.

But I was left wondering quite how much the Minister of Finance understands when I saw him reported as suggesting that

A bank deposit protection scheme may help defuse the battle between the Reserve Bank and the country’s biggest trading banks over how much extra capital they should have to hold on their balance sheets, Finance Minister Grant Robertson indicated today.

It is a lot more likely to amp up the tensions I’d have thought. From a fiscal perspective – the Crown as underwriter of a deposit insurance scheme – deposit insurance increases your interest in having bank capital ratios as high as possible (and the discussion document talks of funding deposit insurance with a levy on bank profits, rather than directly on insured deposits). But it was noticeable that there was no discussion at all of the interaction between the two: in principle, the higher your minimum capital ratios, the cheaper the deposit insurance should be. I guess we will know the Governor’s final decision on capital before the Minister tries to legislate deposit insurance, but you would hope for some more joined-up discussion at some stage.

On which note, on the Radio New Zealand news last night, I heard the Prime Minister quoted as saying (apparently at her post-Cabinet press conference)

“Our banking system is one of the strongest and most resilient in the world”

I suspect she is probably right about that (floating exchange rate, vanilla loan books, little or no government interference in housing finance markets, no history of recent financial crises, banks part of much bigger overseas groups (from a similarly governed country).

But, if she is right, if that is what she has picked up from her briefings, from Grant Robertson, and perhaps even from the Governor, what possible grounds are there for requiring the huge increases in minimum bank capital ratios that the Governor is currently proposing? We’ve not seen a cost-benefit analysis (but, who knows, perhaps she has). On the face of it, let alone digging more deeply, there is no such case. She is content, it appears, to let an unelected bureaucrat impose potentially large costs on the New Zealand economy – over a period (next few years) when things are likely to be difficult anyway – for little or no gain (given the strength and resilience of the banking system, of which she spoke, and the inability to commit to such capital standards for more than a few years ahead).