Yesterday afternoon the Governor of the Reserve Bank and the chief executive of the Financial Markets Authority released their report on bank conduct and culture. Despite highlighting several times in the report that this was really none of their business (of course they phrased it more bureaucratically: “neither regulator has a direct legislative mandate for regulating the conduct of providers of core banking services”), they’d spent an estimated $2 million of public money to mount their bully pulpit, lecture the banks, lobby for more powers for themselves. And yet, rather lost among the soundbites – especially those from the Governor loudly lamenting the apparent risks of “complacency” – was this simple summary (from the second page of the Executive Summary)

…culture and conduct issues do not appear to be widespread in banks in New Zealand at this point in time.

Perhaps these regulatory agencies should stick to their core responsibilities, assigned by law. Developing a culture of doing excellently what Parliament asked them to do, of being open and accountable to citizens, and avoiding overreaching their mandate (relying on implicit threats) would be good to see from both the Reserve Bank and the FMA. All government agencies should know their limits and stick within them. Perhaps their respective boards should be asking some hard questions of management.

Oh, and dealing effectively with complaints made against, or to, the agencies themselves would also represent quite a (welcome) change. Physician heal thyself.

But getting back to the report itself, the simple truth is that there just wasn’t much there. Not much economic analysis – just somewhat ad hoc “sermons” – no cross-industry comparative analysis, and not even the simple acknowledgement that in institutions run by human beings mistakes will be made from time to time.

Perhaps there is something in the line that it was rather a once-over-lightly review. Perhaps too neither institution really had a strong interest in finding serious problems – just enough for the Governor to advance his ambitions with more portentous lectures on how private businesses needed to run themselves better.

But it was well-known for months that the review was underway. There was plenty of opportunity for any serious systematic issues – whether in a single bank or across the system – to be brought to light by those adversely affected. And, as it happens, as part of the review the FMA and RBNZ commissioned a poll, surveying the experiences people had had with their own banks, and their trust in banks and the banking system. It isn’t clear from the published report how the (on-line only) sample was selected, but I thought the results were quite reassuring.

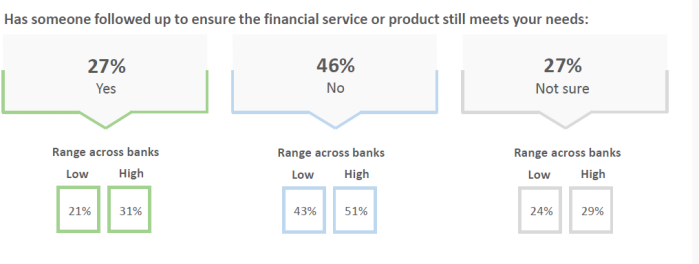

There was this summary, for example

It often seems as though every second shop I go into has staffed trained to attempt to sell products I don’t want or need (“City Council rubbish bags?” I’m routinely asked – and never buy – at the local New World), so if only a quarter of bank customers have had staff offer them financial products they don’t want or need, bank marketing must be a bit better targeted than I’d realised.

There is also a degree of unrealism about some of the questions. I’m quite sure that when I’ve dealt with my bank they have rarely put my long-term financial interests first. Why would they? They are a profit-maximising private business looking to maximise value for shareholders, but through a repeat-game business where alienating the customers is often detrimental to the longer-term interests of shareholders too. (And for many products the bank may have no idea what my “long-term financial interests” actually are.)

Or there was this question.

Q: ‘After purchasing a financial service or product, such as credit card, insurance, loan, term deposit, KiwiSaver, etc., has someone followed up to ensure the product continues to meet your needs and is still suitable for you?’

Surely even at best this is only a nice to have? Annoying calls from firms “just following up to see that everything is okay” have a cost (to the recipient too). And there is some (considerable) onus on customers. If I reflect on this question, I probably have a couple of credit cards I no longer need – and am paying a small amount to the ANZ for each year – and no one has rung to check whether they are still “meeting my needs”. But I don’t expect them to. I’m an adult.

I’m not totally laissez-faire on such matters. There are dangers that long-term contracts, hard to get out of, could be sold to people who simply don’t understand them. (Occupational pension schemes that people had no choice but to join are another example.) It is reasonable for society to have (legal) protections built into the system. But this report highlights precisely no systematic problems. The report briefly, and reasonably, mentions a class of “vulnerable customers”, but again it was not apparent that there are either systematic problems or easy solutions.

Perhaps the most publicised part of the report is the initiative by the FMA and Reserve Bank to try to get all banks to stop sales-related incentives for frontline staff. Given that the two institutions acknowledge that their legal mandates are limited it isn’t clear how much this is more than bluff, bravado, and a bit of pushing at an open door (some banks already being in the process of phasing out such incentives). I hold no brief for specific remuneration practices, but I was struck by how little actual analysis there was in the report, including the role of sales-based incentives in a whole range of other sorts of firms and industries. I didn’t explicitly check, but when I bought a car a few weeks ago I didn’t assume other than that the salesman would be benefiting personally if I happened to buy a car from him. No doubt he knew that I knew. There are risks, and one deals with them by some mix of dealing with reputable firms (invested in their brand), mechanic checks, and so on. It isn’t clear in what respect the FMA and the Reserve Bank think basic banking products are so different. There are no perfect ways of resolving agency issues (even within organisations), again something missing from the report. Then again, rhetoric is cheap and serious analysis is hard (and grabs fewer headlines).

One of the Governor’s consistent themes is that banks – and indeed private business more generally – are too short-term in focus. He never produces any evidence to support his claim, or to back his view that he is better placed than private shareholders and managers to appropriately factor in time horizons, conditioned on the huge uncertainty everyone faces. It shows through again in this report. There are several claims that banks are too focused on short-term customer value or satisfaction, but no evidence is adduced to support this. Frankly, I’d find it a little surprising if it were true. Lifetime customer value is an approach that has been around in the marketing etc literature for 30 years now (and the basic idea won’t been unknown prior to that), and if banks really were just prioritising the short-term presumably they’d run into trouble eventually? And yet New Zealand (and Australian) banks – outside the immediate post-liberalisarion period – have been both stable and profitable over many many decades, and haven’t even been losing customers to newer better providers more willing or able (or something) to meet customers’ long-term needs.

So, overall, I wasn’t impressed. From the beginning, the review looked like a bit of power and influence grab – especially by the new Governor, playing politics – bidding for more resources. It came at a time when the banks – legitimate private businesses (not, as the Minister of Finance put it this morning, operating as some sort of “privilege”) – were (and are) in a weak position to stand up for themselves (given the bad stories from Australia). And so banks, who face a market test every single day – not just the share market, but customers with the ability to take their business elsewhere – have to quietly put up with lectures from senior bureaucrats who’ve never faced such tests, never had to put their ideas or products to the market, deferentially swearing to go along and do as Orr and Everett say. And, of course, if the banks do end up having to put in place more reports, more systems, more compliance checks, well, the burden of regulation always falls less heavily on big established players than on small operators or new entrants. And so the big players – more deft at playing the political/bureaucratic games – don’t really have much to worry about. But customers might.

None of this is to suggest that ethics and morality (two words absent from the report)should be unimportant in business. Without them, the basis for trust – central to well- functioning markets and societies – is corroded and eventually lost. But it also isn’t clear that yet more mandated reports, yet more boxes to check, yet more rules to get legal sign-off on compliance with, is any sort of real substitute for the sort of personal and institutional integrity many hanker after. I’m a trustee of a couple of superannuation schemes, which the FMA is responsible for regulating, and I’m struck by the sheer cost and additional complexity new waves of rules add – even rules specifying the maximum number of words in one specific report – and the contrast between that and the likely value being added for members. And the improbability that the thicket of rules will really do much the stop the rogues. Or even to cultivate a culture of honour and decency – as distinct from formal compliance – among the promoters and adminstrators of such schemes.