Yesterday afternoon the Governor of the Reserve Bank and the chief executive of the Financial Markets Authority released their report on bank conduct and culture. Despite highlighting several times in the report that this was really none of their business (of course they phrased it more bureaucratically: “neither regulator has a direct legislative mandate for regulating the conduct of providers of core banking services”), they’d spent an estimated $2 million of public money to mount their bully pulpit, lecture the banks, lobby for more powers for themselves. And yet, rather lost among the soundbites – especially those from the Governor loudly lamenting the apparent risks of “complacency” – was this simple summary (from the second page of the Executive Summary)

…culture and conduct issues do not appear to be widespread in banks in New Zealand at this point in time.

Perhaps these regulatory agencies should stick to their core responsibilities, assigned by law. Developing a culture of doing excellently what Parliament asked them to do, of being open and accountable to citizens, and avoiding overreaching their mandate (relying on implicit threats) would be good to see from both the Reserve Bank and the FMA. All government agencies should know their limits and stick within them. Perhaps their respective boards should be asking some hard questions of management.

Oh, and dealing effectively with complaints made against, or to, the agencies themselves would also represent quite a (welcome) change. Physician heal thyself.

But getting back to the report itself, the simple truth is that there just wasn’t much there. Not much economic analysis – just somewhat ad hoc “sermons” – no cross-industry comparative analysis, and not even the simple acknowledgement that in institutions run by human beings mistakes will be made from time to time.

Perhaps there is something in the line that it was rather a once-over-lightly review. Perhaps too neither institution really had a strong interest in finding serious problems – just enough for the Governor to advance his ambitions with more portentous lectures on how private businesses needed to run themselves better.

But it was well-known for months that the review was underway. There was plenty of opportunity for any serious systematic issues – whether in a single bank or across the system – to be brought to light by those adversely affected. And, as it happens, as part of the review the FMA and RBNZ commissioned a poll, surveying the experiences people had had with their own banks, and their trust in banks and the banking system. It isn’t clear from the published report how the (on-line only) sample was selected, but I thought the results were quite reassuring.

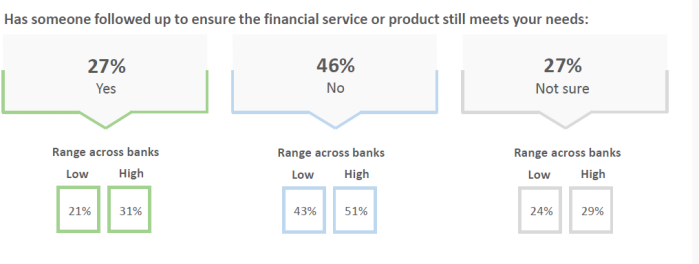

There was this summary, for example

It often seems as though every second shop I go into has staffed trained to attempt to sell products I don’t want or need (“City Council rubbish bags?” I’m routinely asked – and never buy – at the local New World), so if only a quarter of bank customers have had staff offer them financial products they don’t want or need, bank marketing must be a bit better targeted than I’d realised.

There is also a degree of unrealism about some of the questions. I’m quite sure that when I’ve dealt with my bank they have rarely put my long-term financial interests first. Why would they? They are a profit-maximising private business looking to maximise value for shareholders, but through a repeat-game business where alienating the customers is often detrimental to the longer-term interests of shareholders too. (And for many products the bank may have no idea what my “long-term financial interests” actually are.)

Or there was this question.

Q: ‘After purchasing a financial service or product, such as credit card, insurance, loan, term deposit, KiwiSaver, etc., has someone followed up to ensure the product continues to meet your needs and is still suitable for you?’

Surely even at best this is only a nice to have? Annoying calls from firms “just following up to see that everything is okay” have a cost (to the recipient too). And there is some (considerable) onus on customers. If I reflect on this question, I probably have a couple of credit cards I no longer need – and am paying a small amount to the ANZ for each year – and no one has rung to check whether they are still “meeting my needs”. But I don’t expect them to. I’m an adult.

I’m not totally laissez-faire on such matters. There are dangers that long-term contracts, hard to get out of, could be sold to people who simply don’t understand them. (Occupational pension schemes that people had no choice but to join are another example.) It is reasonable for society to have (legal) protections built into the system. But this report highlights precisely no systematic problems. The report briefly, and reasonably, mentions a class of “vulnerable customers”, but again it was not apparent that there are either systematic problems or easy solutions.

Perhaps the most publicised part of the report is the initiative by the FMA and Reserve Bank to try to get all banks to stop sales-related incentives for frontline staff. Given that the two institutions acknowledge that their legal mandates are limited it isn’t clear how much this is more than bluff, bravado, and a bit of pushing at an open door (some banks already being in the process of phasing out such incentives). I hold no brief for specific remuneration practices, but I was struck by how little actual analysis there was in the report, including the role of sales-based incentives in a whole range of other sorts of firms and industries. I didn’t explicitly check, but when I bought a car a few weeks ago I didn’t assume other than that the salesman would be benefiting personally if I happened to buy a car from him. No doubt he knew that I knew. There are risks, and one deals with them by some mix of dealing with reputable firms (invested in their brand), mechanic checks, and so on. It isn’t clear in what respect the FMA and the Reserve Bank think basic banking products are so different. There are no perfect ways of resolving agency issues (even within organisations), again something missing from the report. Then again, rhetoric is cheap and serious analysis is hard (and grabs fewer headlines).

One of the Governor’s consistent themes is that banks – and indeed private business more generally – are too short-term in focus. He never produces any evidence to support his claim, or to back his view that he is better placed than private shareholders and managers to appropriately factor in time horizons, conditioned on the huge uncertainty everyone faces. It shows through again in this report. There are several claims that banks are too focused on short-term customer value or satisfaction, but no evidence is adduced to support this. Frankly, I’d find it a little surprising if it were true. Lifetime customer value is an approach that has been around in the marketing etc literature for 30 years now (and the basic idea won’t been unknown prior to that), and if banks really were just prioritising the short-term presumably they’d run into trouble eventually? And yet New Zealand (and Australian) banks – outside the immediate post-liberalisarion period – have been both stable and profitable over many many decades, and haven’t even been losing customers to newer better providers more willing or able (or something) to meet customers’ long-term needs.

So, overall, I wasn’t impressed. From the beginning, the review looked like a bit of power and influence grab – especially by the new Governor, playing politics – bidding for more resources. It came at a time when the banks – legitimate private businesses (not, as the Minister of Finance put it this morning, operating as some sort of “privilege”) – were (and are) in a weak position to stand up for themselves (given the bad stories from Australia). And so banks, who face a market test every single day – not just the share market, but customers with the ability to take their business elsewhere – have to quietly put up with lectures from senior bureaucrats who’ve never faced such tests, never had to put their ideas or products to the market, deferentially swearing to go along and do as Orr and Everett say. And, of course, if the banks do end up having to put in place more reports, more systems, more compliance checks, well, the burden of regulation always falls less heavily on big established players than on small operators or new entrants. And so the big players – more deft at playing the political/bureaucratic games – don’t really have much to worry about. But customers might.

None of this is to suggest that ethics and morality (two words absent from the report)should be unimportant in business. Without them, the basis for trust – central to well- functioning markets and societies – is corroded and eventually lost. But it also isn’t clear that yet more mandated reports, yet more boxes to check, yet more rules to get legal sign-off on compliance with, is any sort of real substitute for the sort of personal and institutional integrity many hanker after. I’m a trustee of a couple of superannuation schemes, which the FMA is responsible for regulating, and I’m struck by the sheer cost and additional complexity new waves of rules add – even rules specifying the maximum number of words in one specific report – and the contrast between that and the likely value being added for members. And the improbability that the thicket of rules will really do much the stop the rogues. Or even to cultivate a culture of honour and decency – as distinct from formal compliance – among the promoters and adminstrators of such schemes.

I admit an almost pathological dislike of banks. I thought I was unique until I read Nassim Taleb say he had asked to be down-graded from business class so he could avoid being sat next to a banker.

The Keynes quote ““If you owe your bank a hundred pounds, you have a problem. But if you owe a million, it has.”” strikes a chord and the headline relating to UK banks “”World’s biggest banks face £264bn bill for poor conduct”” that related to “” residential mortgage bond securitisation mis-selling scandal is responsible for £66bn of the costs “”.

When ten years ago a NZ bank asked me if I wanted insurance for my mortgage I asked them what would they think if an insurance company attempted to sell banking services.

The problems with banks are much the same as the problems with poor beer and service at pubs in the centre of London – lack of repeat transactions by the same customers so effectively no free market competition. If you have no debt it is fairly easy to move banks in NZ. Over the years I have had mortgages with ANZ then ASB and now back to ANZ. Because of my psychopathic distrust of banks I object to anything other than great service and in recent years that is what I’ve had.

So with some reluctance I admit you are correct with your article claiming we have little to worry about. Your central point is “” banks, who face a market test every single day – … – have to quietly put up with lectures from senior bureaucrats who’ve never faced such tests””. Where our senior bureaucrats can serve the public is to assist the formation of new banks and to increase the power of local knowledge in banking.

As an example of the latter: I own two adjacent properties each with a house on it and I decided to transfer a 3rd of the bare land from one property to the other. The smaller property had a mortgage on it of about $200k and my bank decided I had pay for a valuation since the land size was not smaller – my counter point that a 3 bedroom house in Auckland North Shore with 500sm of land had to be worth well over $200k. All it needed was local knowledge rather than centralised rule following.

So no more regulations but let us have more competition with specialised local banks and finance firms – that may mean our govt persuading the big banks to share ATMs to help smooth a level playing field for new entrants and it may relate to your article about deposit insurance..

LikeLike

Interesting example re the valuation requirement. It is possible the RB LVR restrictions have reinforced silly requirements like that.

LikeLike

I find it totally rational to have it on the banks check list (especially since the property is held by a limited company) but a local person would know it’s irrelevance in this situation and ought to have the authority to overrule. However capitalism and the free market came to my rescue and to save maybe $300 and as a point of principle I moved my mortgage to anther bank.

Niall Ferguson in his ‘The Ascent of Money’ points out that the global financial crisis of 2007-2008 occurred because mortgages had been sold that owner occupiers were unable to service. The man in the street in Detroit knew it. Clearly the well paid management of Northern Rock bank and many other UK banks were simply too far away to know it.

I read somewhere that Germany’s economic success is based on the large number of small local saving banks – when they invest in a business they have local knowledge. Am I right in supposing South Canterbury Finance were successful until they invested in distant property?

LikeLike

I note today’s article on Stuff asking whether Kiwibank had failed in its objective to provide competition for the Australian banks. The main thrust of why it had not succeeded was down to either successive governments have failed to capitalized Kiwibank sufficiently, or “it’s only been 16 years, much of that time dealing with the effects of a recession – give it time to make its mark.”

LikeLike

I have to wonder why Kiwibank aren’t taking a far bigger share of the market and the billion dollar profits. I have a vague memory of the previous government taking a “dividend” similar to the one that was taken from Housing NZ. If it had been reinvested it seems certain there would have been huge benefits for the people of NZ (in both cases). Perhaps the government of the day had the same attitude to its citizens that banks have to their customers.

I did think the inquiry was going to actually look at the extremely high profits too. That seems to be the elephant in the room.

LikeLike

Profits were never going to be within scope. That is really a Commerce Commission issue, and in any case the RB is rather conflicted on that score: bank regulators focused on financial stability really like high and fairly stable bank profits.

LikeLiked by 1 person

The Australian banks have grown in NZ initially by acquiring existing and established NZ banks and have ended controlling most the $173 billion in depositors savings. Kiwibank was setup by the use of a postal service and government funding growing organically. It takes a lot of time and effort to grow organically.

LikeLike

Ironical really that the RBNZ should bellow forth telling others what to to do when it has been behaving in an even worse manner forever.

One thinks that they would do well to put their own house in order before making themselves look so foolish by demanding others do what they won’t.

Have they announced yet when they will give the board a proper role and what that will be?

Have they slipped into the conversation anywhere that they would obey the current law when it comes to OIA requests?

Have they announced with fanfare they will be more transparent and accountable to their owners, the taxpayer?

Have they managed to actually remoind themselves of their regulatory function and dispense with all the rest of the thnings they pontificate on that are not within their remit as the RBNZ as set out in the Law?

No I thought not.

Till they do they should not be in the business of telling others how to run theirs>

LikeLike

Did you see this Michael?

https://www.stuff.co.nz/national/politics/108379364/serious-storm-clouds-threaten-nz-democracy–report?

I wonder how healthy the narrative is these days. I see it as a twin engined jet. One engine powered by the 8% activist progressive (high and dry do-gooders) and Mike Hoskings on the other (property-construction sector). Adern is looking weak on China (she could be demonstrating Palmolive dish washing liquid) and yesterday a talk back host was raving about “positivity” and nuclear power. I have seen valid responses to all their positions but they hold the floor?

LikeLike

Yes, it was good to have Simon’s contribution. I agree with him on some points and, unsurprisingly, not on others. I guess societies tend to end up with the governments they deserve and, sadly, there doesn’t seem to be much strong or widespread demand for something much better or different.

LikeLike

I don’t think it is a case of what we deserve, I think it is a matter of dominant narrative. If a man in a suit is saying “NZ needs a bigger population” how is the ordinary person supposed to respond. Voices have been silenced through a hostile academic environment and in the media. There has been a veritable army devoted to the task?

John Carran, 2 April 1996

LikeLike

Not disputing your points, but NZ is a pretty passive country. There is little pushback and the citizenry doesn’t seem to demand much different. Elites argued for decades that Britain needed to be “in Europe” and yet, partly by happenstance but partly reflecting sustained public unease, the Brexit referendum happened, and won. Much as I dislike Trump, you could say the same for his electoral success in 2016 – went against almost everything the establishment, D and R, stood for. But it happened.

LikeLiked by 1 person

I think the “man in the suit” is being pushed by workers to find more workers. The Teachers Union and teachers want more teachers. They went on strike to get more pay and more time off. The Ministry of Education has shortlisted 500 new migrant teachers next year. I listened to one teacher from India correcting my daughters pronounciation on vegetables from “Veg’tables” to now “Vijitables”. I held myself back from walking into the class and correcting the migrant teacher from India. I think we should stick with Brits for teachers.

The police Union and police went on strike for more pay and more front line police. 1500 extra migrant officers has been touted. Already chinese faces fill the ranks of our police force. But they do look rather young and fresh out of undergraduate studies rather than the older and more experience police from other countries. Perhaps the immigration tightening of the private institutes has pushed these new low qualification graduates into joining the police to get their work permits.

Seems everybody is striking at the moment, bus drivers, truck drivers, nurses, midwives, train drivers, care givers all wanting higher pay and less working hours equates to more migrant workers.

LikeLike

Add young doctors who have raised the issue of 70 hour weeks and higher pay. The answer, of course is to go on strike as well for less hours and higher pay. Guess we bring in more migrant doctors as well.

LikeLike

“Cause Missed”

Someone in Letters to the Editor – Press (in response to that report) is blaming Energy Return on Energy Invested (ERORI) for a productivity decline. I am personally fond of the notion that a ship has an optimal crew (the regions have limited potential; developed countries reach a peak development – all else equal).

LikeLike

What is the optimal crew if they are aged 60 as an average? Does a geriatric crew need nurses and doctors as well?

LikeLike

GGS. If you try to solve an ageing population with migrants you finish up with a bigger population who are attempting to utilise fewer resources.It has been modelled by the UN etc.

LikeLike

Just pointing out that with your ship analogy you can always replace the crew with younger people and retire the older crew. But in a country you are somewhat stuck with the an aging crew without a replacement crew. The replacement crew just adds to the aging crew and with old age stretching longer and longer ie old people not dying, you have rather few choices other than to cull older folk or you do what the Japanese do, tie them up in their beds and inject sedatives. Or you have to go down the more migrant path as the more humane path to handling the old age and eventually dementia problem.

NZ is the size of Japan and it has one of the largest ocean boundaries in the world because it is a continent. It is definitely not short of resources. Anyway our 10 million cows(they eat and drop doo doo to the extent of 20 people) prove that we have the capacity to feed and handle as many as 200 million people. 90% of our produce gets exported feeding the rest of the world and not feeding ourselves.

LikeLike

There is a wider and ominous trend, which you can see in some statements circulating around this review, where regulators (either MP, ministers or bureaucrats) threaten regulation if certain perceived bad behavior is not remedied.

“FMA Chief Executive, Rob Everett said he could propose a “legislative intervention” to the Government if banks failed to significantly improve their behaviour.”

You see this type of statement quite often in the UK and Europe, particularly in the context of social media providers and their perceived ‘failure’ to regulate user content (i.e. speech). Sad to see it now appearing in New Zealand.

They are essentially saying, do what I want without regulation, or I will regulate to make you do it – it is a kind of mafia mentality at a legislative level (“nice business, shame if someone came and regulated it…”)

Surely this is a total attack on the rule of law and the function of regulation itself. The social media example shows the issue more starkly – the statements that facebook must urgently change its content moderation beg the question of whether speech ought to be regulated. These are deep philosophical questions (as is whether buyers and sellers should be free to bargain themselves) and at least the legislative process allows these topics to be raised and considered. Instead, the Orrs, Everetts etc can, as you say, sit and bully from their pulpit without the usual scrutiny.

I guess, in reality the bigger companies know this and can call the regulator’s bluff if they want to. But equally, these threats are not nothing and if ignored it only strengthens the arm of the regulators when it comes to regulate – the regulator can casts themselves as stoic defenders against cowboy companies who do as they please (i.e. act within the bounds of the prevailing law).

It also suggests regulation is something to punish and humiliate recalcitrant subjects, rather than being rules that have been developed, coolly and dispassionately, to deal with specific issues.

LikeLike

Thanks for those comments, with which I agree almost entirely.

LikeLike