Seven months (and counting) into his term as Governor, Adrian Orr still hasn’t deigned to deliver an on-the-record speech on either of his main areas of statutory responsibility (monetary policy and financial stability) but he has this morning done what it seems almost all new CEOs – public sector and private sector – now do, and restructured his senior management, ousting or demoting several top managers, elevating one or two, and opening up a raft of vacancies. Public sector senior management restructurings seem to generate most of the Situations Vacant business for the Dominion-Post newspaper these days.

A few people have asked my thoughts on the restructuring, so…..

As a first observation, I give credit to the Governor for resisting the temptation of across the board grade inflation (although there is at least one example, see below). Every public sector senior management advert one sees – I pay attention mostly because my wife has been in the market – is full of Deputy Chief Executive roles (not infrequently five or ten of them). The Bank’s Act constrains the number of Deputy Governor positions (only one, in the bill before the House at present) but if he’d wanted to, all these SLT positions could have been designated Deputy Chief Executive roles. As it is, having resisted title inflation, the Governor might find some potential applicants a bit more hesistant than otherwise: an Assistant Governor (even for Economics, Financial, and Banking) may sound less glamorous than a Deputy Chief Executive title.

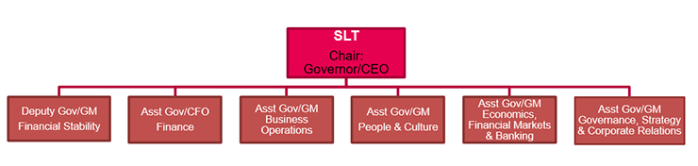

This is the new structure, which looks a lot like those for all manner of public sector organisations.

Three of those positions are filled straight away.

Appointments to Senior Leadership Team

Geoff Bascand – (Currently Deputy Governor and Head of Financial Stability) has accepted a role on the SLT as Deputy Governor and General Manager of Financial Stability.

Lindsay Jenkin (currently Head of Human Resources) has accepted a role on the SLT as Assistant Governor/General Manager of People and Culture

Mike Wolyncewicz (currently Chief Financial Officer and Head of Financial Services Group) has accepted a role on the SLT as Assistant Governor/ Chief Financial Officer Finance.

Of those two appointments (Bascand and Wolyncewicz) seem sensible and appropriate. Bascand currently holds a statutory Deputy Governor appointment and would have been hard to shift even if the Governor had wanted him out. His role is slightly – though perhaps sensibly – diminished as he will no longer have overall senior management responsibility for financial markets.

To be blunt, the new Assistant Governor for People and Culture has the feel of tokenism on two counts. The first count relates to the current tendency for HR managers to be given glorified titles and to report directly to the chief executive (the message supposedly being “we value our people”, as if organisations never did when HR was a fairly low-level support role). Line managers are the people who convey (by their actions mostly) to staff the extent to which they are valued (or otherwise). And the second relates to the incumbent, who just is not particularly impressive. As someone put it to me, perhaps she might be okay in some modest commercial operation, but she never showed any sign of being suited for a key leadership role in a significant policy organisation. But….she is a woman, and in promoting her Adrian Orr manages – after 84 years – to have a woman in a top tier role (although still not in a key role in policy or operational areas, the raison d’etre for the organisation). It will have been an easy win to simply grade-inflate the Manager, Human Resources role. After all, as he said a few months ago

We will be working actively. We are just going to have to be far more aggressive at getting the gender balance balanced,” Orr said in a recent interview

(And before I get angry emails or anonymous comments from past or present Reserve Bank staff, I will reiterate my view – and it is only mine – that there are no conceivable grounds on which Lindsay Jenkin would be in the top tier of a major policy organisation other than her sex. I wish it were otherwise.)

In the entire restructuring, the person one should probably feel most sorry for is Sean Mills, Assistant Governor and Head of Operations, whose job is dis-established and who is leaving the Bank, having joined under a year ago. I suppose he knew the risks – taking on a direct report job in the hiatus between Governors, when no one had any idea who the new Governor would be or what structure he or she would prefer. I’ve never met Mills, and have heard nothing good or bad about him, but it is always a bit tough to lose your job after less than a year.

Two long-serving key senior managers – both in their roles for 11 years now – are demoted as part of the restructuring, one perhaps a bit more obviously than the other.

The first is Toby Fiennes, currently Head of Prudential Supervision. His role – a big job – appears to have been split in two.

Toby Fiennes (currently Head of Prudential Supervision Department) has accepted the role of Head of Department for Financial Stability Policy and Analytics.

with one of his current managers (very able) taking up the role responsible for actual oversight of financial institutions.

Andy Wood has accepted the new role of Head of Department for Financial System Oversight.

I always had some time for Fiennes (although I’ve probably criticised speeches and articles here) and thought him in some respects the best of the main departmental heads. Perhaps it is just that the job has gotten so big that the Governor no longer wanted one person doing it, but the new role is much-diminished relative to what he has been doing for the last decade. And Geoff Bascand already had the key overall financial stability role, so there was no possible promotion opportunity.

The bigger, and more obvious, demotion is that of (current) Assistant Governor and Head of Economics, John McDermott.

John McDermott (currently Assistant Governor and Head of Economics) has accepted the role of Chief Economist and Head of Department for Economics in the Economics, Financial Markets and Banking Group.

After 11.5 years as a direct report to the Governor, and almost as long with the Assistant Governor title, McDermott loses both.

I’m always hesitant to write much about McDermott. He was my boss for six years, and while we had our differences we sat across from each other for years and exchanged views on all manner of work and family things. I liked him, was looking just the other day at the personal gift he gave me when I left the Bank, and I was genuinely pleased to applaud his daughter’s award the other night at the Wellington East Girls’ College prizegiving.

Unfortunately, I don’t think he was the person for the role he has held for eleven years, and which he never really grew into or made of that position what it should have become. He has a strong track record as a researcher, and apparently was for quite a while the most widely-cited New Zealand economics researcher, but the key senior manager for monetary policy – effectively a deputy governor without the title – required more than McDermott had to offer. In public view, this was apparent in speeches and Monetary Policy Statement press conferences. And thus, sad as it perhaps is for John, I think the Governor has made the right choice. Whether McDermott stays for much longer in the diminished position he will now take up perhaps depends a lot on who gets vacant (and crucial) new role of Assistant Governor for Economics, Financial Markets, and Banking).

Two other senior managers in core roles leaving the Bank

Mark Perry (Head of Financial Markets)…..elected to leave the Reserve Bank.

Bernard Hodgetts (Head of Macro-Financial Department, who is currently seconded as Director Reserve Bank Review in the Treasury) has also chosen to leave the Reserve Bank after he finishes his role leading the review.

The Head of Department for Financial Markets won’t be an easy role to fill – I wouldn’t have thought there were any obvious internal candidates.

Three more comments on the review:

- even if a role like “Assistant Governor, Governance, Strategy and Corporate Relations” is the sort of title one sees in lots of government agencies, it feels like another example of grade inflation. Presumably this involves the communications functions, the Board Secretary, and churning out the myriad hoop-jumping documents like the Statement of Intent. People with “strategy” in their title in public sector organisation are rarely at the heart of what the organisation do.

- there will be a lot of focus on who gets the role of Assistant Governor, Economics, Financial Markets, and Banking. This is (slightly) bigger role than Murray Sherwin held 20 years ago, without the benefit of the Deputy Governor title. We will have to wait until the adverts appear to see whether the Governor is after a policy leader (someone who really knows this stuff) or a generic public service manager. If – as I hope – the former, it has been speculated to me that the Governor may try to attract back to the Bank the current Treasury chief economist Tim Ng (whose talents would be better used doing almost anything than wellbeing budgets). Another possibility is the current Treasury deputy secretary for macro, Bryan Chapple who has a central banking background and led some of the financial markets reform work at MBIE. No doubt there will be others applying, especially as the holder of the position is almost certainly to be a statutory appointee to the new Monetary Policy Committee.

- this restructuring also probably helps clarify who will be the four internal members of the new Monetary Policy Committee. The Governor and Deputy Governor will be members ex officio, and it is hard to see how the other positions would not be given to the Assistant Governor, Economics, Financial Markets,and Banking) and to John McDermott, as head of the Economics Department.

Overall, the restructuring is quite a mixed bag. There are some good appointments and some poor ones already, and quite a lot will depend on a handful of the remaining appointments (especially the quality of person they can attract to that Assistant Governor role – which, notwithstanding my earlier cautions about grade inflation, really should be a deputy chief executive position, both for recruitment reasons and for the stature and standing of the person in international central banking circles).

If I have a caveat about the overall structure, it is probably that the Bank would be better for having at least one senior policy person – whether as Deputy Governor or so Advisor to the Governor – who didn’t have a demanding line management role. Such roles aren’t uncommon in other central banks, but I guess it depends on the Governor’s own preferred operating style.

And since I have the opportunity of a post about the Bank, I should note that I have not abandoned the issue of the Governor’s total non-transparency in respect of his speech about transparency to the Transparency International AGM (at which he was introduced by the State Services Commissioner, who has responsibilities for open government). I am pleased to see this issue has had a little bit of media attention, including this article which pointed out that 90 per cent of Transparency International’s funding comes from the taxpayer. I have an Official Information Act request in with the Bank for any briefing notes or text the Governor used, for any recordings that may exist, and if none do for a summary of what was said (memories – very fresh, since I lodged the request within hours of the Governor delivering his speech – are official information too. I don’t expect much, but there is a point to be made – all the more so given the topic, the audience, the introducer, and the funding source for the body to which he was speaking. I can’t imagine Orr said anything very controversial, in which case why the secrecy? And if what he said was controversial – foreshadowing for example Monday’s forthcoming culture review – it shouldn’t be said only to select private audiences. It was simply an unnecessary own-goal, some sort of silly reassertion (perhaps Wheeler like) of a Reserve Bank perception that it really should be above such trivial matters as disclosure, transparency and the Official Information Act.