First, some more kudos (albeit slightly ambivalent) to the Governor. As of this Monetary Policy Statement they have started publishing a spreadsheet with detailed quarterly forecasts for about 30 variables. I remain unconvinced of the value of such forecasting (especially up to 3.5 years ahead) – which has a non-trivial opportunity cost – but if they are going to do such forecasts it is only right that we should have access to them. The forecasts won’t be right but they will shed a little more light on how the Bank is thinking about how the economy is (or might) work, and the usefulness of the table will increase as a time series of such forecasts is built up. And one day perhaps they’ll develop sufficient confidence to release, with a lag, the staff background papers that contributed to the forecasts.

Watching the webcast press conference, it was curious to see the Governor introduce his chief economist with the description “the wisest man in the Reserve Bank”, just a few days after the Governor had stripped the same individual of his Assistant Governor title and demoted him – by putting another senior manager between McDermott and the Governor. Perhaps wisdom isn’t greatly valued at the the top of the Reserve Bank? More probably, it was just another cheap Orr line.

As I’ve noted previously, McDermott often isn’t that convincing in speeches and press conferences. We had another example yesterday. The Bank seemed to be a bit on the defensive over recent very short-term forecast errors, and this time I was mostly inclined to sympathise with them: there are significant uncertainty margins in how things are even measured, and you get the sense reading the SNZ commentary that (for example) even they don’t really believe the size of this week’s reported fall in the unemployment rate. But McDermott went on to over-egg things claiming, as if his name was really Pangloss, that “the outcomes for monetary policy are as good as it gets”, asserting that things were turning out just as planned. They had cut the OCR in 2016, we were told, and what we see is what you’d expect having done that.

I doubt the Governor was particularly taken with that line of argument. He – rightly – pointed out several times that inflation is still below the target midpoint, and their job is still to get it back up. They need considerable capacity pressures to achieve that.

Of course, there is a modicum of truth in what McDermott had to say. Having stuffed things up in 2014, raising the OCR when it wasn’t needed (with the full support of McDermott, as yesterday’s chart on the advice to the Governor confirms), they had to cut the OCR, by quite a lot in the end. Do that and of course you should expect inflation to pick up gradually – take your foot off someone’s throat and they start breathing more freely again too.

But, of course, the Bank has been telling us for years that they are aiming to get inflation back to 2 per cent, and it was the year to December 2009 that their (often preferred) sectoral core factor model measure of inflation was at 2 per cent.

The Bank doesn’t publish forecasts of core inflation, but the medium-term inflation forecasts they do publish are good proxies (since two years out one doesn’t usually know about petrol price or tax shocks that throw headline inflation around). Two years ago, at the end of the Bank’s OCR-cutting phase, they forecast that (core) inflation would be back up to 1.9 per cent by now. In fact, it was only 1.7 per cent in the year to September. A year ago, in the November 2017 MPS, they were forecasting inflation would be either 1.9 or 2.0 per cent in all their medium-term horizons. But in the latest projections they don’t seem to see (core) inflation back to 2 per cent until mid-2020, long enough that they will have been below the target midpoint for more than a decade.

Perhaps one shouldn’t cavil too much about current outcomes, but it has been an awfully long time coming, and the wait needn’t have been anywhere as long if the Reserve Bank’s senior managers had been doing their job better. Oddly, I also heard the Governor twice suggest that “only six months ago people were suggesting we weren’t doing our job [and should have cut]”. I’m not sure who he is referrring to here – I don’t recall a groundswell of calls for rate cuts six months ago – but if I’m among those he is responding to, I hold to my view: we would have had better inflation outcomes (the primary job of the Bank) had the OCR been lower in 2016 and 2017. (That isn’t the same as saying I’d cut right now.)

And eight or nine years into this economic expansion, it isn’t as if the Bank is well-positioned should another serious recession come along soon. The Governor was asked again about this yesterday, and gave his (now customary) complacent response. There was, we were told, nothing to worry about. The OCR didn’t really matter that much, because it was not much more than happenstance that that was the instrument currently being used. There was lots of handwaving, and (still) not a lot of convincing argumentation. And never an acknowledgement that if other countries are even somewhat constrained (or feel they are) that will markedly worsen the environment we face. Perhaps one day the Governor could devote a speech to the subject, or is he not ever going to do a speech on what is, still, his primary statutory responsibility?

There was reference again to a Bulletin article the Bank published a few months ago, which I wrote about here. I stand by my conclusion

In summary, I welcome the fact that the Reserve Bank has begun to talk more openly about the potential limitations in its response to the next recession, but it is disconcerting that they still seem to be trying to minimise the potential severity of the issue. In that, they aren’t alone. I’m not aware of any central bank that has yet laid out credible plans to minimise the damage (although senior officials of the Federal Reserve have been more willing to talk about the issues openly). In that, they are doing the public a serious dis-service, and risking worse outcomes than we need to face – repeating the sort of reluctance to address issues that saw the world drift into crisis in the early 1930s. Fortunately for the central bankers perhaps, it won’t be central bankers personally who pay the price. That won’t be much consolation for the many ordinary people who do.

Since politicians, and not central bankers, are accountable to the voters, the Minister of Finance should be taking the lead in requiring a more pro-active (and open) set of preparations to be undertaken by the Reserve Bank and The Treasury.

(There was also a brief exchange – not entirely audible on the webcast – about a peculiar episode in the last recession when it appeared that the Bank had convinced itself the OCR couldn’t safely be cut below 2 or 2.5 per cent. I was at The Treasury at the time and when we heard of this stance, it struck us as distinctly odd. The argumentation – repeated yesterday – apparently was that if they cut further the exchange rate could fall very sharply. And yet in an open economy, with well-hedged foreign debt, a fall in the exchange rate is a natural and normal part of the stabilising transmission mechanism. I mention it here mostly as an example of the sort of central bank caution – here and abroad – that has contributed to such weak inflation over the last decade and (at the margin) at muted recovery. Even if the specific floor has changed, it isn’t clear how much the mindset has.)

Perhaps one of the most interesting aspects of the projections yesterday was the inflation numbers. Usually – for decades now – the published projections for inflation have involved a gradual return towards the midpoint of whatever the inflation target range is at the time. Sometimes that return path looked rather slow – in the Bollard years when core inflation was around 3 per cent, Alan was happy enough to publish projections showing inflation only back to 2.5 per cent at the end of the forecast horizon – but it was, almost without exception, a convergent process. If you were starting from 3 per cent with a target midpoint of 2 per cent, the end-point forecasts were 2 or a bit above, not (say) 1.8. And the same when, as in recent years, the starting point has been below the midpoint.

But not now. Here are the medium-term inflation projections (those two and more years ahead), which monetary policy can do a lot about if it chooses.

Mostly – and the more so the further out – above 2 per cent. Looking back a couple of years I did find an MPS where the final projections were at 2.1 per cent, but it was clearly a case where the then-Governor had chosen to portray a dead-flat OCR track. By contrast, in these latest projections the OCR has risen by 66 basis points by the end of the forecast horizon.

The Bank doesn’t seem to have explained quite why it (well, the Governor) is making this choice, which is clearly a conscious and deliberate one. There seem to me to be two possibilities:

- the first is that, given the new employment dimension to the mandate, and that they had expected unemployment to stay around 4.3 or 4.4 per cent for the next 18 months (prior to this week’s HLFS numbers), the Governor was deliberately choosing to prioritise further reductions in unemployment over meeting the midpoint inflation target, or

- alternatively, given the risks going into the next recession he is deliberately aiming for inflation in the upper half of the inflation target range to pull inflation expectations up more securely, and provide more leeway in the next recession.

There were hints of something along these lines in the reports of the off-the-record speech Orr gave on such matters a few months ago, but we’ve had nothing open and official. That isn’t good enough.

(I’m quite comfortable with leaving the OCR unchanged at present – relative to the alternative of signalling an early tightening – as I’d still be surprised if, between domestic pressures and external threats, we saw anything like the growth the Bank is forecasting over the next year or two. But the actual policymaker owes us a more considered explanation for the choices and tradeoff he personally is making with our economy.)

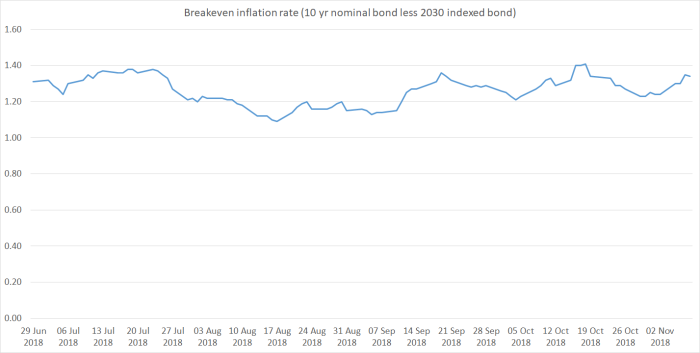

And whatever the explanation, the Governor clearly has some way to go to convince people putting their money on the medium-term inflation outlook. Here is the chart of the breakeven inflation rate from the government bond market for the second half of this year.

The data are up to yesterday, so include both the unemployment and MPS news. Expectations of medium-term inflation, as reflected in market prices, remain stubbornly low.

As I said at the start of this post, the new table of forecast data the Bank is releasing enables to illustrate a little more clearly how the Bank thinks things are working. For example, this chart shows their projections for quarterly growth in potential output and for annual net immigration (working age population) – the latter being a series we won’t even have on any sort of timely basis in another month or so.

Population growth (of working age) is one of the biggest single contributors to any sense of what potential output growth might be. But the Bank expects the net migration inflow to more than halve, while potential output growth is barely changed. (And for anyone who responds “but isn’t that what you say we should expect”, the Bank’s forecasts have no further reduction in the exchange rate and has, in time, increases in real interest rates.) Using their GDP and employment forecasts, productivity growth (GDP per person employed) averaged 0.6 per cent per annum over the last decade, has been non-existent over the last couple of years, but is expectedly to rebound strongly to around 1.5-1.6 per cent per annum in 2020 and 2021. Without any real sense of the channels at work that might bring about this startling rebound, it feels like little more than wishful thinking. That isn’t new – I’ve highlighted in repeatedly, under both Wheeler and Orr. It might even be convenient for the government, but only until – most probably – the outcomes again disappoint.