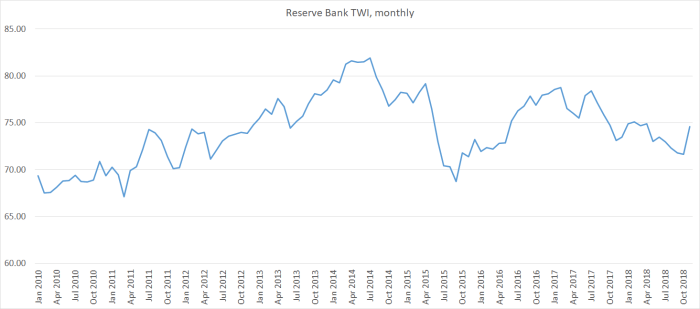

It doesn’t seem long – and, in fact, it isn’t long – since people were squabbling over a bit of a fall in the exchange rate. The National Party was blaming the Labour-led government, while the government seemed to be taking some credit for the fall and talking about a rebalancing of the economy that they claimed was underway. To support their claims, they not infrequently invoked the support of the rather left-wing Governor of the Reserve Bank.

And now they’ve all gone quiet again as the exchange rate has rebounded again. On the Reserve Bank’s TWI measure, the rebound has been about 6 per cent. Even by the standards of this decade – when the exchange rate has been reasonably stable – it isn’t that big a move.

The level now is about the same as the level at the time the choice of the new goverment was decided in October 2018. It poses new fresh inflationary threat (which seemed to be the National Party concern when it was falling) and no greater buffering, or signal of rebalancing, as the government and the Governor had liked to claim.

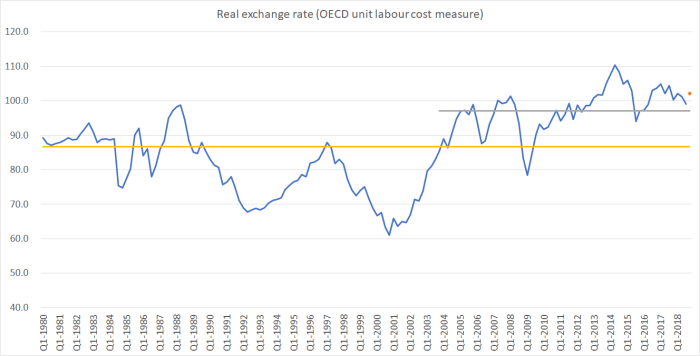

What of longer-term comparisons? Here I like to use the OECD’s real relative unit labour cost measure – partly because there is a long run of data. Here is how the longer-term picture looks (the dot representing today’s estimated level).

On average, the real exchange rate has been high since around 2003 (with a sharp but shortlived dip in the 2008/09 recession). Even the lows the Prime Minister and Governor liked to talk up had still been a bit above the 15-year average (the grey line); current levels even more so.

But I’ve also shown (yellow line) the average for the entire period since 1980. The current level of the real exchange rate is about 18 per cent above that long-term average.

That would make sense, and be welcome, if – for example – the last 35+ years had been ones in which New Zealand had been chalking up a stellar productivity growth performance, if New Zealand firms had been successfully many more foreign markets lifting the foreign trade share of the New Zealand economy. But, of course, that hasn’t been the story at all. There were short periods when it sometimes looked as if these sorts of developments were actually happening, but they’ve never lasted, and none of those periods have been in the last 15 years (when the real exchange rate has consistently averaged high). Instead, our productivity levels have drifted further behind those in other advanced economies – including, notably, over the last five years when there has been little productivity growth at all – and foreign trade shares of our economy have stagnated and then shrunk. Indicators of the relative size of the tradables sector of our economy have also not been encouraging.

These aren’t developments that should leave anyone very comfortable. In the shorter-term, there isn’t much obvious impetus for strong domestic growth – commodity prices are easing, confidence is weak, population growth is ebbing – and the risks to the global outlook seem to be mounting, and perhaps even crystallising. Then again, if things go badly wrong in the short-term, the exchange rate can – and probably will – move quite quickly.

The bigger concern is that there is no sign of an economy rebalancing towards some better – higher productivity, more outward-oriented, tomorrow. And the persistently high exchange rate, over decades, seems to have been reflecting deeply misguided policies that have helped produce the last few decades of disappointing economic performance, all combined with a depressing indifference from the leading figures in all our main political parties. There is little chance of breaking out of the slow spiral of continued relative decline without a quite materially different approach. Part of making that work would be likely to involve the real exchange rate revisiting – settling – the sorts of lows we experienced at times in the first 15 or so years after liberalisation. Even back then, when senior figures talked of rebalancing, it was mostly wishful thinking – since the lows were purely the results of short-term cyclical forces. These days, such talk bears even less relation to reality – and to the scale of the challege before us. But perhaps it generates a favourable news story for a day or two.