It doesn’t seem long – and, in fact, it isn’t long – since people were squabbling over a bit of a fall in the exchange rate. The National Party was blaming the Labour-led government, while the government seemed to be taking some credit for the fall and talking about a rebalancing of the economy that they claimed was underway. To support their claims, they not infrequently invoked the support of the rather left-wing Governor of the Reserve Bank.

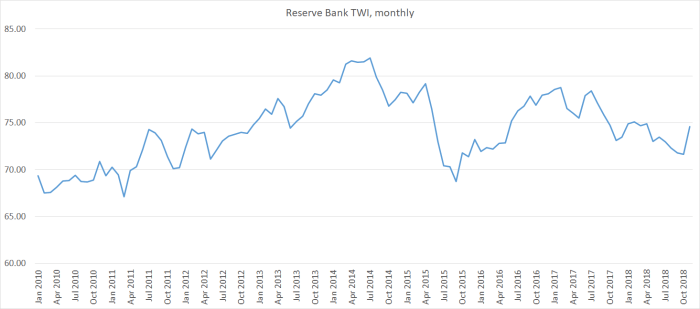

And now they’ve all gone quiet again as the exchange rate has rebounded again. On the Reserve Bank’s TWI measure, the rebound has been about 6 per cent. Even by the standards of this decade – when the exchange rate has been reasonably stable – it isn’t that big a move.

The level now is about the same as the level at the time the choice of the new goverment was decided in October 2018. It poses new fresh inflationary threat (which seemed to be the National Party concern when it was falling) and no greater buffering, or signal of rebalancing, as the government and the Governor had liked to claim.

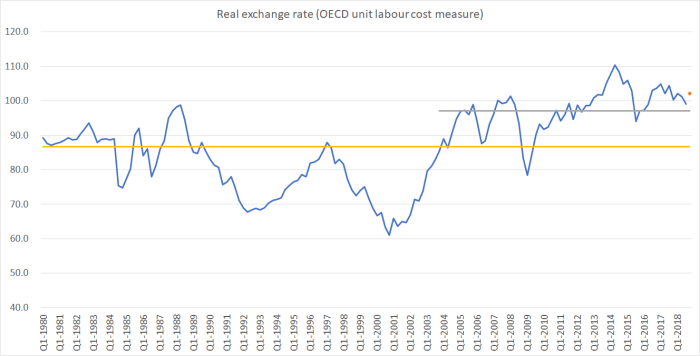

What of longer-term comparisons? Here I like to use the OECD’s real relative unit labour cost measure – partly because there is a long run of data. Here is how the longer-term picture looks (the dot representing today’s estimated level).

On average, the real exchange rate has been high since around 2003 (with a sharp but shortlived dip in the 2008/09 recession). Even the lows the Prime Minister and Governor liked to talk up had still been a bit above the 15-year average (the grey line); current levels even more so.

But I’ve also shown (yellow line) the average for the entire period since 1980. The current level of the real exchange rate is about 18 per cent above that long-term average.

That would make sense, and be welcome, if – for example – the last 35+ years had been ones in which New Zealand had been chalking up a stellar productivity growth performance, if New Zealand firms had been successfully many more foreign markets lifting the foreign trade share of the New Zealand economy. But, of course, that hasn’t been the story at all. There were short periods when it sometimes looked as if these sorts of developments were actually happening, but they’ve never lasted, and none of those periods have been in the last 15 years (when the real exchange rate has consistently averaged high). Instead, our productivity levels have drifted further behind those in other advanced economies – including, notably, over the last five years when there has been little productivity growth at all – and foreign trade shares of our economy have stagnated and then shrunk. Indicators of the relative size of the tradables sector of our economy have also not been encouraging.

These aren’t developments that should leave anyone very comfortable. In the shorter-term, there isn’t much obvious impetus for strong domestic growth – commodity prices are easing, confidence is weak, population growth is ebbing – and the risks to the global outlook seem to be mounting, and perhaps even crystallising. Then again, if things go badly wrong in the short-term, the exchange rate can – and probably will – move quite quickly.

The bigger concern is that there is no sign of an economy rebalancing towards some better – higher productivity, more outward-oriented, tomorrow. And the persistently high exchange rate, over decades, seems to have been reflecting deeply misguided policies that have helped produce the last few decades of disappointing economic performance, all combined with a depressing indifference from the leading figures in all our main political parties. There is little chance of breaking out of the slow spiral of continued relative decline without a quite materially different approach. Part of making that work would be likely to involve the real exchange rate revisiting – settling – the sorts of lows we experienced at times in the first 15 or so years after liberalisation. Even back then, when senior figures talked of rebalancing, it was mostly wishful thinking – since the lows were purely the results of short-term cyclical forces. These days, such talk bears even less relation to reality – and to the scale of the challege before us. But perhaps it generates a favourable news story for a day or two.

Michael I know that you are of the opinion that the housing crisis is an inequality problem rather than a productivity one. I believe it is both as the housing market affects the proper functioning of the labour market.

Anyway it looks like progress is being made by the current government on a number of housing fronts. Legislation for infrastructure financing via targeted rates and bond financing is coming as is legislation for Urban Development Authorities.

I have written about the implications of this for integrated land-use and infrastructure provision for Greater Christchurch here.

View at Medium.com

LikeLike

Auckland’s productivity is lower than most major cities mainly due to the lack of a financial services hub. Most major cities are essentially financial services hubs where computers generate the income flows. Each trader can be managing billions of dollars in funds to generate hundreds of millions in sales income. No matter how many houses you build you will never get that level of productivity.

LikeLike

Inequality problem, is that wrong? I thought Michael’s preferred opinion is Land Use regulations and restrictions that has resulted in a housing shortage.

LikeLike

Thanks Brendon. I remain a bit sceptical of UDAs (and esp the proposed eminent domain powers).

LikeLike

My question would be whether the incoming capital flow from cashed up immigrants (and some hot money) has distorted the real value of the dollar.

The next question is whether there will be a corresponding drop when or if the people flow reverses.

LikeLike

The nature of the NZD buying has consistently been the unwinding of speculative “short-sold NZD” positions. Inevitably, once the fall in the Kiwi has abated, it is only a matter of time before the speculators lose patience and buy-back the Kiwi dollars they had earlier sold. Swift Kiwi appreciation is the result of large volumes of NZD buying but in a restricted volume market.

https://www.interest.co.nz/currencies/96944/roger-j-kerr-says-nz-dollar-now-likely-go-above-us70c-coming-weeks-speculators

LikeLike

The amounts involved (what migrants bring) are mostly pretty small these days – many migrants are quite young – so won’t be directly affecting the exchange rate. my argument has been that building the physical capital stock that migrants need puts additional and sustained pressure on real interest rates and the real exchange rate.

LikeLike

I thought it was Land use regulations and restrictions that lead to lack of supply that puts upward pressure on prices that puts additional and sustained pressure on real interest rates and the real exchange rate?

A Northland boatyard owner has been dealt a major blow after his resource consent applications for various works were declined by independent commissioners which he has been operating now for 40 years.

https://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=12162153

LikeLike

“” building the physical capital stock “” applies to places that are growing such as Auckland. And NZ cities are growing partly because of foreigners arrive but also because of a rapid movement from rural to urban. Surely it makes little economic difference if someone moves from a village in India or China to Auckland than if they move from Dargaville.

Your conomists eye sees agricultural mechanisation and automation as inevitable and therefore to be encouraged. However NZ economy depends on what happens in rural areas and our best export opportunities are inventing new uses for no8 wire – businesses closely related to agriculture (why do I have to buy Danish blue cheese that comes from Denmark?). It is hard to get entrepreneurs to live in the country when the last local pub, school and church closes. It also has a social cost.

We don’t need a Shane Jones with a Provincial Growth Fund (in PNG it would be called a slush fund – pity no local had ever experiences slush and the way the purity of snow becomes unpleasant, dirty and slippery dangerous) but quiet longterm investment outside our cities would be wise. They achieved it in the past – when Ardmore was a remote village it was where student teachers trained; now I think they may go to Epsom.

Why does NZ spend so much on infrastructure in Auckland when the same expenditure on buildings and roads would produce double the results elsewhere? Growth of our cities is inevitable but it would be done better more slowly and that may help your interest rates and real exchange rate.

LikeLike

The beauty of MMP has a combination of 2 components ie the electorate vote which would have favoured the regions under FPP and the Party vote which is based on the number of people. Since a city like Auckland has 1.7 million people, that is 37% of the voting public in one city. That moves the power centre to Auckland.

LikeLike

The middle of the night and I had to search Google for the meaning of ‘Real Exchange Rate’. An IMF website explains it in terms of Big Macs and also states ” the economics profession itself lacks a foolproof method of establishing when a currency is properly valued “.

You say NZ’s real exchange rate has been high since 2003 (the year I arrived but I don’t think I am responsible) but on your graph it appears that the average is just below what is presumably the base line 100. Surely that means on average our prices are about right – there is no incentive to buy from abroad because our prices are only slightly lower than an international average.

You say about a rapid 6% change in our nominal exchange rate [my brain wants to call it ‘real’ because when I change currency that is the reality] is a rebound and “isn’t that big a move”. Yesterday I visited a friend who sells second hand machine parts internationally with sales invariably in US dollars and with over 10,000 competittors world wide; he has a very different attitude to that 6%.

To the extent that a govt can manipulate exchange rate it would seem sensible for countries searching for export growth to keep their exchange rate low: many imported goods are discretionary as are foreign holidays so it would keep them down and drive exports up and although the population would be poorer the economy would boom. Is that what Japan, South Korea and then China have done? If our real exchange rate was lower it sounds as if it would help NZ grow by excouraging exports but wouldn’t it also mean elderly baby boomers being less well off and having to curtail our endless foreign holidays (or are they paid for by downsizing while house prices are irrational?).

LikeLike

Two quick points:

– the 100 is just the standardised basing the OECD used for all the individual country indexes (it has no independent meaning),

– re the 6% move, yes agree it can make quite a difference to individual firms. My comment was only in reference to the normal size of fluctuations historically.

On your final sentence, yes that captures it quite well. The other way of framing it is that current policy is, unintentionally, oriented to support ageing baby boomers etc at the expense of coming generations (who can’t afford to buy houses, and suffer from the productivity growth that never was).

(As a teaser, there is a PNG post coming this morning)

LikeLike

That exchange rate is real enough for us oldies. I have been looking at Lufthansa flights into Athens, Greece for Christmas and then onto Munich for the New Year. The lift in the NZD translated to a overnight savings of almost $150 for 3 people. That is a nice dinner in a nice restaurant somewhere in Athens already with that sudden lift in the NZD.

LikeLike

The difference with Japan, Korea and China is that they needed their currencies low to attract investment in manufacturing infrastructure to attract foreign intellectual property.

NZ develops high end intellectual property but does not invite investment in manufacturing in NZ. Instead it sells up its the intellectual property to overseas buyers who then uses that intellectual property in manufacturing outside of NZ. eg Rocketlab, whereby Peter Beck and Stephen Tindall Foundation sells up for $200 million to a US corporation who then values the business in excess of US$1 billion (which ACC has invested at a premium) to manufacture in the US and UK, ship the rockets back to NZ for weekly rocket launches.

The Accident Compensation Corporation of New Zealand (ACC) is now an investor in Rocket Lab, the US rocket technology company founded in New Zealand. The company has now raised more than US$288 million to date, soaring past its previous US$1 billion-plus valuation.

https://www.newshub.co.nz/home/money/2018/11/acc-joins-rocket-lab-s-multimillion-dollar-investment-round.html

LikeLike