You might idly dream – or hope, increasingly desperately, for your own sake (younger readers), or for your children or grandchildren – that one day real house prices might be sustainably lower again. There is no good or defensible reason why they shouldn’t be. It is just that our political “leaders” choose to keep on doing nothing real about it. From time to time some of our politicians talk a good talk about fixing this national disgrace – once upon a time the current Minister of Housing was foremost among them (embraced even by the libertarians at the New Zealand Initiative) – but then do nothing, or attempt to distract us with interventions that have little or nothing to do with the real problem.

The Tax Working Group’s report, out last week, assumes this state of affairs goes on indefinitely. Why do I say that? Because in the revenue projections they include in the report (and on which they construct a case for permanent income tax cuts):

- the bulk of the revenue is from gains in urban property prices (land and buildings), and

- they assume that property prices rise (indefinitely) at 3 per cent per annum, only 2 per cent of which is general consumer price inflation.

Since actual physical buildings experience real depreciation, and since over the long term construction costs are unlikely to rise at a rate much different than general CPI inflation, the implicit assumptions seems to be that urban land prices will rise even faster. (It has never been clear to me how anyone thinks they can safely forecast real asset prices, let alone plan responsible tax policy on such forecasts, but set that to one side just for the moment.)

So most of the revenue would arise from general consumer price inflation – which simply shouldn’t be taxed (since no one is better off as a result; there is no addition to purchasing power) – and the rest apparently from assuming that the rigged (by central and local government) housing market continues to get even more out of line. If we are going to have a capital gains tax on urban property, perhaps the government could at least consider using any proceeds to compensate the generation put in an ever-more-impossible position by their own policy choices/failures? Alternatively, if the government (Mr Twyford) really is still serious about fixing the housing market – and he claims to be so – they need to recognise that there will be little or no revenue from a capital gains tax for a very long time. In principle, the ability to deduct capital losses from other taxable income would actually make it a net drain on the public finances were anything serious ever to be done about fixing the housing market (investors, but not owner-occupiers, would be partly compensated for their losses, upending most people’s sense of fairness).

There is a choice:

- reasonable amounts of revenue, much of it plundered by taxing inflation compensation, if the rigged housing market is allowed to continue, while doing nothing to compensate the actual losers from that (governmentally) distorted housing market,

- or little or no revenue (perhaps even net fiscal costs) if a government ever gets serious and fixes the housing and urban land market.

Reading the entire report yesterday, and even going back to read the interim report, I was struck by how thin and weak the economic analysis in the document was. As someone noted to me yesterday, it had a strong feel of something in which the working group started with a conclusion and went pretty much straight to how to write rules, without thinking about the underlying economics. I noted a year ago how little any concerns around productivity (lack of it) figured when the Tax Working Group set out their plans. And they delivered – there was very little about those considerations in their reports. Not even a recognition that, for all the talk about reallocating investment, if anything probably too few real resources have gone into housebuilding over the years not too many (given the growth of the population).

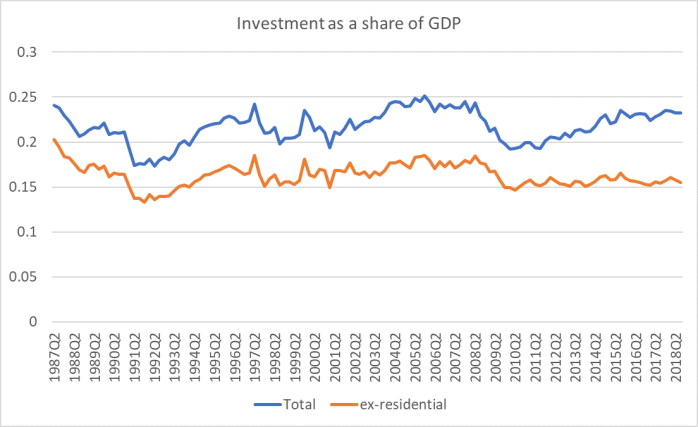

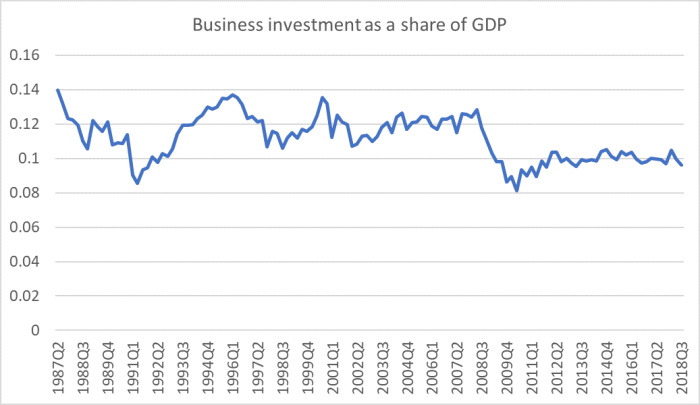

There was lots of focus on raising more revenue, and little on the low rates of business investment we already have, or on the way in which we tax much of capital income more onerously than almost any other OECD country. The idea of fixing inflation distortions directly didn’t get much space either. The current system bears very heavily – and quite unjustly – on people holding savings in the form of bank deposits, and it also gives away money, totally unnecessarily (and without economic justification) to business borrowers. Allow deductions of interest expenses only for the real component of any interest rate – it wouldn’t be that hard to do – and you’d both improve efficiency and get more money out of leveraged property investors (and in ways that didn’t rely on a continued rigged market).

The economic analysis around the proposed capital gains tax itself was also weak – I’d say “surprisingly weak”, but there was an agenda going into this review, so I can really only say “disappointingly weak”. I know I saw no mention of the idea that most real capital gains (and losses) are windfalls (since markets tend to price assets efficiently on the information available at the time) – and that, in the case of windfalls, a capital gains tax is pure double taxation. I don’t think I saw a single mention anywhere of the fact that, if these recommendations are adopted, New Zealand will have probably the very highest rate of capital gains tax in the world. The discussion of the lock-in problems around capital gains taxes was threadbare – it was noted, but there was no sustained analysis, no careful discussion of various published studies on the effect, and nothing linking back to the fact that if our CGT rate is the highest in the OECD, our lock-in problems are likely to be more significant. There was little or no serious analysis of the potential impact on entrepreneurship and innovation – and certainly nothing that put that issue in the context of an economy with low rates of business investment.

There was also nothing at all about the incentives a realisations-based CGT creates for assets to be held not by those best able to utilise them, but by those least likely to have to face a CGT charge and those best-placed to utilise any losses: capital gains taxes (like ring-fencing, like the PIE regime) will create more of an incentive for more assets to be held by institutions, foundations etc, rather than directly by individual investors, not because those institutions are better managers or owners, but because they are less likely to have to crystallise a CGT liability. Tax policy for the big end of town.

And, of course, there was nothing about the systematic asymmetry built into the system, in which gains are fully taxed (when realised) but many losses may never be able to be fully utilised. Take two separate businesses each valued at $100 million on the day the CGT is implemented, both owned by individuals who are 55. Over the following decade, one business does well and when the owner comes to retire he sells it for two hundred million dollars. He is liable for CGT on that gain. The other business does poorly and when the owner comes to retire, there is little or no value left in the business. In principle, he can offset that capital loss against other income, but at 65 it is very unlikely that over the remainder of his life he will anywhere near enough income to fully utilise those losses (and even if he does, there is a further – perhaps lengthy – time delay). In fact, the TWG proposes that some losses could only be used to offset other losses in that same sort of activity (not against, say, labour income). Since the nature of a market economy is that some businesses do well and others don’t, mine isn’t at all an implausible scenario. There might be a decent case (in equity, although not in efficiency) for taxing windfalls etc if the treatment of losses was fully symmetric – the government then would be a pure equity stakeholder in all businesses – but that isn’t what is proposed.

And finally, I was also struck by how threadbare was the discussion around the New Zealand Superannuation Fund. That organisation appeared twice in the report. The first was this bid.

35. The New Zealand Superannuation Fund (NZSF) has suggested the use of a limited tax incentive to spur investment into Government-approved, nationally significant public infrastructure projects that would benefit from unique international expertise.

36. NZSF suggested that investors pay a concessionary rate of 14% (i.e. half of the

current company rate of 28%) on profits made in New Zealand from qualifying projects. Qualifying investors would need to have a demonstrated capability to deliver world-class infrastructure projects; they would also need to bring expertise that is not ordinarily available in New Zealand and commit that expertise to the delivery of the infrastructure.

37. NZSF’s suggestion has merit. The Group recommends that the Government consider the development of a carefully designed regime to encourage investment into large, nationally significant infrastructure projects that both serve the national interest and require unique international project expertise to succeed.

I wrote about this bid when NZSF first published their submission. I wrote then that

I’m all in favour of lower company (and capital income) taxes more generally. Standard economic analysis supports that sort of policy, and all of us would be expected to benefit from adopting such a policy approach. But that isn’t what is proposed by NZSF; it is just a lobbying effort to skew capital towards particular sectors they happen to favour. It is a pretty reprehensible bid to degrade the quality of our tax system. There is no economic analysis advanced in support of their proposal – so little it almost defies belief – no sense of considerations of economic efficiency, just the success of lobbying efforts in a few other countries (including two struggling middle income countries not known for the efficiency of capital allocation or quality of governance, and the United States – which not only has plenty of poor infrastructure, but a corporate tax code riddled with exemptions and distortions).

Same goes for the Tax Working Group’s treatment of the issue. We deserve better.

The second substantive issue in which NZSF is mentioned is around the tax liability of NZSF itself.

56. During its discussions on retirement savings, the Group noted the oddity that the NZSF must pay tax to the New Zealand Government. The NZSF reports that it paid $1.2 billion in tax, or 9% of New Zealand’s corporate tax take, in the 2016-17

tax year.

That is a good thing. It helps to ensure that the NZSF – operating at arms-length from the government of the day – faces the same incentives as any other New Zealand investor. Were it not so the ownership structure of various assets could look quite different, since NZSF would be in a position to pay more than other potential investors for any particular asset, not because they would be better owners, but just because they were tax-favoured.

There does appear to be a small substantive issue, relating to NZSF’s activities overseas

It is more difficult to argue that the NZSF should benefit from sovereign immunity when it is subject to tax in its home jurisdiction. The NZSF reported paying approximately $14 million in tax to foreign governments in the 2016-17 tax year (New Zealand Superannuation Fund, 2017). This is a cost to the NZSF that does not benefit New Zealand.

59. Tax-exempt status would better recognise the fact that the NZSF is an instrument of the Government of New Zealand and make it easier for the NZSF to apply for tax exemptions in foreign countries where they are available. Not all governments recognise the principle of sovereign immunity, so the NZSF may still have to pay tax in some jurisdictions, even if it becomes tax-exempt in New Zealand. Nevertheless, the NZSF will benefit from lower compliance costs in New Zealand and some reduction in foreign taxes.

That $14 million is a real cost to New Zealanders, but as the TWG themselves recognise even exempting NZSF from all New Zealand taxes would probably not reduce that number to zero.

But what is really striking is that there is no discussion – not a word – about the risks that exempting NZSF from taxes might pose to the efficient allocation of capital in New Zealand. Instead we get shonky arguments like this

Tax-exempt status would also reduce the amount of contributions that need to be made by the Government over time in terms of the funding formula in the New Zealand Superannuation and Retirement Income Act 2001.

Well, yes, but so what? Reduced contributions aren’t a real saving in this context, just a substitute for reduced tax revenue from the NZSF.

Ah, but “the NZSF will benefit from lower compliance costs in New Zealand”. No doubt that is true, but NZSF with its $37 billion of your money is considerably better placed to cope with the inevitable compliance costs of the tax system than most of the rest of us, including most of the rest of the business operations that would become subject to the TWG’s capital gains tax. Hard to believe that they could really run that line with a straight face.

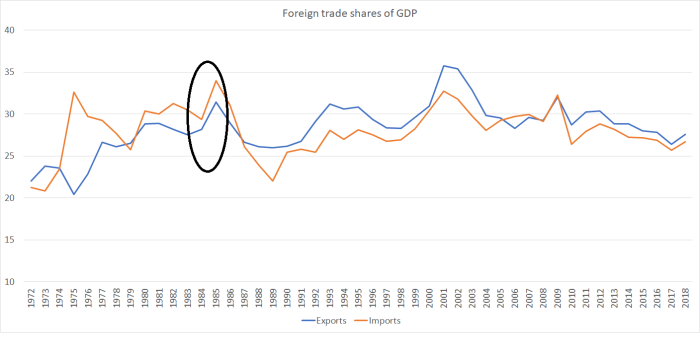

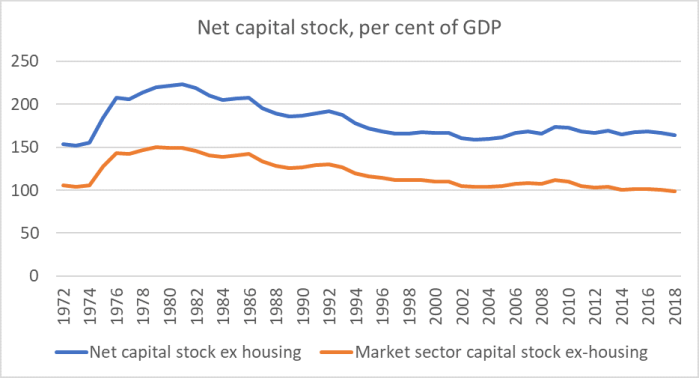

(I don’t know what accounts for the sharp lift back in mid-70s, but you can see the Think Big effect in the early 80s.)

(I don’t know what accounts for the sharp lift back in mid-70s, but you can see the Think Big effect in the early 80s.)