Since the announcement last week that the Reserve Bank Governor is leaving at the end of his term, and that his senior deputy won’t be a candidate to replace him, there has been a lot of commentary around both about what the Board and the (post-election) Minister of Finance should be looking for in a Governor, and what changes might be made in the legislative arrangements under which the Reserve Bank operates. As just one example, both the centre-left economics columnists in yesterday’s Sunday Star Times were writing about aspects of the topic.

That seems entirely appropriate. The Reserve Bank exercises huge discretionary power in both monetary policy and financial regulation, and the once-vaunted accountability mechanisms have actually turned out to be quite weak. And the basic structure of the legislation the Bank operates under is now getting on for 30 years old. Much has changed in that time.

Finding the right individual for the job of Governor matters a lot. Even within the limitations of the current legislation, the right individual (building the right new senior management team) can make a material difference, in revitalising the organisation, and putting it on a more open and transparent footing – both as regards policy, and the conduct of the Bank’s own affairs. Still, we should be careful of what we wish for. The Herald’s editorial last Friday argued, writing about the monetary policy responsibilties, that “the next Governor will need to be bold”. Well, perhaps. But “boldness” isn’t a great quality unless one is sure (a) of to what end it is directed, and (b) of the judgement, capability and character of the person being bold. If I think back over 30 years of New Zealand monetary policy, Alan Bollard’s deep cuts in the OCR in the crisis conditions of late 2008 probably qualify as bold. But so did Don Brash’s MCI experiment and Graeme Wheeler’s 2014 tightening cycle. Neither of those ended well.

In the Sunday Star Times, Rod Oram argued

So, the best we can hope for is the next government, regardless of which party leads it, has the courage to recruit a rare individual as the next Reserve Bank Governor – a person who is highly experienced in the intricacies of the job, yet insightful and brave enough to restore the institution to world leadership.

That last line or so seemed both unrealistic and somewhat ahistorical – perhaps partly because Oram appears to have come to New Zealand only as the Reserve Bank’s “glory days” were already passing.

The Reserve Bank of New Zealand gets credit for being the first country in the world to introduce (modern) inflation targeting. I was present at the creation, and am proud of having been part of that. But it was at least as much accident as design – a Treasury that was determined we had to have a contractural arrangement (pretty much every other government agency was getting one), and a muddied post-liberalisation post financial crisis world in which nothing much else would work. We weren’t forerunners in central bank independence, in getting on top of inflation, in the idea of announcing medium-term targets, or in the publication of accountability documents. And most of the specific details of our model haven’t been followed when other countries came to revise their legislation. And if you read our economic analysis during the late 1980s and 1990s it was mixed bag, to say the least. If I recall with pride the day I read Samuel Brittan of the FT praise our second-ever Monetary Policy Statement, which I’d largely rewritten over a weekend after Saddam Hussein invaded Kuwait and oil prices rocketed, I read some of other stuff we (I) wrote and cringe at least a little. We were doing some good stuff, but were rushing to catch up with what being a modern central bank really involved, and there were so little institutional resilience that we stumbled into the MCI debacle only a few years later. (For those too young to understand the reference, (a) be thankful, and (b) I will do a proper post about it one day.)

And what of banking regulation? After an extensive and acrimonious internal debate in the early 1990s, the Reserve Bank did change quite materially its approach to banking supervision and regulation. Pulling back from the seemingly-inexorable pressures to become ever more intrusive and interventionist in our banking supervision, we adopted a model which emphasised director-responsibility, and public disclosure, with the aim of better aligning incentives, to strengthen market discipline and reduce the prospect of public bail-outs etc. Capital requirements were left in place, but as much because the banks wanted them – they feared they look “unregulated” without them – as because of any Reserve Bank preference. I wasn’t that closely involved, but I mostly thought it was a step in the right direction – and lament the way that the Reserve Bank has wound back on public disclosure requirements in recent years. But if there were elements of the model that did, in small ways, influence the thinking and practice of other countries’ regulatory models, they weren’t very important. It was innovative, and may even have been right, but it wasn’t really tested – as the key institutions of our banking system became increasingly Australian-dominated (and hence under the overall oversight of Australian regulatory authorities). And it hasn’t become the global model – bailouts abounded in 2008/09, no one thinks that problem has been solved, supervision and regulation is at least as intrusive and second-guessing as ever, and the Reserve Bank’s resistance to deposit insurance now looks more anomalous than ever. There was some good and interesting stuff done, and some able people were involved in doing it, but it was never the basis of “world leadership”.

In any case, how realistic is the idea of “world leadership” in this area? We are a small country, we don’t resource our central bank that generously (and I don’t think we should spend more), and central banking feels like one of those areas (risk management, crisis management etc) where one should be wary of the pathbreaking – after all, how do we distinguish it from what turns out to be a dead end?; isn’t this what we have academics and think-tanks for etc? And realistically, if one looks through the lists of people talked about as potential candidates as Governor, be it Geoff Bascand or Adrian Orr (probably the names at the top of most lists) or others – Rod Carr, John McDermott, Murray Sherwin, David Archer, Arthur Grimes, New Zealanders running economic advisory firms, New Zealanders who are past or present bank CEOs here or abroad etc – very few look as though they have even the glimmerings of what Oram seems to be looking for. And even those who just might, have other weaknesses. For me, I’d settle for someone with the character, energy and judgement, backed up a solid underpinning of professional expertise, to revitalise the institution, rebuild confidence in it, and provide a steady hand on the policy levers, backed by high quality analysis and an openness to alternative perspectives, through both the mundane periods and the (hopefully rare) crises. And all that combined with a fit sense of the limitations of what monetary policy and banking regulation/supervision can and should do (on which point, I’ll come back another day to Shamubeel Eaqub’s column – not apparently online – on what he thinks the Bank and the new Governor should be doing.)

Finding the right person is a challenge, but it is also highly desirable to take the opportunity now to think about the legislation under which the Bank operates – in particular, the governance provisions. Ours is quite an unusual model, whether one looks across other central banks and financial regulatory agencies, or across other New Zealand public sector institutions. Under our law, all the extensive discretionary powers of the institution are vested in one individual – him or herself unelected, and selected primarily by unelected people (the Board) – and the range of powers the institution itself exercises is itself unusually wide. And, as I’ve noted previously, there is no statutory requirement for the Reserve Bank to have, or publish, a budget, let alone anything of its medium-term financial plans, even though financial control of public spending is one of the cornerstones of democracy. Parliament has less control over the Reserve Bank’s spending than over that of, say, the SIS. And the Reserve Bank takes an approach to the Official Information Act that suggests they still see themselves as somehow “different” and above the normal standards – for them, transparency and accountability are about them telling us what they want us to see, not about citizens’ access to information and analysis generated at public expense.

So I was pleased to see the Dominion-Post’s editorial this morning, Good time to reform Bank. In making their case, they quote me

“In New Zealand public life, it is difficult to think of any other position in which the holder wields as much individual power, without practical possibility of appeal,” Reddell has argued.

Joyce should also look to make the bank more transparent. It publicly releases official accounts of its forecasts and analysis reasonably regularly, but it seldom reveals anything of how its debates are conducted behind closed doors.

Again, this is not the case internationally. The US Federal Reserve releases the minutes of its regular meetings three weeks after they happen. New Zealand likes to brag about its open approach to official information, but in this sphere as in others, it has fallen behind the pack.

As they note, there has been reasonably widespread support for reform. They note support from The Treasury, and from the Green Party (a recent post from James Shaw reaffirmed that support). And when the Treasury looked at the issue a few years ago (before the Wheeler appointment), they found that most market economists also supported change. The Labour Party has toyed with favouring change, and when the previous Labour government commissioned an inquiry 15 years ago, their reviewer Professor Lars Svensson also recommended change. And we know that Graeme Wheeler himself favoured change – he made the point again in the (rather soft) interview in Saturday’s Herald.

When Bill English was Minister of Finance, the government wasn’t willing to countenance change. Having let the chance slip before Wheeler was appointed, going with any model other than Wheeler’s favourite one (legislate to give him and his deputies all the power) over the last few years, would probably have been a political negative for English. And the Wheeler option is an unsatisfactory one on a number of counts – since the Governor appoints and remunerates his deputies and assistant, it isn’t much protection against poor decisionmaking or a bad Governor. But now the slate is clear: the Governor is moving on to new opportunities, and his deputy will simply be holding the fort for six months. A decision now to think hard about reforming the governance model isn’t a reflection on the current Governor (not that Lars Svensson saw his recommendation in 2001 as being so either), and provides an opportunity for the government to provide a steer to the Board about what sort of Reserve Bank they want the new Governor to run. It is unlikely new legislation could be put in place by next March (when Grant Spencer’s acting term runs out), but a new Governor could be appointed on the expectation that that person will lead the transition to a new, more modern and internationally comparable, governance model for the Bank.

Who knows if the new Minister of Finance is interested, but flicking through some old posts, I was encouraged to find one from September 2015, reporting an exchange in the House between then Associate Minister of Finance Steven Joyce and the Greens then finance spokesperson Julie Anne Genter. In response to a question on governance, Joyce responded

Hon STEVEN JOYCE : The suggestion that the member makes, of having a panel of people making the decision, is, I have to say, not the silliest suggestion in monetary policy we have heard from the Greens over the years, and many countries—

A backhanded dig at the Greens at one level, but not an outright dismissal by any means.

Commissioning a background piece of analysis from, say, the Reserve Bank and Treasury, to review carefully, and neutrally, the issues and options, to be delivered to the Minister at the end of September, after Wheeler has left and the election is over, would be an appropriate step now. Such a document – which could later form the basis for a public consultative document – would be a useful contribution to advancing the issue, and a resource that would enable any incoming government to work through the issues and analysis relatively quickly – consistent with the sort of timeframe relevant to the appointment of a new Governor.

Reform in this area is something I’ve championed for a long time, both inside and outside the Bank. It isn’t primarily a matter for the Bank – it is about how Parliament and the executive want a powerful public agency to be structured and governed – although of course the Bank may have some specific insights on some of the relevant technical details (of which there are many – reform in this area isn’t the stuff of some two page bill).

I’ve laid out my own arguments for reform more fully in past posts (eg here) and a discussion document of my own.

Making the case for change is, I think, relatively easy. There is a much wider range of potential alternative models. At one end, one could leave most other things intact, and simply shift the power from the Governor to a committee of him and his deputies/assistants. At the other, one could perhaps break-up the Bank, creating a separate financial regulatory agency (paralleling the Australian approach) with separate governance structures for the Bank and the new successor institution.

I don’t have a strong view on whether the regulatory functions should be kept in the same institution as monetary policy – there is a variety of models internationally. But if the functions are kept in a single institution, I think there is a pretty strong case for separate governing bodies for each of the main functions – both because different sets of expertise are required, but also to help manage the tensions and conflicts and strengthen accountability for the exercise of the various different parts of the Act(s). This post covers some of that ground. The key features of the governance model I propose would be:

- The Reserve Bank Board would be reformed to become more like a corporate (or Crown entity) Board, with responsibility for all aspects of the Reserve Bank other than those explicitly assigned to others (NZClear, foreign reserves management, currency, and the overall resourcing and performance of the institution).

- Two policy committees would be established: a Monetary Policy Committee and a Prudential Policy Committee each responsible for those policy decisions in these two areas that are currently the (final) responsibility of the Governor. Thus, the Monetary Policy Committee would be responsible for OCR decisions, for Monetary Policy Statements, for negotiating a PTA with the Minister, and for the foreign exchange intervention framework. The Prudential Policy Committee would be responsible for all prudential matters, including so-called macro-prudential policy, affecting banks, non-bank deposit takers and insurance companies. The PPC would also be responsible for Financial Stability Reports.

- Committees should be kept to a moderate size, and should comprise the Governor, a Deputy Governor, and between three and five others (non staff), all of whom (ie including the Governors) would be appointed by the Minister of Finance and subject to scrutiny hearings before Parliament’s Finance and Expenditure Committee. There should be no presumption in the amended legislation that the appointees would be “expert” – however that would be defined – although it might be reasonable to expect that at least one person with strong subject expertise would be appointed to each committee.

- The Secretary to the Treasury, or his/her nominee, would be a non-voting member of each committee (the case is probably particularly strong for the Prudential Policy Committee).

In addition, the legislation should be amended to provide for the publication of (substantive) minutes of the meetings of these bodies (with suitable lags), and to require stronger parliamentary control, and public scrutiny, over the Bank’s spending plans.

It isn’t, of course, the only possible answer, but of those on offer I think it provides the best balance among the various considerations: providing internal expertise and external perspectives, clear lines of accountability for diverse functions, greater transparency and financial accountability, coordination across functions and arms of government, all while providing a significant role for the Governor as chief executive, and linch-pin, of the organisation, without anything like as dominant a personal policy role as there has been until now.

We won’t find – and probably shouldn’t be seeking – a Governor who walks on water. But an able person who would effectively lead a revitalised Bank into a new era, with this sort of governance structure, would be making a very substantial contribution. Change management skills and a commitment to organisation-building should be at least as important as personal technical expertise. I hope that is the sort of person, and the sort of structure, that the post-election Minister of Finance, and the Board, end up looking for.

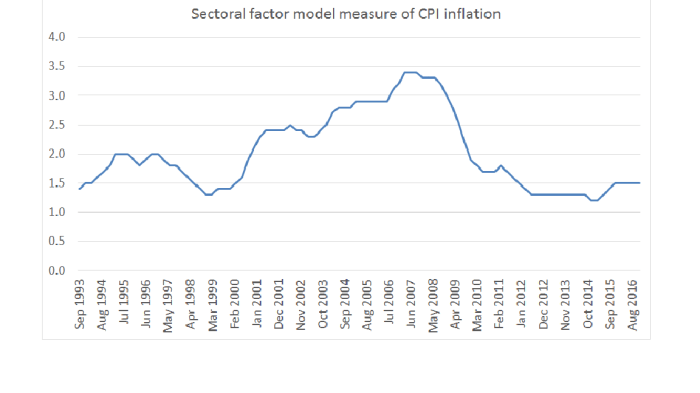

The fact that this measure is not very volatile tends to mean more weight should be put on deviations from the target – they aren’t likely to be simply “noise”. Perhaps the latest estimates will eventually be revised up a little in time, but as it happens the sectoral factor model estimate is now around the median of the whole suite of core measures. The medium-term trend in inflation was probably around 1.5-1.6 per cent late last year.

The fact that this measure is not very volatile tends to mean more weight should be put on deviations from the target – they aren’t likely to be simply “noise”. Perhaps the latest estimates will eventually be revised up a little in time, but as it happens the sectoral factor model estimate is now around the median of the whole suite of core measures. The medium-term trend in inflation was probably around 1.5-1.6 per cent late last year.