The Prime Minister went to Auckland yesterday, accompanied by his Deputy and his Minister of Finance, to deliver what is popularly billed as a “state of nation” address at the Auckland Rotary Club. I’m staggered that the Prime Minister could give such an address in Auckland and not once mention that house price debacle that his government, and the previous Labour government, have presided over, and done little to address.

But the bit of the speech that caught my eye was this

I’m proud that on the other side of the globe from the European capitals I visited a few weeks ago, New Zealanders have built a cohesive and globally competitive country that can provide valuable lessons to the rest of the world.

In recent years, New Zealand has dealt with the biggest financial crisis since the Great Depression, we’ve dealt with devastating earthquakes and we’ve made significant progress on deep-seated social and Treaty issues.

We now have a dynamic and diversified export sector,

In particular the suggestion that we have “built a globally competitive country” and as a result we “now have a dynamic and diversified export sector”. (I wasn’t too sure about the “valuable lessons” we can apparently offer to the rest of the world, but I’ll leave that aside for now.)

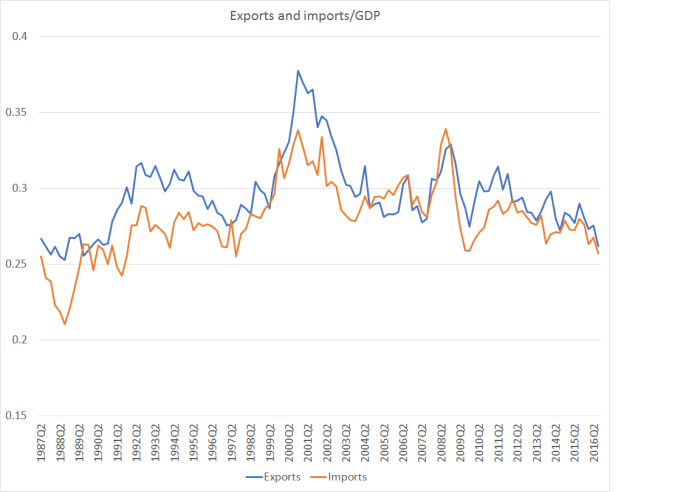

Statistics New Zealand typically advise that the best way to look at longer-term trends in components of the national accounts is to use ratios of the various nominal series. Doing so avoids deflator problems, and also recognises that prices – earned and paid – matter. Here is the chart showing exports – and imports – as a share of GDP.

Exports as a share of GDP are now below where they were when the Prime Minister was Minister of Finance/Treasurer in the last days of the Shipley government in the 1990s (and lower than at any time since then, under Labour or National governments).

In a thriving, globally competitive, economy one would more normally expect to see both exports and imports trending upwards as a share of GDP. For small countries that is even more important than large countries.

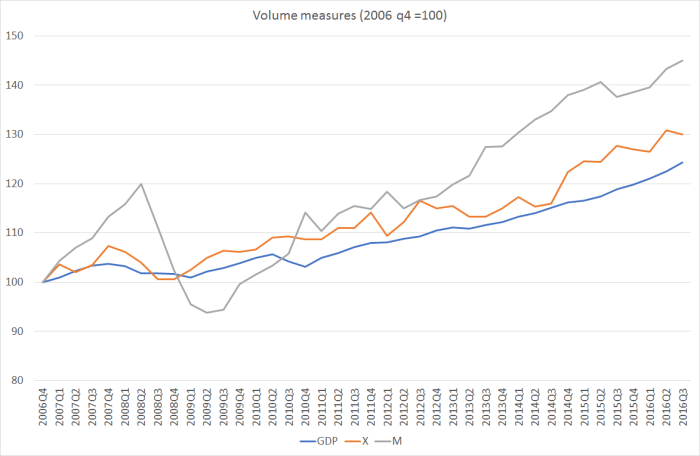

Out of curiosity I did dig out the data on export and import volumes and how they’ve grown relative to GDP. Here is the chart for the last decade.

Export volumes have certainly increased a little faster than real GDP has, and import volumes more so. But if the value of what we sell to the world (and then buy from it) hasn’t increased as a share of GDP, it doesn’t look like a particularly impressive story.

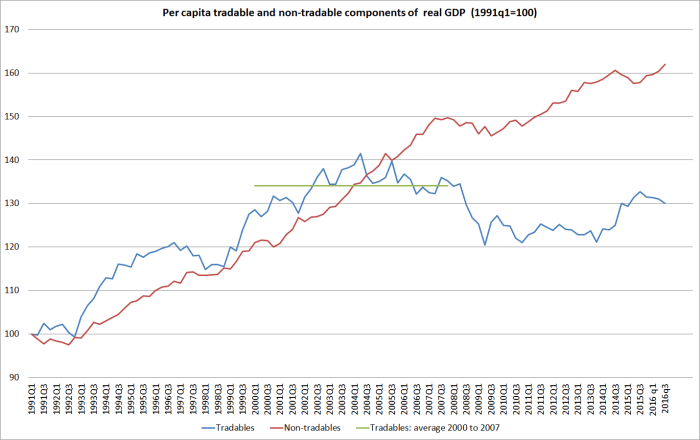

And finally, here is the chart I run every so often, showing an estimate of GDP broken down between the tradables sector (primary plus manufacturing plus export of services) and the non-tradable sector (the rest). And I’ve presented both series in real per capita terms. It isn’t a perfect proxy by any means, but it tries to get at the idea that domestic production for domestic consumption – especially in the manufacturing sector – is often exposed to global competition too.

In real per capita terms, this estimate of tradables sector GDP hasn’t grown in more than 15 years. The current estimated level is lower than the average for the 2000 to 2007 pre-recession period.

The evidence for this economy being globally competitive is slim at best. There are no doubt plenty of individual firms doing well, but it doesn’t add up to much, especially as the starting point – the initial share of exports (or export value-added) in our economy – was already so low for a country our size.

In part, firms seeking to export – or produce locally in competition with imports – have been battling uphill. The TWI measure of the exchange rate is around 79 this morning – on the Reserve Bank’s real exchange rate measure only around 5 per cent off the post-float peak. High real exchange rates can be a welcome thing, when they result from rapid productivity growth and the growing success of New Zealand firms in international markets. The high exchange rate rate then helps share the gains around. But that simply isn’t – and hasn’t for a long time – been the New Zealand story.

I’m not entirely sure why politicians come out and say this sort of stuff (“globally competitive”, “dynamic and diversified export sector”). It is particularly sad coming from the Prime Minister, who in his early years as Minister of Finance used to make exactly the sorts of points I’ve made in this post in speeches up and down the country: he was particularly fond of a version of the tradables/non-tradables chart. And the government has long had as one of its targets a material increase in the share of exports in GDP, suggesting that they knew there was something not quite right about New Zealand’s economic performance.

But now, almost nine years in, they seem reduced to simply making up lines like these, that perhaps might feel or sound good, so long as no one actually looks into them. Doing so discredits the speaker, and perhaps as importantly it further cheapens and debases political dialogue and debate. Bill English should be better than that.

When you read the whole speech, it is almost as if he sees the role of government as primarily a social service provider, like some kind of church. Perhaps the Nats have taken research which shows that people really don’t care about long run economic growth as long as they can get a job and the threat of extreme poverty is remote.

LikeLike

Yes, and the optimism about the ability of the state to transform individuals and families seems to defy most past experience internationally.

I guess the (missing) long-run economic growth is hard to relate to directly – which is why Oppositions need to paint picture and frame the issues in an appropriate way. But it is also why the NZ relative decline is so unnerving – once people become used to something it is hard to motivate change. And of course we come from a culture/institutional background (Northern European/Anglo) that didn’t get wealthy/productive primarily by focusing govt policy on lifting overall economic performance (unlike, say, the catch-up growth in places like Singapore, Korea, Taiwan). Particularly among the Anglos success was more or less taken for granted for couple of hundred years.

LikeLike

The problem actually is mainly due to a MMP government which means you can’t have strong government because you have to agree to not disagree with your support parties.

LikeLike

Michael I think Bill English and this government (and previous NZ administrations) inability to get on top of affordable housing is symptomatic of our wider economic problem.

If New Zealand is going to improve its trade-able sector -by value (because as you show we can improve volumes) then that value-added activity will happen in towns and cities. But the problem is our cities are grossly un-competitive -so are not attractive places for trade-able sector/value adding businesses to set up shop.

Japan has many problems -in particular they seem to collectively lost confidence in having children. But at a city-level they have been superior to NZ for a long time. As is many, many other cities around the world. A careful reading of articles like https://nextcity.org/informalcity/entry/when-tokyo-was-a-slum and https://medium.com/@brendon_harre/what-is-the-secret-to-tokyos-affordable-housing-266283531012#.ho8jl2gn5 shows that in New Zealand it is not just the household sector which are struggling with unaffordable towns and cities it is also the productive/trade-able business sector.

LikeLike

Just curious: re the per capita tradables vs. the non-tradable sector comparison, is the denominator the same or based on the number employed in each sector?

LikeLike

Total population for each – so it isn’t an attempt to get at productivity growth in the respective sectors, simply to avoid the focus going population-driven upward trend one sees in almost all volume series over time.

LikeLike

Thanks, appreciated.

LikeLike

Hmmm…. is there a way of breaking the export stats into ‘value added’ products compared to commodity products (milk powder, CHF90, logs etc etc)…. just wondering what the mix is over time and how that might be trending…

Digging into the export data and seeing what is going on between different types of exports might be useful compared to a broad brush approach… agree that the ig picture is not that encouraging… but details matter…

LikeLike

I had a brief attempt at doing something like that last year, but it was more difficult than I’d realised to do it well, and i never finished the exercise. I’ll try to get back to it, but my overall impression is that there hasn’t been that much diversification over say the last 25 years – around 85 per cent of our exports are still essentially natural-resource based (farm, fish, export-electricity [aluminium], oil, coal, wine and tourism). Even the current boom in tourism and export education involves shares of GDP less than in the previous surges in the early 2000s.

Of course, there is also plenty of embedded productivity growth over the years in even raw commodity production (as also in Aus).

LikeLike

Tradeables will drop as a share of GDP as population grows due to larger internal markets. Fall in imports/exports might not be as bad as it looks.

LikeLike

Yes, one would expect a smaller tradables/export share in a much more populous country – but the sorts of changes we’ve seen aren’t just about that, especially as NZ’s export share of GDP was already very low for a country our size.

LikeLike