A reader who is paid to, among other things, monitor the Reserve Bank got in touch to suggest that the Reserve Bank’s claim, highlighted in this morning’s post, to have “initiated an easing cycle in June 2014” was neither a typo nor a piece of carelessness (I’d assumed the latter), but something conscious and deliberate.

Recall that in this morning’s MPS, the Bank wrote that

The Bank initiated an easing cycle in June 2014, by lowering the outlook for the policy rate from future tightening to a flat track, and then cutting the OCR from June 2015

Most people, when they think of an easing cycle or a tightening cycle, think of actual changes in the OCR. On that conventional description, the OCR was raised four times, by 25 basis points each, from March 2014 to July 2014. Note those dates: not only was the OCR raised in the June 2014 MPS, but it was raised again the very next month.

And if one compares the crucial final few sentences in the press releases for the March and June 2014 MPSs there is no material change in wording from one document to the other, and there is nothing in chapter 2 of the June 2014 MPS (the policy background chapter) to suggest a change in policy stance.

So how might they now – revisionistically – attempt to describe an “easing cycle” as having been commenced in June 2014? Well, the only possible way they could do so – perhaps hinted at in that phraseology “by lowering the outlook for the policy rate” – is using a change in the forecast for the 90 day rate from the previous set of projections, in March 2014, to those in the June 2014 MPS.

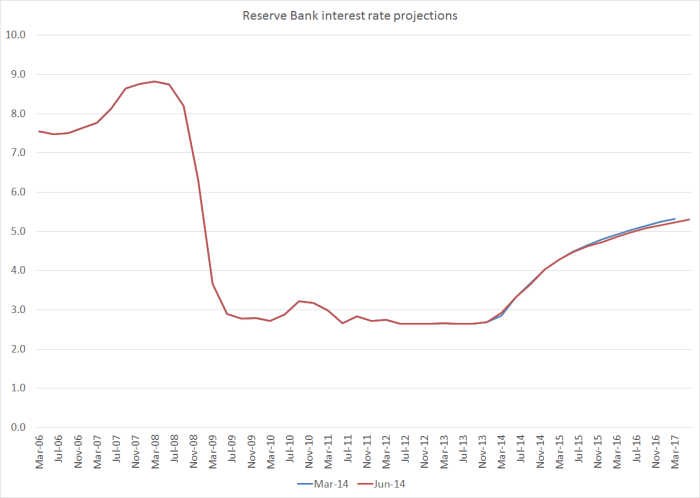

But here is the chart showing the two sets of projections

The differences are almost imperceptible. In fact, the June track (red line) is very slightly above the blue line in the very near term, and at the very end of the period the difference is that the 90 day rate is projected to get to 5.3 per cent in the June 2017 quarter rather than the March 2017 quarter. And recall that there were no contemporary words to suggest a change of stance.

Sure enough over subsequent quarters the Bank did start to revise down the future track, but there is no evidence that over that period they thought of themselves – or openly described themselves – as having begun an “easing” cycle. That didn’t happen – and even then they didn’t think of it as a “cycle” – until the OCR was first cut in June 2015. Here is the Governor talking about monetary policy in a February 2015 speech.

We increased the OCR by 100 basis points in the period March 2014 to July 2014 because consumer price inflation was increasing as the output gap became positive and was expected to increase further. Since July, the OCR has been on hold while we assessed the impact of the policy tightening and the reasons for the lower-than-expected domestic inflation outcomes.

The inflation outlook suggests that the OCR could remain at its current level for some time. How long will largely depend on the development of inflation pressures in both the traded and non-traded sector. The former is affected by inflation in our trading partners and movements in our exchange rate; the latter by capacity pressures in the economy and how expectations of future inflation develop in the private sector and affect price and wage setting.

In our OCR statement last Thursday we indicated that in the current circumstances we expect to keep the OCR on hold for some time, and that future interest rate adjustments, either up or down, will depend on the emerging flow of economic data.

Again, no sense from the Governor that he was well into an “easing cycle”, as we are now apparently supposed to believe.

Now, there is a theoretical argument that the stance of monetary policy can be summarised not just by the current OCR but by the entire future expected/intended track. But as the Reserve Bank has often – and rightly – been at pains to point out, projections of interest rates several years in the future contain very little information, as neither the Reserve Bank nor anyone else knows much about what will be required 2 to 3 years hence. And it is a dangerous path for them to go down, for it invites those paid to hold the Governor to account to do so not just in respect of the actions he or she takes, but in respect of their ill-informed (but best) guesses as to what the far future of the OCR might hold.

If this is the explanation for the Reserve Bank’s words this morning – and sadly it seems like a plausible explanation – it is, at best, a case of someone trying to be too clever be half, and change the clear meaning of plain words (to the plain reader) in mid-stream. At best, too-clever-by-half, but at worst a deliberate attempt to use a verbal sleight of hand to deceive readers, including the members of Parliament to whom the document is, by law, formally referred. Sadly, it looks a lot like the “alternative facts” label – one that should be worn with shame – might have have been quite seriously warranted. They didn’t start easing in June 2014; at best by later that year they started slowly backing away from their enthusiasm for (a whole lot more) further tightening.

I’d hoped for better from the Reserve Bank, its Governor, incoming acting Governor, and other senior managers who may perhaps have aspirations to become Governor next March.

Lewis Carroll wasn’t intending Through the Looking Glass as a prescription for how powerful senior public officials should operate.

“When I use a word,” Humpty Dumpty said, in rather a scornful tone, “it means just what I choose it to mean—neither more nor less.”