I might have a post later on the substance of today’s Monetary Policy Statement – or might not, since the bottom line stance seems entirely correct to me (regular readers may think this a first). But I couldn’t let one particularly egregious misrepresentation go by without comment; a claim so blatantly wrong that one almost had to wonder whether the Bank was now taking communications advice from Sean Spicer and Kellyanne Conway.

In each MPS Box A “Recent monetary policy decisions” appears. This box is one of my minor legacies to the Bank. I banged on often enough about the statutory requirements for MPSs – which require some retrospective assessment and self-evaluation – that they agreed to include this box. It is rarely done well and – in fairness – the Act probably needs changing, to provide for reviews and assessments rather less frequently. And the content tends, perhaps inevitably, to be rather self-serving. But the latest version was just too much.

It begins as follows

The Bank initiated an easing cycle in June 2014

When I first saw that I assumed it was just a typo – bad enough, but these things happen. The OCR wasn’t actually cut until June 2015. But no, the authors were apparently serious. The whole sentence reads

The Bank initiated an easing cycle in June 2014, by lowering the outlook for the policy rate from future tightening to a flat track, and then cutting the OCR from June 2015

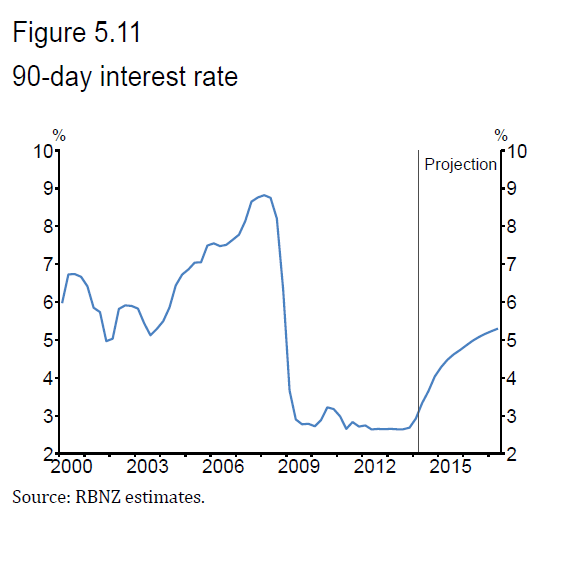

Do they really expect to be taken seriously? For a start, their statement isn’t even true. Here is the chart of the projected 90 day interest rates from the June 2014 MPS.

The OCR was not only increased in the June 2014 MPS, but they projected another 200 basis points or so of increases. By now – March quarter of 2017 – the OCR was projected to be still rising, and at 5.2 per cent.

And here was what the Governor had to say in the June 2014 MPS

There was no doubt that the Bank – the Governor – in June 2014 thought they would be raising the OCR a lot further, and had no thought in mind of beginning an easing cycle any time in the following few years.

I’m not sure what has gone wrong in this quarter’s Box A. All the key players – the Governor and his closest advisers – were around in June 2014, and are around now. They know what happened, and in June 2014 they were pretty confident of their tightening stance. But they made a mistake. It happens. What shouldn’t happen is crude attempts to rewrite history.

I rather doubt this was deliberate on the Governor’s part – probably some carelessness further down the organisation, and then insufficient care in reading and approving the final text. But it isn’t a good look, and I hope they will take the opportunity to acknowledge the mistake and issue a correction.

Perhaps the FEC and/or the Bank’s Board might ask just what went on?

That really surprises me. I thought NZ was “outside the asylum” on stuff like that, to use Eric Crampton’s terminology.

LikeLike

I have to believe there is an innocent explanation – stuff up rather than deliberate – and to back that in Box A there is a chart showing 90 day rate projections over time, and they include in that the Dec 2014 track which was still heading upwards, at a much more muted rate.

But it isn’t a good look, especially as the material in this box is some of the statutorily required material in an accountability document to Parliament – it isn’t just some random piece of discretionary analysis.

LikeLike