Readers may be getting bored with a full week of posts on nothing other than Reserve Bank topics. In truth, so am I. But here is one last post in the sequence.

Saturday’s Herald featured, as the front page of the business section, an interview with outgoing Reserve Bank Governor Graeme Wheeler. This seems to have become a bit of a pattern – the Herald gets access to the Governor the day after the MPS, to provide a bit of a platform for whatever the Governor wants to say. The interviews are notable for being about as searching and rigorous as, say, the recent Women’s Weekly profile of Bill and Mary English.

The interview allowed the outgoing Governor to “launch the campaign” to become Governor for his deputy (and former Government Statistician), Geoff Bascand. That shouldn’t surprise anyone. Then again, it has now been 35 years since an internal candidate was appointed Governor. Successful organisations – the Reserve Bank of Australia is one example – are often seen promoting from within.

But my interest in the interview mostly centred on the Governor’s claim that “the economy is in very good shape”, and that we really should be grateful to the Reserve Bank for being a “big part of that outcome”. I had to read it several times to be sure I wasn’t missing something. Here was the full excerpt:

Broadly, if you look at where New Zealand is now “in terms of growth, inflation, unemployment rate, current account as a share of GDP, labour force participation and compare all that with a 20 or 30 year average, then the economy is a very good shape”, he says.

“It is puzzling to me why some of the commentators been so critical when the Reserve Bank is a big part of that outcome. We aren’t the whole story by any means, but our monetary policy configurations do have a major impact on the economy.”

In the initial version I read online on Saturday, and in the hard copy newspaper, that “compare all that with a 20 or 30 year average” read “compare all that with a 2009 year average”. Quite which of them the Governor actually said, or intended to say, isn’t clear. But either way, it isn’t very convincing. 2009 was the depth of the recession: economies tend to recover from recessions. Pretty much every economy in the world – perhaps with the exception of Greece – has done so to a greater or lesser extent. It is no great achievement to cut interest rates a lot in a recession.

But lets grant that the Governor meant to refer to comparisons with a 20 to 30 year average (I’ve seen him make such comparisons previously). How then do his claims stack up? He lists several indicators to focus on. Of them

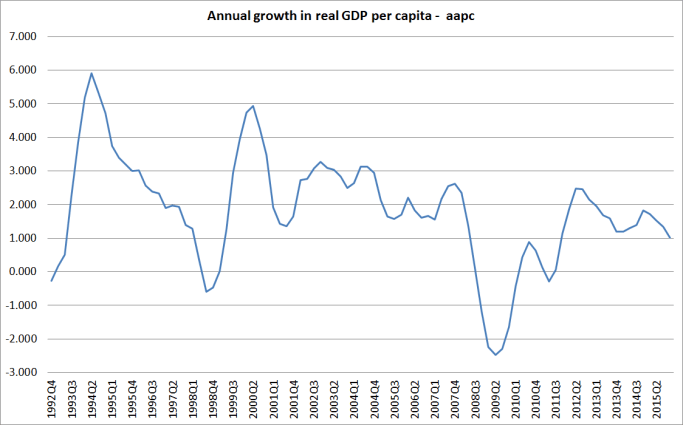

- Per capita growth – the only sort of growth that really matters – has been pretty weak this cycle compared to that in previous recoveries and growth phases,

- Inflation is (of course) low, but then it is supposed to be higher. The target is centred on 2 per cent – a rate we haven’t seen for several years – and was previously centred on 1 per cent, and then 1.5 per cent. Trend inflation outcomes are the responsibility of the Reserve Bank, but those outcomes have been away from target for some time.

- The unemployment rate is below a 20 or 30 year average – although well above the average prior to the mid 1980s – but then all estimates (including the Bank’s) are that the NAIRU has been falling over that time, and no one claims that that has been because of monetary policy (any more than previous increases were).

- The current account deficit is certainly smaller than it has been. But that is mostly because interest rates have been so much lower than had been expected (s0 that the servicing costs of the large stock of external debt have been surprisingly low). Much of the time, the Governor is more inclined to lament, than to celebrate, just how low interest rates have been, here and abroad.

- Labour force participation is higher than the historical average, but it isn’t clear why this is unambiguously a good thing. Work is a cost to individuals as well, at times, a source of satisfaction, but mostly people work to live. In a subsistence economy, pretty much 100 per cent of adults work. When New Zealand had the highest per capita incomes in the world, participation rates were lower.

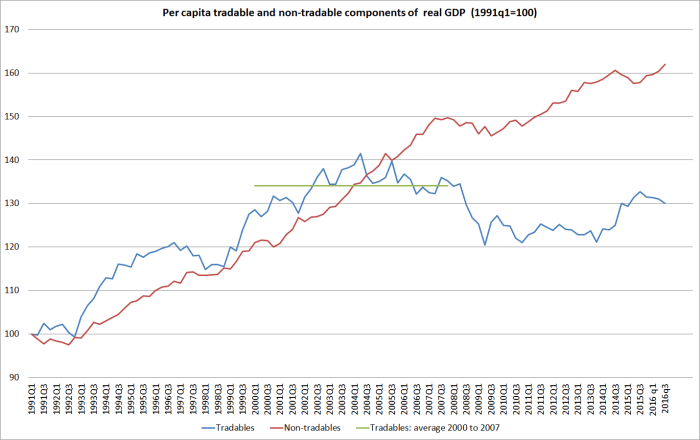

But, of course, even then the Governor has cherrypicked his data. There isn’t even any mention in this list of disastrously high house prices, or of the household debt stock, let alone of the real exchange rate, or the productivity growth performance, or the weak performance of the tradables sector, or of the large gaps between New Zealand incomes/productivity and those in most other advanced countries.

You might think that those are simply “Reddell hobbyhorse” indicators. But we know the Governor cares a lot about house prices and household debt, and about the real exchange rate. And it isn’t that long – before he became embattled, and seemed to feel the need to become something of an apologist for New Zealand’s economic performance – since he was talking about exactly the same sort of stuff.

Just a few weeks after he became Governor, he gave a speech in Auckland on Central banking in a post-crisis world . In the opening paragraphs of that speech he counselled

With these assets we should be capable of stronger economic growth. Internationally, and particularly in smaller economies, economic growth is driven by the private sector and its ability to compete on global markets. We need to reverse the slowdown in multifactor productivity growth since 2005 and the decline in value added in our tradables sector. And we need to reverse the shift of resources into the public sector and other non-traded activities.

Productivity growth hasn’t improved – if anything the reverse – since then, exports as a share of GDP have been slipping, and there has been no sustained rebalancing towards the tradables sector.

They were the Governor’s words, not mine.

Another couple of months into his term, he gave another interesting speech, this time Improving New Zealand’s Economic Growth. Back then he seemed concerned about productivity (and the lack of it)

Since 1990 we’ve outperformed many OECD countries on inflation and unemployment. Our inflation rate has been one and a quarter percent below the OECD median and our unemployment rate half a percent lower. But our per capita income has lagged behind and we’ve run large current account deficits. Real per capita GDP growth has been one and a quarter percent, about half a percent below the median and our current account deficit has averaged five percent of GDP – about the 6th largest relative to GDP in the OECD region.

There are two main ways in which our prosperity can improve over the longer run. The first is if the world is willing to pay more for what we produce. The second is by raising our labour productivity – that is by increasing the level of output per working hour. In the short term, we can generate higher income if we increase labour force participation or work longer hours. But we already have a higher proportion of our population in the labour force than nearly all other OECD economies and we work longer hours than most people in the OECD.

and

This is striking given the high international rankings for the quality of our institutions, control of corruption, ease of doing business, and according to the World Bank, the highest per capita endowment of renewable resources in the world.

Chart 2: Labour productivity growth in selected OECD economies, 1990-2011

(Average annual rate)

Source: OECD

So why is our per capita income so far below the OECD median? Partly it’s due to our geographic location and small economic size. Distance and economic size matter a lot even in a more globalised world of trade, capital and knowledge flows, and increasing interdependence. This also partly explains why our export range is concentrated over relatively few products – with food and beverages accounting for almost half our exports. The OECD and IMF believe size and distance, which limit economies of scale and market opportunities, account for around three quarters of the gap in our per capita income compared to the OECD average.

But this is not the whole story. Despite our high international rankings in key areas, the latest World Economic Forum’s Global Competitiveness Report ranks New Zealand’s overall competitiveness at 25th out of 142 countries. Besides market size, we perform poorly on our macroeconomic environment, and especially on our budget deficit and low national savings. But regulatory and performance-related factors also diminish our growth potential. Many of the remedies to substantially improve our ranking lie in our own hands, and groups such as the 2025 task force, the Savings Working Group, and the Productivity Commission, emphasised reforms that can raise our living standards.

He thought then there were three areas governments should focus on

Three areas seem particularly important. The first, is to raise our level of saving and investment, and improve the quality and productivity of our investment.

The other two were to close fiscal deficits, and to lift human capital. On the latter he observed

The bottom income deciles are populated by those with lesser skills, and those who experience prolonged and recurrent spells of unemployment. Addressing these groups would both promote productivity and reduce inequality.

Very little has changed since the Governor gave those speeches early in his term. The fiscal deficit has been closed, and no doubt the Governor would welcome that. But in late 2012 and 2013, there was just no sign that he thought the economy was in “very good shape” – rather it had key pretty deeply embedded structural challenges – and few of the key indicators he cited have changed for the better since then.

Now, to be clear, (and as central bank governors have pointed out for decades) very little of this is down to the Reserve Bank. Central banks aren’t responsible for – and don’t have much influence on trends in – house prices, current account deficits, productivity growth (labour or multi-factor), the health of the tradables sector, savings rates, participation rates or NAIRUs, let alone human capital and inequality. So the fact that the economy isn’t in particularly “good shape” – even if it isn’t doing that badly on some purely cyclical measures – isn’t the Governor’s fault, or that of the Reserve Bank. What the G0vernor can do is keep inflation close to target, and help safeguard the soundness of the financial system.

Which makes that line of the Governor’s, from Saturday interview, so puzzling

“It is puzzling to me why some of the commentators been so critical when the Reserve Bank is a big part of that outcome. We aren’t the whole story by any means, but our monetary policy configurations do have a major impact on the economy.”

After all, since 2009, the Reserve Bank has twice started tightening monetary policy only to have to reverse itself. I’m not today getting into the question of how much of that was a foreseeable problem. Even if none of it was, the fact remained that the Bank twice (out of two times) had to reverse itself. Neither episode – tightening and then reversal – had the sort of major positive impact on the economy that the Governor talks of. At best, they probably did little damage. And those episodes aside, the Reserve Bank just hasn’t done much on monetary policy for years. People – like me – have been critical of the Reserve Bank’s monetary policy management because of (a) those reversals, (b) the refusal to even acknowledge mistakes, (c) more recently, almost laughable attempts to rewrite history to suggest they were easing when in fact they were tightening. And, of course, the persistent deviation of inflation from target, and the concomitant extent to which the unemployment rate has been kept unnecessarily higher than required, or than the Bank’s own estimate would have suggested. Those outcomes suggested that, on average, monetary policy has been a bit too tight, as well as unnecessarily variable.

Is the aggregate cyclical position of the economy terribly bad? No, it isn’t. But it isn’t great either, and the longer-term metrics give even less reason for an upbeat story. The Graeme Wheeler who took up the job of Governor in late 2012 was better than this. Back then, he was willing to highlight what he saw as some of the structural problems. Perhaps it wasn’t his job – central bank governors don’t need to get into that territory, but he chose to. If he ventures into such territory, what we should expect is a Governor who calls things straight – for whom black doesn’t become white just because the Governor himself has himself had a rough few years. If he no longer feels he can name the serious economic challenges New Zealand still faces, perhaps he’d have been better to keep quiet rather than further undermine his good name with the sort of propaganda that we shouldn’t hope for, but might nonetheless expect, from a political party or lobby group.

Why do I bother, you might wonder? I was reading this morning a brief piece written to mark the anniversary of the death of US Supreme Court justice Antonin Scalia, by one of his former law clerks. The author wrote about “five lessons for living well” that he had seen in the judge’s life. One of them was

“Be honest in the small things, even if it makes life more difficult”

If our democracy and institutions are to be strong, it is what we should expect from people in powerful public office. It is too easy to put out “propaganda” and for it to slide past, and for people to nod in acquiescence when they read stuff they don’t know a lot about. At one level, Graeme Wheeler’s interview doesn’t matter much – and he’ll be off to pastures new shortly – but we deserve better, from our journalists and (in particular) from those who seek out and voluntarily assume high public office.