Winston Peters gave a speech on the economy yesterday to a Wellington business audience. Going by Alex Tarrant’s report, the delivered version must have been quite a bit different than the prepared and published text, but here I’m going to focus on the published text.

When I first started thinking about the possible role of immigration policy in explaining New Zealand’s dismal long-term economic performance, the immediate response from the person I sat next to at Treasury was “careful, or you’ll be sounding like Winston Peters”. In a similar vein (although I stress that it wasn’t the representative reaction – most people were simply puzzled and didn’t know what to make of it) one manager thumped the table and with the emotion very evident in his voice declared that it was disgraceful that we were even having such a discussion at The Treasury.

Peters has long been a polarising figure, and particularly so for the denizens of economic orthodoxy (of whom I generally counted myself as one). And, of course, he has been around for a long time – first becoming a Cabinet minister the same day in 1990 as Murray McCully, and presumably with aspirations to again becoming a senior minister after this year’s election. He has been Minister of Maori Affairs, Minister of Foreign Affairs, Treasurer, and Deputy Prime Minister. Very few ministerial careers will have spanned a longer period – Sir Keith Holyoake at 28 years is the longest I could think of.

And yet there has always been the question of what he has actually achieved, or delivered. At present, the list of concrete New Zealand First achievements includes the Super Gold Card, some stuff about cheaper doctor’s visits for children, and……..well, not that much else. That isn’t to say the presence of New Zealand First has had no other influence on policy over the years (quite possibly some of the government’s immigration policy changes last year and this have been partly pre-emptive measures). But in office, Peters just has not accomplished much.

That is true of monetary policy – long one of his bugbears. He negotiated a new Policy Targets Agreement when he became Treasurer in 1996. That agreement slightly increased the inflation target – mostly reflecting actual outcomes which had been in the upper half of the previous range. But even that agreement was a very long way short of the pre-election rhetoric. And once the agreement was signed he never gave the Bank any subsequent trouble. We managed to do some really daft stuff under his watch – the infamous MCI experiment – but he never called us out on it. He served as Foreign Minister under Helen Clark, and while he seemed to be a safe pair of hands in that role, his biggest achievement seemed to be securing a much bigger budget for MFAT. Somehow, I suspect that was not one of the priorities of his voter base.

And, of course, it is true of immigration policy. As I wrote about here, despite all the rhetoric – much of which I think was touching on, or prompted by, legitimate issues and concerns – there was nothing material in the detailed coalition agreement in 1996, and also nothing in the arrangement with Labour over 2005 to 2008. Throw into the mix his opposition to asset sales, his unease about foreign investment, his opposition to raising the NZS age and so on, and I’ve long been pretty sceptical of Peters.

And so I turned to an election year speech on economic policy with wary interest.

I liked some of his lines (even recognised some of them). He is totally right to call out the government for the way they make up lines to try to (a) pretend all is well (or even better) in the economy, and (b) to mask evident points of vulnerability (eg housing problems are “quality problems”). In his words, from the title of the speech, “the facade of prosperity”. Productivity is poor and per capita real GDP growth is pretty weak.

And while I wouldn’t word things quite this way

The fact is, massive immigration is neo-liberal, globalist voodoo.

It is an attack on those who believe in the nation state.

As a general proposition, I think the ideology of large-scale immigration in much of the advanced world isn’t far from that description. Based on faith rather than sight. Our politicians typically aren’t ideologues and like to think of themselves as practical people, but they’ve supped from the same streams of thought, and seem indifferent to the lack of hard New Zealand specific evidence on the benefits to New Zealanders of their preferred approach. For many, as Peters put it,

In their make-believe world immigration is a free good – a gift.

I’ve been pretty critical of the ex post government “spin”, that attempts to suggest that all is rosy. But Peters portrays it as the fruit of some deliberate and different economic strategy adopted by the current government.

Every country could flatter its economic growth by turning on the immigration tap.

But only NZ has seen governments reckless and irresponsible enough to try it.

In fact, to a considerable extent the current government has been running much the same immigration policy as its predecessors, including governments of which Peters was a part.

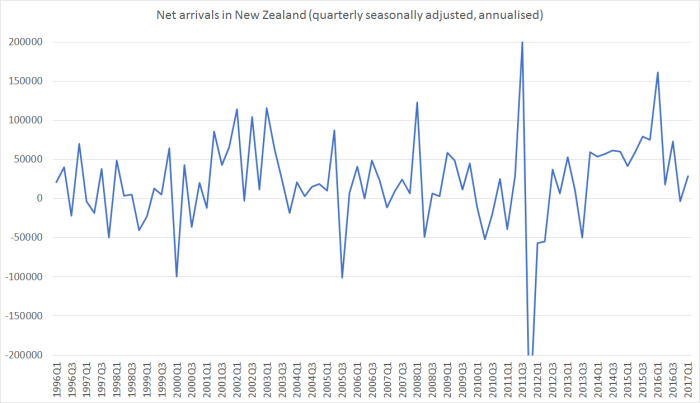

One can see it in the centrepiece of our immigration policy, the residence approvals target. It hadn’t changed for years, until a modest cut was announced last year by the current government. And what of actual approvals?

For the 12 months to March 2017, the number of approvals is a bit lower than the last June year. Overall approvals fluctuate from year to year, but average approvals under the current government are pretty similar to those under the previous government.

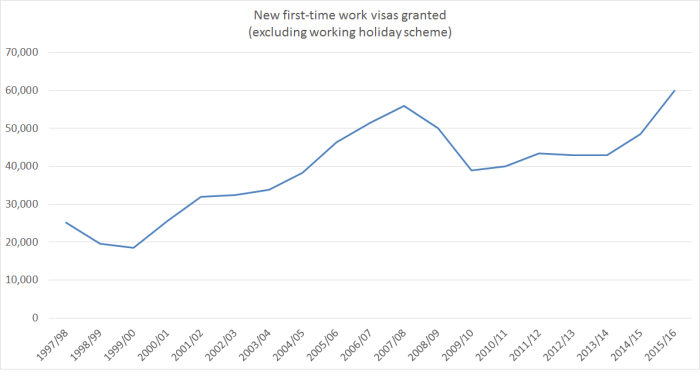

And here, using the MBIE data, is the numbers of people getting a first work visa in each year (excluding for the moment working holiday scheme people).

Not surprisingly, numbers dipped during the recession, but even with the increase in the last couple of years, the total number of people granted first-time work visas was still barely higher than in the last year of the previous government.

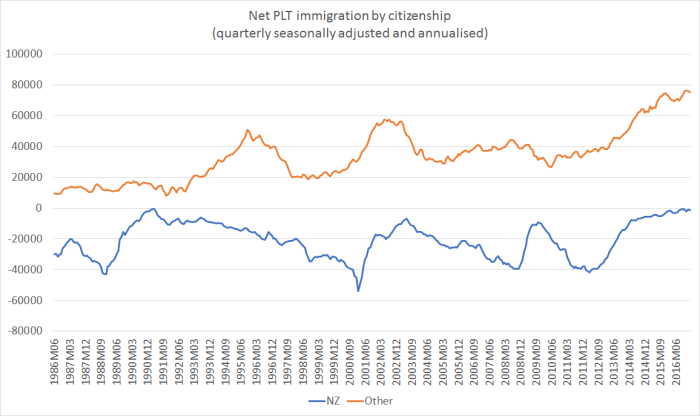

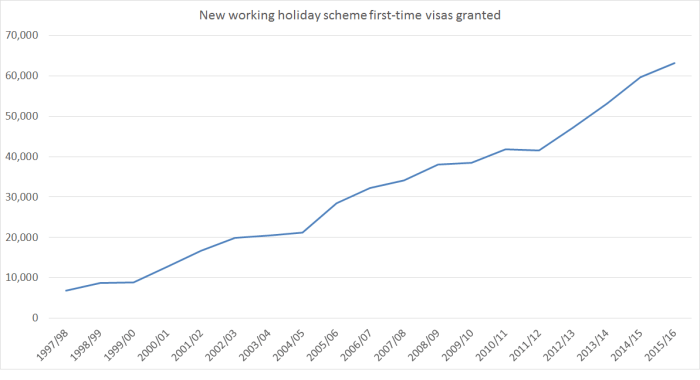

There are big differences in two areas. The first is working holiday scheme arrivals.

Even The Treasury has raised concern about the labour market impact of these visitors, but looking at the chart, it is a pretty strong and steady trend increase going back almost 20 years now. It certainly doesn’t look like a whole new strategy by the current government.

Students are another matter. There has been a recent big increase in student visa numbers, although still only back to around the 2002/03 peak.

Here, of course, there has been a deliberate policy change by the current government, in allowing many or most students significant work rights while they are in New Zealand. It looked like, and was, an “export subsidy”, and has probably had adverse implications for New Zealanders at the lower end of the labour market (with commensurate gains to the students and their employers). But this looks like the only significant liberalisation by the current government. Otherwise, they’ve largely been running the same (misguided) immigration policy as their predecessors

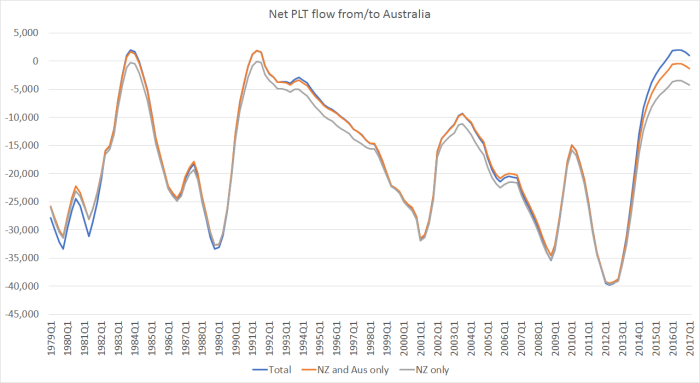

The student issue aside, I suspect that most of what has happened isn’t strategy – has there been any sign of a serious economic strategy? – but of being overwhelmed by unexpected events (while the large scale mediocre New Zealand immigration policy ran on in the background). In particular, the weakness of the Australian labour market (perhaps reinforced by the increasing recognition of the limited entitlements most New Zealanders have in Australia) means that the net outflow of New Zealanders has slowed markedly, and for longer than most had expected. The escape valve for New Zealanders for the last 40 years or so isn’t working at present, and New Zealand has to cope somehow.

It is a bit like the larger influxes of settlers back to France, after Algeria gained independence, and to Portugal in the 1970s when Mozambique and Angola gained independence. Opportunities that once existed abroad were no longer there, and a huge reflux of people put pressure on the home economy. It boosted aggregate GDP quite a bit – all these new people needed roofs over their heads – but it didn’t do anything very evident for productivity or the per capita things that matter.

So I don’t buy the line that the current government set out to supercharge population growth. It just happened. Perhaps the protracted weakness of the Australian labour market was foreseeable, but it wasn’t widely foreseen. If it had been the government could have wound back our non-citizen immigration programmes. It probably wouldn’t have, because ministers still seem to believe the twin gospels of “productivity spillovers” and never-sated “skill shortages”, oblivious to the way that in aggregate immigration increases aggregate pressure on resources, not eases it. But they could have done something.

As it is, they seem mostly overwhelmed by events, without any real strategy other than a desperate hope that it will all come right, in the meantime all the “made up stuff” serves mostly to try to distract attention from the unbalanced, not very productive, mess the New Zealand economy is in.

The government might well be without a strategy, but you have to wonder if any other party has a serious alternative on offer. Because in the Peters speech yesterday there was a lot of rhetoric about the past, and talk of how

New Zealand First has comprehensive, common sense economic policies designed to build a strong and resilient economy.

But there wasn’t a single word about they would actually do about immigration policy, in any of its dimensions.

I’ve heard Peters in the past talk of reducing the net PLT inflow to around 10000 to 15000 per annum. But not even that was repeated in yesterday’s speech – which, in a way, is welcome, because there is no meaningful way the net PLT inflow can be successfully targeted from year to year. And there was nothing else, at all. Even though it is only 4.5 months until the election.

Perhaps Peters thinks he can ride high simply on rhetoric. And perhaps he can. Perhaps he is concerned not to be outflanked by the Labour Party, which has also yet to release its immigration policy. But there was nothing at all in the speech. I’ve seen references to Peters wanting to set something around Pike River as some sort of “bottom line”, but (with due respect to the families of the victims) there are many more important issues in New Zealand. Judging from his rhetoric, you might suppose Peters thinks immigration is one of those things.

And so I can’t help wondering if we are being set up for a repeat of the last two times Peters went into government: lots of talk in advance, and no action on immigration policy at all. If it happens, of course, the establishment will be quietly content. But nothing fundamental will have changed.

Of course, one can only hope that is true of another area of policy that he did discuss in some detail.

Since the Global Financial Crisis we have been in a new economic era that makes reform of the Reserve Bank Act urgent.

Updating the obsolete Reserve Bank Act is critical to take account of the realities of 2017 rather than using a tool that is now decades out of date.

While we cannot slavishly copy from others, in the area of monetary policy we can certainly learn from the experience of countries like Singapore.

The city-state of Singapore has a population of around 5.7 milllion people in a country hardly larger than Lake Taupo.

They don’t have our advantages but they have achieved an enviable record of growth and stayed competitive through using an exchange-rate based monetary policy.

Singapore has a managed float and has a good record in moderating short-term currency fluctuations to ensure that the Singaporean dollar reflects their economy’s fundamentals.

There is no magic wand to get the dollar down to an appropriate and competitive level – and we have never pretended that there is.

But in today’s environment of historically unprecedented low interest rates, failure to reform the Reserve Bank’s Act to make it fit for purpose is inexcusable.

Reduced exchange rate volatility might be helpful, but it simply isn’t the main game. And Peters offers no thoughts at all on how the average level of the real exchange rate – one of the critical symptoms of our economic problems – might be lowered. And even if you were after materially reduced exchange rate volatility, a Singapore style policy simply isn’t feasible in a country as dependent on foreign capital as New Zealand is.

All in all, it was pretty disappointing stuff – the more so, because he isn’t far wrong in calling out the unreality of so much of emerges from the government on economic matters at present.