What to write about the Monetary Policy Statement?

The Governor continues to deny that any mistakes were made last year. I’m not sure why. As I’ve said before, perhaps the first OCR increases were defensible (certainly lots of onshore economists thought so), but to keep on hiking and then take a year to start cutting, quite grudgingly, even as core inflation stayed very low, was just indefensible. The Governor and his staff are human, so they will make mistakes. They should acknowledge this one and then move on. Unfortunately the continuing reluctance to admit any mistake, perhaps even to themselves, is colouring how they are running policy now. The OCR is still higher than it was at the start of last year – the only OECD country of which that is true – even as inflation expectations have fallen further. What is it about a situation of rising unemployment, near-zero per capita GDP growth, and well-below-target inflation makes them think we’ve needed higher real interest rates?

I was disappointed, if not overly surprised, by the questioning of the Governor at the press conference this morning. Here are a couple of questions I think we should expect the Governor to provide straight answers to:

- Governor, the Reserve Bank – like its peers abroad – has been telling us for years that core inflation is just about to pick up, and it hasn’t. If anything, it has kept drifting down, and with the unemployment rate still rising it is likely to fall further. In the very first paragraph of your Annual Report last year you once again told us that inflation was heading back to the midpoint. Again it hasn’t done so. . How have you corrected for this persistent bias, and why should we (or the public) have any more confidence in your inflation outlook now?

- Governor, given the Bank’s persistent forecasting bias – shared, of course, by local market economists – why not adopt a strategy that aims to get core inflation to something nearer 3 per cent. Given the (unintentional) biases you’ve shown to date, that might give us a good chance of actually getting core inflation up to 2 per cent. If inflation really looked to be rising strongly – to something well above 2 per cent – surely you have plenty of time to correct when you actually see the material increases in inflation?.

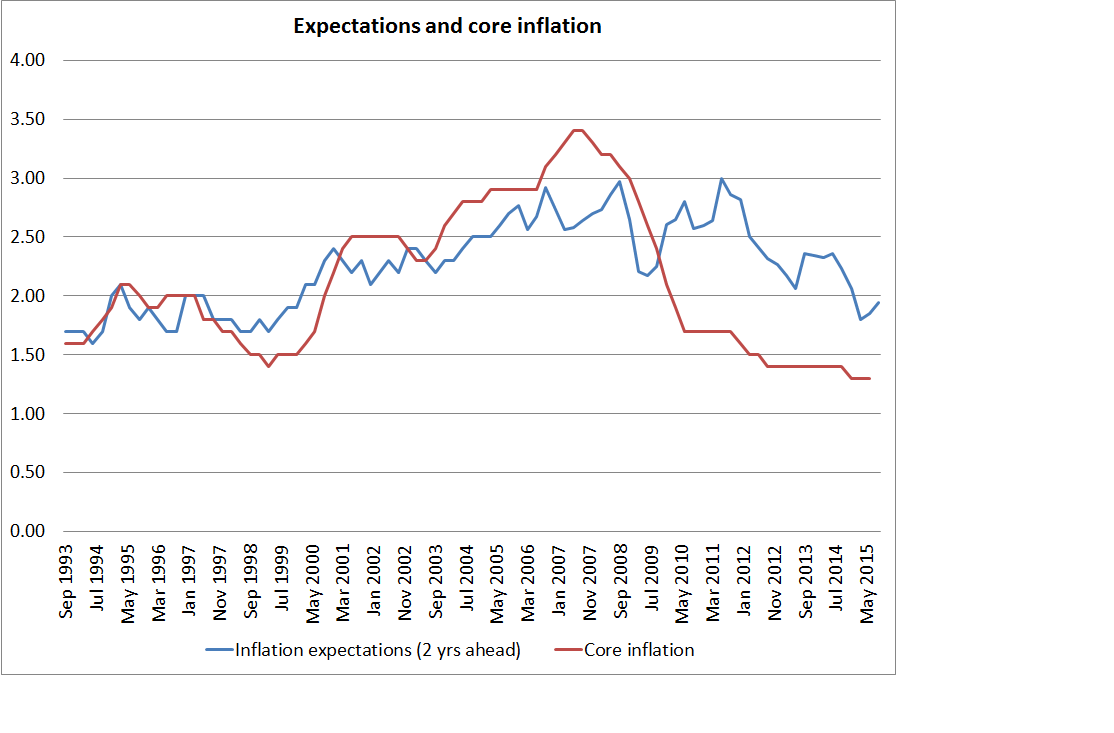

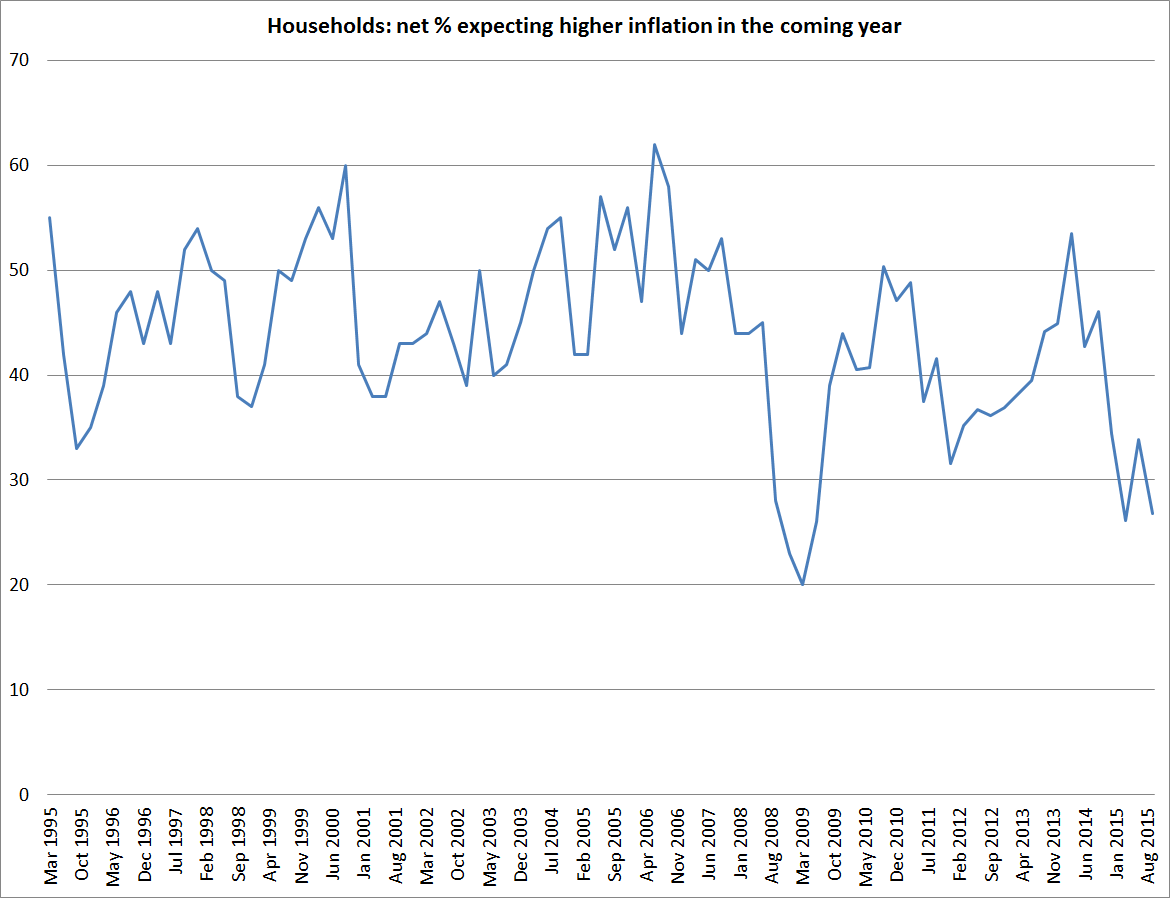

There was, as far as I could see, no particular basis in the document for a belief that core inflation is about to head back towards 2 per cent. Indeed, there is almost an attempt to sweep those awkward measures under the carpet, and to focus instead on headline inflation. Yes, headline inflation will probably pick up to some extent, and perhaps it will even creep over 1 per cent early next year. The evidence for that proposition isn’t great, and the Bank’s own past published research has cast doubt on it. Some tradables prices will no doubt rise – some already have – but exchange rates fall for a reason and are often accompanied by falling non-tradables inflation. It is those core or domestic components of inflation that really matter, and there was nothing in the Governor’s July speech or in this document to think the downside surprises have come to an end. Indeed, the Bank acknowledges that non-tradables inflation is likely to fall further (partly for one-off reasons), and as they are projecting the unemployment rate to carry on rising it would be surprising if their favoured core inflation measure did not fall further.

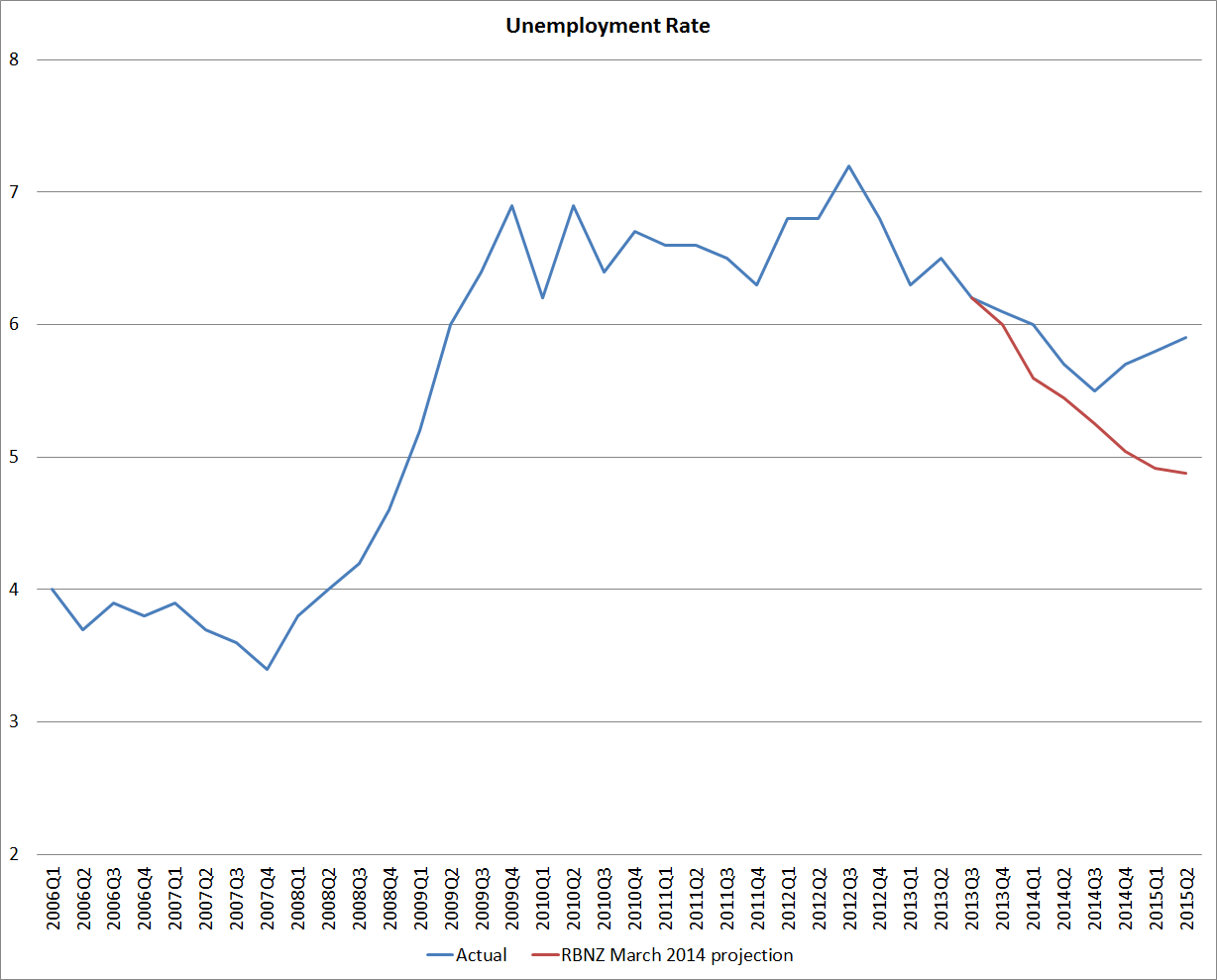

I’ve gone on quite a bit over the last few months about the apparent indifference to the unemployed. No one thinks that a 5.9 per cent unemployment rate is New Zealand’s NAIRU, the rate has been rising for several quarters already, and the Reserve Bank is now forecasting that the unemployment rate will rise even more. There is, conveniently, no chart of the unemployment rate in this MPS, but the tables at the back show them forecasting an unemployment rate up to 6.1 per cent next March, and only back down to 5.9 per cent a year later in March 2017. The unemployment rate was only 6.2 per cent in March 2010, just after the 2008/09 recession ended. Seven years on they expect no material inroads will have been made on the unemployment rate.

That March 2017 unemployment rate of 6.1 per cent is well within the sort of window that monetary policy can do something about. But the Governor is doing next to nothing more about it (these unemployment forecasts are after taking account of today’s cut and one more OCR cut). Lest I upset some economists, I should be clear that I’m not suggesting that monetary policy has very much impact on the longer-term average unemployment rate, but it has a considerable influence on fluctuations around the normal or natural level (itself determined by some mix of regulation, demographics, and so on). If core inflation was already 2 per cent and clearly rising, higher short-term unemployment might be an unavoidable price of keeping inflation in check. But core inflation is now 1.3 per cent, and probably falling. There is really no excuse for the OCR still to be so high. This is one of those times when there is no nasty trade-off: looser monetary policy would raise inflation (which we need, to get back to target) and lower the unemployment rate. Targeting house price inflation in Auckland isn’t part of the Reserve Bank’s mandate.

I don’t really understand why this high unemployment rate doesn’t seem to bother more people. I don’t hear market economists talking about it, or business journalists. I don’t hear business lobby groups doing so. The libertarian economist Bryan Caplan wrote a nice piece a couple of years ago about the grave evil of unemployment, and the way that people on the right tended not to take the problem seriously. But curiously, I also don’t hear the political Opposition talking much, or with much intensity, about unemployment.

And, as I’ve noted before, I really wonder what the Governor says to the unemployed people when he runs into them? How does he justify the Bank having run monetary policy in ways that delivered years of above-trend unemployment, scarring permanently the prospects for some of the people concerned. Mistakes happen, but the minimally decent thing to do is to acknowledge them and apologise. And how does he justify not adopting a more aggressive policy now, a stance that might get more of the unemployed back to work sooner? The Chief Economist gave us a little lecture about the neutral interest rate having fallen 3 basis points a quarter for the last decade, but whatever neutral is – and no one knows – there is no sign that keeping medium-term trend inflation near 2 per cent requires an OCR as high as it is now.

I was encouraged by one aspect of the Governor’s press conference. He seems to be becoming slowly more uneasy about the situation in China. In answer to one question he uttered the dreaded d word – deflation, observing that if there was a substantial depreciation of the yuan that would export deflation around the world. He actually sounded worried. Given that almost every emerging market currency has depreciated markedly against the USD in the last 12 months or so, and that the Chinese are rapidly running through their foreign reserves, he probably should be worried. But if he is worried, he should be doing some preparation, focusing on keeping inflation expectations up, and on removing the obstacle that the near-zero lower bound poses for monetary policy. We still have some way to go to get to zero, but that space is steadily diminishing, and if the Bank’s Statement of Intent is any guide, he is doing nothing pre-emptive about managing the risk.

I wonder how the Bank’s Board and the Minister of Finance feel about this Monetary Policy Statement. Is the Minister yet asking for advice from the Board and/or Treasury on just what is going on?