The coverage in recent days of the first (branded) KiwiBuild houses – one purchased by a young well-travelled couple, no children, she just graduating as a doctor, he something in marketing – brought to mind the books I’d had sitting on a pile for ages intended for a post about the first Labour government’s state house building programme (we used to be told that the KiwiBuild vision was modelled on the earlier programme).

As for the KiwiBuild houses themselves, even the purchasers are unashamed in talking up their good fortune (at the expense of the taxpayer).

The owners of one of the new homes have compared their purchase to winning Lotto.

Couple Derryn Jayne and Fletcher Ross paid $649,000 for their four bedroom home, which they said is great value for money, compared to prices elsewhere in Auckland.

They had given up hope of finding a house on the open market after a year-long search.

Which, frankly, is a bit odd. Of course house prices in Auckland – and much of the rest of the country – are obscene, but even in Auckland you can pick up a first house for well under $649000. I googled houses for sale in Clendon Park for example. It mightn’t be a suburb entirely to everyone’s taste but my in-laws lived there until a decade or so ago. And it is a first house we are talking about, where it isn’t obvious why the taxpayer should be assisting a lucky young couple into a brand-new four bedroom house.

Defenders of the government are quoted in the media. There is an article in this morning’s Dominion-Post (which I can’t find online) in which, for example, Shamubeel Eaqub notes that

…the eligibility criteria were broad. “People also may not know how challenging it is to be a doctor without a private practice and with large debts. I have heard stories of young doctors leaving places like Queenstown because they couldn’t see a way of ever owning a home there.”

Another person quoted in the article observes “even doctors have to start somewhere”.

No doubt. And no doubt it is quite tough for many people starting out, even professionally-qualified couples. But lets just think for a moment about people rather further down the income ladder, typically without the sort of future income advancement opportunities that (many) doctors have. Teachers and nurses for example, or motor mechanics, or retail managers, hairdressers, and so on. If we “need” special lotteries to help favoured young professional couples into homes, how are people further down the income scale ever supposed to manage? Ah, but, says the minister Phil Twyford, that is to miss the point: apparently KiwiBuild isn’t supposed to help low-income families, even though if there was ever a case for direct state intervention in the market it would surely be for those people rather further down the income scale; the sorts of people who not many decades ago could reasonably have expected to buy a basic first house.

An Auckland University economist (Ryan Greenaway-McGreevy) is also quoted in the article. He argues, sensibly enough, that “it shouldn’t be a surprise that a new doctor could qualify. ‘Perhaps it speaks to how unffordable housing has become.'”

Which is, surely, the point. Most people further down the income scale, and especially in Auckland, simply can’t afford to purchase a house at all, at least not without ruinously overburdening themselves. The economist goes on to suggest that KiwiBuild will lower prices for everyone. Even if that were true, it still wouldn’t justify a lottery in which the favoured few pick up a house below market price at the expense of the taxpayer. But, of course, there is little sign that it will be true – many of the early KiwiBuild projects are just rebadging construction that was already going to happen, and over time there is no clear reason as to why we should not expect any specific KiwiBuild construction not to displace private sector activity that would otherwise have taken place.

And surely the evidence against that optimistic hypothesis is in the market prices. If people really believed that whatever the government was doing – KiwiBuild or whatever – was going to lower house and urban land prices over time, then those prices would be dropping already, perhaps quite steeply. Sure, Auckland prices seem to have gone sideways over the last 18 months or so – after a huge surge over the previous few years – but those in many other urban areas are still rising (in both real and nominal terms). Over the last five years, the REINZ numbers now indicate that Auckland and non-Auckland house prices have risen at around the same rate (on average 8 to 9 per cent per annum). CPI inflation is, by contrast, averaging under 2 per cent. When nothing has been done to fix the land market, and most KiwiBuild construction is likely to simply displace private sector construction, none of that should be very surprising. KiwiBuild is producing photo-ops, and Lotto-like wins for the favoured (and lucky) middle class few, but it is no fix – not even any material part of a fix – to the dysfunctional housing market successive governments have delivered us.

And what of the first Labour government’s state-housing programme? Actually, it didn’t do a lot for people at the very bottom either. In the mid 1930s there was much talk of “urban slums”. Ben Schrader’s history of state housing in New Zealand has a nice quote from a newspaper editorial written just a couple of weeks after the 1935 election, contrasting the newly built National War Memorial Carillion tower with the surrounding neighbourhood (in Wellington’s Mt Cook)

“The Tower was built right in the middle of Wellington’s slum area, and a stone’s throw away from it, men, women, and children are making a different kind of sacrifice. They live in squalor and dirt, in little shacks lacking even the ordinary comforts of existence.”

But the state house programme wasn’t for these people. They couldn’t afford the rents. In fact, as Schrader records, one contemporary critic calculated that a worker would have to earn 20 per cent above “the weekly living wage (the amount the Arbitration Court determined was necessary to support a familiy in “reasonable comfort’) to be able to afford the rent on a state house. In its defence, Labour argued that people moving into state houses would free up other houses for poorer people – and in those immediate post-Depression years without the sort of tight land use controls we have today perhaps there was even something to that story (but I’m not aware of any evidence to confirm that conclusion). But it certainly wasn’t a programme targeted to help those at the bottom (indeed, when later governments offered to sell state house to sitting tenants there was often a material wealth transfer to the fortunate minority). And for the first decade or more Maori was also explicitly excluded. Again from Schrader:

“This thinking [around separatism] was challenged in 1944 after the Department of Native Affairs surveyed Maori housing conditions in the industrial Auckland suburb of Panmure. It found Maori crowding into tents and shacks made from rusting corrugated iron and discarded packing cases. Cooking was mostly done over open fires and sanitary conditions were primitive. Sobered by this and other similar reports, the government agreed in 1948 to build state houses for Maori.”

As for the photo-ops in an earlier age, everyone is familiar with the picture of Prime Minister Savage helping to carry the dining table into the first state house in Miramar, but Schrader records

“The Fife Lane function was so successful that a coterie of cabinet ministers repeated the furniture-carrying stunt at the opening of the first state house in each of the main cities.”

I wonder how more photos of Jacinda Ardern and Phil Twyford appearing with new KiwiBuild owners there will be? And how people further down the income scale – perhaps mostly Labour voters – will be feeling about their own prospects of ever owning a modest house (not even a four bedroom brand new one) in one of our major cities. That only seems likely if the government were to tackle the regulatory constraints on our urban land market, and despite the pre-election talk there is still as little sign of that so far as there was action under the previous government. Very little.

(On a completely different topic, I’d just add my voice to the long list of those seriously troubled by the government’s decision to give residency to an imprisoned Czech convicter of dishonesty, and convicted and imprisoned for drug importing, and not even to be willing to explain why. Personally, I can’t conceive any circumstances under which I would support giving such a privilege to a person with such a – very recent – background, the more so when such a person comes from an EU country – none of them is perfect, but none is Somalia or the People’s Republic of China. There are plenty of decent and honest people who would like to live here, and we only take so many: why favour the Czech drug smuggler over any of them? As with the extraordinary exercise of ministerial discretion under the previous government to grant Peter Thiel citizenship, these sorts of cases point to a need for much more openness and accountability. If you want ministers to exercise personal discretion in your favour, you should expect all the details of your case to be published routinely, so that ministers can be properly held to account. It simply isn’t good enough to have the Prime Minister tell us we should “read between the lines” and then refuse to go further. Why would we be inclined to believe that ministerial discretion is being appropriately exercised in this case – and that a drug smuggler with gang associations should be free to stay among us – when the track record (under both parties) inspires so little confidence?

I noted that there are plenty of decent and honest people who would be keen to live in New Zealand. Stuff’s new article on the utter failure of the Immigration New Zealand arm of MBIE to take seriously the scams suggests that many of those who do get to live here probaby do so at the expense of the honest and decent ones.

[head of immigration advisory agency Carmeto] Malkiat believed most visa applications contained some level of exaggeration and misrepresentation, and significant number involved substantial corruption. There was now a generational pattern of exploited migrants in turn exploiting the next wave to arrive, he said.

“The reality is that if all immigration advisers speak up, 80 to 90 per cent of all applications are wrong, and should not be approved – it is a massive number,” he said.

“Most of the industry exists because of fraud. If there was no fraud, many advisers and lawyers would leave the industry [because they wouldn’t be needed].”

It was clear Immigration NZ was not equipped to deal with the widespread fraud that it was encountering, Malkiat said.

Former immigration minister Tuariki Delamere, now an immigration adviser himself, said he too had sent tip-offs to INZ but seen no action. “I sympathise with that adviser [Malkiat] doing that. Senior [INZ] staff have said to me they are understaffed and there are so many [cases to investigate]. I sympathise with them … but I am happy you are exposing it because the only way you stop [these frauds] is by prosecuting them and publicising it.”

Lawyer Alastair McClymont said he “used to tell INZ about them all the time as well – but nothing ever happened”.

Immigration New Zealand declined to comment on the complaints about its service.

That final line says it all really. It is a disgrace. Whether through these immigration scams or the political donations process, Labour and National in turn preside over the increasing corruption of the New Zealand system. And yet their inaction – and silence – suggests they just don’t care. )

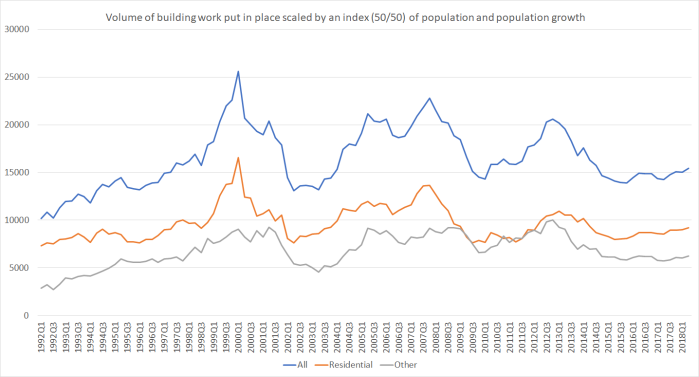

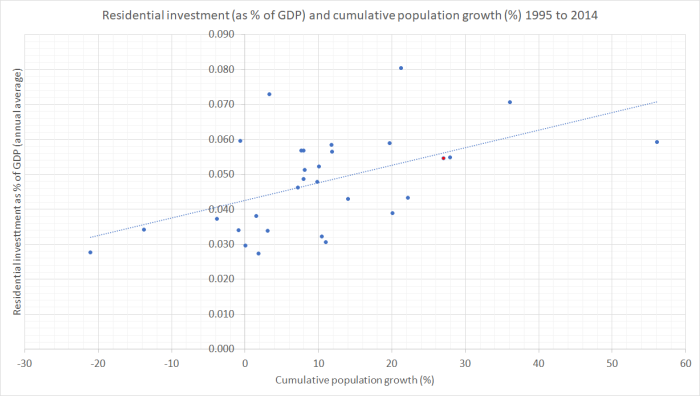

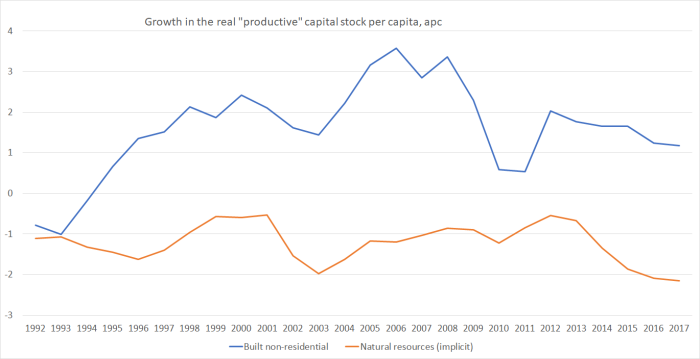

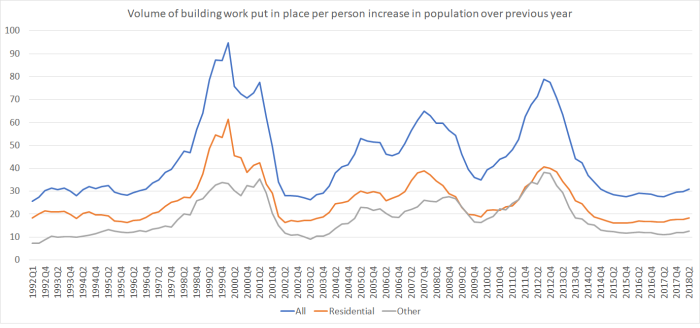

The peaks on this measure happen when population growth is at its cyclical troughs – unsurprisingly, since the normal base level of replacement and improvement work is still going on.

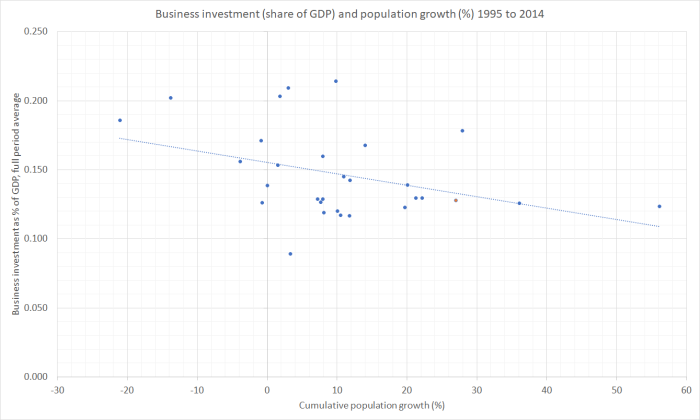

The peaks on this measure happen when population growth is at its cyclical troughs – unsurprisingly, since the normal base level of replacement and improvement work is still going on.