The Reserve Bank released its six-monthly Financial Stability Report this morning, followed a bit later by the Governor’s press conference. The FSR seemed to be mostly about laying the defensive groundwork for next Thursday’s announcement of the Governor’s final decision on minimum bank capital requirements. And the press conference was mostly pretty tame, the Governor having announced that he wouldn’t answer any questions on bank capital issues, and the assembled journalists having come quietly and not asked any. The Governor himself was mostly on his best behaviour again. It is to be hoped that the journalists get an opportunity to question the Governor seriously, and in an informed and open way, when the capital decisions have been announced and the year-overdue cost-benefit analysis has finally been released.

There was some discussion at the press conference about the Bank’s staffing for supervision. We were told that they now have 38 staff in that area, up by five, although they avoided answering the question of how many people they have assigned to each main bank. Asked about plans for further staffing increases, the Governor indicated they were planning on 30 more people, but he had to be hauled into line by his deputy who stressed that it was all contingent on how much the government agrees to allow them to spend in the forthcoming Funding Agreement. Count me just a little sceptical that there would be much marginal value, in terms of system soundness gains, from the 30th additional person, especially if (as we must) we assume the Governor is pushing ahead undaunted with his capital plans. It was one of the Governor’s own vaunted “independent experts” who wrote recently.

The RBNZ has adopted a principle of being conservative as regards bank capital to offset possible risks from its light-handed approach to supervision. That is a choice and one partly based on the view that having very large resources devoted to intrusive oversight of banks is not the most efficient road to go down. That is a conclusion that engineers and safety experts often apply when dealing with the design of structures. There is a choice between building bridges many times stronger than you expect them to need to be OR you having large teams of inspectors who pay frequent visits to examine all bridges and monitor flows of traffic over them. It is clear that nearly all countries follow the first strategy.

That may be a useful guide for bank supervision.

“Belt and braces” springs to mind.

The Governor told us he hadn’t been “particularly close” to easing the LVR limits, those restrictions first put in place – as avowedly “temporary” – more than six years ago. Now that the central bank has been delivered into the hands of enthusiasts for direct controls, facilitated by a government with not much belief in indirect instruments or markets, we must assume it would take something really rather severe to see the LVR controls lifted again. It has always reminded me of exchange controls – imposed in a hurry in 1938, finally fully lifted in 1984. But again, no one seems to have thought to ask whether there would not be an element of “belt and braces” about having binding LVR controls in place at the same time as – the already resilient (Governor’s words) banking system is facing a near-doubling of its minimum capital requirements. I guess enthusiasm for regulation begets enthusiasm for yet more regulation.

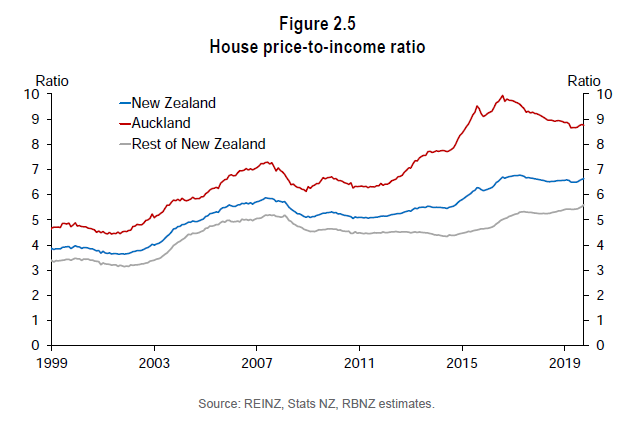

Remarkably, in the FSR the Bank claimed that there had been a “gradual reduction in housing market imbalances”. It wasn’t fully clear what they had in mind, but since those words appeared in the same (short) paragraph that featured a link to this chart, it appeared to be something about price to income ratios.

The price to income ratio might have fallen back in Auckland, but it has been continuing to increase in the rest of the country (taken together) and for the country as a whole a current ratio (estimated) of 6.64 is immaterially different from the peak of 6.78. Whether these are really “imbalances” – as distinct from equilibrium outcomes given land use restrictions – is another question.

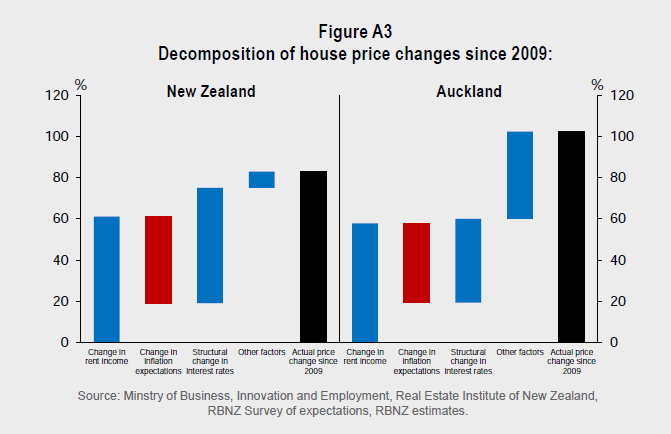

The Bank itself persists in minimising the importance of these fundamental regulatory distortions. In the FSR there is a box which attempts to address the question “How have lower long-term interest rates affected housing valuations?” It is an attempt to argue that low(er) interest rates themselves are a big part of what has gone on.

This is their main chart (in which it is a little puzzling why they start from 2009 – the depths of the recession/crisis – rather than, say, take a peak to peak approach).

Focus on the left-hand panel, for the entire country. (In these charts, blue bars are positive contributions and red bars negative ones.) It isn’t very satisfactory that they appear to have modelled nominal house prices rather than real house prices. It isn’t clear why they have done so, but (at very least) it appears to be convenient for them, enabling them to (claim to) show that lower interest rates are a big part of what explains house prices rises, when lower inflation expectations – an offsetting factor (in red) – would be expected to be fully reflected in lower nominal interest rates over a 10 year horizon. Taken together, the effect of real interest rates looks quite small.

Similarly, this highly reduced-form approach tends to imply that rents are an exogenous explanatory factor in house prices, and using nominal (rather than real) rents only compounds the problem. As I’ve pointed out here on various occasions, the sharp fall in real long-term interest rates should have been markedly lowering real rents over the decade – real rents should be more affordable than ever. Almost certainly it is the supply restrictions, interacting with unexpected population surges, that has driven up house prices, in turn driving up rents. Interest rates are, at most, a second order issue: had the OCR not been lowered in line with the fall in neutral rates then – all else equal – house/land prices would be lower, and the entire economy weaker.

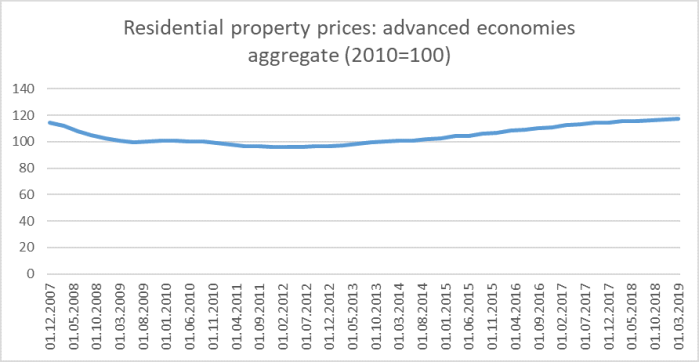

Perhaps an easier way to see the point is this chart, showing the BIS measure of real house prices for the advanced economies in aggregate.

Real and nominal interest rates have fallen a lot almost everywhere in the advanced world since 2007 (Japan excepted) and yet real house prices are barely higher now than they were in 2007. Lower interest rates do not explain high house prices, rising rents certainly don’t. The culprit here (and in Australia) is tight planning restrictions, the effects of which are exacerbated by rapid population growth.

There were a couple of other significant points in the document that caught my eye, consistent with my description of the document earlier as laying the defences for the capital requirement increases next week.

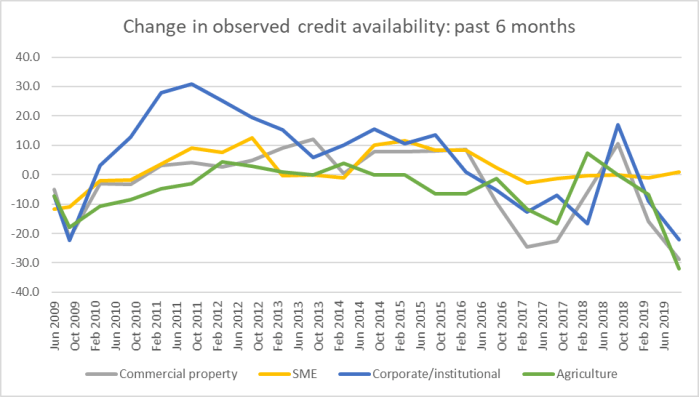

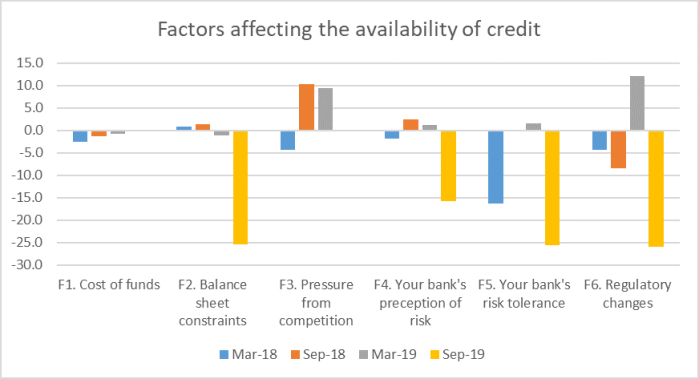

The first related to credit conditions. You will recall that the Bank recently released the results of its credit conditions survey. I wrote about them here. Across the various classes of business lending, actual credit conditions were reported to have tightened quite a bit, and conditions were expected to tighten further over the coming six months. And why? Well, this was the chart – from their own data.

“Regulatory changes” is explicitly identified as the biggest single factor – surely mostly the bank capital proposals – closely followed by “balance sheet constraints” and “your bank’s risk tolerance”, both which one would expect to be directly influenced by the expected change in capital requirements. And yet not a word of this made it into today’s FSR, presumably because it would have been a bit awkward or uncomfortable to have confronted it directly. (There were a couple of mentions of credit conditions, but none of the role their own policy proposals appear to have played.)

And then there were stress tests. One of the highly unsatisfactory elements of the way the Bank has tried to spin the case for much higher capital requirements is their reluctance to engage seriously with the results of various stress tests done this decade, all of which – no matter the shock – suggest that the banks come through in pretty good shape, in turn suggesting that (a) banks have plenty of capital and (b) bank lending standards in recent years haven’t been that bad at all. Typically the Bank waves its hands, suggests the stress tests might not capture things perfectly, and hurries on to another issue. But in this FSR they’ve come up with a new argument – not previously seen, at least as I recall it, in a year of consultation.

While the stress tests are calibrated to a severe downturn event, the Reserve Bank is seeking to ensure that the system will be resilient to even larger shocks.

Well perhaps, but the scenarios they’ve already tested seemed plenty demanding (and appropriately so). For example, a 4 per cent fall in GDP, a 40 per cent fall in house prices (and a 50-55 per cent in Auckland house prices) and an increase in the unemployment rate to 13 per cent. It is the interaction between lower house prices and higher unemployment rates that creates large mortgage losses.

There are few examples anywhere of house prices falling more than that (including in the crises – typically in fixed exchange rate countries – people like to quote), and as for the unemployment rate, I devoted a whole post to that a few years back, where I concluded that there was not a single example, across the entire OECD, where a floating exchange rate advanced economy had experienced an increase in its unemployment rate as large as was implied by the Bank’s stress test in the entire post-war era (now 75 years, across perhaps 25 market-based countries). The Bank seems to be wanting to prepare for a Greek crisis, or for a rerun of the Great Depression, without taking account of the stabilisation role monetary policy and a floating exchange rate now play in countries like New Zealand. Without a lot more open engagement on the sorts of risks they see, it is pretty tawdry stuff.

In the course of his press conference, the Governor took the opportunity to wrap himself around the recent reports of the foreign academics he’d hired to provide some comments on the Bank’s capital proposals, lamenting only that these “excellent”, “very positive”, “wholly independent of us” reports hadn’t had much local media attention “unlike some other views” (it wasn’t quite clear who he was having a dig at there, but perhaps Kate McNamara’s stories are still leaving a sting). Victoria University academic, and bank capital expert, Martien Lubberink was live-tweeting the Governor’s press conference and was moved to observe of these reports

I wrote about those reports in a post a few weeks ago, summarising

As I said at the start, for handpicked reviewers, chosen at a time when the Governor had already put his stake in the ground, the reports were much what one should have expected. The Bank seems to have taken the reports as reassuring support – but that is why they hired these particular people, known for particular predispositions – but I suggest you don’t. Many of the bigger picture questions simply haven’t been engaged with, adequately or at all.

(many of those bigger picture questions were rehearsed in the post)

and went on to conclude that there was a surprising absence from the reports (and from any Reserve Bank papers on the issue)

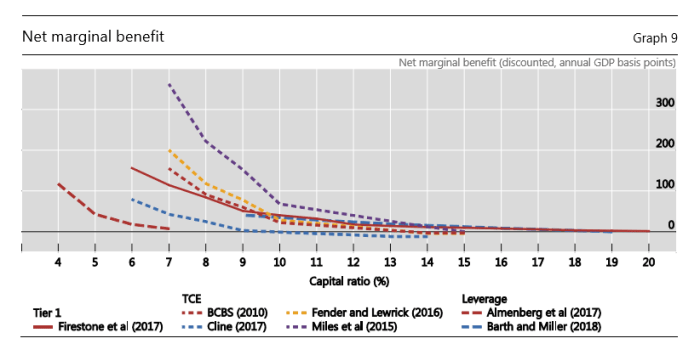

And, somewhat to my surprise, I didn’t see any mention at all of the paper that came out three months ago, from a working group of major central banks, looking at issues around appropriate minimum capital requirements, working within the academic framework these reviewers are comfortable with. I discussed that paper here and highlighted this chart and these issues

On my reading, this is the bottom line chart in the BCBS paper.

They report the net marginal economic benefit (slightly lower GDP each year, offset against savings from a less serious crisis decades hence) from higher bank capital ratios, drawn from a series of studies. On these models there were really big gains in lifting capital ratios, up to around to around 9-10 per cent. If there are gains at all – and they don’t report margins of error around these estimates – they are looking extremely small beyond about 13 per cent. Perhaps that doesn’t sound too far from the 16 per cent number the Reserve Bank is proposing for the big banks but (among other limitations, many made inevitable by data limitations):

- this modelling is done on actual capital ratios, not regulatory minima (a 16 per cent minimum ratio is likely to see banks aim for something between 17 and 18 per cent actual ratio), and

- none of this modelling takes account of differences in accounting and regulatory treatment across countries: conventional wisdom, (backed by estimates done by PWC) suggest that effective capital ratios in New Zealand (and Australia) would be far higher if things were measured the same way they were done in various other advanced countries, and

- none of it takes account of the regulatory floor in how risk-weighted assets are calculated. As the Bank is quite open about, a significant part of what is proposing is that in calculating risk-weighted assets, the big banks will have a floor of 90 per cent of what the standardised rules would generate (the more normal floor is, as I understand it, about 72 per cent). A 17.5 per cent headline actual capital ratio would, on RB proposed rules, be akin to something like 20 per cent in the sort of framework the BCBS authors are looking at.

Nothing in this paper suggests any reason for confidence that effective capital ratios of, say, 20 per cent of risk-weighted assets would be generating net economic benefits, even on the (overly pessimistic) macro assumptions the authors are using. But that is what the Reserve Bank claims to believe. The onus, surely, is on them to show us, and to engage on their assumptions and analysis – in open dialogue – well before decisions are made.

Neither in todays report nor in the press conference was a rigorous, open, accountable, excellent central bank of the sort we should expect on display. Perhaps it is too easy to become accustomed to this mediocrity. Perhaps that accounts for the not-very-searching questions at the press conference – nothing at all for example about the recent very public concerns about the Governor’s conduct over the bank capital proposals.

Next week all will be revealed. No one seems to expect any material departure from the initial proposal, even if there are a few cosmetic modifications, or adjustments to the transitional arrangements. Perhaps then we will get all the answers: really good and convincing cost-benefit (and associated sensitivity) analysis, serious engagement with the serious analytical points raised in submissions (rather than attempts to treat submissions as akin to a public opinion poll), a sustained narrative around transitional paths and risks in allowing material tightening in credit conditions when conventional monetary policy is almost exhausted, and so on.

Perhaps.