Yesterday afternoon we had the latest round of official comment from the Prime Minister and the Minister of Finance, at the post-Cabinet press conference (transcript here). It was really just more of the same. The Prime Minister, in particular, tends to play down the risks to New Zealand, and offers little effective leadership. Then again, the journalistic questioning didn’t seem very searching – no one, for example, asked about the rate at which Australian case numbers were growing and whether, with an open border and lots of travel (30000 arrivals a week from Australia) we aren’t really just in a Common Virus Area with Australia. “Wash your hands and carry on” seems to be the gist of her message – as, no doubt, it was for many of her overseas peers….until it wasn’t. There is still no pro-active discussion with the public about how the government is thinking of handling things just a little way ahead (do or don’t school closures play a part in their thinking, as just one example).

Much the same criticism can be mounted of their approach to the economic costs and dislocations, which will already be mounting by the day. There are signs – including in an RNZ interview this morning – of some greater degree of realism from the Minister of Finance, but he must be constrained in his public comments by the apparent political imperative to play things down, and focus on the China-related disruption rather than on the widening and deepening global situation, and the implications of that for New Zealand.

The Prime Minister and Minister of Finance announced the gist of the package of measures they will actually announce next week (the Minister’s statement is here). Even setting aside the lack of specifics, what they did announce still seems almost entirely backward-looking.

The Business Continuity Package includes:

- a targeted wage subsidy scheme for workers in the most adversely affected sectors.

- training and re-deployment options for affected employees; and

- working with banks on the potential for future working capital support for companies that face temporary credit constraints;

As if the biggest disruptions and dislocations are not still yet to be, and when they unfold their effects will be pervasive – almost every firm in the country will be hit to a greater or lesser extent.

Now, the Minister has said that he has officials working on longer-term options (and he is somewhat stymied by having a central bank – his Monetary Policy Committee – that isn’t doing its job). And that leaves me thinking that this “package” to date is as much about politics and being seen to be doing stuff – especially six months out from an election – as about a serious response to a worsening situation. Perhaps that is too cynical, but between Ministers and officials surely there is a recognition of what is near-certain to be, not far down the track?

It isn’t at all clear what sort of sensible dividing line the government has in mind for who is and isn’t going to be eligible (even now, won’t every business in Queenstown and Rotorua being feeling the effect?). “Training options” must have seemed like a good idea to someone, but if far-reaching social distancing is coming soon – as Siouxsie Wiles put it yesterday – it is hard to see polytechs etc effectively doing much of such training.

And, on the other hand, there seems to be no urgency around measures that might ensure adequate income support if/when we get to point where large numbers of people – across a whole range of sectors – simply can’t work (quaratined, self-isolated, or whatever) and their employers’ can’t afford, or won’t pay them.

Then, of course, there is what they won’t do

Media: ANZ’s chief economist says scrapping next month’s minimum wage increase in response to coronavirus is a no-brainer. Are you considering that?

Robertson: No.

PM: No.

Media: Will you consider it at all?

Robertson: No.

PM: I think, in fact, one of the benefits that we have—perhaps relative to other economies—is not only are we well placed in terms of low debt; our position around surpluses, the upgrade package, so that stimulus already going into the economy. Also we have to keep in mind what we need people to keep doing, of course, is continue to spend and consume. And so also the adjustments we’ve already had to benefits, and I would say, of course, what people are anticipating in their wages, is all part of continuing to keep the economy ticking over.

So they might a good talk about maintaining labour market attachment, but they won’t even consider postponing the next minimum wage increase. Minimum wage increases tend to have their most visible effects in downturns, amplifying the difficulty marginal new entrants and less-able workers have in getting (back) into a job. As I say, so far the economic policy response looks more like politics.

The one bit of the ‘indicative package’ that was new was this

- working with banks on the potential for future working capital support for companies that face temporary credit constraints;

That seems to be all we know for now.

But there is likely to be a significant issue there, one which is likely to get much bigger quite soon.

Hamish Rutherford has a piece in the Herald about this, drawing in part on a chat we had late yesterday. I suggested that one option officials might have in mind could be some sort of guarantee scheme. As far as we know, banks themselves don’t currently face funding constraints, so there shouldn’t be any need for direct government lending. But banks will become increasingly uneasy about continuing to extend new credit – increased overdrafts etc – to firms that already have a lot of debt, and where it isn’t clear when (or even if) normality in business conditions and cash-flows will resume.

One other reason why we really don’t want direct government lending is that government (Treasury, Reserve Bank or whoever) has few or no credit evaluation capability, and even less so in extremely uncertain unsettled times. If something is going to be done along the lines the Minister suggests, it needs to harness the interests and expertise of the banks themselves, who actually know about the businesses – and key individuals – they’ve been lending to.

I drew some parallels with the guarantee schemes the government put in place – supported by the Bank and Treasury – in 2008/09 for financial institutions. The retail deposit guarantee scheme generated a great deal of controversy, but the wholesale guarantee scheme – designed to help banks tap international markets – was pretty well-designed (in my view, but I was the principal designer): we didn’t guarantee what didn’t need guaranteeing, and we charged a fairly significant price to banks using the guarantee to ensure they had incentives to graduate from it as soon as possible. Broadly speaking, they were sensible interventions. But it is important to remember the context. Officials and ministers were pretty confident of the credit standing of New Zealand banks – finance companies were a different issue – (and, where relevant, Australian parents) – we were providing guarantees into an environment where the credit quality of those we were dealing with wasn’t materially impaired, but rather global funding markets had dried up almost indiscriminately. For what it was worth, we could also cross-check our judgements with market pricing – CDS spreads – and with the views of external ratings agencies.

None of that is on offer if the goverment is serious about taking on business credit risk now. Few New Zealand companies are externally rated, few have quoted CDS spreads. Most just are not that big or (their finances) visible to anyone much other than their banks and owners. And, of course, in many cases it would be the riskiest credits that banks would be looking to the government to support, creating major incentive and monitoring issues. For a firm that has next to no debt and substantial physical assets, support from their own bank isn’t likely to be much of a problem for some considerable time. But for the firms that were straining the tolerance of their bankers anyway, why would it be attractive for the government to take the risk? Most firms will be somewhere in the middle, but remember that those with the higher current debt levels and those now bleeding cash fastest will be the ones eyeing up the possibilities of government support. I really wish officials well trying to devise something workable, sensible – oh, and scalable when things get a lot worse.

(I haven’t really touched on the Reserve Bank’s new capital requirements. They will be accentuating the difficulties borrowers face this year, exactly as the Bank was warned in consultation last year – whack on large new capital requirements with the likelihood of a severe downturn in the next few years and you will materially exacerbate problems, when there are few other effective tools.)

On matters re the Reserve Bank we are to get from the Governor this afternoon some thoughts on how the Bank might approach non-traditional monetary policy when/if the limits of the OCR are reached. No doubt I will write about that material in the next few days, but in meantime as reference here is link to my post about an article the Bank published on the issues and options the Bank published a couple of years ago.

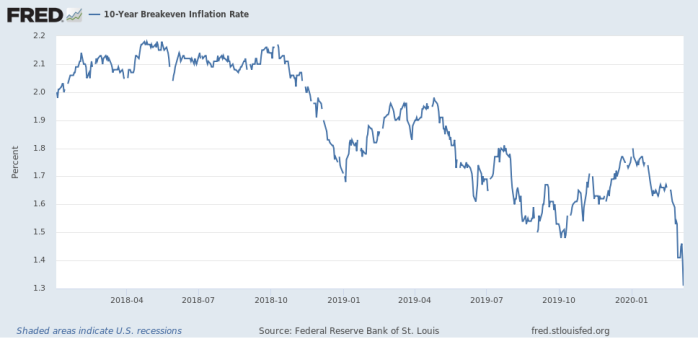

And finally, inflation expectations. I’ve been making the point that there really isn’t a great deal economic policy can do to limit the immediate costs and dislocations over the next few months, and that the focus should really be on getting in place early and decisively policies that will support a recovery as rapid as possible. Part of that – and a theme of mine throughout the life of this blog – has been avoiding any sharp slippage in inflation expectations, which risks “trapping” economies in a very difficult position even after the worst is over, given the current limitations on monetary policy. Real interest rates could be rising, not falling – and in the current environment it is probable that real retail rates should be zero or even negative. I’m sure all that seems quite abstract to many readers, so I wanted to end with a couple of concrete illustrations of the risk.

In this chart I’m sure the breakeven inflation rate for US government 10 year bonds (gap between yields on conventional and indexed bonds) as at the US close this morning.

These aren’t record lows, but the implicit expectations are much lower than they were averaging just a few months ago. Much of last week’s 50 basis point cut, simply stopped real interest rates moving higher. Now, sure, in tense periods these indicators can be thrown around changing (unobservable) risk premia, but this isn’t a time for complacency, when everyone knows there are severe limits to what more central banks can do. Rational agents will be revising downwards their future expectations, and to the extent they do that poses big risks – accentuating the deflationary climate that has been building for more than a decade now, not just in the US but throughout the advanced world.

What about New Zealand? This chart simply shows the gap between the Reserve Bank’s 10 year bond data and the yield on the September 2030 indexed bond. The latest observation is as at yesterday, but New Zealand 10 year bond rates don’t seem much changed this morning.

The recent movement isn’t as dramatic as for the US but (a) the starting level – not much above 1 per cent – was far too low already, and (b) the direction is clear, and concerning.

We need a much more pro-active central bank, doing its core job.

(In closing, it is curious to reflect that the biggest single form of stimulus to demand/activity in New Zealand since coronavirus become prominent is the spat between Mohammed bin Salman and Vladimir Putin and the resulting collapse in world oil prices. Who knows how large the stimulus effect will be – or how significant any countervailing havoc wreaked on, eg, US corporate credits – but whatever the effect it is larger than anything/everything our goverment and central bank have done.)

We can only hope Covid 19 is a short-term emergency. Perhaps as temperatures warm in the northern hemisphere it will begin to taper off, although of course we will be going into our winter here so if the disease gets a grip we may well be affected for months to come. As you point out, “training” is an unlikely solution. When it only takes one unprotected sufferer to put over 40 medical staff out of action, who would fancy their chances when mingling with classes of trainees day after day? Hopefully the fall in oil prices will provide some stimulus. Even so there would seem to be a case for slashing GST to assist low income earners and the newly unemployed in particular. I hope we are coordinating closely with Australia because, as you point out, we are pretty much a common area thanks to the Trans Tasman Travel Arrangement, and our major banks’ parents are located there too. But perhaps Ardern’s thoroughly rude theatrics in Sydney a week or so ago have put the kibosh on that.

LikeLike

Unfortunately the virus seems to have removed Jacinda’s standard response to a crisis – a hug, followed by thoughts and prayers of course. So it is no wonder she is finding things difficult.

Not that Simon, if in power, gives any indication he would be much better. Perhaps it is a time where age and experience would be useful.

The election is likely to be a hindrance as both sides try to score points rather than any attempt to find a joint way through the coming months.

LikeLiked by 2 people

I think Simon Bridges have understood very well that Labour has overstepped the boundary with the heavy handed approach to regulation. Property Investors have been unfairly targeted by a fascist communist Labour government approach, also criminalising watching Youtube videos, having semi automatics in your personal possession and being a landlord. Frightening.

I would say well done Simon Bridges. The aim should be to repeal every legislation that Labour has put in. Kris Faafoi should also be removed from parliament to put up such extremist fascist communist legislative measures against landlords.

LikeLike

Oh, I think we know the difference in a crisis situation. Getting hugged by Jacinda would be an odd but probably comforting experience; by Simon, not so much (more creepy/oompa-loompa)

LikeLike

I don’t think hugs are recommended by Health Officials at this time. No wonder Jacinda Ardern looks uncomfortable now that she has lost her only public relations attribute. After watching a fun Youtube on new greetings, I have started kicking shoes as a greeting these days instead of hugs and handshakes.

LikeLike

[…] “The prime minister, in particular, tends to play down the risks to New Zealand,” Riddell wrote. […]

LikeLike

[…] “The prime minister, in particular, tends to play down the risks to New Zealand,” Riddell wrote. […]

LikeLike

[…] “The prime minister, in particular, tends to play down the risks to New Zealand,” Riddell wrote. […]

LikeLike

Michael, credit exploded yesterday. High yield, cross-over, leveraged loans and EM debt all came under severe pressure. Bank funding costs are rising, we can see that clearly in places like Australia where BBSW-OIS is widening. And the big Aussie bank stocks are all down heavily.

So we know that bank funding conditions are deteriorating. Add to that the RBNZ capital review and falling commodity prices and banks will have zero tolerance to support business.

They will issue platitudes and use their marketing departments to butter up the only 2-3 journalists they need to, but they’re gonna be hard-nosed in dealing with customers.

We have a global issue of trust here. Trust in our medical systems, our politicians and agencies; which is why we have runs on supermarkets. Credit is about trust, and it’s being tested which is a big risk to us given our debt load and rollover risk.

LikeLike

Thanks Peter. Do you happen to know what has happened to Aus bank CDS spreads?

(Unfortunately when I wrote the brief mention of funding I just took the press statement yesterday from the RBNZ and NZBA at face value. More fool me.)

Generally agree about trust. At a political level it is hard to see who in the West deserves trust re the handling of this.

LikeLike

No sorry. I didn’t sign on to the permissions for that on Bloomberg as they’re pretty expensive. Sovereign CDS hasn’t done much and I’m guessing that bank CDS hasn’t done much either. TBH, people don’t really trade CDS much these days from what I can see. But I can see BBSW and OIS and that’s been widening.

Combination of widening funding indicators LIBOR-OIS and plunging bank stock and other partial indicators like HYG, JPEIPLSP are all very correlated to NZD and suggest credit stress has really blown out in the past 3-4 days.

LikeLike

Thanks Peter. I did see an FT piece saying that CDS spreads for JPM (and from memory other big banks) had increased by up to 50 per cent on Monday, but that seemed to be partly in the context of energy exposures, so not clear how much would spillover to Aus banks.

LikeLike

Banks are flush with liquidity and as a result banking costs are rising. The problem is they can’t get that liquidity out to lenders fast enough. This is the unintended consequence of the Australian Royal Commission in banning performance targets in lending for bank employees. It is incredible how lazy bank staff have gotten these days. They just sit on a loan application these days for months before deciding to action. If it looks like too much work it gets a rejection after sitting months on someones desk just to show they are doing something.

This is not about the lack of trust. This is about a logistical blockage. You can’t make make a profit by sitting on a pile of cash.

LikeLike

Correction: The banks can’t get that cash liquidity out to borrowers fast enough.

LikeLike

Adrian says firmly that he understands what’s going on.

Well, If he does, he’s the only one in the world it seems… and it would be wonderful if he could enlighten us.

At present, all he’s said is “trust us” and “our economic fundamentals remain sound”; this is pretty much what Andrew Mellon and Herbert Hoover told Americans in 1929…

LikeLike

So far Adrian Orr has made all the right calls. He did drop interest rates by a surprise 50 basis points way before anyone else. You can call that foresight or lucky. He does not need to drop now because he has already dropped the OCR way before any other Central Bank did.

I did think that was rather aggressive and it has certainly ignited the property market and boosted confidence in that sector. Any more interest rate drops and we will have house prices running at 20% per annum increments which even property investors like myself do not want. Slow and steady. No panic, steady as she goes is the right response

LikeLike

Isn’t the opinion amongst a number of economists that post the GFC most advanced economies have too many ‘zombie’ firms? (Particularly Europe but I assume that New Zealand would also fit this description to some degree)?

Shouldn’t this current crisis (as hopefully a short, sharp shock) be viewed as a good opportunity to clear them out? (For the greater good of course).

I can’t see dynamism ever returning to our societies/economies if there is always support of some kind to see things through.

LikeLike

I’ve never been fully convinced by that story, but there is an important distinction between bailing out individual firms – which i’m generally v wary of (and would oppose, say, bailing out Air NZ if it comes to that) – and support the wider economy towards full employment, which will tend to benefit firms as well.

LikeLike

Thanks.

I appreciate that in your commentary that you have been proposing measures that are as broad and macro as possible. But it would seem as though (per your points above) that the government is currently focused on targeted micro initiatives that is not too far off bailing out individual firms – surely this is something a classic conservative opposition would be against but I have yet to see any sign that National have any alternative proposals.

Isn’t this approach the worst kind of policy making? Administratively complex, potential to favour (perhaps by design?) the ‘right’ political constituencies and likely low RoI (relative to other opportunities for the government to provide support?)

Perhaps this is yet another example of the whittled down public service not being up to task. Alternatively per your assertion it is entirely driven by politics.

That being said there have been some worthwhile policy initiatives implemented during previous crises that have become permanent policy settings.

What (if any) policy changes do you believe would be worthwhile implementing now that would be both beneficial for firms navigating the current crisis, and for their recovery and performance in the long term?

LikeLike

I think we have to face a degrading of our political establishment and our key bureaucratic institutions. The PM seems to have no real clue, the Governor of the RB is profoundly unserious, and the new Secy to the Tsy knows little about NZ and has no prior experience in national policymaking. And as you suggest the Nats seem no better.

Culmination of 20 years of decay, then exposed in a crisis.

Will have to think about your final question. Might comment further tomorrow.

LikeLiked by 2 people

[…] “The prime minister, in particular, tends to play down the risks to New Zealand,” Riddell wrote. […]

LikeLike

[…] “The prime minister, specifically, tends to minimize the dangers to New Zealand,” Riddell wrote. […]

LikeLike

I see the Prime Minister has overnight decided the two major gatherings planned for this weekend, the Pasifika Festival in Auckland and the Christchurch mosques’ shootings memorial in which she herself will be involved, should proceed. Meanwhile we also learn this morning that in Italy deaths have soared to over six hundred – over two hundred in the last 24 hours – while the country has entered lock-down with all major events cancelled. More than ten thousand are said to be infected which suggests the mortality rate is very high. An Italian expert warned on the BBC news earlier this morning that the spread of the disease is “exponential”, starting with a handful of cases and racing away into the thousands in a matter of days. They advised others to learn from Italy’s experience while there is still time. It seems to me therefore that proceeding with these large gatherings this weekend is extremely unwise. The government should be leading by example through its own behaviour. This would now seem to be our last window of opportunity to head off the spread of the disease.

LikeLike

Never mind that members of the Muslim community said that memorials of tragedies aren’t their way: “why would we want to remember such an event” I recall one saying, or something similar.

LikeLike

I entirely agree. Even if she covered herself with formalistic advice from MoH, now is the time for some leadership from here, which would signal to others to start cancelling big events etc. As I was pointing out on Twitter, the Australian numbers are themselves exponential (doubling every 6 days or so) and with an open border and 30000 arrivals a week (normally) from Aus, we have to think of ourselves as in a Common Virus Area with Australia. The Premier of Victoria was yesterday talking about fairly extreme responses being not far away in Aus. Meanwhile here MOH was still sending out tweets last night saying the risk is low, no need to stock up on groceries, and – in essence – wash your hands and all will be well.

Three weeks ago Italy had 4 confirmed active cases.

LikeLike

I found much to disagree with in today’s NZ Herald opinion piece by Stuart McCutcheon “Coronavirus travel bans unjustified, discriminatory”

https://www.nzherald.co.nz/opinion/news/article.cfm?c_id=466&objectid=12315315

Although it is not a refutation of his argument I did wonder if he would have written it if 12,000 students from China were not involved.

The arguments I have with the article are:

1. In general it makes sense for NZ to align its bans with Australia – as he says staying in lockstep.

2. WHO states travel bans temporarily delay the onset of outbreaks – buying time is just what we need. Just a few days delay will permit more training for health workers, more resources stockpiles, new lessons learned from other countries.

3. He claims anecdotally people are already arriving here from China via 3rd countries. If they have been outside an infected area for 14 days then they have had their quarantine. Alternatively the prof is assuming his Chinese studentts are dishonest and will lie to immigration officers on arrival.

4. Travel bans increase the perceived threat of a disease and heighten discrimination and stigmatisation – at present what NZ needs most is to get the public to perceive the threat. The incidents of discrimination against people of Chinese appearance will have been reduced by the travel ban since the public can be fairly confident that the Chinese and Koreans we meet in public places (I live in Auckland North Shore) have not just arrived from a infection zone.

5. He claims it is illogical that we allowed in 9,000 returning Kiwis. However if citizenship of a country means anything it surely means access so I cannot see how our government had a choice. Surely it is easier for our authortities to check on 9,000 cases of self-isolation than to add another 12,000 students who in the main can access their studies online (assuming our universities are up to speed).

6. His references to “small island developing nations” and popularist leaders did not help his argument.

A travel ban is always going to be controversial – should it have been applied earlier or later, how long will the ban last, etc. Probably our govt did the right thing. It was necessary discrimination against a disease not an ethnic group or a country; it would become that if we permit travellers from Iran and Italy and Korea while banning Chinese. Judging by the reducing number of reported cases it is quite possible the ban on Chinese residents may be lifted long before bans on various EU countries.

LikeLike

Haven’t read that piece yet. However I am wondering if now there is anything much to be gained by maintaining the China travel ban (for us or Aus). Suspect we should either close the borders – Israel style, 14 days isolation for everyone – or, in step with Aus, consider lifting the China ban. For now, they have clearly got on top of the virus and are no longer the main source of risk. My bias, for what it is worth, is that closure of borders is probably too late, and the bigger issue is going to be domestic social distancing.

As it happens, in the current climate I can’t see too many being keen to travel anyway,

(I’m sure McCutcheon is right about the small number of Chinese students going via 3rd countries – it has been actively promoted by some universities in Aus)

LikeLike

I don’t see how we can trust Chinese reporting on the disease given the nature of that regime and their track record so far. It is far too early to relax any precautions. We are in the lull before the likely storm. Anything we can do now to mitigate its impact on the health of New Zealanders must take priority.

LikeLike

It is a hypothetical anyway, since we would have to act with Australia. I guess my point is really that far more cases are now being exported from Italy – and soon the rest of Europe and the US – that we don’t gain anything much from keeping the China-specific ban on, and gratuitously upset the Chinese (and as you know I’m only too happy to have us upset them for real distinctive threats).

We do seem now to be at the point where we block everyone – 14 day quarantine for any arrival, as Israel has done – or we simply have to fall back on the extreme social distancing, as the Italians are doing, the South Koreans have done, and (mainly privately) Sing, HK, and Taiwan have done. Even then it may only spread out the infection rate, but that will save lives, and the horrors of eg Italian hospitals right now (better – including more ICU beds per capita – than our health system in normal times).

LikeLiked by 1 person

Now that most of the political dissidents have been killed off as viral infected deaths, the viral infection death rate is bound to fall. The drastic city lockdowns and isolation is bound to have the desired positive benefit of reducing the transmission rates anyway. No one can doubt that those are rather extreme effective measures but more likely an excuse to regain political control rather than from any viral infection.

LikeLike

Reblogged this on The Inquiring Mind and commented:

A thoughtful post, Michael Riddell makes some very pertinent points.

LikeLike