Yesterday I dug out some discussion notes I’d written while I was working at The Treasury during and just after the last New Zealand recession. One of them – written in June 2010, already a year on from the trough of the global downturn (although as the euro-crisis was really just beginning to emerge) – had the title “How, in some respects, the world looks as vulnerable as it was in 1929/30”. The point of the “1929/30” was that the worst of the Great Depression was not in the initial downturn from1929 – which, to many, seemed a more-or-less vanilla event – but from 1931 onwards. It was only a four or five page note, and went to only a small number of people outside Treasury/Reserve Bank, but in many respects it frames the way I’ve seen the last decade, capturing at least some of issues that still bother me now, and lead me to think that – faced with the coronavirus shock – macro policymakers should err on the side of responding aggressively (monetary and, probably, fiscal policy).

The more serious event – akin to the 1930s – didn’t happen in the last decade, at least outside Greece. At the time, much of the focus of macroeconomic policy discussion – including in New Zealand – was around ideas of rebalancing and deleveraging. My note pointed out that, starting from 2010, it was very difficult to envisage how those processes could occur successfully over the following few years consistent with something like full employment. To a first approximation it didn’t happen. There was fiscal consolidation in many advanced countries, but not material private sector deleveraging. In most OECD countries it took ages – literally years – to get the unemployment back to something like the NAIRU. And, of course, there was a huge leveraging up in China. In much of the advanced world investment remained very subdued.

There were twin obstacles to getting back to full employment. On the one hand, short-term policy interest rates in many countries had got about as low as they could go. And on the other hand there was a view – justified or not – that fiscal policy had done its dash, and whether for political or market (or rating agency) reasons, further fiscal stimulus could not be counted on (even in a New Zealand context: I found another note I’d written a year earlier just before the 2009 Budget, which noted of “scope for conventional market-financed fiscal easing” that “our judgement – more or less endorsed by the IMF and OECD – is that we are more or less at that point [scope exhausted]”.

The advanced world did, eventually, get back to more-or-less full employment. But the world – advanced world anyway – never seemed more than one severe shock away from risking dropping into a hole that it would be very hard to get back out of. The advanced world couldn’t cut short-term interest rates by another 500 basis points. For a time that argument didn’t have quite as much force as it does now – when excess capacity was still substantial one could tell a story about not being likely to need so much policy leeway next time – but that was then. These days we are back starting from something like full employment. There was also the idea of unconventional monetary policy instruments: but while some of them did quite some good in the heat of the financial crisis, and in the euro context were used as an expression of the political determination to hold the euro-area together come what may, looking back no one really regards those instruments as particularly adequate substitutes for conventional monetary policy (limited bang for buck, diminishing marginal returns etc). And then there is fiscal policy. Few advanced countries are in better fiscal health than they were prior to the last recession – and New Zealand, reasonably positioned as we are – is not one of the few, and the political/public will to use huge amounts of fiscal stimulus for a prolonged period remains pretty questionable.

Oh, and there is no new China on the horizon willing and able to have its own massive new credit/investment boom – resources wisely allocated or not – on a global scale to support demand elsewhere.

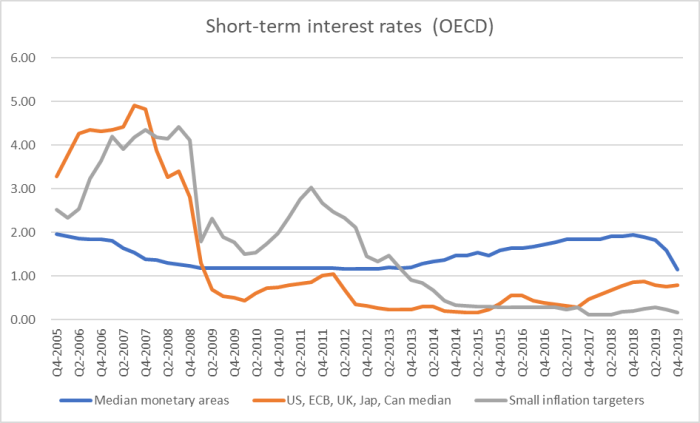

How about that monetary policy room? Here are median nominal short-term interest rates for various groupings of OECD countries.

You can see where we are 10 years ago. Across all the OECD monetary areas (countries with their own monetary policy plus the euro-area) the median policy rate is about where it was then (of the two biggest areas, the US is a bit higher and the euro-area a bit lower). Same goes for the G7 grouping. And as for “small inflation targeters” (like New Zealand) those countries typically have much less conventional monetary policy capacity than they had in 2010 (New Zealand, for example, had an OCR of 2.75 per cent when I wrote that earlier note, and is 1 per cent now).

Back then, of course, the conventional view – not just among markets but also to considerable extent among central banks – was that before too long things would be back to normal. Longer-term bond yields hadn’t actually fallen that far. Here are the same groupings shown for bond yields.

One could, at a pinch, then envisage central banks acting to pull bond yields down a long way (and with them the private rates that price relative to governments). These days, not so much. Much of the advanced world now has near-zero or even negative bond rates. A traditionally high interest rate country like New Zealand now has a 10 year bond rate around 1 per cent. Sure those yields can be driven low, but really not that much if/when there is a severe adverse shock.

And 10 years ago if anyone did much worry about these sorts of things – and there were a few prominent people – there was always the option of raising global inflation targets. In the transition that might have supported demand and getting back to full employment. In the medium-term it would have meant a higher base level of nominal interest rates, creating more of a buffer to cope with the next severe adverse shock. It would have been hard to have delivered, but no country even tried, and now it looks to be far too late (how do you get inflation up, credibly so, when most of your monetary capacity has gone, and it would hard to convince people – markets – of your sustained seriousness).

My other point 10 years ago in drawing the Great Depression parallels was that the Great Depression was neither inevitable nor inescapable. But it happened – in reality it might have taken inconceivable cross-country coordination to have avoided by the late 1920s – and it proved very difficult (not technically, but conceptually/politically) to get out of. The countries that escaped earliest – the UK as a prime example – did so through a crisis event, crashing out of the Gold Standard in 1931 that they would have regarded as inconceivable/unacceptable only a matter of months earlier. For others it was worse – in New Zealand the decisive break didn’t come until 1933, and even then saw the Minister of Finance resigning in protest. If we get into a deep hole in the next few years – international relations generally not being at their warmest and most fraternal, domestic trust in politicians not being at its highest – it could be exceedingly difficult to get out again. Look at how long and difficult (including the resistance of central banks to even doing all they could) it proved to be to get back to full employment last time.

In the Great Depression one of the characteristic features was a substantial fall in the price level in most countries. The servicing burdens of the public and private debt – substantial in many countries, including New Zealand/Australia – escalated enormously, and part of the way through/out often involved some debt defaults and debt writedowns.

Substantial drops in the price level seem unlikely in our age. Japan, for example, struggled with the limits of monetary policy and yet never experiencing spiralling increases in the rates of deflation (of the sort some once worried about). But equally, inflation expectations ratcheted down consistent with the very low or moderately negative inflation, meaning real interest rates were never able to get materially negative. Japan at least had the advantage that in the rest of the advanced world, nominal interest rates and the inflation rate were still moderately positive.

That could change in any new severe downturn. A period of unexpectedly weak demand, with firms, households and markets all realising that authorities don’t really have much useable firepower, could see assumptions/expectations about normal rates of inflation dropping away quite sharply (in New Zealand they fell a lot, from a too-high starting point, last time round, even with unquestioned firepower at our disposal). In that scenario, authorities would struggle to lower real interest rates at all for long – falling nominal rates could quite quickly be matched with falling inflation expectations. As people realise that, it becomes increasingly hard to generate a sustained recovery in demand, and very low or negative inflation risks becoming entrenched. It isn’t impossible then to envisage unemployment rates staying very high – unnecessarily and (one hopes) unacceptably high – for really prolonged periods (check the US experience in the 1930s on that count). An under-employment “equilibrium” brought by official negligence is adequately dealing with the effective lower bound on nominal interest rates.

I cannot, of course, tell if the current coronavirus is that next severe adverse shock. But it looks a great deal as though it could be, and the risks are sufficiently asymmetric – not much chance of inflation blowing out dangerously – that we shouldn’t be betting that it won’t be. Some people argue that since the virus will eventually pass for some reason it isn’t as economically serious as other shocks. That seems wrong. All shocks and recessions eventually pass – many last not much more than a year or two – and the scale of disruption, and reduction in activity, we are now seeing (whether in the New Zealand tourism and export education industries, or much more severely in northern Italy, Korea and the like) has the potential to markedly reduce economic activity, put renewed downward pressure on inflation and inflation expectations (we see the latter in the bond market already), all accompanied by a grim realisation of just how little firepower authorities really have, or are really politically able to use. (Ponder that G7 conference call tomorrow, and ask yourself how much effective leeway the ECB has now, compared to 2007, or even 2010. )

Against that backdrop, it would seem foolhardy now not to throw everything at trying to prevent a significant fall in inflation expectations, by providing as much support to demand and economic activity as can be done. That means monetary policy, to the extent it can be used – in New Zealand for example, a central bank that was willing to move 50 points last August, on news that was weak but not very dramatically so, should be champing at the bit to cut at least that much this month. The downside to doing so, in the face of a very real threat to norms around inflation – and a likely material rise in unemployment – is hard to spot. And since everyone knows monetary policy has limited capacity – and those who haven’t realised it yet very soon will – we need to see fiscal policy deployed in support, in smart, timely, and effective ways. In some countries it is really hard to envisage that being done well – the dysfunctional US in the midst of an election campaign, starting with huge deficits – but there really is no such excuse in countries such as New Zealand and Australia. (Oh, and of course – and after all these years – something needs to be done decisively re easing the effective lower bound.)

(There is, of course, widespread expectations of a huge Chinese stimulus programme. That is as maybe, although it will bring both its own risks – domestic ones just kicked a little further down the road – and the risk of new immediate dislocations, including the possibility of a significant exchange rate depreciation, exporting (as it were) deflationary pressures to the rest of the world.)

We are only one serious adverse shock away from a very threatening economic outlook, where the limits of macro policy would mean it would be difficult to quickly recover from. By the day, the chances that we are already in the early stages of that shock are growing. Perhaps it will all blow over very quickly, and normality resume, but (a) even if that very fortunate scenario were to eventuate, the risks are asymmetric, and (b) we’d still be left sitting with very low interest rates and typically high debt, one serious adverse shock away from that hole.